On Tuesday, Tesla’s (NASDAQ:TSLA) stock suffered a catastrophic double-digit decline in the first trading session of 2023 on the back of weaker-than-expected delivery figures for Q4 2022. Going into this Production & Delivery report, investors and analysts had high expectations due to –

Tesla’s CEO, Elon Musk, hyping up Q4 as an “EPIC” quarter during their last earnings conference call and repeatedly making such comments on Twitter.

Heavy discounting activity from Tesla towards the end of 2022.

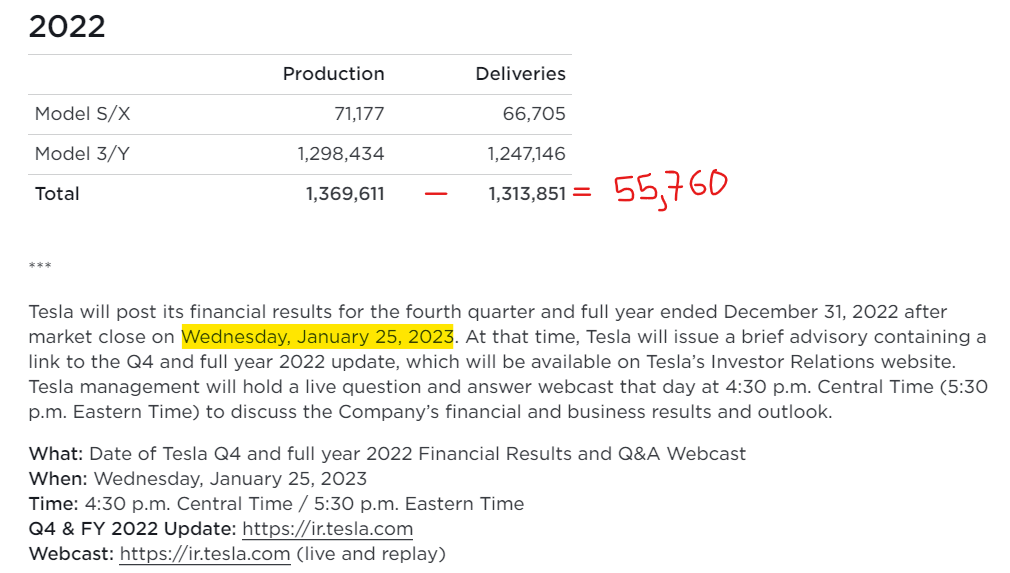

In Q4, Tesla delivered a record ~405K vehicles (vs. consensus estimate of ~427K vehicles). While +40% y/y growth in vehicle deliveries for 2022 in the current macroeconomic environment is quite robust, this figure fell well short of management’s delivery guide of “slightly below 50%“.

Tesla Investor Relations

Tesla Investor Relations

Now, a ~5% delivery miss in isolation doesn’t mean much to Tesla’s long-term fundamental growth story; however, the growing difference between production and delivery figures are raising demand and inventory concerns.

Given the current macroeconomic conditions, I would happily accept 40% y/y growth. However, Tesla’s heavy discounting towards the end of Q4 gives me good reason to take a pause and re-evaluate my investment thesis.

Despite executing two price cuts in December, Tesla failed to meet management’s delivery guidance by a significant margin. Just imagine where Tesla’s delivery figures may have landed without those discounts! Now, your guess is as good as mine, but I think we can agree that Q4 deliveries would have been lower than 405K if Tesla did no discounting activity in December. If the macroeconomic environment continues to worsen, Tesla is more than likely to under-deliver in 2023.

In my view, Mr. Market has been pricing in a sales growth slowdown and profit erosion (due to discounting) for 2023 into Tesla’s stock through the ongoing capitulatory sell-off. From a near-term perspective, Tesla’s recent price action makes sense. However, the long-term fundamentals for Tesla have never been stronger, and if we try to look 3-5 years out, the ongoing sell-off is just ridiculous.

In this note, I will perform a reverse DCF exercise to find out what sort of future growth is priced into Tesla’s stock at current levels. Additionally, we will review Tesla’s technical charts to take a measure of possible short-term moves in the stock. Lastly, I will share an updated valuation for Tesla based on my fresh projection for Q4. Without further ado, let’s begin.

