NicoElNino

Teradata (NYSE:TDC) is a database and analytics company that enables enterprises to break down data “silos” and unlock the power of their “big data”. The company has recently reported exceptional growth in its cloud annual recurring revenue which increased by 89% year over year. Teradata is poised to benefit from the growth in the cloud industry as companies “digitally transform” their operations. Management also believes its stock is “significantly undervalued” and initiated a $31 million share buyback in Q3,22. In this post, I’m going to break down the company’s business model, financials and valuation, let’s dive in.

Business Model

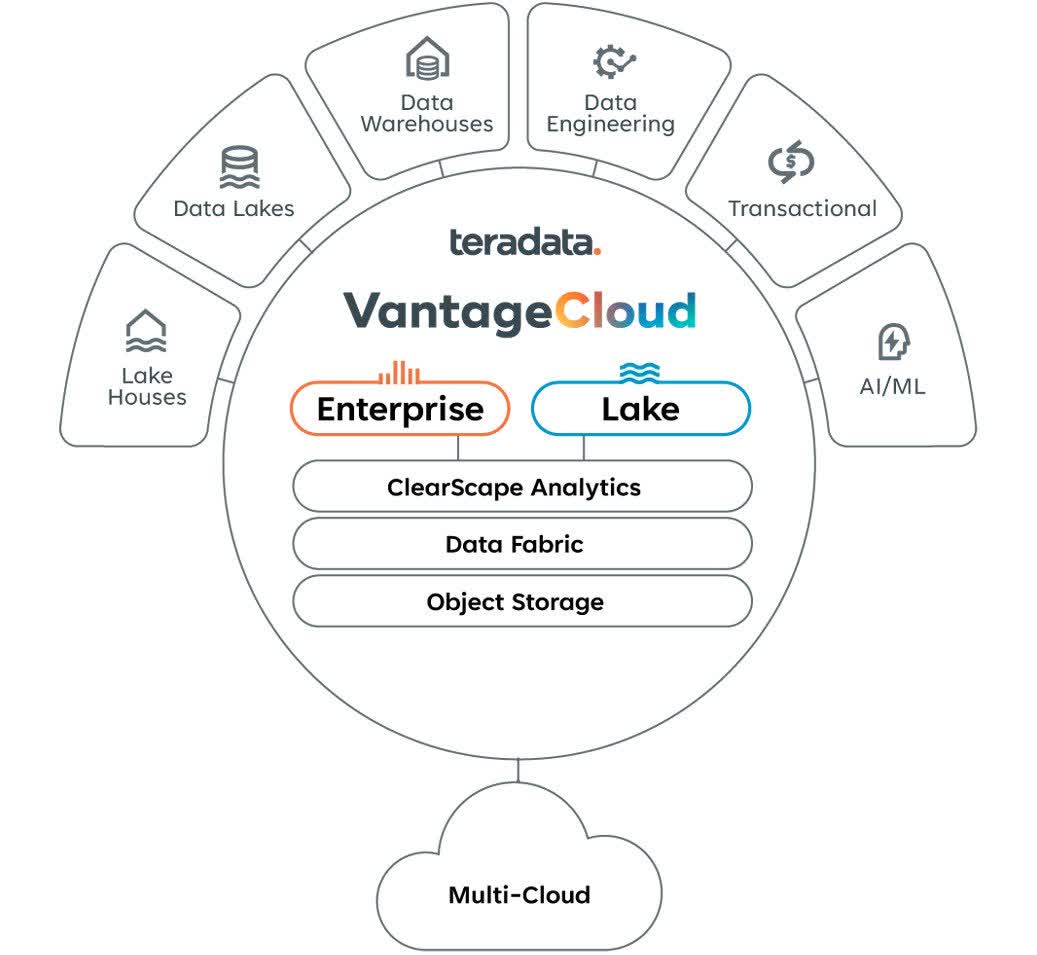

Teradata’s flagship platform is called “Vantage” and enabled data from multiple cloud sources to be unified, analyzed, and queried from one dashboard. Its compatible data sources include “data lakes”, data warehouses, and much more. As it’s built on the cloud the platform is scalable across multiple dimensions from the amount of data to the depth of the analytical queries.

Its platform is regarded as a leader in Cloud databases and Gartner reviews indicate it has 4.4 stars out of 5. This is level with the high-performance MongoDB and only 0.1 points below the iconic Microsoft SQL server.

Teradata Vantage cloud (Teradata)

Its products have many use cases across multiple industries from automotive to financial services. For example, the largest automaker in Europe Volkswagen utilizes Teradata to boost the efficiency of its Bodyshop processes. Other applications include fraud prevention, supply chain optimization, customer experience, and much more.

Teradata has a range of partnerships with large technology companies such as Microsoft and consultancies such as Accenture and IBM. This gives the platform multiple routes to market, which is a positive sign.

Mixed Financials

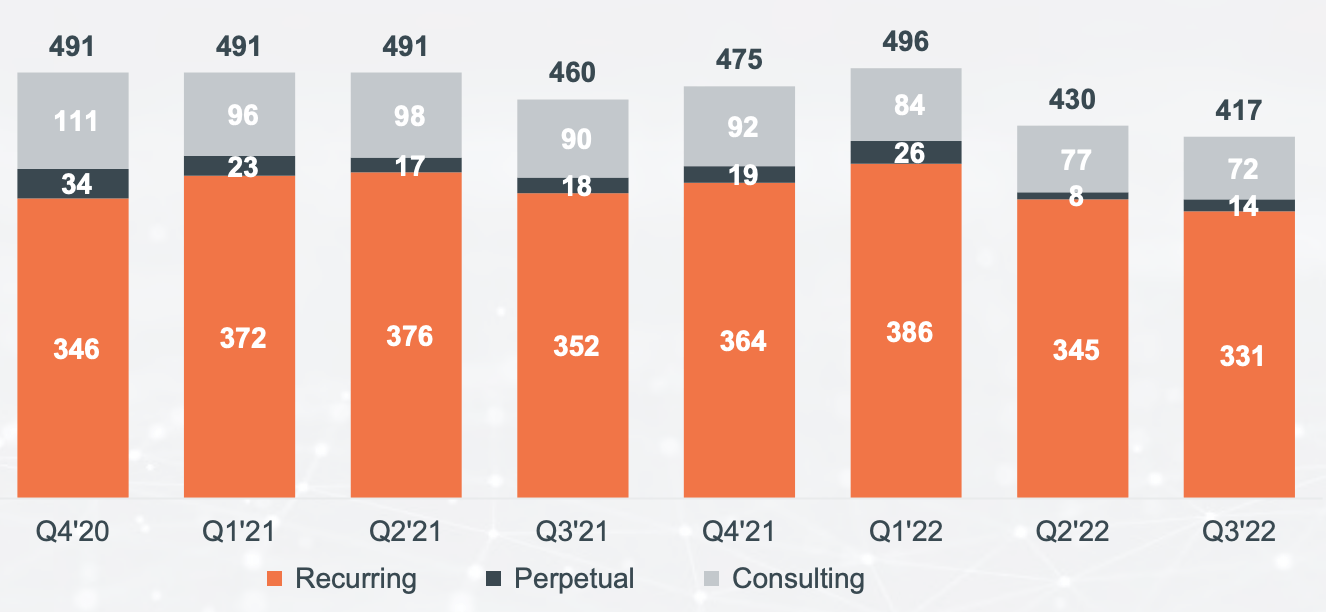

Teradata reported mixed financials for the third quarter of 2022. Revenue was $417 million, which declined by 9.85% year over year and missed analyst expectations by $6.1 million. However, if we account for foreign exchange headwinds on a constant currency basis, total revenue was $417 million, which declined by just 4% year over year. Teradata has over 40% of its revenue from outside of the U.S., which is great for diversification, but not when U.S. dollar strengthens significantly relative to foreign currencies. Revenue was also impacted by the ceasing of its operations in Russia, which resulted in a loss of $16 million.

The vast majority (79%) of the company’s revenue is recurring, which only declined by 2% on a constant currency basis. Teradata is aiming to move more of its revenue plans to a subscription model, which will likely increase consistency over time.

Revenue (Q3,22 report)

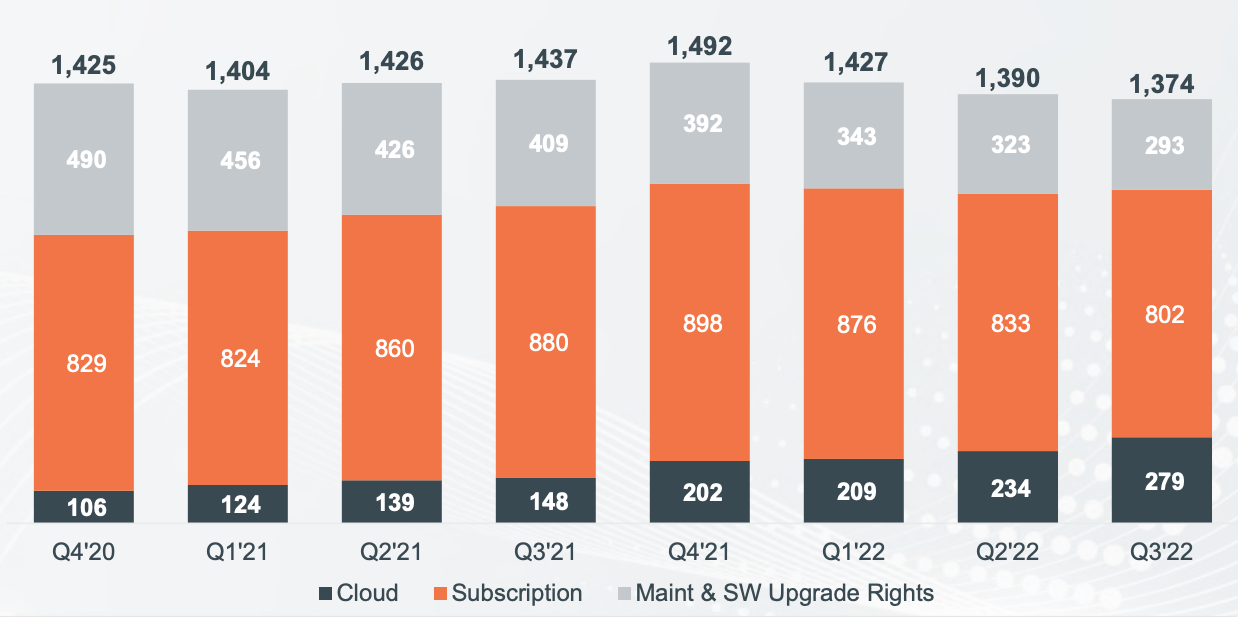

Taking a step back, a positive for Teradata is the company. has reported outstanding growth of 89% in its public cloud annual recurring revenue [ARR] to $279 million. On a constant currency basis the result was even more spectacular as the business reported 100% growth in cloud ARR year over year. Cloud-based ARR is a major growth segment of the company with huge potential.

The cloud industry was valued at $406 billion in 2021 and is forecast to grow at a rapid 19.9% compounded annual growth rate [CAGR] to reach a value of over $1.7 trillion by 2029. This growth is driven by the “digital transformation” of organizations as they move their workloads to the cloud. Companies move to the cloud for a variety of reasons including improved flexibility in operations, scalability, and even cost savings if optimized correctly.

In the third quarter of 2022, the company signed a range of deals in this industry. This includes an eight-figure cloud migration, a major bank in Chile, and one of the “world’s leading” financial services institutions.

ARR by Product (ARR by Product)

In the third quarter of 2022, Teradata reported a gross margin of 62.6% and gross profit of $261 million. This declined by $21 million due to mainly foreign exchange headwinds and the exit from Russia.

On a more positive note, earnings per share were $0.08, which beat analyst estimates by $0.05. On a non-GAAP basis, the result was even better with EPS of $0.31 reported, which beat analyst expectations by $0.02.

Teradata has a solid balance sheet with $506 million in cash and short-term investments. The company does have $628 million in total debt, but the majority ($498 million) is long-term debt and thus manageable.

Moving forward, management has continued to forecast strong growth in its cloud ARR, which is expected to increase by 80% year over year. Although, foreign exchange headwinds are still expected.

Advanced Valuation

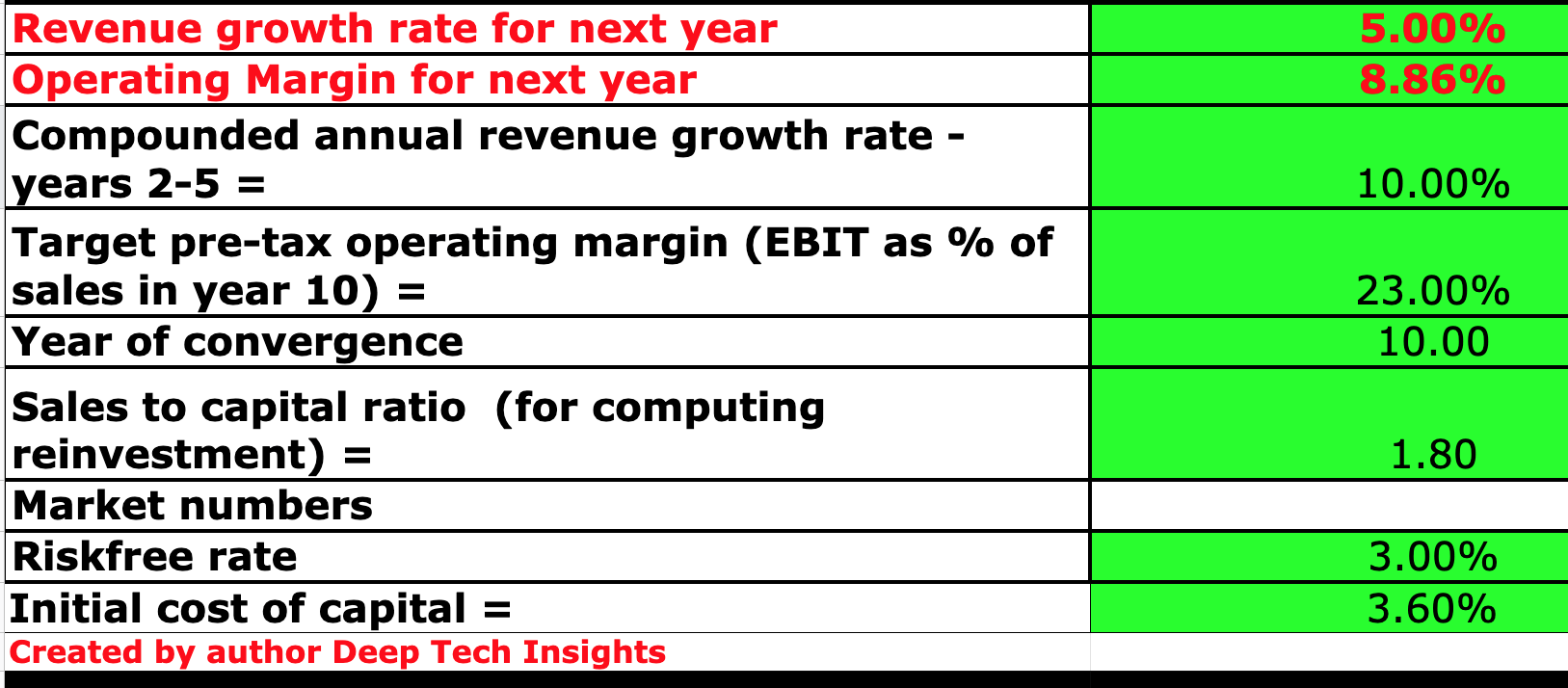

In order to value Teradata, I have plugged its financials into my discounted cash flow model. I have forecast 5% revenue growth for next year, which I expect to be driven by a more favorable comparison now Teradata has exited from Russia. In addition, I have forecast 10% revenue growth for next year which I forecast to be driven by the continual growth in its cloud business.

Teradata stock valuation 2 (created by author Deep Tech Insights)

To increase the accuracy of the model, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast the business will increase its operating margin to 23% over the next 10 years, which is the average of the software industry. I forecast this to be driven by increasing growth in its higher margin cloud segment, as well as economies of scale benefits.

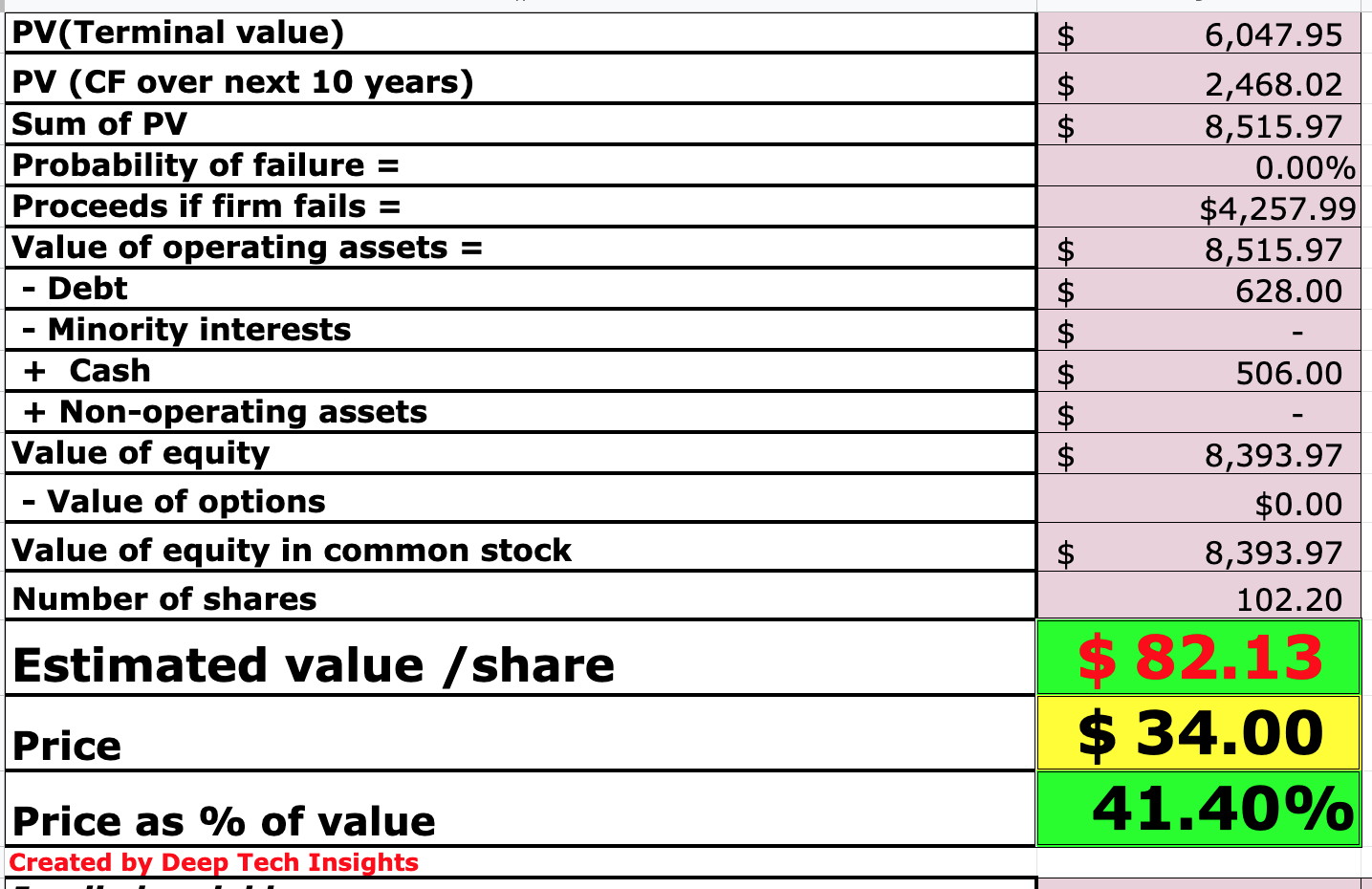

Teradata stock valuation 2 (created by author Ben at Motivation 2 Invest)

Given these factors I get a fair value of $82 per share, the stock is trading at ~$34 per share at the time of writing and thus it is significantly undervalued.

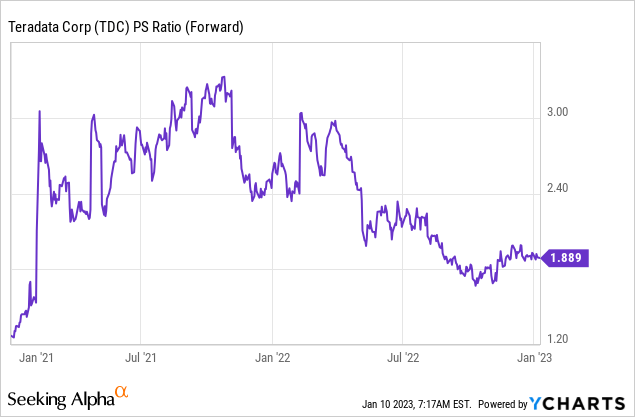

As an extra datapoint, Teradata trades at a price to sales ratio = 1.92, which is 6% cheaper than its 5 year average.

Risks

Recession/Longer sales cycles

Many analysts have forecast a recession, therefore I expect longer sales cycles for the company as decision-makers curb spending. In addition, foreign exchange headwinds are expected to continue as the U.S dollar remains strong.

Final Thoughts

Teradata is a solid software company that is poised to continually benefit from the growth in the cloud industry. The company is facing a few headwinds related to foreign exchange rates, but I believe this will not impact the business long term. Its stock is undervalued intrinsically and relative to historic multiples, thus it could be a great long-term investment.

Be the first to comment