jetcityimage

Thesis

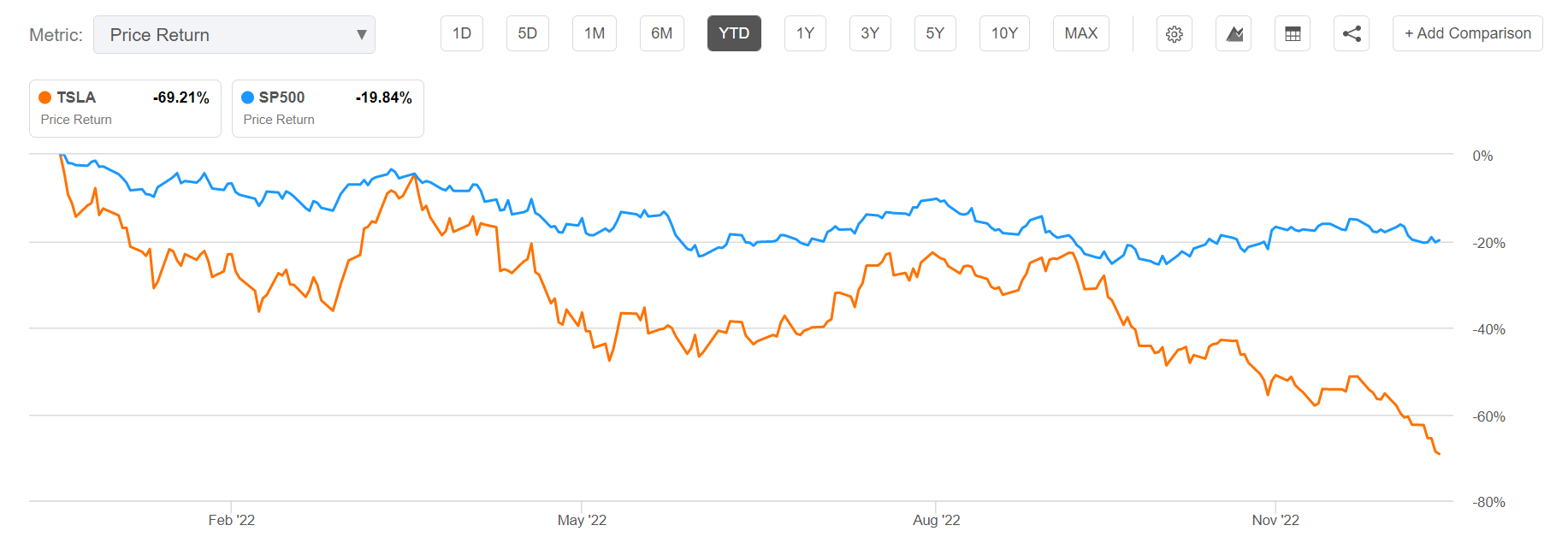

Tesla (NASDAQ:TSLA) stock is dropping like a stone and now down by approximately 70% YTD. For reference, this loss of value is worse than what investors needed to suffer with Meta Platforms (META) (down about 65% YTD), and the S&P 500 (SPY) has only lost about 20%.

Seeking Alpha

Personally, I am confident to argue that the current sell-off provides investors with an attractive buying opportunity. To be fair, there is a lot of noise surrounding the world’s leading electric car marker, including (1) Elon Musk selling shares, (2) Elon Musk being CEO of Twitter, and (3) various macroeconomic challenges. But these concerns should prove to be temporary. And from a fundamental perspective – in relation to Tesla’s long-term potential – the stock clearly looks undervalued at FWD x26 EV/EBIT.

Is It Elon Musk, Or Interest Rates?

