ChrisHepburn

Published on the Value Lab 2/7/23

TeamViewer (OTCPK:TMVWF) created an out for its Manchester United (MANU) sponsorship agreement which was the first potentially positive news for the company. Just now the earnings release continues to pile on the good tidings with TeamViewer still accomplishing growth despite pressures on headcounts in tech and slowdowns in tech and remote spending after the COVID-19 boom. In particular, the data points to continued performance in the AR line of products, which drives the higher value TeamViewer businesses. As the multiple continues to look compressed considering the excessive marketing spend on MANU and the continued growth, we see why the markets are responding so positively today to TeamViewer results.

A Look at the Q4

At the beginning of the year, TeamViewer had no problems producing growth. The AR product Frontline was seeing uptake among large customers with very reputable manufacturing businesses, and we were seeing margin expansion and clear billings and sales growth. With the onset of the rate hiking cycle, markets became concerned about the spending in tech and the potential reversal of remote work trends as the ball returned to the employers’ court. However, this didn’t really happen. While tech companies have been known to see slowing sales cycles over the last couple of quarters, TeamViewer’s momentum barely broke, and this latest quarter shows acceleration in billings growth and continued momentum in terms of pricing.

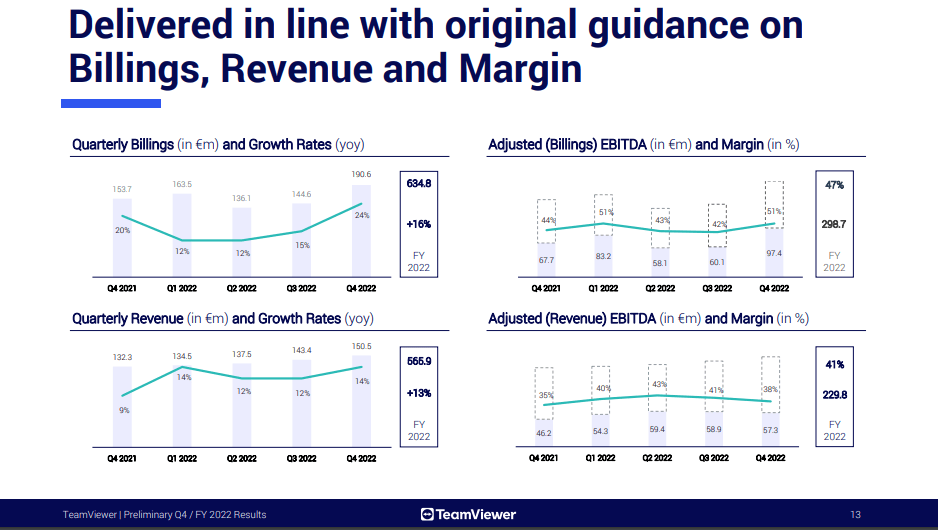

Highlights (Q4 2022 Pres)

Margins see year on year expansion and EBITDA sees substantial YoY growth of almost 50% for the last quarter. With quarterly data so important right now as it indicates the direction of the business at the confluence of a host of factors affecting macroeconomics, this uptick just now bucks the trend and gives an optimistic view on the company.

Billings growth was primarily concentrated around large customers and it was also driven by volumes and not pricing. Enterprise is where the growth is happening, and average selling prices are holding but billings are growing more than 33% in Q4.

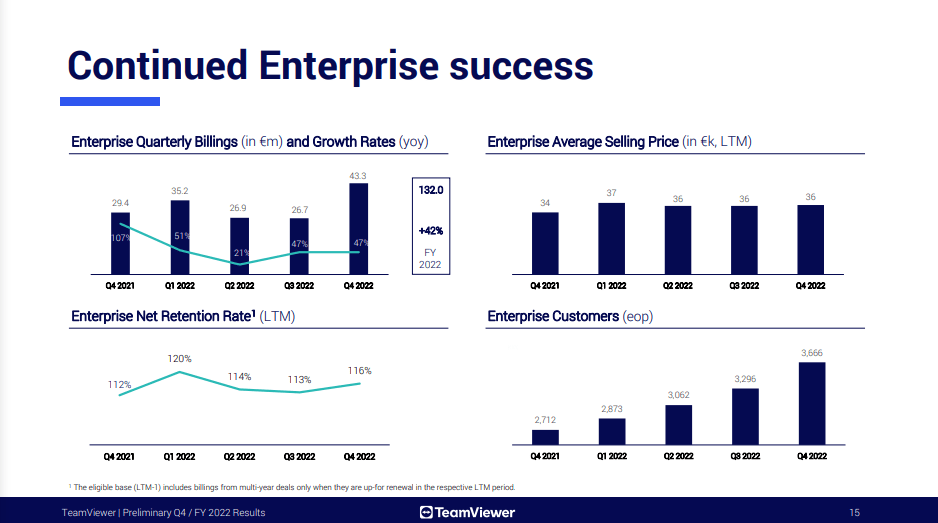

Enterprise Growth (Q4 2022 Pres)

At the end of 2021, AR billings was about 13 million EUR in Q4, but with the addition of customers like Ford (F) and ABB (ABB) this year, but also the conversion of new customers in logistics, with Siemens (OTCPK:SIEGY) and with Hyundai (OTCPK:HYMLF), the quarterly billings levels are probably higher, easily at around 20 million EUR as the company had disclosed in prior calls that around 50% of new orders in enterprise are coming from AR. This isn’t a huge jump from prior levels considering the scope of growth in the category, and is consistent with previous management disclosure. Moreover, the higher than expected factory orders and health in the German industrial system signals positively for TMV’s major markets in Europe within enterprise and OT.

Bottom Line

Cash conversion continues to be decent at around 61% FCFE on billings-based EBTIDA and 75% on revenue-based EBITDA. The multiple remains low at around 8x EV/EBITDA, and with both growth in billings but also a potentially 2500 bps expansion to EBITDA margins possible if the MANU partnership comes to an end, this multiple seems excessively low. A great AR business is growing in the sales mix, and the company is moving further and further away from dependence on its lower value remote access services. Enterprise is generally on the more cutting edge side, and it’s increasing substantially in the mix at around 30%, with AR being around 15%. While the SMB business is less exciting, and also more commodified, the growth is still there. The company appears to be a good growth proposition at a reasonable price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment