PonyWang

Taiwan Semiconductor Manufacturing (NYSE:TSM) just released its fourth quarter earnings and beat expectations. Earnings per share (“EPS”) came in at $1.82 vs. $1.77 expected, while revenue came in at NT$625.53 ($20.54 billion) vs. $20.92 billion expected. It was a very strong release from a company that fell 40% in the 2022 tech crash, thanks mainly to the weakness of other semi names in the same period.

We got some indication of how TSM would do in the fourth quarter a few days before its release came out. On January 10, the company revealed that it had brought in NT$192.56 billion ($6.53 billion) in revenue in December, up 23.9% year-over-year but down from the previous quarter. Bloomberg calculated that sales would come in at NT$636 billion ($20.88 billion) based on this-a miss.

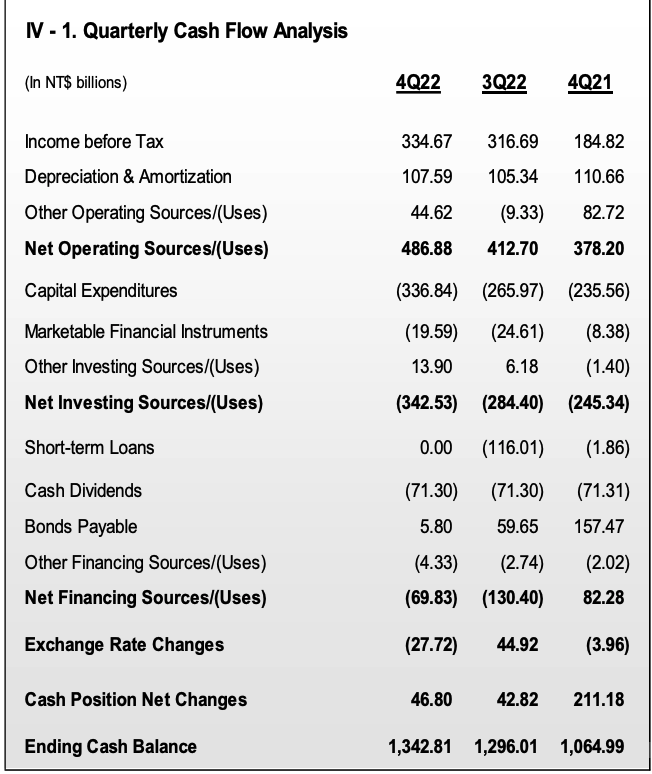

Given what we already knew, TSM’s earnings release was much better than expected. Revenue missed, but earnings came in stronger than expected, and operating cash flow increased 28%.

TSM cash flow analysis (Taiwan semiconductor)

Free cash flow was another standout metric in the quarter. At $4.93 billion, it improved by $110 million from the prior quarter. Total free cash flow for the year was $17.33 billion, a significant improvement over the previous year. Guidance was for $16.7 to $17.5 in first quarter revenue, a 14.3% sequential decline but a 16% year over year increase.

These results compare extremely well to those of other semiconductor companies. In its most recent quarter, Micron’s (MU) revenue declined 47% year over year. NVIDIA (NVDA), for its part, reported a 17% decline. It’s impressive that TSMC is still guiding for modest full year growth in this environment, as many similar companies are already seeing revenue decline in 2022. Micron is guiding for actual losses for the next few quarters.

What we saw in this earnings release lines up pretty well with what I wrote in my latest article on TSMC. When I last checked in on it, I said that TSMC was a high moat company with a strong competitive position. The fact that it’s both profitable and growing in this environment is what you’d expect of a company that’s better than most of its peers.

I started buying TSM stock earlier this year when I noticed that the company’s sales were holding up much better than those of other semiconductor companies. The fourth quarter release convinced me that TSM will continue to do better than its sector. For this reason, I consider the stock a buy, and intend to add more of it.

Competitive Landscape

A big part of my thesis on Taiwan Semiconductor has to do with its competitive position.

A company can have strong growth, a modest valuation and high margins, but all of those things can change if its competitive picture isn’t good. So, let’s look at the competitive advantages that TSMC has going for it.

First things first, it has few major competitors. Its main rivals in the foundry business are Intel (INTC) and Samsung (OTCPK:SSNLF); it enjoys a 60% share of its market, with its two biggest competitors sharing the rest.

Can TSM be reasonably expected to maintain this lead?

If capacity is any indication, then the answer is yes. Taiwan Semiconductor’s capacity is currently 2.7 times greater than that of Samsung, and its revenue is 105 times that of Intel’s foundry. So Samsung will need to invest heavily in property plant and equipment (“PPE”) if it wants to catch up with TSM, while Intel’s revenue indicates that it is in the same boat.

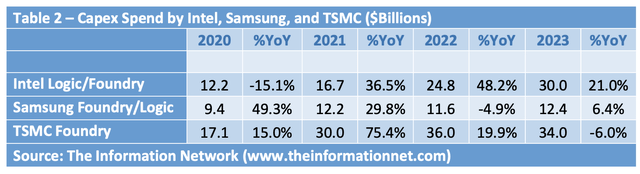

Sheer cost is one big reason why it’s difficult to catch up with Taiwan Semiconductor in foundry services. Manufacturing advanced chips requires expensive ASML Holding (ASML) machines that cost between $160 million (DUV machines) and $400 million (next gen EUV). TSM has 35 EUV machines, costing $200 million on average. So, you’d need $7 billion just to get your hands on the EUV machines needed to beat TSMC in its market. That’s on top of the training, supply chain and management expertise you’d need. Now of course, a company that’s already in the foundry space like Samsung is part of the way there, but with roughly one third of TSM’s Capex spend, it doesn’t appear on track to close the gap.

Capex spend (The information network)

Implications of the Latest Release

There are some conclusions we can draw from TSM’s fourth quarter earnings release. Among the most obvious are:

-

It has among the fastest growth rates in the semi space. Micron, NVIDIA and Intel have all seen revenues decline, TSMC is still growing by high double digits.

-

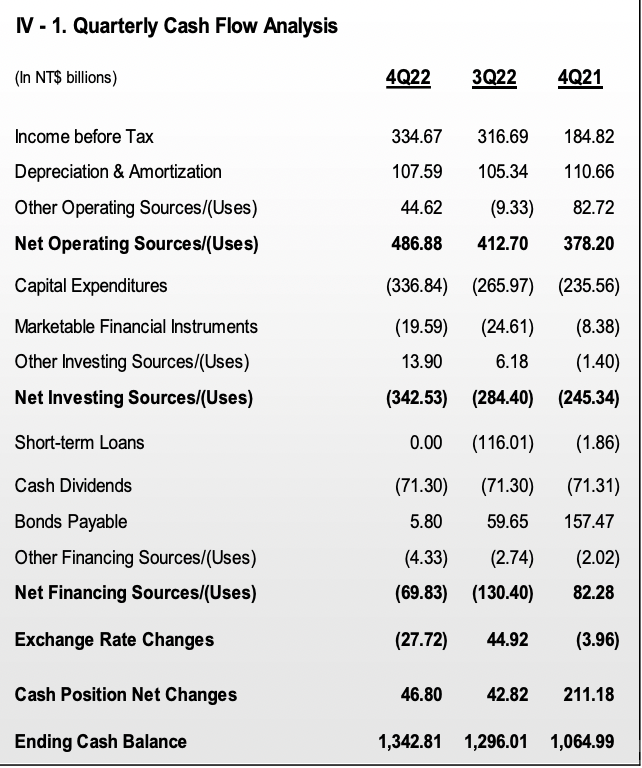

It has high margins. For example, the gross margin is 62%, the operating margin is 62%, and the net margin is 47.3%.

-

The EBIT payout ratio is only 21%.

