IchigoRider/E+ via Getty Images

Q2: Solid Quarter

Symbotic (NASDAQ:NASDAQ:SYM) delivered mixed Q2 results with revenue beating expectations but EPS missing estimates. The company reported revenue of $424.3 million, a 59% YoY increase, beating consensus by $11 million. However, EPS came in at -$0.07, a miss of $0.03. Company provided Q3 guidance of $450 – $470 million, which was above consensus. Market reaction was mixed, with stock up initially by 10% but then retraced the gains throughout the week.

Symbotic is part of our robotics portfolio, and we have high expectations from the company. The company wants to transform a $1 trillion legacy industry with its fully automated AI and robotics platform. We started our coverage of the company in November 2023 with a buy rating (see below) Symbotic: This Warehouse Transformer Has More Upside

November 2023 Article (Seeking Alpha)

Three months ago, on February 12th, we issued another bullish article after Q1 results, reiterating our Buy rating but lowering our price target due to deployment slowdown. Symbotic: Still A Buy But Price Target Lowered

February 2024 Article (Seeking Alpha)

While the company is showing consistent progress quarter over quarter, its high valuation is keeping the stock price range bounded between $40 and $60 (see below). We believe that Symbotic will break through this range but we don’t know when.

Symbotic Price (Seeking Alpha)

We maintain a long-term view on Symbotic and provide long-term price targets only. In this article, we will analyze the Q2 earnings report and update our valuation accordingly.