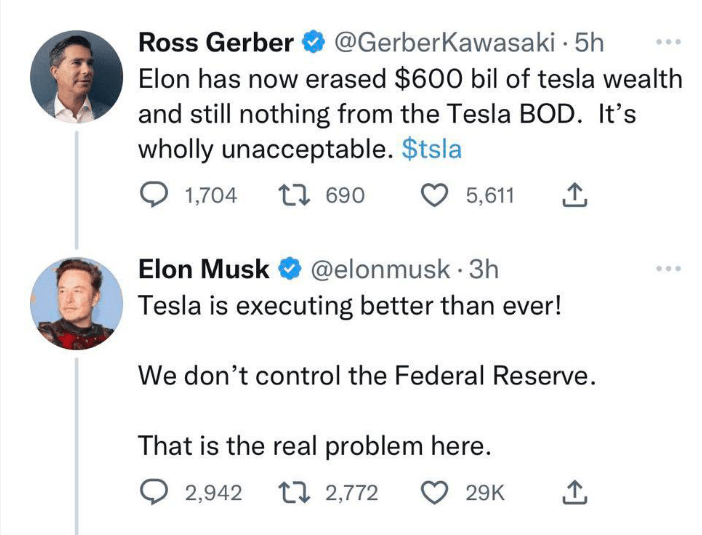

With some Tesla investors, the narrative is building that Tesla’s sharp sell-off is strongly correlated to Elon Musk’s takeover of Twitter. Ross Gerber for example, a notable Tesla bull, has implied that Elon Musk’s behavior/ actions have erased $600 billion in market capitalization. But Elon quickly defended himself with the argument that the sell-off has been caused by higher interest rates.

Twitter

Let us look these two positions with a little bit more context.

Elon Musk Shifting Focus Away From Tesla

A key argument why some investors believe that Tesla shares are falling is anchored on the simple observation that Tesla shares have lost approximately 40% since the Twitter deal closed on 27th October, while the S&P 500 (SPY) is down by only 2%.

Some investors are clearly concerned that with the Twitter acquisition, Elon Musk will lose focus on his role as Tesla’s CEO – now being Chief Executive Officer of Tesla, SpaceX, Twitter, The Boring Company and Neuralink.

Moreover, there has been some evidence that Elon Musk is shifting additional resources away from Tesla, not only his own time and energy. In late October, Musk invited about 50 Tesla engineers to the Twitter headquarters, asking their support in improving various algorithms on the social media platform. However, Musk argued that the commitment was non-material to Tesla’s business operations: (emphasis added)

This was an after hours — just if you’re interested in evaluating, helping me evaluate Twitter engineering … that’d be nice. I think it lasted for a few days and it was over.

In any case, Elon Musk has by now said that he will step down as Twitter’s CEO, as soon as a suitable successor is found.

Elon Musk Selling Shares

Enormous blocks of share sales is another observation linked to Musk’s acquisition of Twitter. Since the Twitter deal has been announced, Musk has sold nearly $23 billion worth of stock, despite his promise in April that he won’t. Of course, selling $23 billion of equity in a bear market adds strong downward pressure to prices, and the action certainly pressures both investor confidence as well as sentiment.

Now once again Elon Musk has promised to not sell any shares – until at least 12 months. But will investors trust this promise?

I won’t sell stock until, I don’t know, probably two years from now. Definitely not next year under any circumstances and probably not the year thereafter

Interest Rates

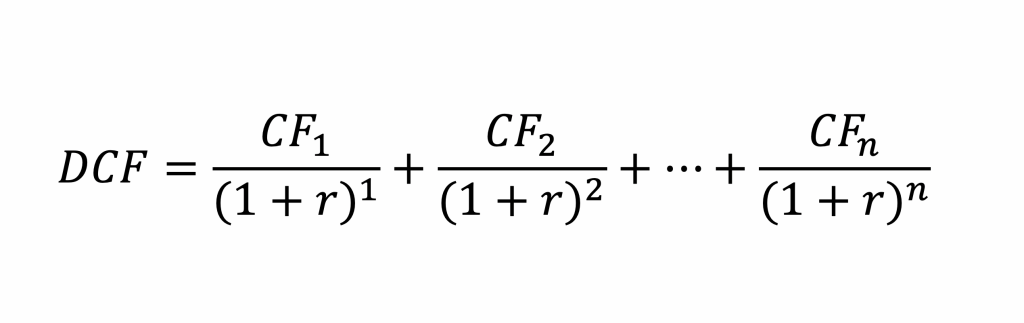

Meanwhile, Elon Musk argued that Tesla ‘is executing better than ever’, and the reason for the stock’s sell-off is due to higher interest rates. While the interest rate argument might be true to some extent, looking at the basic DCF formula…

Magnimetrics

… investors should consider that since the Twitter deal closed, the Fed raised the funds rate by only 50 basis points. However you structure the DCF formula, it is hard to mathematically (and reasonably) prove a $600 billion loss of value due to only 0.5% higher interest rates.

Moreover, while Tesla’s share price might indeed be more sensible to higher interest rates than the S&P 500 (Tesla is a long duration growth asset), the performance discrepancy of Tesla and the S&P 500 for the past few months is simply too excessive to be explained by interest rates.

Macroeconomic Challenges

The real reason why Tesla shares are slipping might simply be the uncertainty and fundamental pressure related to macroeconomic challenges. Elon Musk has already voiced concerns that the economy might fall into a recession in 2023 and Tesla car sales might suffer accordingly.

I think we are in a recession, and I think 2023 is going to be quite a serious recession …

… It’s going to be, in my opinion, comparable to 2009. I don’t know if it’s going to be a little worse or a little better, but I think it’s, in my view, likely to be comparable. That means demand for any kind of optional, discretionary item, especially if it’s a big-ticket item, will be lower.

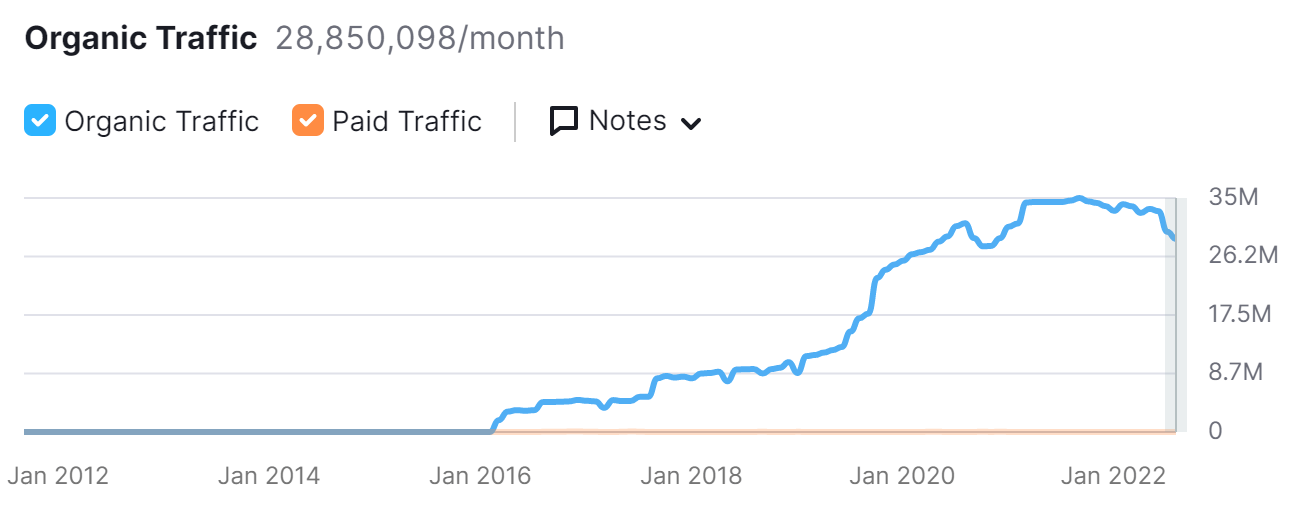

Notably, Tesla shares fell as much as 10% after the car maker announced price discounts of $7,500 to US consumers – an announcement that clearly hints on demand concerns. The thesis of demand concerns is supported by Tesla.com website traffic data from Semrush, which highlights that interest for cars could be falling off a cliff.

