imaginima

Intro

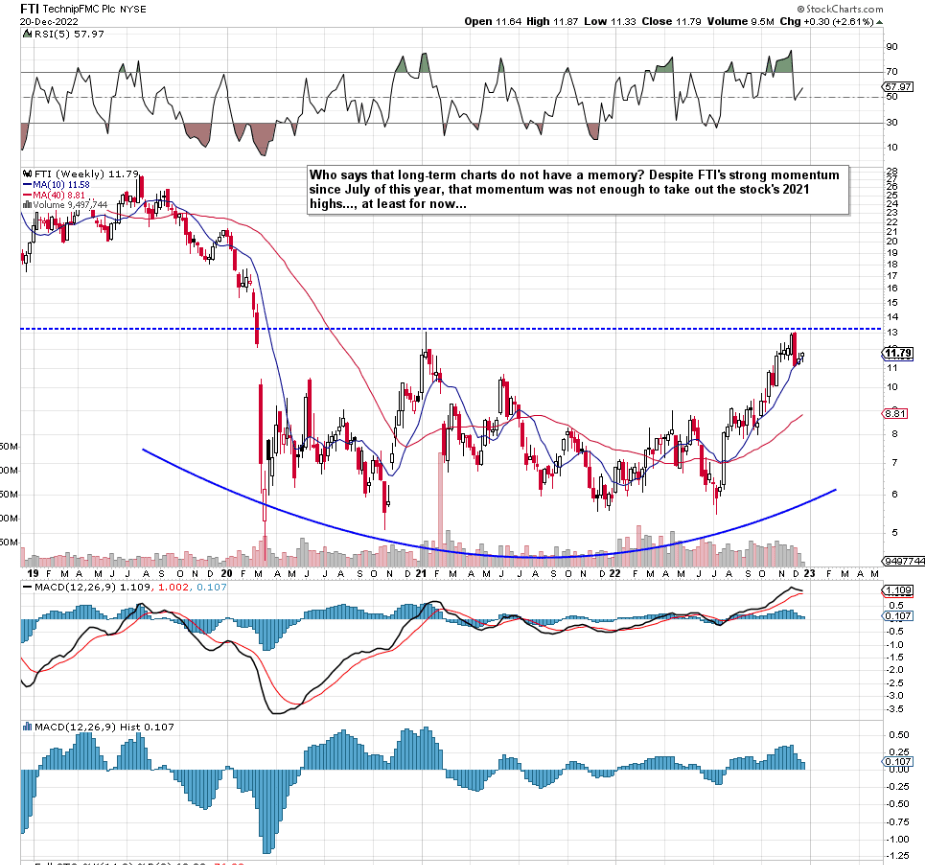

If we pull up an intermediate chart of TechnipFMC plc (NYSE:FTI) (International Oil & Gas Equipment Supplier), we can see that shares have been literally on the rampage since July of this year. Shares initially bottomed in March 2020 and have been undergoing what appears to be a bottoming pattern since that date. However, technical analysis deniers should look at where shares lost their upward momentum in November of this year. As we can see from the chart, shares could not break through their 2021 highs and now remain down roughly $1 a share from their recent November highs.

History repeats itself many times in the financial markets and this can be seen especially on longer-term charts where trends in investor phycology and sentiment (Which in the main do not change) can be more readily seen due to far more information being at the chartist’s disposal. Therefore, the question now is whether momentum can be regained in TechnipFMC so another attempt can be made to take out that overhead resistance as we see below. The first battle the company faces is to remain above its 10-week moving average of $11.58 which is less than 2% below the prevailing share price of TechnipFMC at present. However, if near-term quarterly earnings revisions continue to contract as they have been doing, the possibility of a breakout looks remote at this present moment in time.

FTI Technical Chart (Stockcharts.com)

Q3 Momentum

Remember that the trajectory of the share price of any respective company is determined by the relationship with the company’s profitability trends as well as its valuation. Management recently put forward a vote of confidence in the share price at these levels by buying back $50 million worth of stock plus it also committed to the introduction of a dividend in 2023 due to much improved cash-flow numbers in fiscal 2023.

Current trends are all based on what is expected to come down the track both in the Subsea segment as well as Surface technologies. Both segments continue to show promise with Subsea’s Adjusted EBITDA up 4% in Q3 over the second quarter due to stronger margins and an accelerated pace of activity. Surface Technologies on the other hand grew Adjusted EBITDA by an excellent 26% primarily due to Middle east projects continuing to gain traction for the firm.

