vtwinpixel/iStock via Getty Images

Investment Thesis

We previously covered TSM with a Buy Rating in November.

Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) is expected to report FQ4’22 earnings by January. We already know that the company delivered stellar October and November numbers, despite the tougher YoY comparison and supposed PC destruction. October sales showed an increase of 1% sequentially/56.3% YoY, with November further growing by 5.9% sequentially/50.2% YoY.

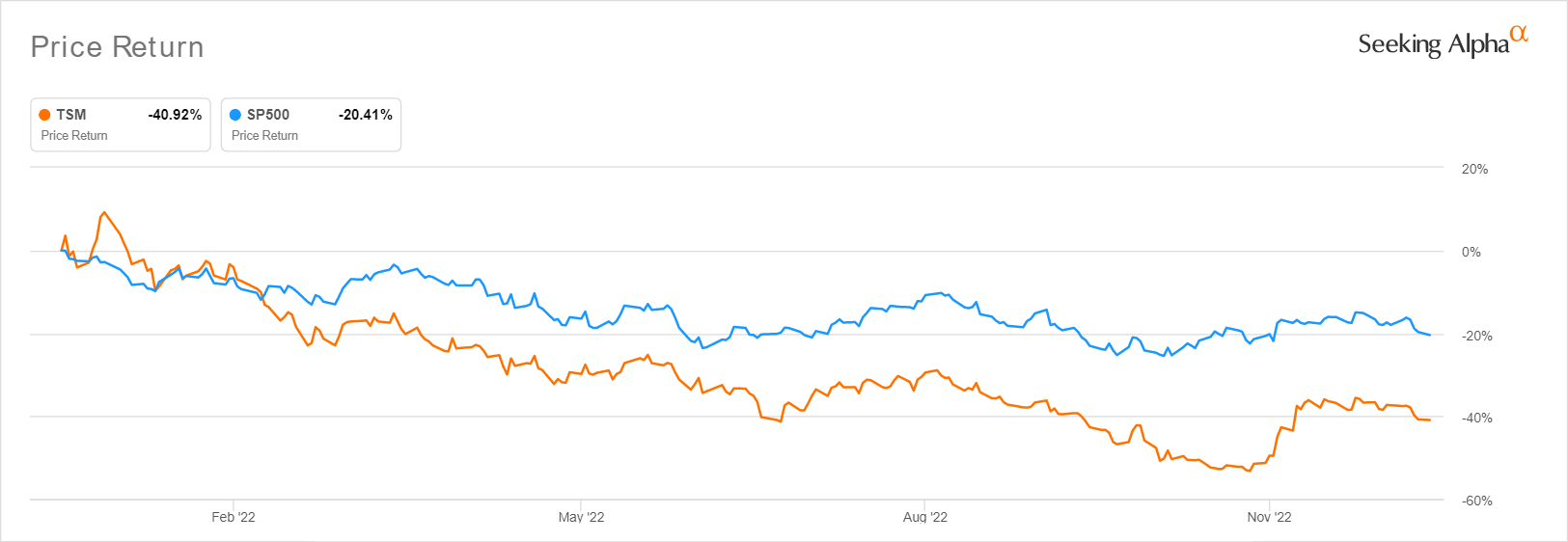

TSM YTD Stock Price

Seeking Alpha

However, the growing geopolitical risks, worsening macroeconomics, and the destruction of PC/gaming/crypto demand have unfortunately aggravated TSM’s stock declines thus far. The stock has suffered a -40.92% plunge YTD, compared to the S&P 500 Index’s fall of -20.41% at the same time. Fellow foundry (or aspiring) peers, Intel (INTC), Samsung (OTCPK:SSNLF), and GlobalFoundries (GFS), were not spared either with a -49.65%, -24%, and -12.98% decline YTD at the same time.

There may be more volatility over the next few quarters as well, depending on how the Chips Ban and personnel restrictions develop. With the newly announced restriction including Yangtze Memory Technologies and 21 “major” Chinese companies in the AI chip segment, TSM may experience sales headwinds from Q1’23 onwards, since China accounted for 10.79% of its revenues over the last twelve months (LTM). Additionally, analysts expect Nvidia (NVDA) to suffer a $400M sales impact before it launches its new Nvidia A800 GPU in compliance with the new export rules. Seeing how the situation is still rapidly evolving, the extreme levels of gloom in the semiconductor market are not surprising indeed.

In the meantime, China seems poised to counter the export restrictions with a 1T Yuan or the equivalent of $143B in support package for its domestic semiconductor industry, against the US at $52B. Even with the supposedly narrowed scope of restrictions amid corporate opposition, there may be more uncertainties in the intermediate term. Investors looking to add TSM should be attentive to this developing risk.

Mr. Market May Be Anticipating A Decline Of Profitability Margins Ahead

Meanwhile, TSM has delivered an impressive expansion of gross and EBIT margins. By FQ3’22, the company recorded a stellar 1.5 percentage point QoQ/9.4 points YoY increase in both gross and EBIT margins, respectively. This has naturally improved its profitability by 18.49% QoQ and 79.75% YoY, while also enhancing its net income margins by 1.4 points QoQ and 8.1 points YoY. This demonstrates the company’s remarkable mastery and strength in the complex global supply chain, regardless of rising inflationary pressures across material and labor costs.

Then again, we reckon these stellar margins are also significantly aided by the low labor costs in Taiwan. Wages in the country average 605.38K TWD annually or the equivalent of $19.72K, based on the exchange rate at the time of writing. On the other hand, TSM plans to begin production in the Arizona plant by 2024, with construction currently ongoing. Wages in Arizona are inherently different at $63.69K annually, indicating a massive 322.97% jump in comparison to Taiwan’s level. These may potentially trigger a notable headwind in TSM’s projected profitability from FY2024 onwards.