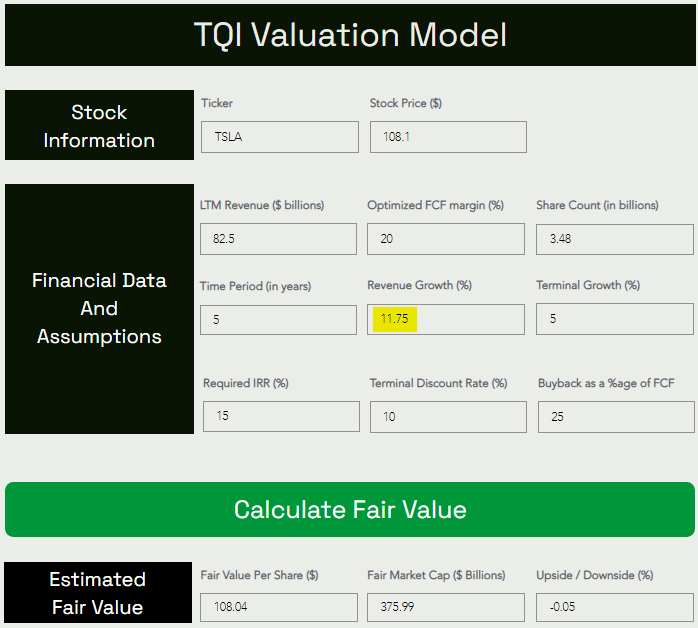

Reverse DCF Analysis: What Sort Of Growth Is Mr. Market Pricing Into Tesla’s Stock?

In order to carry out this exercise, I maintained all of my past assumptions for Tesla and deduced the 5-yr CAGR revenue growth rate by matching current stock price and fair value per share.

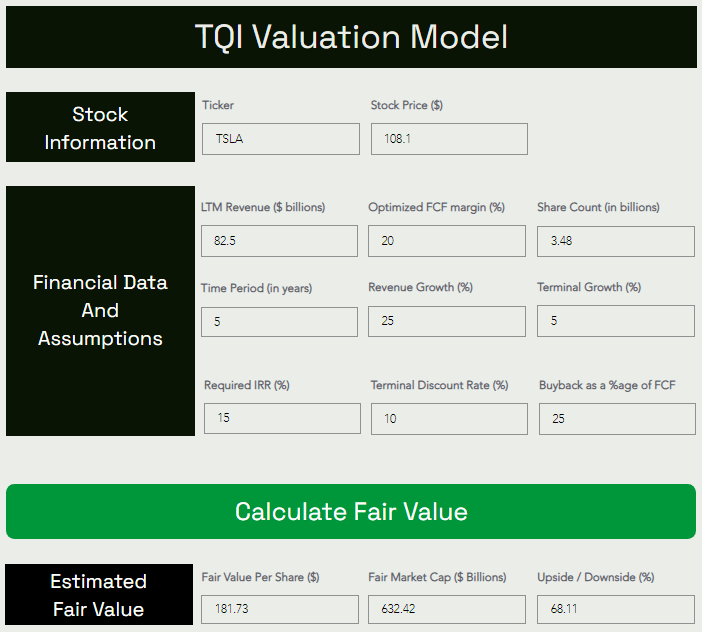

TQI Valuation Model (TQIG.org)

As you can see above, Tesla’s current stock price indicates a 5-yr CAGR revenue growth of 11.75%. Now, I think there’s a big disconnect between Tesla’s business fundamentals and what the Mr. Market is pricing in right now.

