filadendron

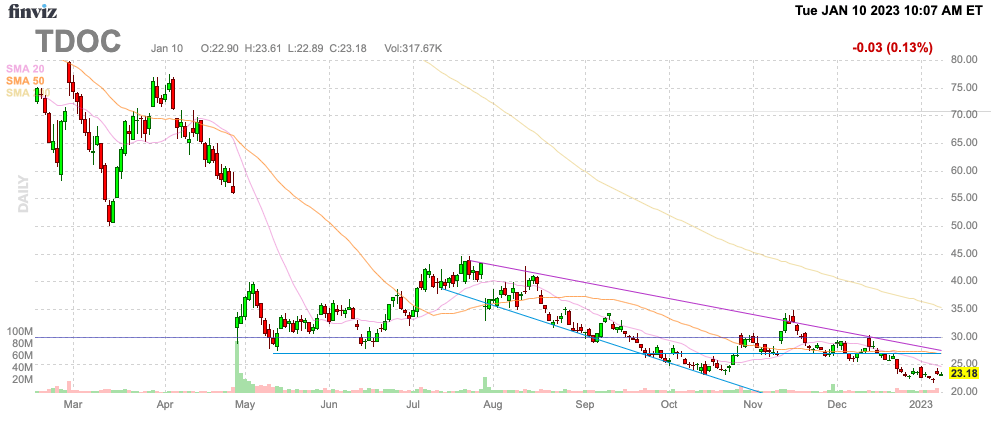

The digital health sector has been decimated this last year as the end of covid fears has reduced the demand for telehealth services just as the capital flowed into new products and services for the sector. Teladoc Health (NYSE:TDOC) remains the primary category leader providing an opportunity to invest in the leader on general sector weakness that will ultimately wipe out competition. My investment thesis remains ultra-Bullish on the stock trading below $25, some 50% below pre-covid levels.

Source: FinViz

Surprise Beat

The virtual health provider upped guidance for Q4 heading into their J.P. Morgan Healthcare conference. Teladoc Health didn’t up guidance materially, but the market was surprised with the company actually beating estimates as other companies cut guidance following the end of the quarter.