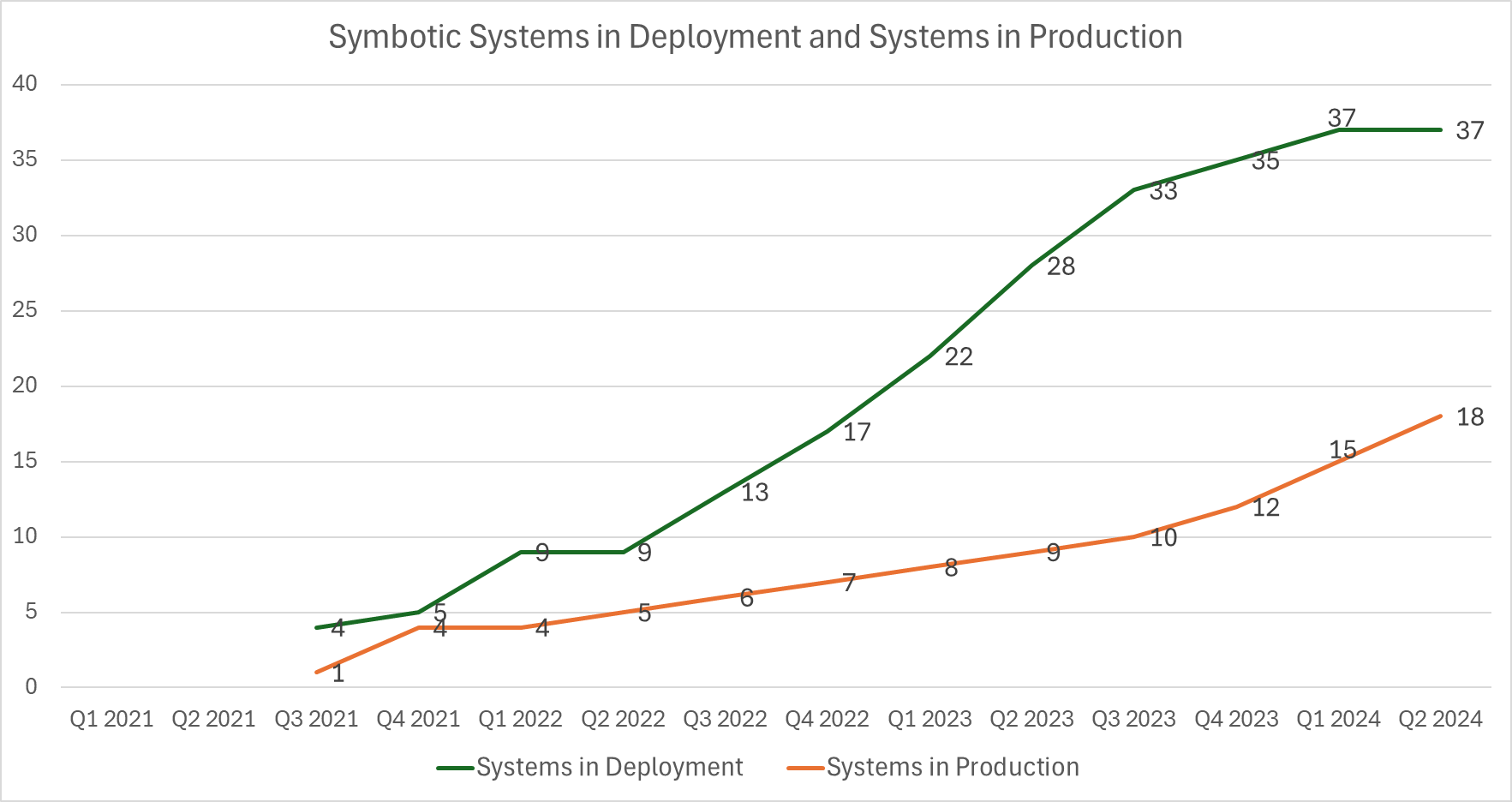

Systems Segment Performance as Expected

Symbotic’s most important KPI is its system deployment performance. We are tracking this metric very closely as it is directly tied to company’s revenue. If the deployments do not scale, we will see revenue slow down, so the total number of systems in deployment is a key metric to watch.

The company completed three new systems during the quarter and started three new deployments. As of Q2, total finished deployments were 18, and ongoing deployments were 37 (see below chart). This is a net increase of six from 15 operational systems and 35 deployments in the last quarter. As a result, the systems segment generated $402 million of revenue in Q2, which is a 56% increase YoY. The systems in deployments stabilized around 37, which was expected due to the standardization upgrades to the systems (this was already guided by the management last quarter). However, management stated in the earnings call that the systems deployments will accelerate again starting next quarter. This is positive news, which means the revenue momentum will stay strong throughout the year.

Systems Performance (Author)

Overall, we think the Q2 system segment results were in line, and the company gave positive deployment outlook for the rest of the year.

Revenue on Track

As we explained in our previous article, Symbotic has a delivery-based revenue model, which has multiple dependencies and risks. In order for the revenue to be recognized, the system deployment projects require coordinated execution between the company, its suppliers, and customers. Any issues or delays with any of these parties can negatively impact revenue.

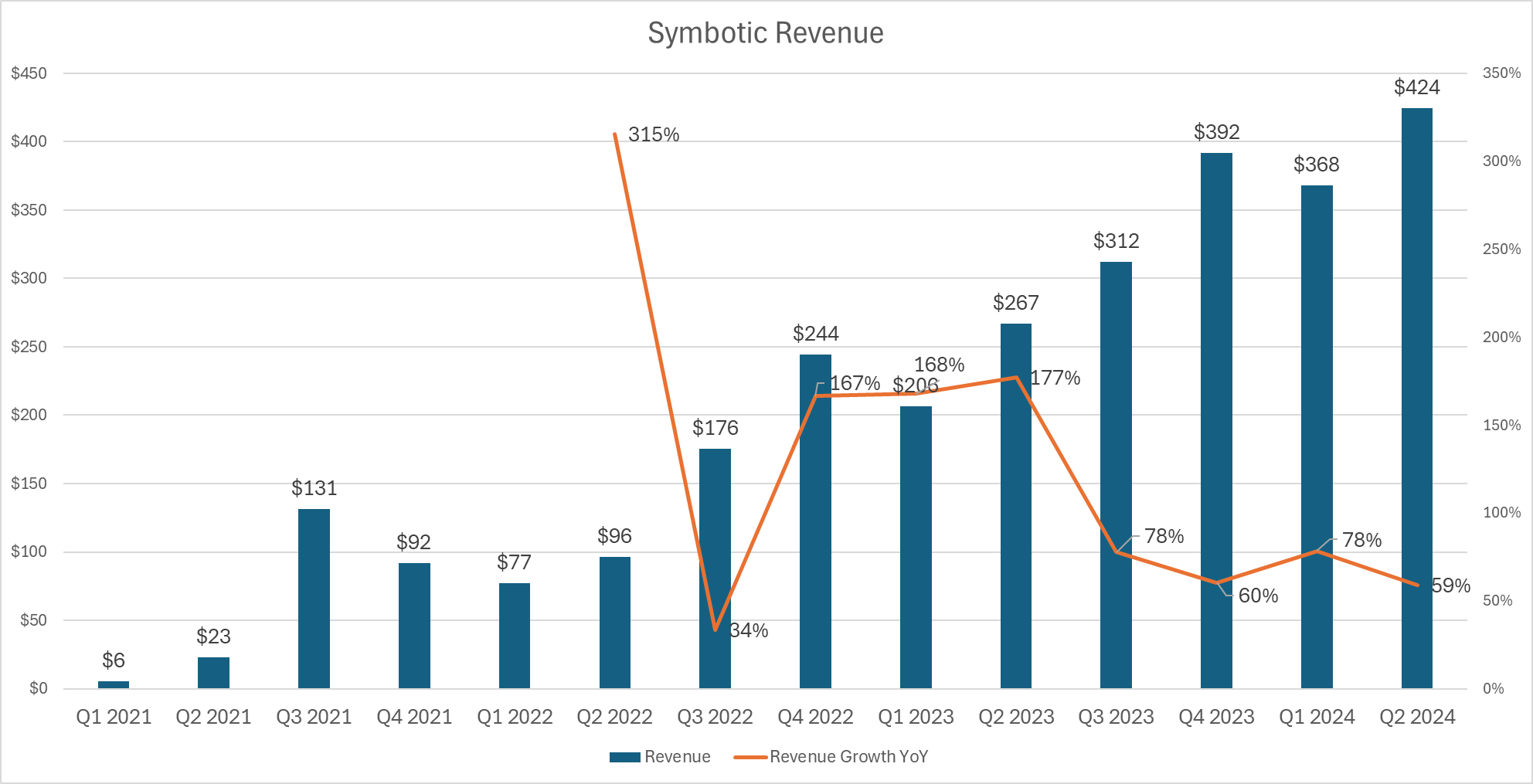

Revenue growth numbers are still fluctuating due to varying deployment sizes and project timings, which is expected(see below). However, the growth momentum is still very strong, and we expect strong revenue momentum in the upcoming quarters due to accelerated system deployments.

Revenue Trajectory (Author)

Operating Metrics Improving

The company continues to show operational improvements on a quarterly basis. Q2 non-GAAP gross margin was 20%, which is in-line with the previous quarter and above expectations. Adjusted EBITDA margin came in at 5.3% compared to 3.5% from last quarter. This was driven by improved operating leverage, accelerated revenue growth and better than expected operating expense. The company also reported a free cash flow of $18 million, which was above expectations.

The company expects gross margin improvements in the upcoming quarters and believes gross margins can go up to 60% levels in the future.

