colnihko/iStock via Getty Images

The term structure of interest rates is something to look at when considering the future path of the economy.

A negative yield curve is often considered the predictor of a looming economic recession.

Well, take a look at the current yield curve in the United States.

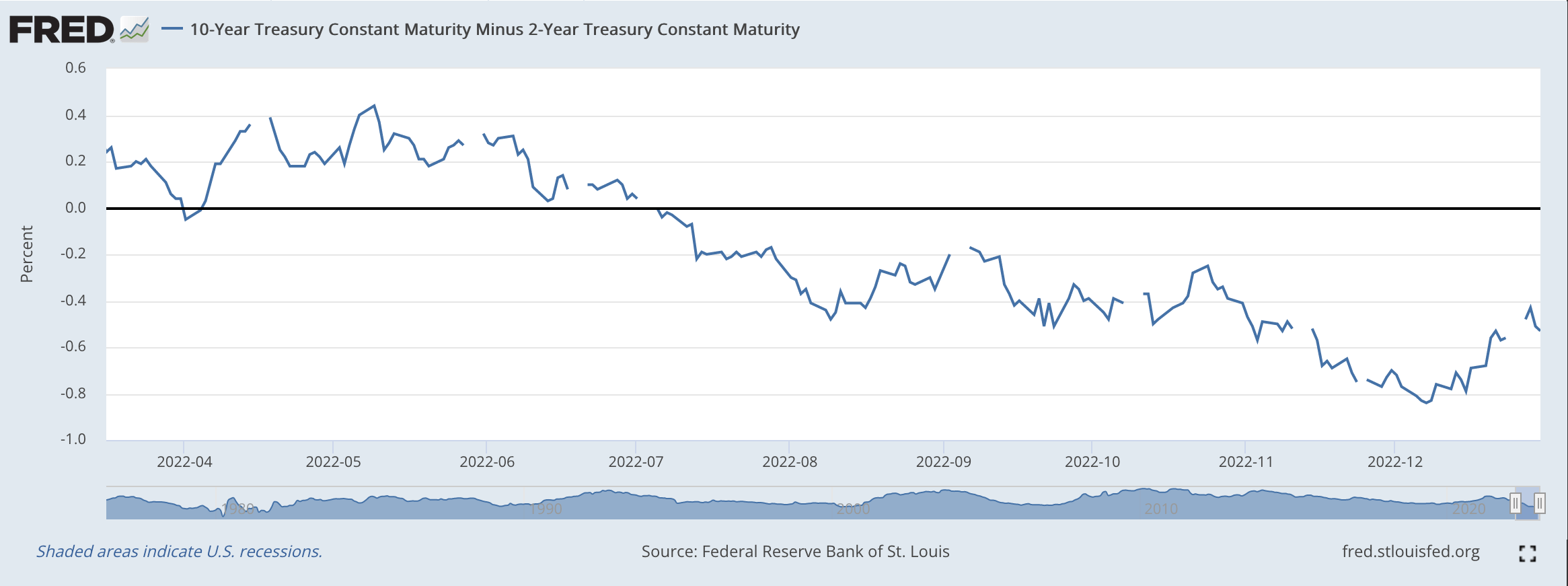

10-year Treasury Yield Minus 2-year Treasury Yield (Federal Reserve)

Right around the first of July 2022, the yield curve for U.S. Treasury notes, the 10-year yield minus the 2-year yield, turned negative.

It has remained negative ever since.

Both yields have risen during this time period, but the rise in the 10-year Treasury has been less than the rise that has occurred in the 2-year note.

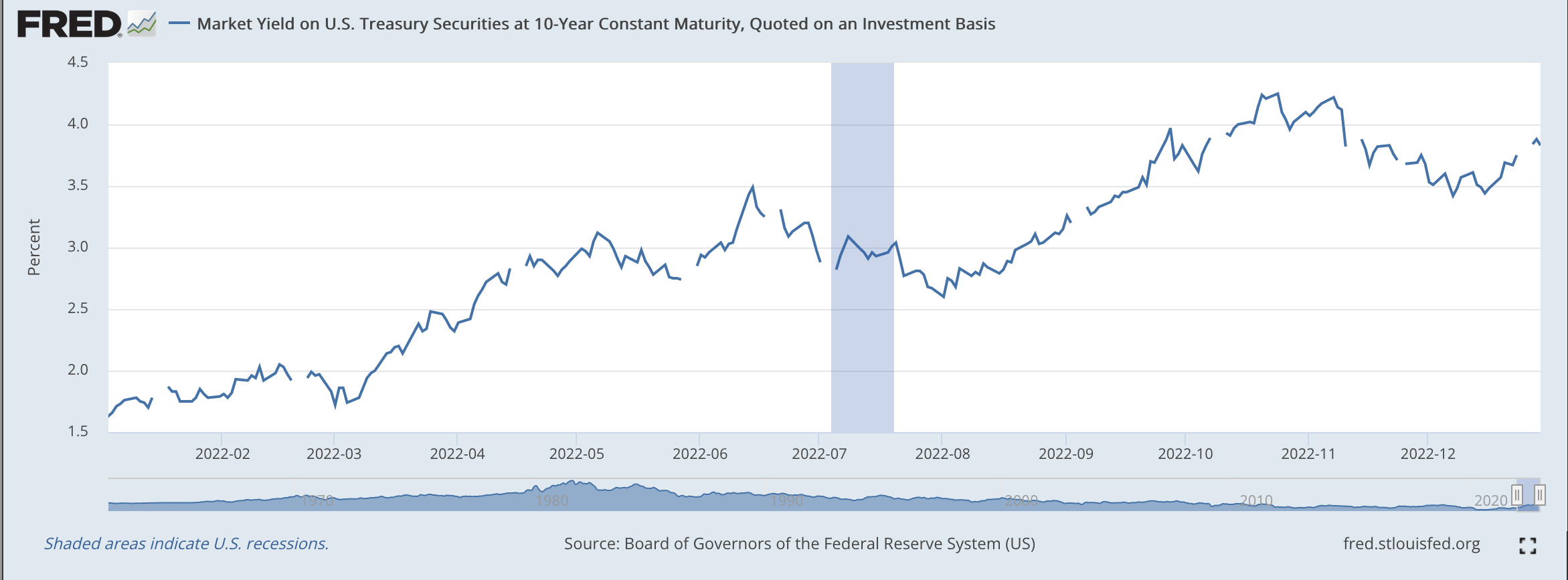

Yield on 10-year U.S. Treasury Constant Maturity (Federal Reserve)

The reason for the slower upward movement to the yield on the 10-year maturity note is that the inflationary expectations built into the yield has actually gone down since March.

For example, the inflationary expectations built into the yield on the 10-year U.S. Treasury note in early June was around 2.75 percent. That is, the annual compound rate of inflation for the next 10 years was expected to be 2.75 percent.

In December, the inflationary expectations built into the 10-year U.S. Treasury note yield fluctuated around 2.25 percent.

That is, inflationary expectations dropped by about 50 basis points from early June to the end of December.

This drop took place during the time that there was so much “noise” in the newspapers and other parts of the press about how bad inflation was and about whether or not the Federal Reserve was going to stick with its statements about sticking with the battle against inflation.

The figures from the bond market seem to indicate that the Fed was really doing its job and that inflation was expected to drop close to the inflation target of 2.00 percent that the Federal Reserve was shooting for.

For a few days in the middle of January, the inflationary expectations built into the yield on the 10-year Treasury note was around 2.15 percent.

The bond market really seems to believe that the Federal Reserve is going to continue to stick with its quantitative tightening so that inflation in the United States will return to the Fed’s 2.00 percent target.

The Recession

But, the bond market also seems to believe that the U.S. economy will go through some kind of recession in the near term that will help the Fed achieve its inflation target.

The Federal Reserve has pushed its policy rate of interest up and up and up in 2022.

On March 17, 2022, the Fed began its move to raise rates. It has raised its policy rate of interest seven times since. Treasury notes responded to this pressure and rose quite a bit.