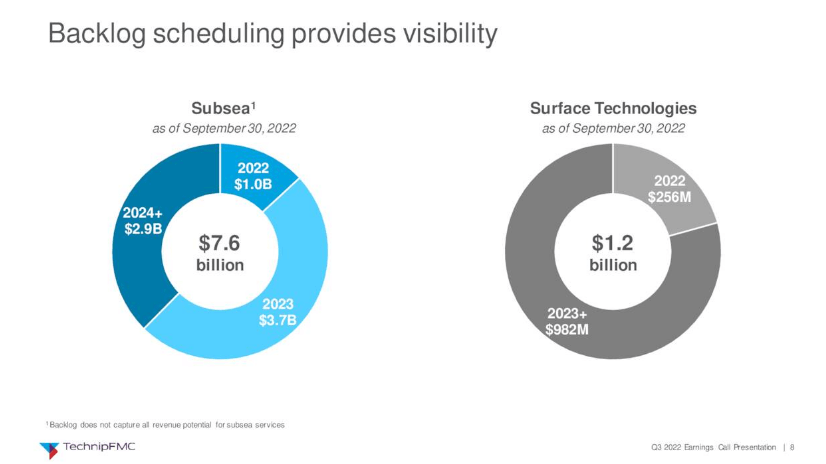

Suffice it to say, when we see the level of the company´s backlog below, TechnipFMC has almost $9 billion of confirmed work ahead of it where the company hopes the market (being a predictive mechanism) will reward the stock now for work which will be duly carried out. Furthermore, margins are not set in stone here so sustained margin gains (Which have been happening) will bring in higher EBITDA numbers than originally envisioned. Confirmed orders of $1.9 billion in Q3 ($1.4 billion in Subsea) increased the year-to-date backlog to an impressive $5.2 billion which in fact is a higher dollar amount compared to the full four quarters of fiscal 2022.

TechnipFMC Backlog (Q3 Company Presentation)

Near-Term Earnings Expectations On the Wane

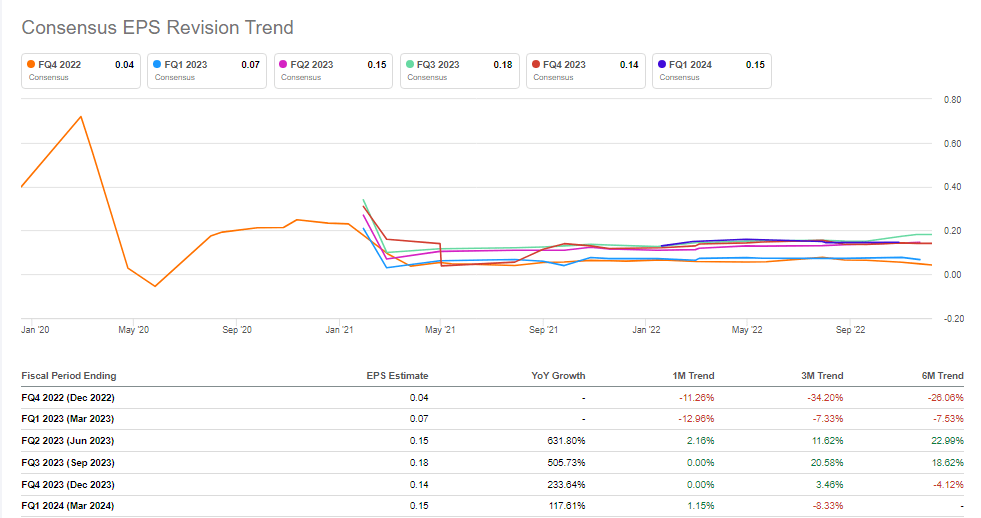

However, if we go back to our initial pretense about how profitability & valuation trends are intertwined when deciphering share-price direction, one must also attempt to ascertain how QUICKLY TechnipFMC’s profitability can change for the better. Management for example alluded to the much improved free-cash-flow numbers expected next year on the Q3 earnings call. However, as we see below, if near-term earnings projections continue to disappoint, free cash flow will not be as high as originally expected. Free cash flow and its associated growth are the most important metrics when gauging a company’s profitability. The higher these metrics can get to, the faster TechnipFMC can grow from sustained re-investment in the right places.

TechnipFMC Earnings Revisions (Seeking Alpha)

Conclusion

From a growth standpoint, there is no doubt that TechnipFMC´s fundamentals remain strong both in the Subsea segment as well as in Surface Technologies. Offshore oil & gas projects continue to gain traction as can be seen from the almost $7 billion estimate management has earmarked for Subsea orders this year. Furthermore, Surface Technologies’ Aramco orders have ramped up of late and the sustained shift to renewable alternatives should continue to increase the company´s backlog in this segment over time.

How fast these projects will be delivered however is another question entirely. Investors should remember that TechnipFMC still has over $2 billion of receivables on its books which demonstrates the difficulty of turning over profits quickly in this industry. Let´s see what Q4 brings. We look forward to continued coverage.

Be the first to comment