GlobalFoundries has reported much lower profit margins indeed, with gross margins of 25.5% and EBIT margins of 12.3% over the LTM. This is not surprising, since the company reported three manufacturing sites in the US, one in Germany, and another in Singapore. All of these come with higher average wages of $54.13K, the equivalent of $50.69K and $51.35K respectively, based on the exchange rate at the time of writing.

Micron (MU) does slightly better, with improved gross margins of 45.2% and EBIT margins of 31.6% over the LTM. However, this is attributed to the company’s eleven manufacturing sites globally across Taiwan, Singapore, Japan, the US, Malaysia, and China. Particularly, a majority of the production output in 2022 was from its fabrication facilities in Taiwan, which may have consequently contributed to the expanded profitability.

However, we choose to be more optimistic about TSM’s intermediate performance in Arizona, since Apple (AAPL) and NVDA are expected to be the first few customers then, with a speculative addition of Advanced Micro Devices (AMD). The latter three have been TSM’s long-term customers, accounting for a significant 33.15% of its revenue in FY2021. Most importantly, these companies have been able to pass on higher costs to their customers thus far, notably expanding their profit margins at the same time.

AAPL recently released the iPhone 14 series, with the Pro and Pro Max version proving highly popular among fans, accounting for 60% of pre-orders against the historical launches at 50%. The superior branding power is truly impressive, due to the eye-watering entry-level price of $999 and $1.09K, respectively. The Cupertino-based company has been able to maintain its premium price tag, despite the tightening of consumer discretionary spending globally. As a result of this phenomenon, it was able to report excellent gross margins of 43.3% and EBIT margins of 30.3% in the LTM, expanding by 1.5 percentage points and 0.5 points YoY, despite the rising inflationary pressures over the past year. In addition, there are already rumors that the iPhone 15 Ultra may come with an even higher starting sales price of $1.29K, further safeguarding the company’s (and likely, TSM’s) profit margins moving forward.

On the same note, NVDA’s gross margins have been stellar at 65% and EBIT margins at 38%, prior to the PC/gaming/crypto headwinds, with AMD similarly recording ~50% and ~21%, respectively. These come as no surprise, considering that they have also been consistently hiking prices. Nvidia GeForce RTX 4090 was priced at $1.59K during its recent launch in 2022, growing immensely by 228.75% since the original launch of Nvidia GeForce RTX 2080 at $699 in 2018. The CEO has notably guided that the high GPU prices are here to stay, due to the “irrelevant Moore’s Law” and rising component costs.

While the TSM management has guided an excellent $10B in annual revenues from the Arizona plant, it remains to be seen if TSM is able to sustain its excellent profit margins. Only time will tell.

In the meantime, we encourage you to read our previous article, which would help you better understand its position and market opportunities.

- Taiwan Semiconductor: Don’t Miss China’s Reopening Discount – Rally Is Sooner Than Expected

- Brutal Market For Taiwan Semiconductor – Another 10% Downside

So, Is TSM Stock A Buy, Sell, Or Hold?

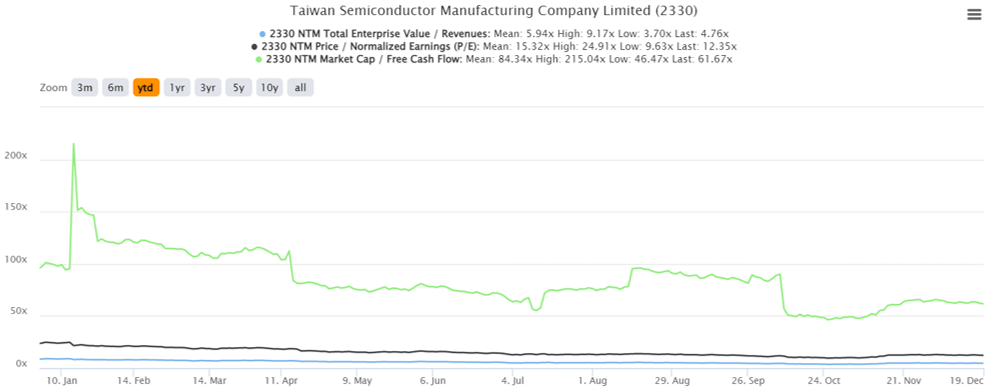

TSM YTD Valuations

S&P Capital IQ

TSM is currently trading at an EV/NTM Revenue of 4.76x, NTM P/E of 12.35x, and NTM Market Cap/FCF of 61.67x, lower than its YTD mean of 5.94x, 15.32x, and 84.34x, respectively. The geopolitical discount is apparent in the moderation seen in its valuations, against its 3Y pre-pandemic P/E mean of 16.67. The pessimism is reflected in the consensus current price target of $98.00 as well, which notably declined by -18.33% from $120 since H1’22. Then again, we reckon the potential decline in its profit margin is already priced in accordingly.

With a 28.78% upside, we believe the TSM stock still looks attractive at its current levels, despite the recent 28.04% recovery from November bottom. The company’s leading foundry market share of 53.4% underscores its intrinsic importance in the semiconductor market, further aided by the diversification of geopolitical risk in Arizona. Hence, we continue to rate the stock as a Buy. Naturally, investors should also size their portfolios accordingly since the stock continues to trade with a notable geopolitical risk.

Be the first to comment