TSM cash flows (Taiwan Semiconductor)

So, we have a solidly profitable, fast growing company with a low dividend payout ratio. It looks like a good picture, but can this continue?

To know whether TSM’s good results can continue, we need to understand why it is performing so much better than its competitors. Semiconductors in general aren’t doing great now, something Taiwan Semiconductor is doing is bucking the trend.

First, its dominant market position gives it pricing power. As mentioned previously, TSM has much more market share than Samsung or Intel, and it is the only supplier to Apple. A company with that kind of share and exclusivity rarely faces clients demanding lower prices.

Second, it is not a commodity vendor. Earlier, I highlighted Micron’s weakness compared to TSM, which is due to the fact that RAM is a commodity while chip manufacturing isn’t. Apple relies on Taiwan Semiconductor to manufacture its A-series chips, making it a vital and indispensable component of the supply chain, not a fungible commodity. Apple doesn’t stockpile A16 Bionic chips and then find itself with too many: it orders what it needs, when it’s needed.

Third, it doesn’t specialize in just one market segment. TSM has 535 customers worldwide, spanning a variety of tech industry segments. Gaming, data center, smartphones, you name it-Taiwan Semiconductor is involved. This is in contrast to NVIDIA which makes a huge percentage of its revenue from gaming which happens to be declining right now.

So, basically, TSM looks stronger than its competitors because it doesn’t have the specific weaknesses inflicting them at the moment. Therefore, this comparative strength looks like it could continue.

Valuation

Having looked at Taiwan Semiconductor’s earnings and competitive position, we can turn to its valuation.

At today’s prices, TSM trades at:

-

13.9 times earnings.

-

5.5 times sales.

-

4.8 times book value.

-

8.75 times operating cash flow.

The operating cash flow multiple is extremely low, suggesting undervaluation. Now, if we look at Seeking Alpha Quant’s ttm cash flow statements, we see that free cash flow is way, way behind operating cash flow for Taiwan Semiconductor. This is due to enormous amounts of capital expenditure. When you invest money into PPE, it’s taken off of free cash flow, because cash spent on equipment or a facility is not “free” to be distributed to shareholders. However, it does create assets and future earnings power if it’s spent wisely. So, I would say that TSM’s valuation is modest on the whole.

One Big Risk to Watch Out For

If you choose to invest in Taiwan Semiconductor Manufacturing, there is one risk you’ll want to watch out for:

Geopolitical risk.

Many people believe that China will someday invade Taiwan. China’s President Xi Jinping has indicated that he could use force as a “last resort” should foreign nations interfere with his planned unification with Taiwan. He has never said what his “red lines” are for determining that an invasion is necessary, which makes the China/Taiwan situation fairly ambiguous. China/Taiwan relations on the whole are ambiguous: the two entities agreed in 1992 that they are part of “one China,” but disagreed on who is in charge of what. It is known that Xi wants to achieve unification with Taiwan, and considers force to be the last resort if peaceful means can’t achieve his ends.

There is some definite risk and uncertainty in this. Xi Jinping wants Taiwan to unify with China, given that other powerful forces don’t want that, it seems possible he’ll be thwarted in his “peaceful unification” efforts and feel compelled to invade. However, the effects of an invasion on Taiwan Semiconductor are not known. Chinese companies would almost certainly be sanctioned, but Taiwan is aligned with the West, so as long as China doesn’t directly attack semiconductor facilities then a war would not be fatal to TSM as a business. The stock market volatility in such a scenario would likely be extreme, though, so know your risk tolerance before buying Taiwan Semiconductor stock.

The Bottom Line

Having looked at its earnings, Taiwan semiconductor stock appears to be a good bet. Its revenue is still rising, unlike that of most semiconductor companies, and even its 2023 guidance isn’t all that bad. It believes it will achieve positive growth for the full year! The picture here is definitely better than with most semi stocks, so if you can stomach China/Taiwan risks, you might benefit from owning TSM stock.

Be the first to comment