Sean Gallup/Getty Images News

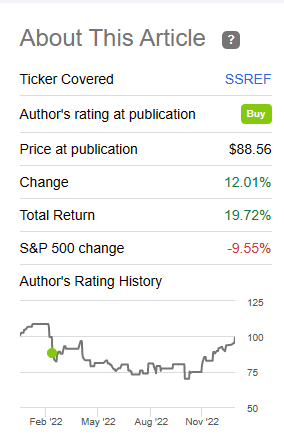

We got what we wanted. When we last covered Swiss Re AG (OTCPK:SSREY) (OTCPK:SSREF) in March 2022, we gave it the bull nod with expectations that it would outperform the major indices. Specifically, we said:

A couple of weeks back we had considered downgrading Swiss Re back to neutral. Our rationale was that the price appreciation alongside the risk of pending results made this a more even proposition for returns. The price decline that followed, alongside the good results that we saw, have kept the scales in favor of a buy. Alongside the lofty dividend we expect 15% total returns over the next year and we are maintaining our bullish rating.

Source: Swiss Re: Drops Back Into The Buy Zone

15% total return is a lofty goal and was an even loftier goal considering what 2022 actually delivered. Swiss Re also faced the pressures of a stronger USD on its total returns. But the stock still delivered and made the 15% total return look easy.

Seeking Alpha

We examine where things stand today.

Q3-2022 Results

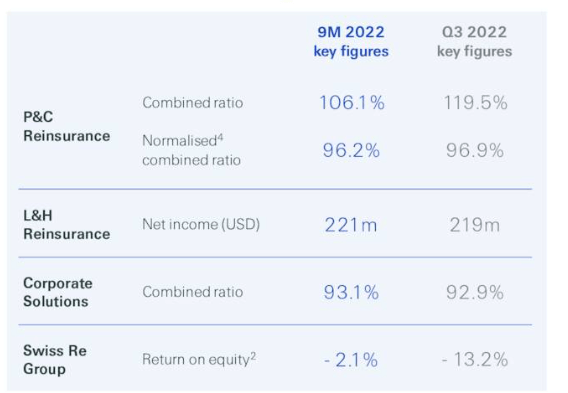

Swiss Re reports its results in three different segments. For the nine months ended September 30, 2022, Property & Casualty Reinsurance was once again on the weaker side with a combined ratio of 106.1% and a normalized combined ratio of 96.2%.

Swiss Re Q3-2022 Presentation

Life and health reinsurance showed a net income of $221 million, which was all achieved in the third quarter. Corporate solutions showed a continuation of the improving trend as the combined ratio stayed in the low 90s.

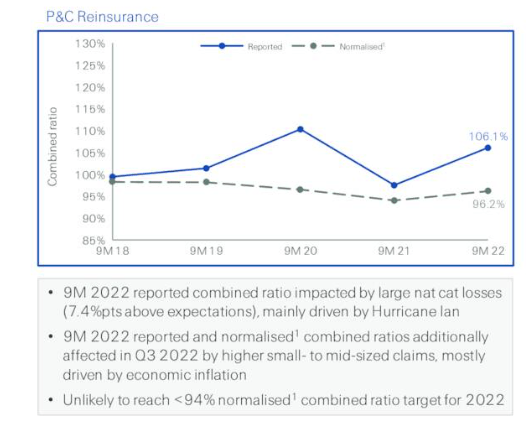

The Property & Casualty Reinsurance always tends to be lumpy as either you have a feast or a famine. Swiss Re tries to get a “normalized loss ratio” here to help investors get a sense of the base business run rate.

Swiss Re Q3-2022 Presentation

Our take here is that the normalized number is great for making estimates for the next fiscal year and practically useless for actually predicting anything. We rarely have an “average” year, and we’re not sure whether Swiss Re’s normalized ratio is representative of the average year. Natural catastrophes have unfortunately been extremely high for the past few years, and reinsurance companies have struggled with making money. Swiss Re is no different here than the other reinsurance companies we follow. On the bright side, the pricing power in this segment is improving by leaps and bounds.

As we go forward, we will work with clients that are willing to acknowledge the underlying risks and the appropriate prices.

But I would expect a material increase in that pricing and I would expect a material increase in the retentions of risk by primary companies as we move forward. The economics of the reinsurance industry has been challenged over the last five years.

I think it’s clear to all that we would not just expect but require better expected returns on the business we write, and therefore, the discussions with our clients are, in some ways, reflecting that reality, but are likely to leave some people unhappy with the amount of price increase that we believe is appropriate in this moment. So we will see where the January 1 renewals go, but it will be challenging, broadly speaking and especially with respect to anything touching the Florida market, I expect.

Source: Swiss Re Q3-2022 Transcript

Those are the realities of the market. Even other strong players like AXIS Capital (AXS) after talking about the big rate hikes on reinsurance rates for a good while, decided to exit the market completely.

Going forward, we expect rates to strengthen materially in this segment, but ultimately the industry needs 2-3 years of average to below-average catastrophes to build up some capital cushion.

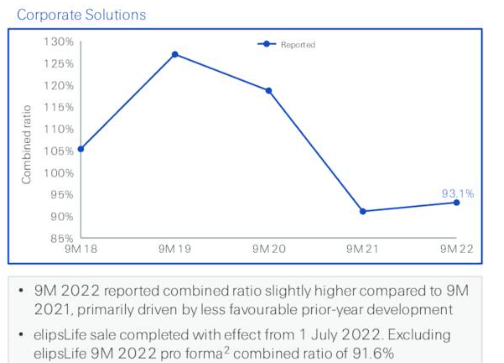

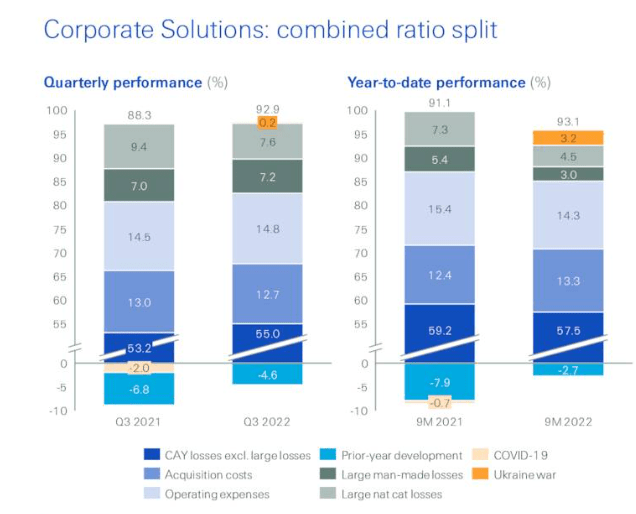

While the Property and casualty reinsurance was hard hit, corporate solutions continued its steady performance.

Swiss Re Q3-2022 Presentation

While year to date combined ratios were higher than last year, the numbers were stellar adjusting for prior year reserve developments and the Ukraine war.

Swiss Re Q3-2022 Presentation

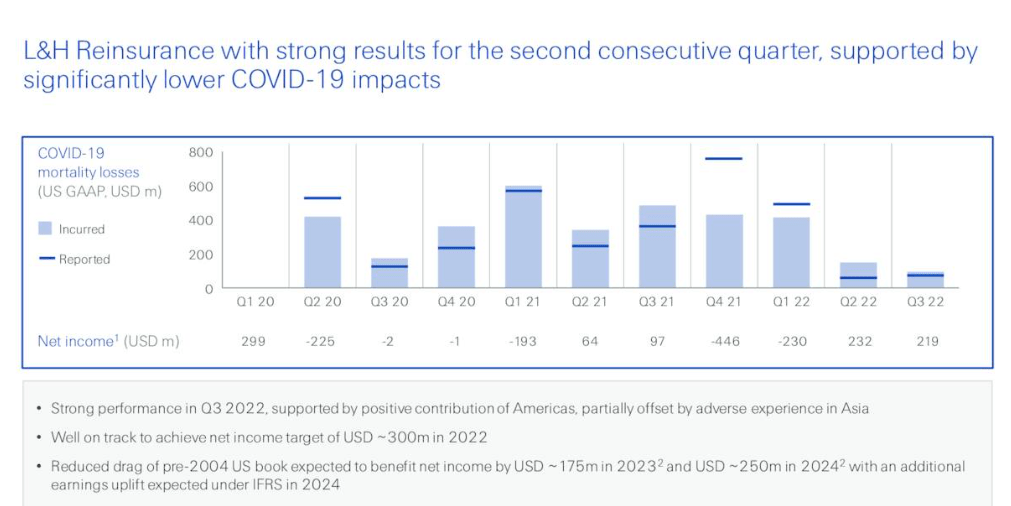

On the life and health reinsurance side, Swiss Re is finally putting COVID-19 stresses in the rearview mirror. Mortality losses were lower, and we expect this segment to report even better results in 2023.

Swiss Re Q3-2022 Presentation

The Big Balance Sheet Side Of The Equation

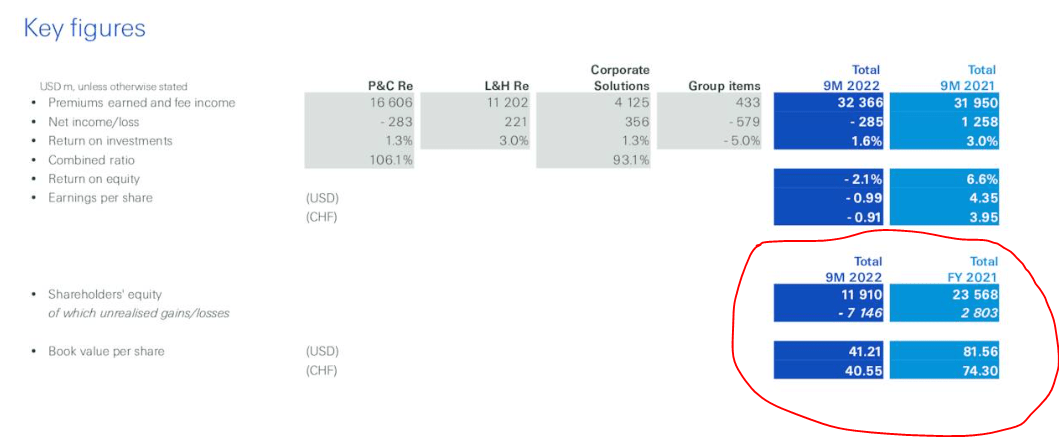

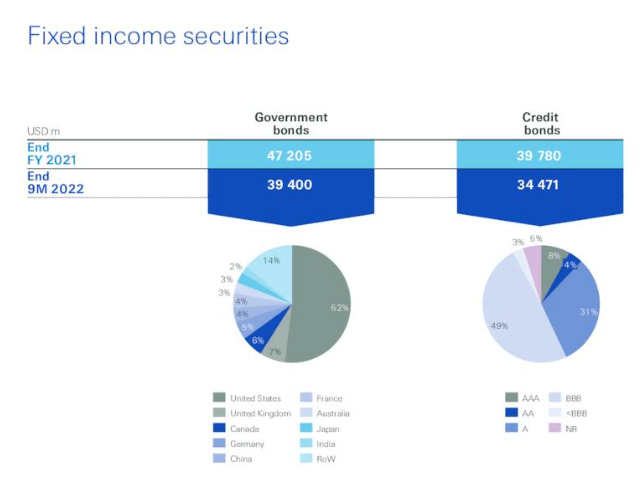

Swiss Re’s headline numbers in 2022 included the big change in tangible book value. Curious investors must have noticed that tangible book value per share dropped from $81.56 (in USD), all the way to $41.21.

Swiss Re Q3-2022 Presentation

That is a stunning amount, but fortunately, there is a good explanation. The drop comes from mark-to-market changes on all their fixed income securities. As interest rates moved up, bonds lost value and since Swiss Re holds primarily bonds, its book value fell. This is similar to banks in the US, although not identical. Banks are allowed to not write down values for investments they classify as held to maturity. They only need to write down values for their trading portfolio. Nonetheless, this did impact book values even in the strong banking group from changes to a portion of their asset side.

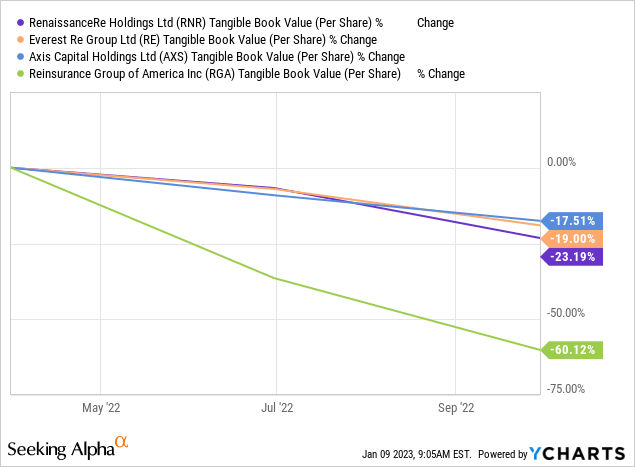

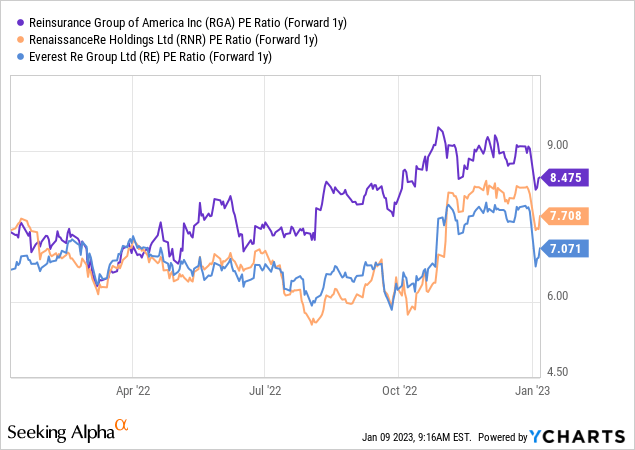

Within the reinsurance side, the movements are about proportionate to how much duration the portfolios had. We have shown RenaissanceRe (RNR), Everest Re (RE), AXIS Capital Holdings Ltd., and Reinsurance Group Of America, Inc. (RGA) as examples below for their tangible book value delta.

It ain’t pretty anywhere by this metric.

But, the key fact to keep in mind is that these are bonds that will be held to maturity and as long as the principle is paid, things should be fine over longer durations. Here, we will add that Swiss Re does take on more credit risk than some of the other companies. Notice the sub BBB bonds.

Swiss Re Q3-2022 Presentation

Valuation & Verdict

Reinsurance and insurance stocks always look cheap on forward P/E multiples and that is definitely the case today as well.

MarketWatch

This is no different for the other stocks we have mentioned here.

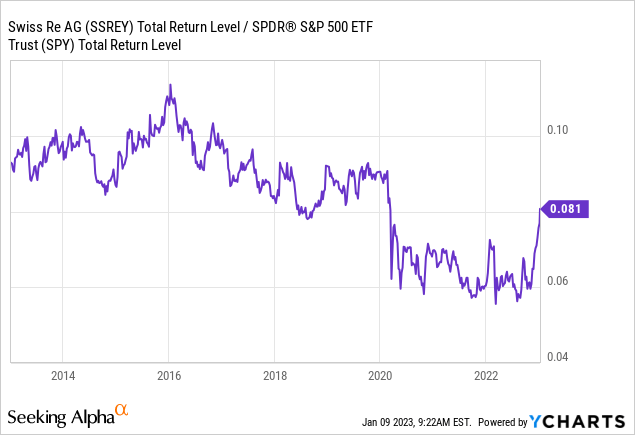

A key reason is, of course, that those earnings are often not realized. Swiss Re’s valuation looks fair based on where the industry is. The sector also is now fully reaping the benefits of higher interest rates on reinvestments and the higher reinsurance rate story is well priced in. We can see this response also in the ratio of Swiss Re’s total return vs S&P 500 (SPY).

The sector is extremely overbought and no longer as attractively priced, both on a relative and on an absolute basis. Keep in mind that when we rated this a Buy in March 2022, we expected a normal year as far as global catastrophes were concerned. We had far higher damage than that, and Swiss Re’s operating numbers were below what we expected. Yet, the stock has outperformed our expectations on the back of the other two tailwinds. The company also takes a little more credit risk than we would like for a reinsurance company, at this stage of the economic cycle. At this point, we are hence downgrading this to a Hold and think other areas of the market offer better opportunities.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment