JHVEPhoto

Introduction

Tenaris (NYSE:TS) is a stock that is ranked highly in the Seeking Alpha Quant rating at position 141, making it worth investigating.

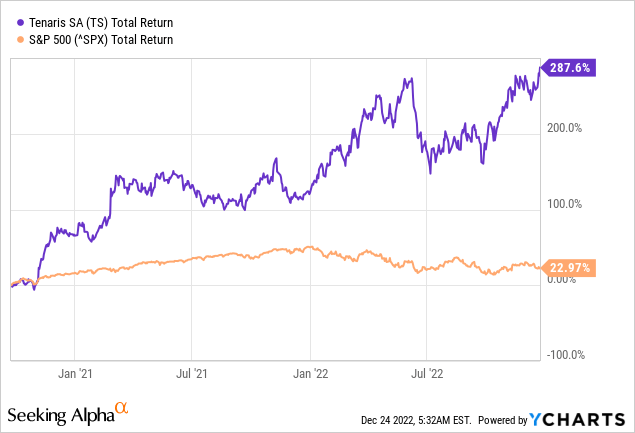

Since the mid-2020s, the stock has soared, with a total stock return of 288% compared to the “mere” 23% of the S&P 500.

The stock was upgraded by Stifel due to its strong position in the global market for oil country tubular goods. Stifel predicts that drilling and completion activity in the United States will continue to rise in 2023, with at least double-digit growth in the Eastern Hemisphere and continued growth in North and South America.

Revenue and earnings per share projections for the coming years have been revised significantly higher, making the stock cheap at current levels.

Company Overview

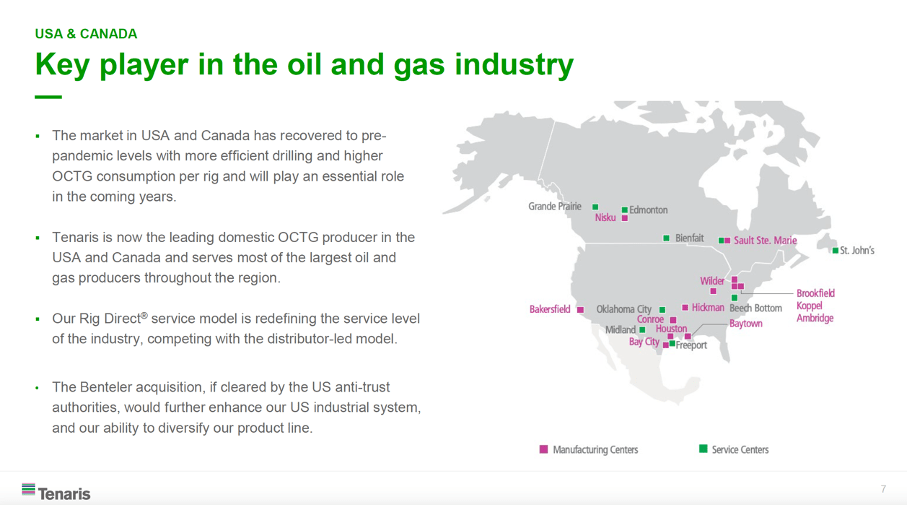

Tenaris: Key player in the oil and gas industry (Tenaris Investor Day)

Tenaris is a global company that specializes in the production and supply of steel pipes and related services for the oil and gas, energy, and infrastructure industries. The company was founded in 2001 as a merger between two leading Argentine steel producers, Tamsa and Siderca. Today, Tenaris has a presence in more than 20 countries and employs over 27,000 people worldwide.

Tenaris operates a number of state-of-the-art steel pipe mills and has a strong research and development program, which enables the company to continuously improve its products and services. In addition to steel pipes, Tenaris also manufactures a range of other products, including pipe fittings, connectors, and accessories. The company has a strong focus on sustainability and is committed to reducing its environmental impact through various initiatives, including energy efficiency, waste reduction, and the use of recycled materials.

Total Addressable Market Expected To Grow At A CAGR Of 6.7%

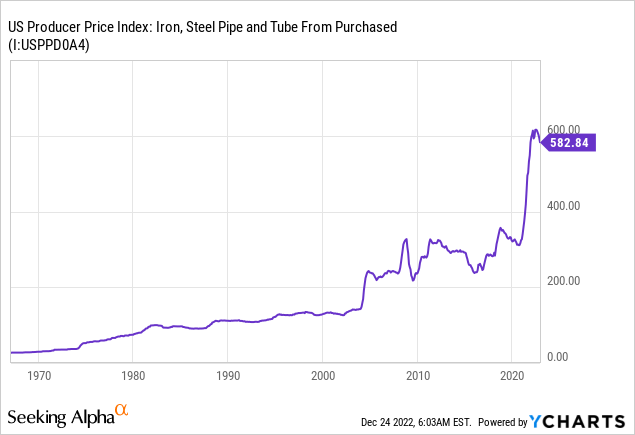

Domestic OCTG producers are reporting record results for their tubular business as domestic OCTG prices are at their highest level ever. In general, the price of OCTG steel tends to be volatile and can fluctuate significantly over time. Prices for oil country tubular goods (OCTG) steel are influenced by a range of factors, including demand for oil and gas, the level of drilling activity, the strength of the global economy, and the availability of steel in the market.

The U.S. Producer Price Index for iron, steel pipes and tubes from purchased steel has risen sharply since the corona crisis but is off from recent highs and is on a downward trend.

The total addressable market (TAM) for OCTG (Oil Country Tubular Goods) is the total demand for OCTG products within a specific market or industry.

According to market research firm Market Data Forecast, the global OCTG market is expected to grow at a compound annual growth rate of 6.7% between 2022 and 2027, reaching a market size of $31.9 billion by 2027. This growth is driven by increasing demand for oil and gas, particularly in emerging markets, as well as a growing focus on renewable energy sources.

Sales Up 70% Year-On-Year

Third Quarterly Highlights (Tenaris third quarterly results)

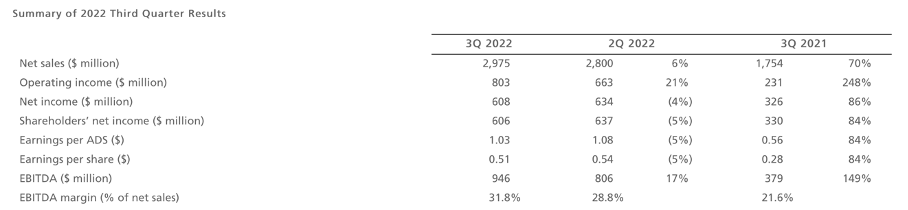

In the third quarter of 2022, Tenaris reported sales of $2,975 million, up 6% from the previous quarter (and up 70% from the same quarter last year). The increase was primarily due to favorable pricing that more than offset lower deliveries, which were impacted by lower deliveries to pipeline projects and seasonal factors.

Total tube volumes fell 4% sequentially but increased 15% year on year. Seamless tube volumes fell 8% sequentially, which was partially offset by a strong 41% sequential increase in welded tube volumes.

EBITDA rose to $946 million, up 17% from the prior quarter and 149% from the same quarter a year ago. The rise in average selling prices offset the rise in raw material and energy costs, resulting in a substantial increase in EBITDA and a higher EBITDA margin of more than 30%.

Although net income fell by 4% sequentially, it rose by 86% when compared to the same time previous year. The decrease was due to non-operating items such as greater financial expenses and lower results from equity participation in non-consolidated companies (Ternium and Usiminas).

Despite an increase in working capital of $601 million due to a building of inventory in expectation of greater shipments and an increase in receivables, free cash flow for the quarter remained positive at $113 million. Tenaris boosted capex, which included $56 million for the wind farm in Argentina. The balance sheet is strong: net cash position has improved from $268 million at the beginning of the year to $700 million now.

Due to declining revenues and free cash flows in fiscal 2020, management decided to significantly reduce the dividend per share. The dividend per share is currently increasing and stands at $0.68 per share, representing a dividend yield of 1.9%.

An Annual Pre-Tax Return Of 16% Can Be Expected

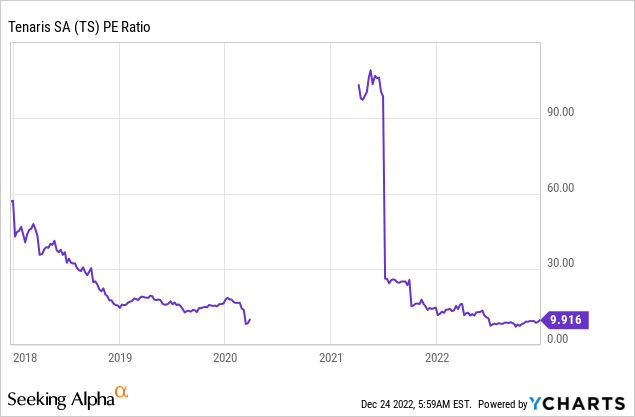

The P/E ratio is a commonly used financial ratio to gain insight in the valuation of a stock. It compares a company’s current share price to its earnings per share.

Tenaris’ P/E ratio currently stands at 9.9, indicating that the company is cheaply valued compared to the S&P 500, which has a ratio of 20. The discount is due to the volatile sector in which Tenaris operates. Moreover, steel production is a very capital-intensive process and OCTG prices can fluctuate widely. Therefore, profits tend to be volatile, resulting in a sharp discount to the stock price.

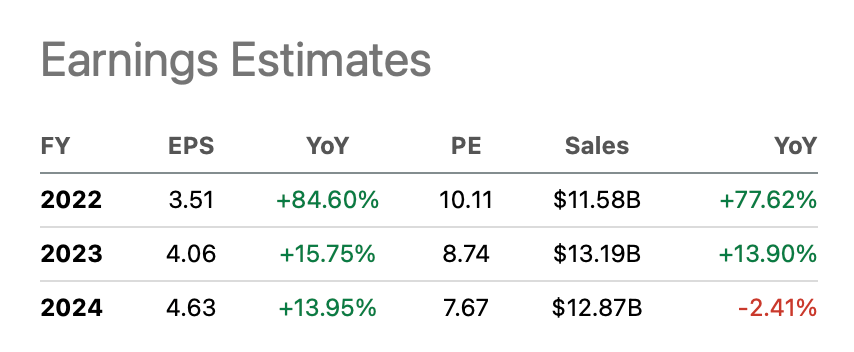

Tenaris is valued in line with its historical averages with a P/E ratio of about 10. Analysts expect strong growth in earnings per share and sales in the coming years. For fiscal year 2024, earnings per share are expected to be $4.63. If we multiply this figure by the average P/E ratio of 10, we arrive at a share price of $46.30 at the end of 2024. This implies a strong return of 30% (14% annualized), including dividend yield the average annual pre-tax return would be 16%. The stock is clearly undervalued given its strong growth prospects.

Tenaris earnings estimates (Seeking Alpha TS ticker page)

Risks Worth To Mention

Tenaris, like any other company, faces a variety of risks that could have an impact on its operations and financial performance.

Tenaris faces the following key risks:

- Market risks: The demand for steel pipes and other products is highly dependent on the oil and gas, energy, and infrastructure industries, which can be affected by a range of factors such as economic conditions, political instability, and changes in regulations.

- Financial risks: Tenaris’s financial performance can be impacted by factors such as exchange rate fluctuations, changes in commodity prices, and the availability of financing.

- Environmental risks: The production of steel pipes and other products can have environmental impacts, and Tenaris is exposed to risks related to environmental regulations, as well as the potential for environmental accidents or damage.

Key Takeaway

Some key points from my article:

- Tenaris is a global company that specializes in the production and supply of steel pipes and related services for the oil and gas, energy, and infrastructure industries.

- The stock was upgraded by many analysts because of its strong position in the growing market for oil country tubular goods.

- The global OCTG market is expected to grow at a compound annual growth rate of 6.7% between 2022 and 2027.

- In the third quarter of 2022, Tenaris reported sales of $2,975 million, up 6% from the previous quarter (and up 70% from the same quarter last year).

- The rise in average selling prices offset the rise in raw material and energy costs, resulting in a substantial increase in EBITDA and a higher EBITDA margin of more than 30%.

- In the upcoming years, analysts predict that sales and earnings per share will expand rapidly. The estimated earnings per share fiscal 2024 is $4.63.

- Investors can expect an annual pre-tax return of 16%. Given the stock’s strong growth prospects, it is clearly undervalued.

Be the first to comment