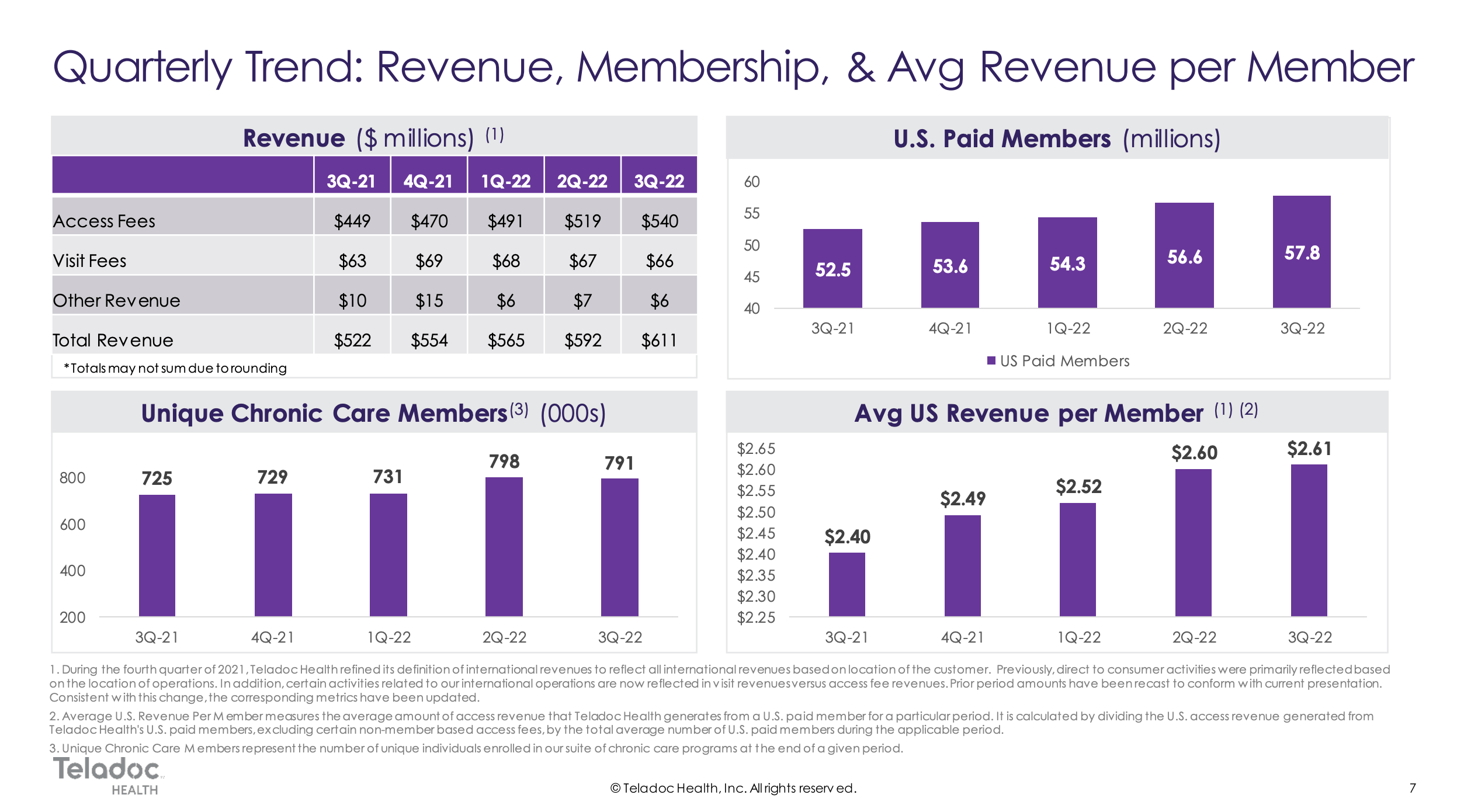

The telehealth firm forecasts Q4’22 revenues now reaching $633 to 640 million. Teladoc Health generated $611 million in revenues in Q3 and has boosted sequential revenues at an ~$20 million clip over the last few quarters from adding additional members and boosting the revenue per member.

Source: Teladoc Q3’22 presentation

At the J.P. Morgan conference, management provided indications that some of the competitive spirits in the market are likely to end. The BetterHelp mental health business has already reached $1 billion in annual revenues and competitors aren’t likely to continue throwing away money on marketing:

And we’ve talked as we have gone through the year about the pressures on ad spend, et cetera., in the marketplace. Certainly, there has been an explosion of capital going into overall digital health, but certainly in the mental health space.

And several of the companies who have operated in this space certainly have plowed a lot of capital into digital — into ad spend. And listen, we’ve also seen some bad actors in the space who have taken advantage of the suspension and regulations to sort of aggressively promote controlled substances.

Teladoc Health didn’t provide any guidance for 2023 where the competitive pressures should dissipate when the likes of Amwell (AMWL) trade at only $3 and continues to generate the type of losses that aren’t sustainable.

More Profitable Than You Think

A key aspect of the current market is the shift in preferring investing for growth to investing in profits. This mantra of focusing on GAAP profits has caused the market to overshoot on the downside with companies like Teladoc with large non-cash charges causing the company to report quarterly GAAP losses.

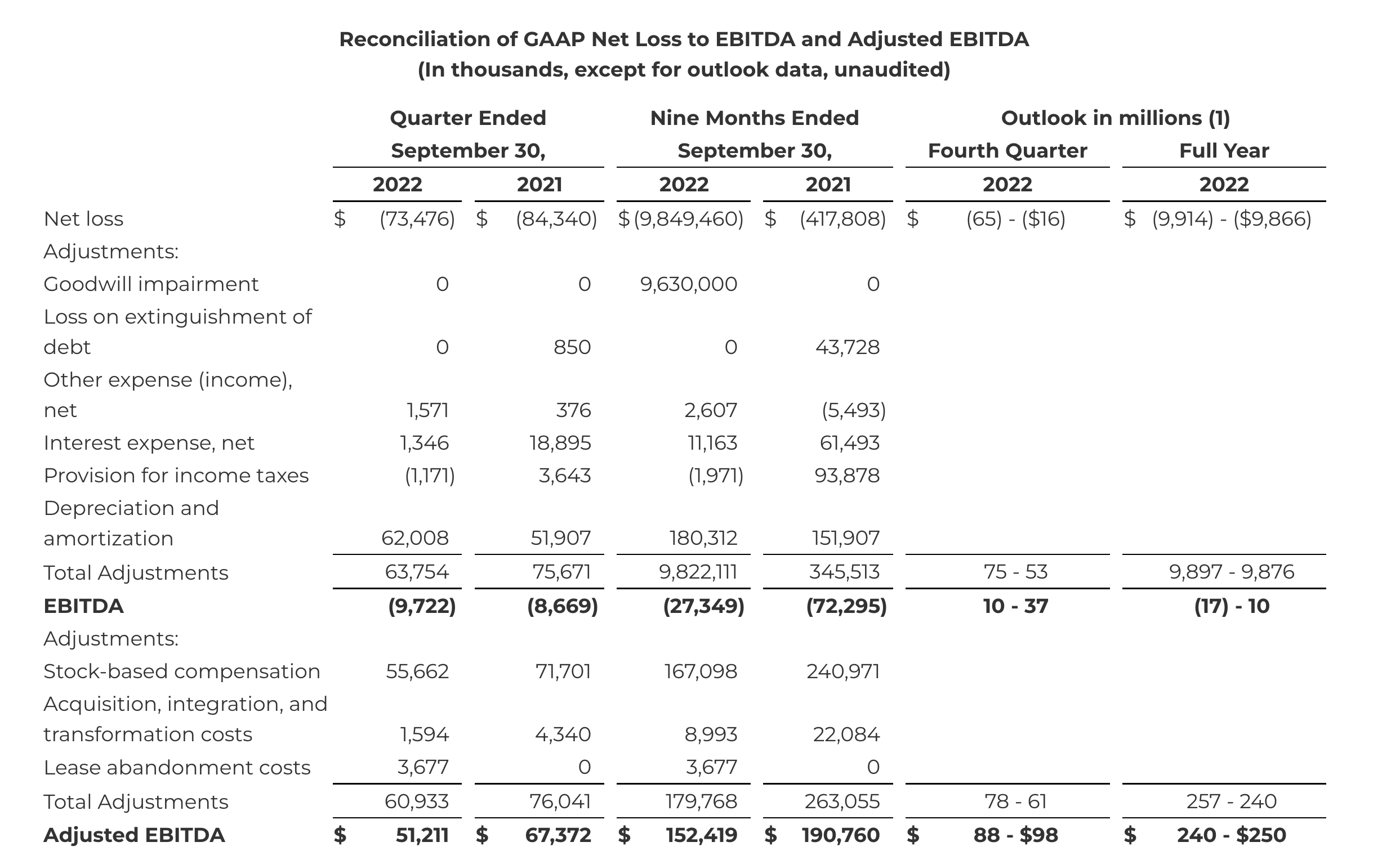

For Q3’22, Teladoc Health had a net loss of $73.4 million, but the company actually reported an adjusted EBITDA profit of $51.2 million. Investors tricked by the market to shift investment metrics from a focus on growth or EBITDA profits to now focusing on GAAP profits will get whipsawed by the stock market.

Investors need to understand what metrics impact EBITDA. For Teladoc, the vast majority of the difference between the $73.4 million net loss in Q3’22 and the EBITDA loss of $9.7 million are the depreciation and amortization charges of $62.0 million.

Source: Teladoc Q3’22 earnings release

To get to the adjusted EBITDA profit of $51.2 million, investors strip out stock-based compensation of $55.7 million and acquisition and restructuring related costs of $5.3 million. The real expenses excluded via this calculation are the minimal interest expenses of $1.3 million and however much of the depreciation charges are related to actual assets and not intangibles and goodwill.

Clearly, investors should be confident in utilizing the adjusted EBITDA figure. Teladoc forecasts the company earning up to $250 million in adjusted EBITDA for the year while the stock only has a market cap of $3.8 billion. Teladoc Health has boosted EBITDA margins by 400 basis points in the last 3 years, yet the stock trades at half the stock price now.

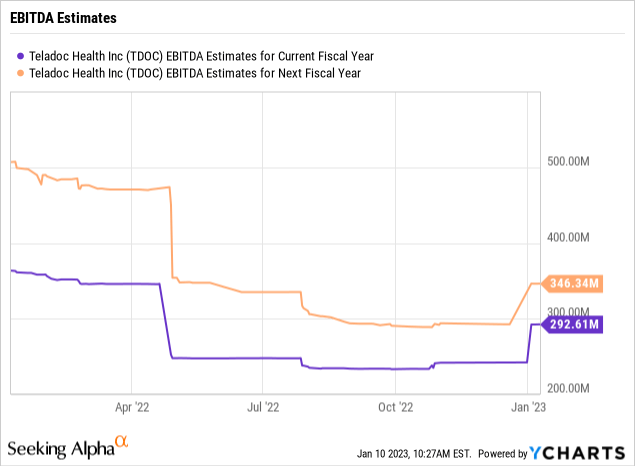

Teladoc Health only trades at 15x adjusted EBITDA for 2022 that nearly mimics adjusted profits for a business forecast to continue growing at a 20%+ clip. The company doesn’t even produce strong margins yet providing tons of upside potential with analysts forecasting a boost in adjusted EBITDA in 2023 to $293 million.

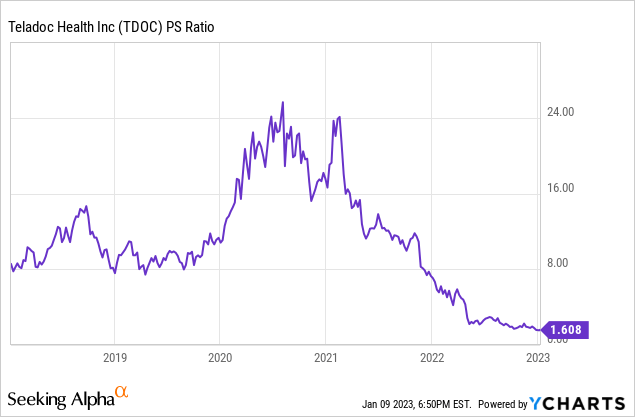

While not preferring the backwards looking P/S ratio for valuing stocks, this chart provides an indication of how Teladoc Health trades at a far lower multiple of sales now. The stock surged to unsustainable levels in 2020, but Teladoc regularly traded around 5x forward sales estimates and in excess of 8x trailing sales compared to below 2x trailing sales now.

Takeaway

The key investor takeaway is that Teladoc has a far bigger business now trading far below pre-covid levels. The stock is poised to rally off the lows here after the telehealth leader reported a solid end to 2022 and the stock is cheap based on adjusted profits.

Be the first to comment