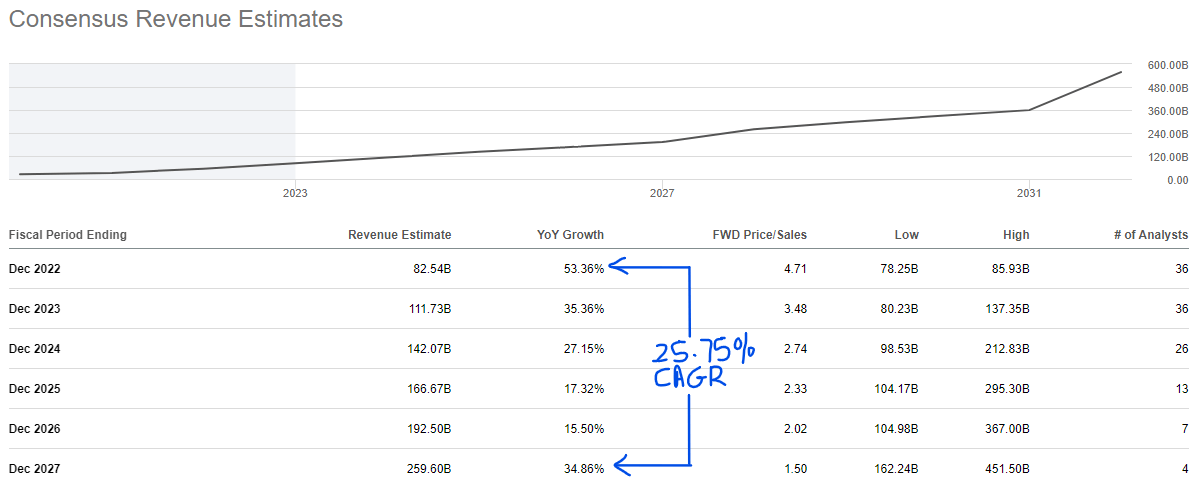

According to consensus analyst estimates, Tesla is set to grow at 25.75% CAGR over the next five years. And Tesla’s executive leadership is targeting ~50% CAGR revenue growth for the medium term.

SeekingAlpha

In my view, Tesla’s revenue growth will land somewhere in between, and as you may know, I have modeled Tesla for 32.5% CAGR growth for the 2023-27 period. Now, if we end up in a deep recession, Tesla’s growth may moderate significantly during the next 12-24 months; however, EV adoption is still in the early innings, with EVs making up only 5% of US auto sales. Tesla currently boasts a market share of just 1% of the global auto market. Furthermore, Tesla’s ambitious projects like Energy storage solutions, Solar Roofs, Dojo AI Supercomputer, Optimus Humanoid Robot, and Autonomous vehicles/Robotaxi address markets worth trillions of dollars.

Overall, I believe that sentiment on Tesla has turned ultra-pessimistic – none of Tesla’s futuristic ventures are getting any credit at all and its EV business is also being sold at a hefty discount [Tesla is priced for 5-yr CAGR growth of just 11.75%]. Tesla has a long, long runway for growth, and any hiccups in Tesla’s growth story during a recession in 2023-24 are likely to be temporary.

Technical Analysis For TSLA

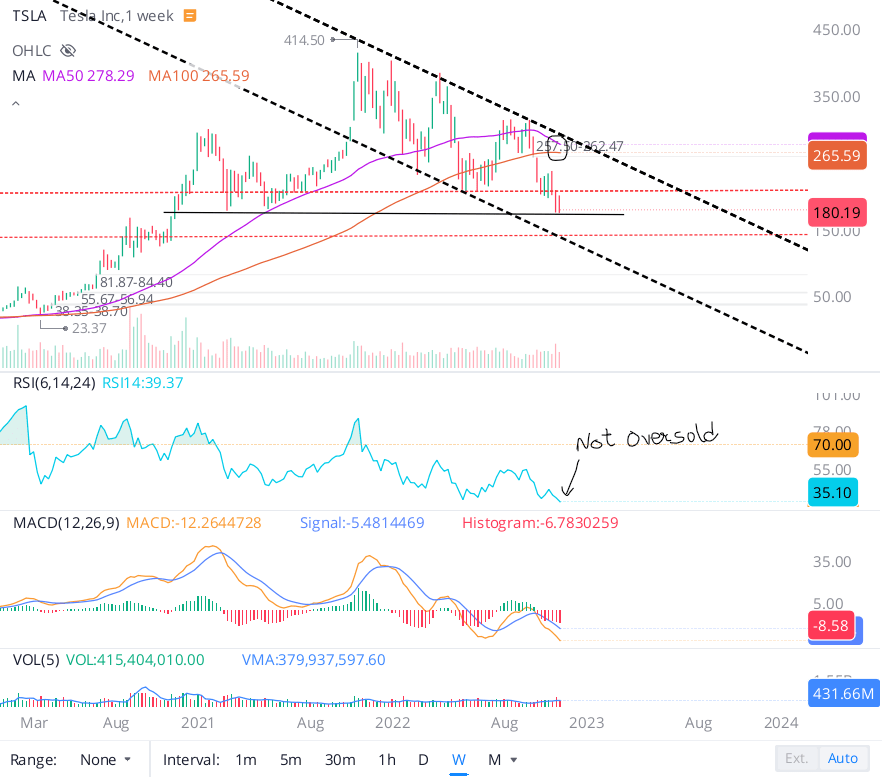

If you have followed my work on Tesla, you know that I have been harping about the need for slow accumulation in this counter. For those looking for an explanation, here’s an excerpt from one of my previous notes (before the breakdown of Tesla’s H&S pattern):

On Tesla’s chart, we are now looking at the potential breakdown of a bearish “Head and Shoulders” pattern, which could mean a quick ride down to the mid-100s (even low-100s is possible). The prospect of a reverse gamma squeeze in Tesla is real, and despite my switch to a bullish stance for Tesla’s stock after considerable valuation moderation, I urge investors to proceed with caution. For anyone looking to buy Tesla for the long term, I see slow accumulation as the right strategy. However, if you are looking for a short-term buy, just skip Tesla for good.

Tesla Chart 20th October 2022 (WeBull Desktop)

After undergoing months of painful correction, Tesla’s stock is finally undervalued; however, given current market conditions, it may very well overshoot to the downside. A bearish post-ER price move indicates that Elon Musk’s positive commentary around [50% CAGR] revenue (volume) growth, [$5-$10B] stock buyback, [best-ever] product roadmap, and Tesla’s future valuation [$4.5T = Apple + Saudi Aramco] has failed to paper over the evident cracks (albeit small misses) in Tesla’s Q3 report. That said, Tesla just reported yet another record-breaking quarter and is set to create new records in Q4. As a long-term investor, I view Tesla’s Q3 miss as nothing but short-term noise.

From a long-term perspective, Tesla is one of the strongest earnings growth stories in the market. And now that Tesla is undervalued, investors shouldn’t pass up on this fantastic company. Considering the rising probability of an economic recession and Tesla’s precarious technical chart (showing a ‘Head & Shoulders’ pattern), I think slow accumulation is the way to go here. As I have said in the past, the low-200s seem like a reasonable entry point in Tesla for long-term investors. If we do see Tesla break down to the mid-100s, I think that would be a great buying opportunity.

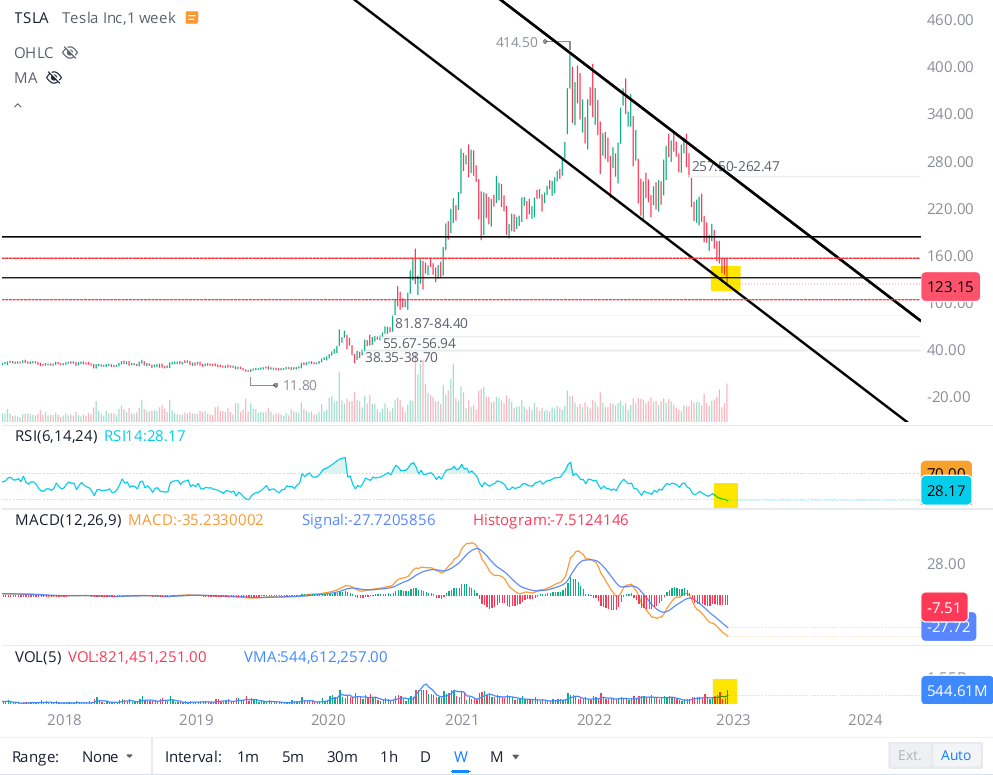

And here’s what I said after the breakdown of Tesla’s H&S pattern in November:

Tesla has one of the worst technical charts in the equity market right now, with a confirmed breakdown of the bearish head and shoulders (H&S) pattern pointing to even more downside from here.

Tesla Chart 21st November 2022 (WeBull Desktop)

The next big support is located on the lower trendline of the falling wedge pattern Tesla has been trading in for months, and that level is ~$140. If a reverse gamma squeeze were to materialize, I think even the low $100s are on the table for Tesla. With this precarious technical setup, buying Tesla as a near-term trade (<12 months) is simply out of the question. And any long-term investor buying here should be prepared for high volatility in this counter.

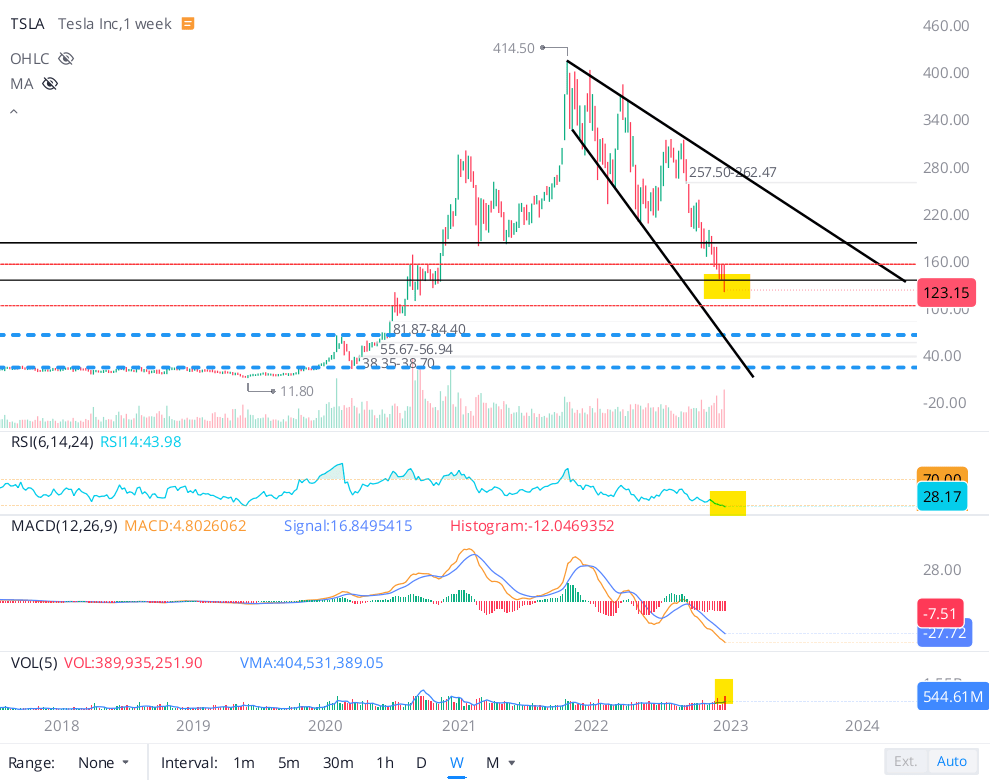

Lastly, here’s what I said in my latest note on Tesla in December:

As of the close on 23rd December 2022, Tesla’s stock was trading at $123.15 per share, down ~20% for the week with heavy volumes. The rapid deterioration in Tesla’s market capitalization reeks of capitulation amid a flurry of margin calls. In this note, we discussed the ongoing reverse gamma squeeze in Tesla and the factors that could continue to drive this move to the downside.

After a rapid decline in its stock price over the last month, Tesla is now trading at the lower trendline of the falling channel pattern we have observed over the last several months. With an RSI of 28, Tesla’s stock is oversold and ripe for a bounce in the near term.

Tesla Chart 23rd December 2022 (WeBull Desktop)

As the sell-off intensifies, trading volumes are picking up, with the ongoing move in Tesla’s stock reeking of capitulation. Tesla is a big retail stock, and its price action is indicative of a flurry of margin calls. On the chart, I also see a megaphone pattern, and a breakdown of the lower trendline of the falling channel would make me re-draw the lines. If Tesla’s stock were to hit the lower trendline of the megaphone pattern, we could be headed down to mid-double digits.

Tesla Chart 23rd December 2022 (WeBull Desktop)

Looking at the rapid decline in Tesla’s stock price, I think a reverse gamma squeeze is playing out, with traders piling into out-of-the-money put options to bet against Tesla. While a test of the low $100s seems like a foregone conclusion at this point, a breakdown of these levels could send the stock plunging lower to pre-pandemic levels in the $60-65 range (and even lower) in 2023.