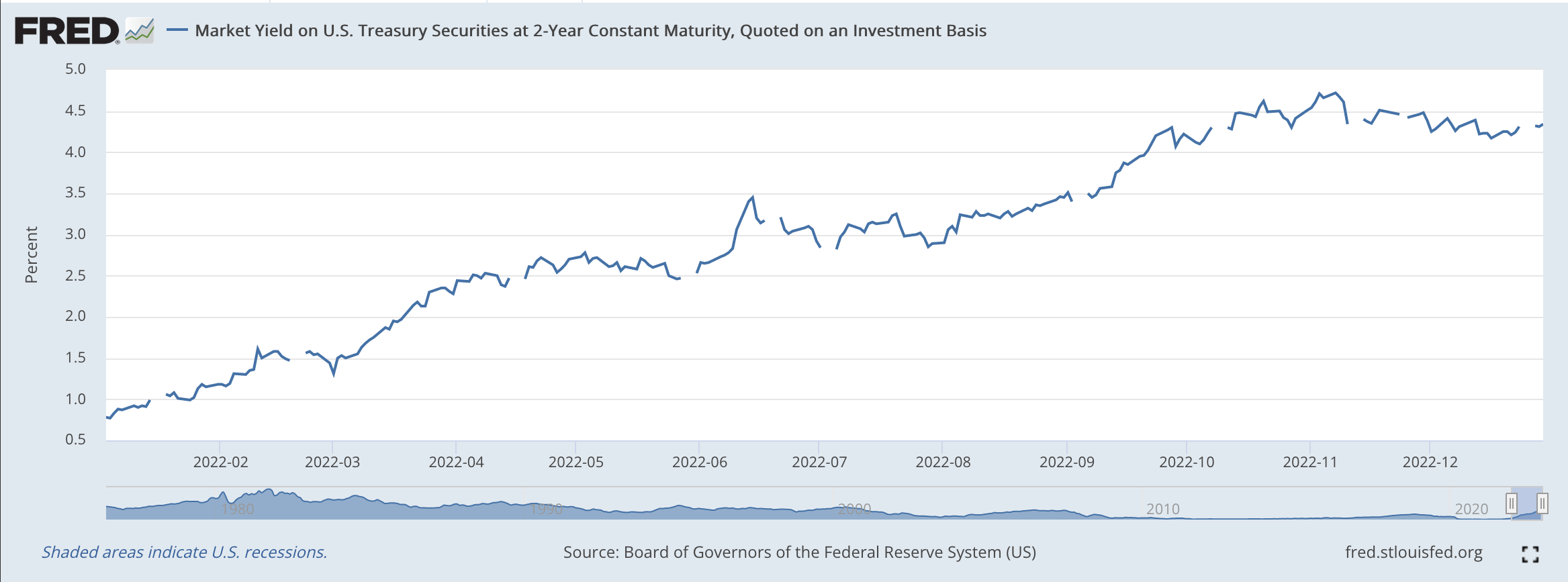

Yield on 2-year U.S. Treasury note (Federal Reserve)

As can be seen, the 2-year yield rose faster than did the 10-year yield and its rise was also steadier.

On March 16, 2022, around the time the Fed began to raise its policy rate of interest, the yield on the 2-year U.S. Treasury note was just under 2.00 percent.

On December 30, 2022, the yield on the 2-year note was over 4.40 percent. This represented an increase of about 240 basis points.

The Federal Reserve was tightening up and the Treasury yield curve was inverting.

Recession ahead.

But, it is, at the present time, still uncertain when a recession might hit, and it is still unknown how deep the recession might be.

Some analysts believe that the United States is already in a recession.

Others believe that we have not quite entered a recession yet.

And, there are still those that believe that the U.S. will not have a recession at this time.

The latest forecasts from the Federal Reserve project that the growth rate for real GDP from December 2022 to December 2023 is 0.5 percent.

From December 2023 to December 2024, the Federal Reserve expects the real growth rate to also be 0.5 percent.

The projections for 2022 include the economy having a very bad fourth quarter going into 2023 given the figures from the other three quarters of the year.

A 0.5 percent rate of growth for 2023 shows a very weak economy.

Will these results be interpreted as including a recession?

That we don’t know.

But, it does indicate that the economy in 2022 and 2023 will be seen as being very weak.

Fed In 2023

My expectation for the Federal Reserve in 2023 is for continued quantitative tightening. That is, the Fed will continue in its efforts to reduce the size of its securities portfolio, and in so doing will continue to reduce the “excess reserves” in the banking system and will continue to support further increases in its policy rate of interest.

Thus, I would expect the yields on the 2-year and the 10-year U.S. Treasury notes to continue to rise.

The rise will go on until the Fed believes that it has gone far enough in reducing the size of its securities portfolio or if the Fed feels that the financial markets are experiencing a drop requiring that “tightening” efforts stop.

These are, of course, known unknowns.

The financial markets are going to need close watching in 2023. The year 2023, I believe, is going to be very precarious for investors.

I expect that bond yields are going to continue to rise until something happens that causes the Fed to “move,” to ease up.

The thing is that the inflationary expectations built into the yields of the longer-maturity bonds are now quite low.

Unless the Fed goes “overboard” once again and floods the financial markets with liquidity, bond yields may not fall back as much during this recession as they have done in earlier environments.

This is just something investors are going to have to watch for. This is a part of the major uncertainty that exists about the upcoming year.

Be the first to comment