2026 – Long Term Revenue Projection

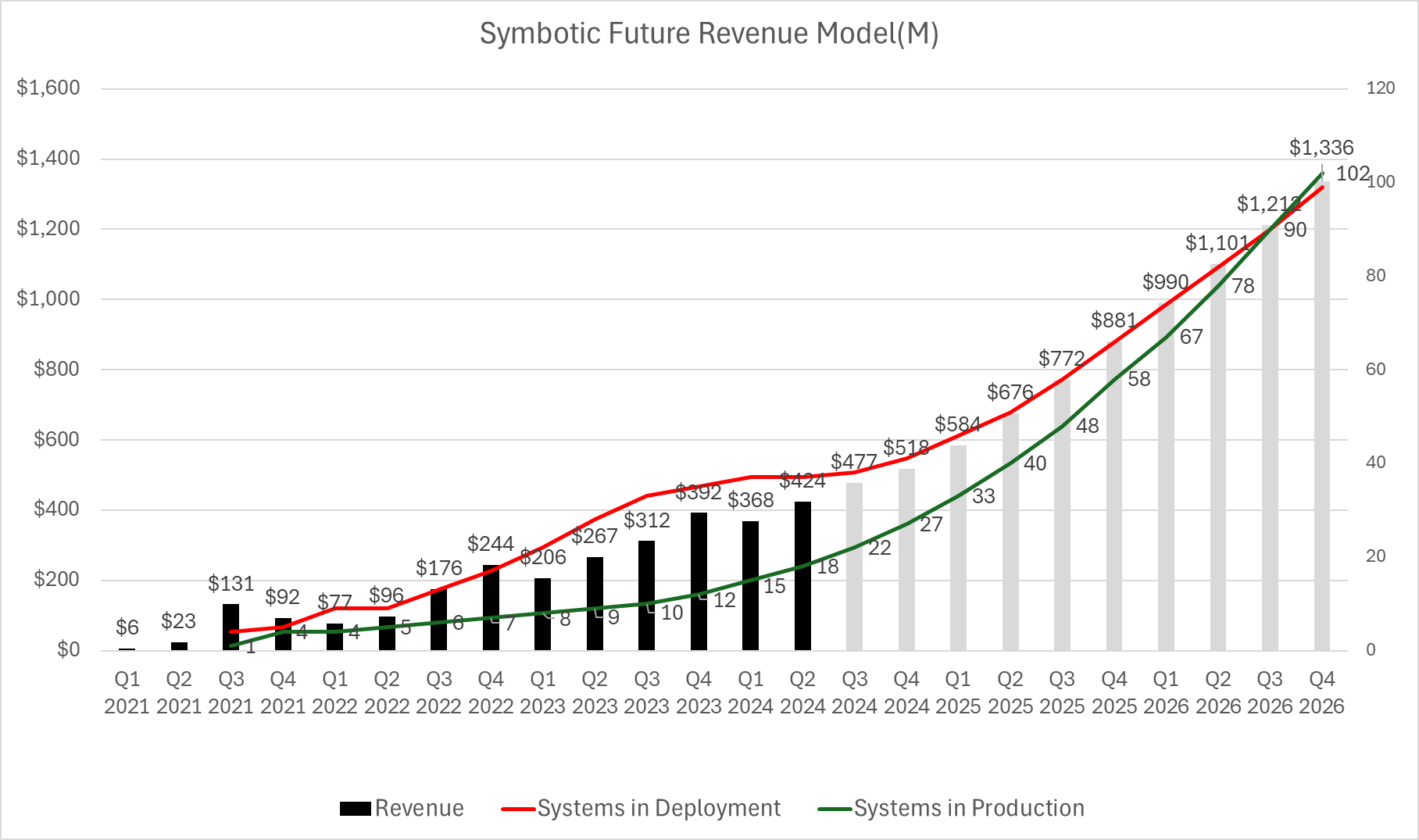

We also want to provide an update to our 3-year revenue model based on the Q2 results. As per the management commentary during the Q2 earnings call, Symbotic will accelerate new deployment starts, which will positively affect the revenue growth rate in Q3 and Q4. Additionally, there will be revenue contribution from GreenBox that will start its first customer deployment in Q3.

As a result, we are raising our revenue estimate for FY 2024. In Q3, we expect 5 new system deployments and 4 completions. We expect the new deployments number to increase to 8 in Q4. From 2025 onwards, we anticipate 15-20 new system deployments every quarter (on top of the completed ones) due to shorter deployment times and Greenbox contributions (see below)

3-yr Revenue Projection (Author)

Our revenue forecast for Q3 is $477 million (vs company guidance of $460 million). Based on our growth model, our revenue projection for FY2026 is $4.6 billion, up $500 million from our previous forecast of $4.1 billion.

Valuation – 2026 Price Target Raised to $88

Symbotic shares closed at $44 as of May 17, 2024, resulting in a market cap of $27 billion. Our revenue projections for FY24, FY25 and FY26 are presented below. The fwd P/S ratio for FY24 has come down to 15, and for FY25, it has come down to 9 (see below)

Revenue forecasts (Author)

According to our model, Symbotic is expected to reach a revenue of $4.6 billion in FY 2026, implying a forward P/S of 5.8. Our main assumption is that the revenue growth of 50%+ will continue over the next three years due to $23 billion backlog. If we apply a modest multiple of 12x to the FY 26 revenue we get a FY2026 price target of $91. This represents a 105% upside potential from the current price.

We think that Symbotic’s valuation is still attractive, given its strong revenue momentum. Additionally, the company is also consistently improving its margins each quarter. Margins are projected to be significantly higher in 2026 as management expects gross margins to reach 60% levels in few years.

Risks

Here are the updated risks after the Q2 earnings:

Concentration Risk: Symbotic’s biggest risk is its overdependence on Walmart. As of Q2 2024, portion of revenue from Walmart increased from 82.5% to 84.2%. While the company aims to reduce its reliance on Walmart, the concentration remains very high.

Robotics Competition: The robotics industry is moving very fast due to advancements in AI and automation technologies. Market is very crowded and top competitors are ABB, Kuka, Amazon Kiva, Exotec and Ocado. Symbotic claims most of these companies focus on ecommerce and are not capable of supporting large-scale off-line retailers

Conclusion

Symbotic delivered a solid Q2 quarter and provided positive outlook for the remaining of FY24. The company announced key innovation updates and is delivering on its growth strategy with accelerated system deployments.

As a result of a more positive revenue outlook and advancements on its innovation roadmap, we remain bullish on the company’s long-term prospects.

We maintain our Buy rating an raising our FY26 price target to $91.

Be the first to comment