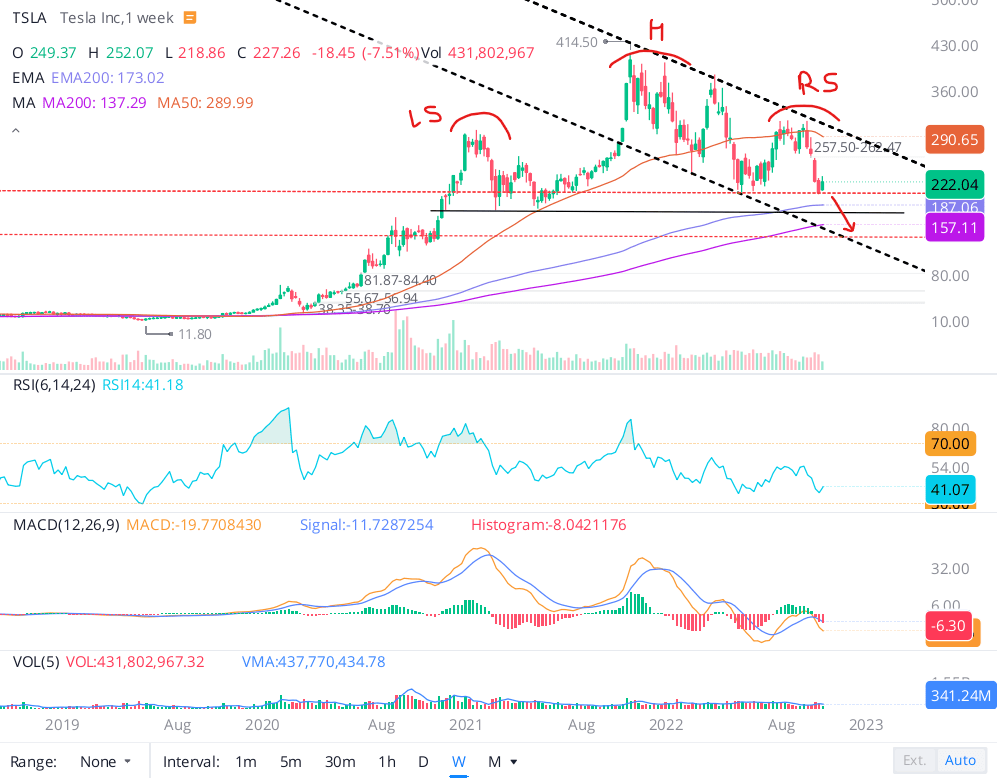

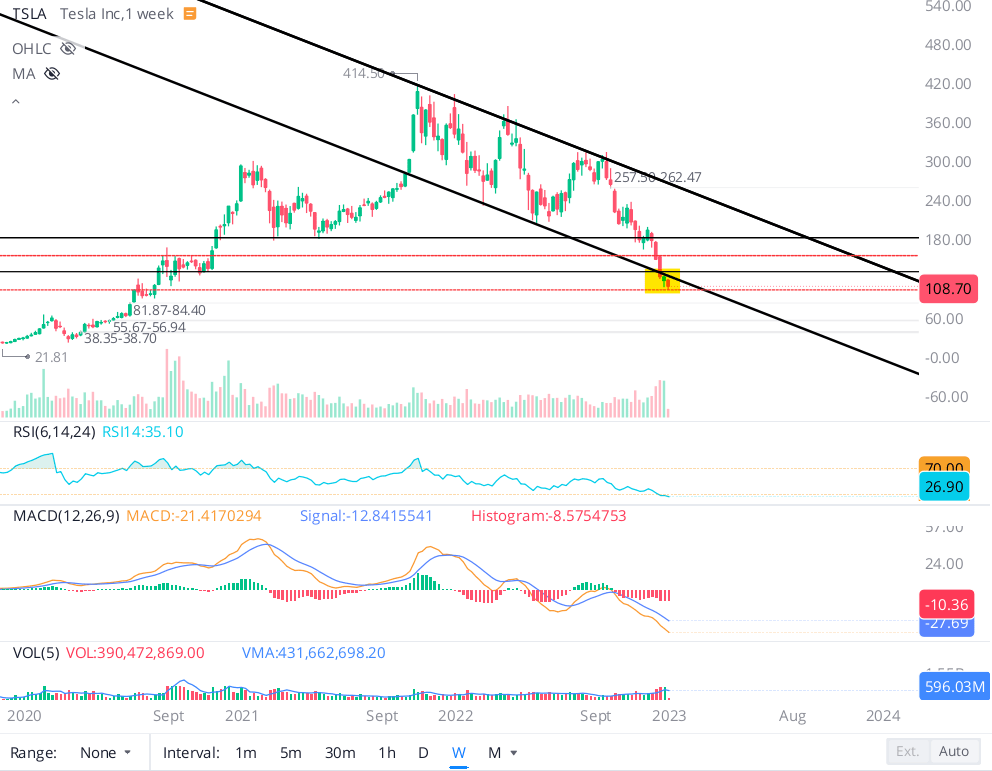

Now, let’s see how Tesla’s stock chart has evolved over the last week.

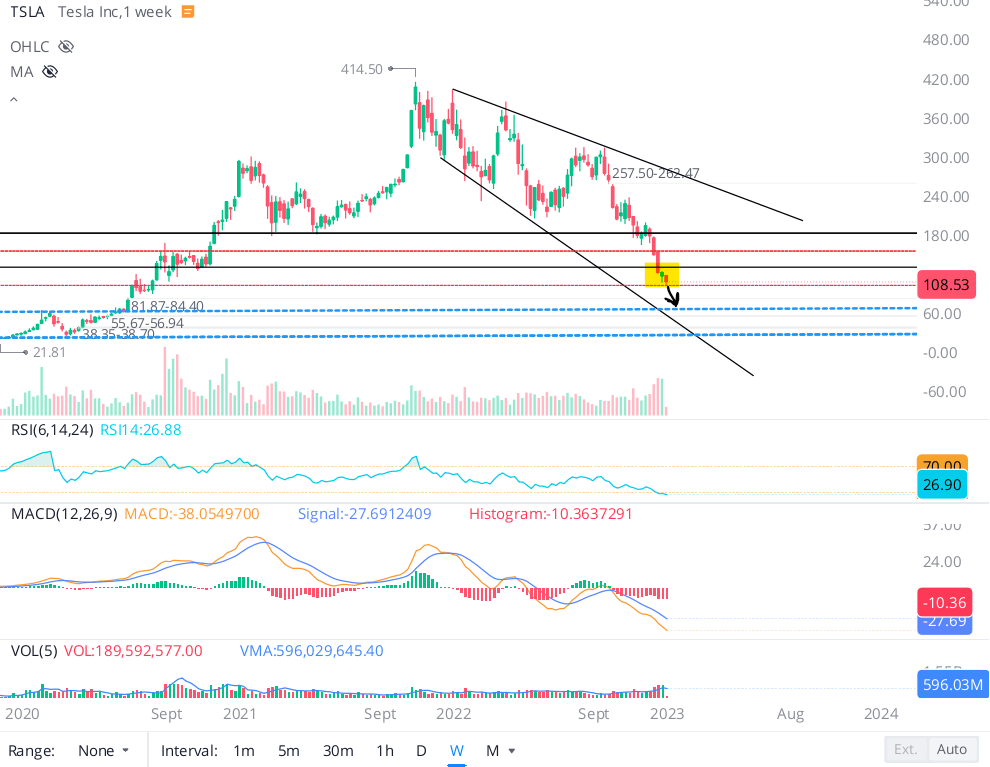

As you can see below, Tesla’s stock has broken below the lower trendline of the falling channel pattern. On Tuesday, Tesla got rejected from this lower trendline and we also got a new 52-week low. The breakdown of $108 level was a bearish signal, and I think we are set for a test of the key psychological support at $100 in upcoming days.

Tesla Chart 3rd January 2023 (WeBull Desktop)

As I said in my previous update, a breakdown of the lower trendline would force me to re-draw my lines, and I am now looking at the megaphone pattern for direction (instead of the falling channel pattern).

Tesla Chart 3rd January 2023 (WeBull Desktop)

With Tesla set to report weaker-than-expected numbers for Q4, Tesla’s stock could remain under pressure. Elon Musk has been extremely bearish on the economy and blamed FED’s actions for the demand problems at Tesla. If we end up in a severe recession, Tesla’s financial performance could deteriorate significantly in the next few quarters. A drastic drop in revenue growth rates and profitability could lead to a continuation of the unwind in Tesla’s stock.

The technical setup for Tesla is precarious, and it could very well be headed to pre-Covid highs of $60-65 per share. Due to this negative setup, I continue to stress on the need for slow accumulation in this counter.