Semrush

Valuation

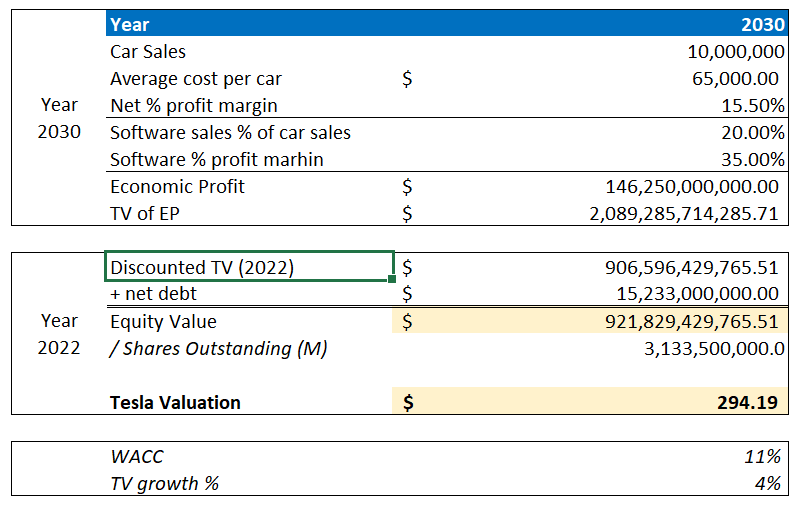

Valuing Tesla, I continue to believe Tesla could sell an estimated 10 million cars per year by 2030 and achieve an average sales price per car of $65,000. Furthermore, I continue to assume:

a net-profit margin of 15.5%, which is only slightly above Tesla’s 2022 net profit margin and in my opinion a very reasonable assumption if one consider increased economies of scale. (Note that I expect sales volume to almost 10x).

In addition, I argue that for every dollar that Tesla generates selling cars, the company will be able to sell 20 cents of software solutions and insurance (for reference, Apple generates about 30 cents worth of services for every dollar of hardware sales). For Tesla’s software business, I argue 35% net-profit margin is reasonable — in line with margins of leading tech/internet companies.

However, I slightly increase my cost of equity estimate – to 11% as compared to 10% prior. The rationale behind this increase is that Tesla’s value is anchored on the future, and betting on the future remains speculative. It is thus, in my opinion, only reasonable to demand an attractive reward for such a speculation.

Based on the above variables, I calculate a fair implied price per share for TSLA equal to $294.19/share.

Author‘s estimates and calculations

Risks and Headwinds

As I see it, there has been no major risk update since I initiated coverage on Tesla stock, except for those discussed in previous sections. Thus, I would like to highlight what I have written before:

Although Tesla has proven to be more resilient than what investors thought, both in relation to a challenging macro-economy and fading risk-sentiment, I believe the major risk for Tesla stock remains that a worsening macroeconomic backdrop will pressure investors risk-sentiment to such a degree that Tesla stock’s growth multiples compress. Or in other words, investors should acknowledge that much of Tesla’s share price performance remains driven by general sentiment towards stocks (Tesla’s beta vs the S&P 500 (SPX) is about 1.7). Accordingly, investors should be prepared to stomach volatility, even though Tesla’s fundamental outlook remains unchanged.

Personally, I do not believe that increasing competition in the race for electrification will influence the demand for Tesla — like “other” smart phone makers do not influence the demand for iPhones. The increased competition could, however, exacerbate Tesla’s supply challenges, as more competition chases for a limited supply of raw materials and key manufacturing components.

Investor Takeaway

I have never thought I would say this, but Tesla stock now appears to be trading in bargain territory. Personally, I would argue that the headwinds presented in the prior sections of this article could be classified as temporary, or noise. Long-term, Tesla remains the leading EV maker, with a strong brand and the world’s most extensive network of EV charging stations.

Personally, I calculate that TSLA stock should be fairly valued at about $294.19/share (which indicates almost 150% upside). Buy.

Be the first to comment