Updated Valuation For Tesla

For Q4, I had estimated deliveries of 425K. And honestly, I am a little shocked to see Tesla miss my estimate by 20K vehicles despite heavy discounting towards the end of December. As a result of this delivery miss and Tesla’s price cuts, I am cutting my revenue forecast for Q4 by $1B. For 2022, I now expect revenues to come in at $82.5B, and this figure is in line with consensus analyst estimates.

Additionally, I now believe that the demand concerns around Tesla are warranted, and rising inventory levels going into a potential recession is bad news. If we end up in a severe recession, Tesla’s sales growth and earnings could fall off a cliff over the next 12-24 months. While this drop is likely to be temporary, I am lowering my 5-yr growth assumption for Tesla to 25% in order to implement a margin of safety.

Here’s my updated valuation for Tesla:

TQI Valuation Model (TQIG.org)

According to my analysis, Tesla’s intrinsic value is ~$182 per share. This means Tesla is now undervalued by ~41.5%. As we discussed in the past, Tesla is overshooting to the downside (and there could be more room to fall)!

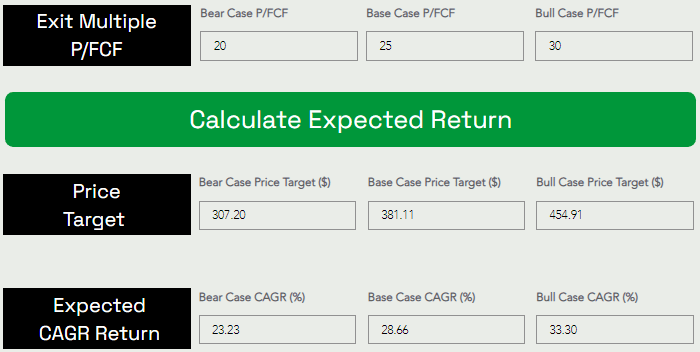

Now, let’s look at expected CAGR returns for the next five years.

TQI Valuation Model (TQIG.org)

Assuming a base case exit P/FCF multiple of ~25x for Tesla, I see the stock hitting $381.11 per share by 2027. As can be seen above, Tesla is projected to deliver CAGR returns of 28.66% for the next five years, which beats my required IRR of 15%. Hence, I continue to view Tesla as a solid long-term buy at $108 per share.

Final Thoughts

Tesla’s beaten down stock took yet another beating in the first trading session of 2023 due to a significant delivery miss for Q4. The demand concerns around Tesla are growing, and honestly, these concerns are not unwarranted. With macroeconomic uncertainty set to persist over the next few quarters, Tesla’s financial performance (and its stock) may continue to remain under pressure.

My immediate reaction to Tesla’s delivery miss was to pause my DCA plan and re-evaluate my investment thesis. After performing a reverse DCF analysis, I think the market is pricing in sales growth well below Tesla’s business prospects.

Tesla’s near-term outlook remains uncertain. With the Fed pulling liquidity out of this economy, demand destruction is a natural outcome, and Tesla is already showing signs of demand cracking up. While Tesla is heading into its first recession, Elon Musk seems distracted with Twitter and using Tesla as his piggy bank to finance Twitter is hurting investor confidence.

In the event of a severe recession, Tesla’s numbers are likely to disappoint, and if earnings were to collapse (or go negative) in 2023, the bottom could really fall out next year. If the reverse gamma squeeze continues, Tesla could be headed all the way down to pre-pandemic highs at ~$60-65 (or even lower). Technology giants like Meta (META) and Amazon (AMZN) are sitting at COVID-lows, and Tesla could join them in the event of a deep recession.

From a long-term standpoint, strong business fundamentals and reasonable valuation make Tesla a lucrative investment idea at current levels. Despite near-term downside risk, Tesla is a high-quality business that I want to own for the long haul. After re-assessing Tesla in the aftermath of a disappointing Q4 delivery report, I continue like Tesla in the low-$100s.

That said, accumulating shares slowly remains the right strategy as volatility cuts both ways, and this is what we are doing within TQI’s GARP and Moonshot Growth portfolios. Within our Managed Risk portfolio, we have implemented a long position in Tesla with a zero-cost, options-based hedge guarding downside up to $60 per share.

Key Takeaway: I rate Tesla a “Buy” in the low $100s, with a strong preference for staggered accumulation over 6-12 months.

Thank you for reading, and happy investing. If you have any questions, thoughts, and/or concerns, please share them in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment