wildpixel

Super Micro Computer, Inc., or Supermicro (NASDAQ:SMCI), is a leading provider of customized solutions in high-performance computing (HPC) and storage systems. Its leading customers include Intel (INTC), AMD (AMD), and NVIDIA (NVDA).

Therefore, the company has significant exposure to data center/enterprise/cloud computing growth that has avoided much of the malaise in consumer electronics.

The company also announced a partnership recently with Arm-based Ampere Computing, expanding its solutions for customers in Arm-based cloud workloads. Given the increased penetration of Arm-based CPUs in the data center segment, Supermicro has demonstrated its ability to expand its TAM and diversify its reliance on x86 architecture.

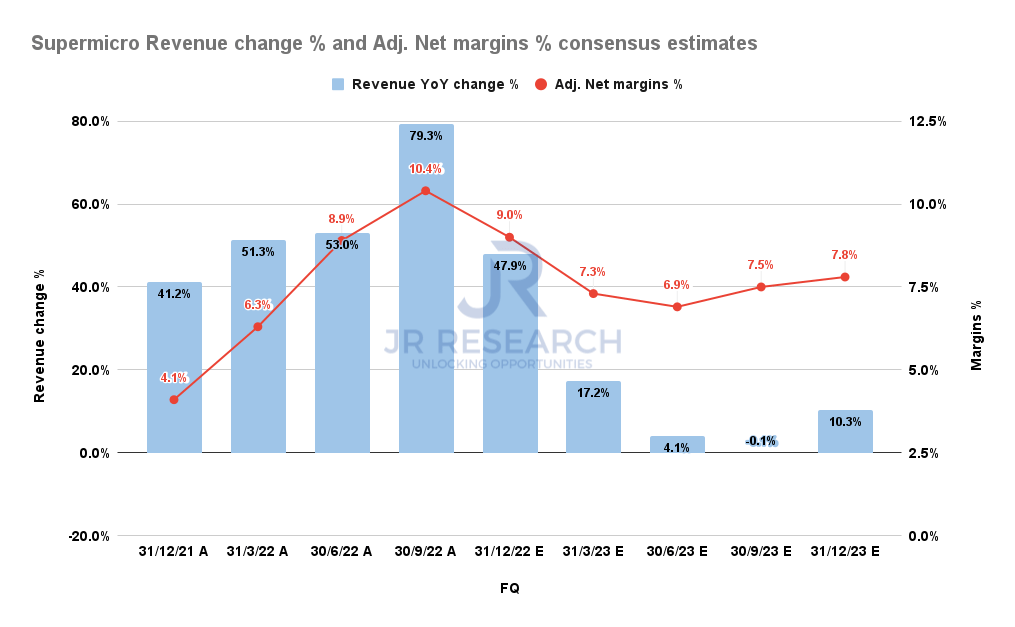

Therefore, the company has also managed to dodge the macroeconomic headwinds that impacted much of its semi peers in 2022. Accordingly, SMCI reported revenue growth of 79% in FQ1’23 (the quarter ended September 2022). As such, the company has significantly outperformed its industry peers, as Supermicro highlighted:

[Our FQ1 revenue grew] about ten times faster than the current industry average. It proves that our Green Computing and Total IT Solutions continue to gain customers’ acceptance and trust. – Supermicro press release

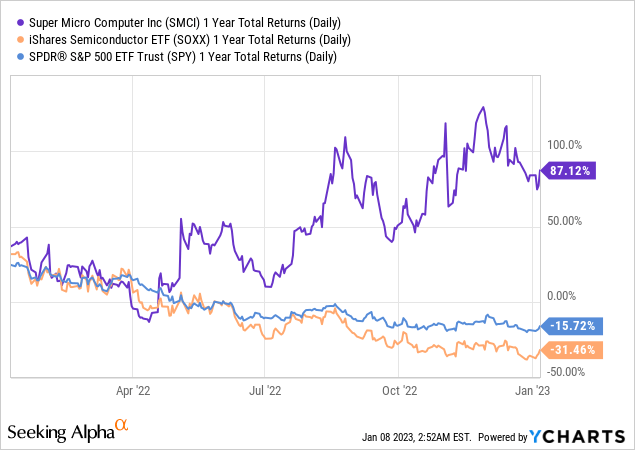

However, before investors get over-excited that they could have missed a super outperformer in 2022 and want to jump on board now, consider its 1Y total return.

SMCI posted a 1Y total return of 87%, easily outperforming its peers represented in the iShares Semiconductor ETF (SOXX) and the S&P 500 (SPX) (SPY). Relative to SMCI’s 5Y and 10Y total return CAGR of 31.2% and 23.3%, we believe much of its near- and medium-term upside could have been baked in.

There’s little doubt that management remains confident that the new product launches from AMD, Intel, and Nvidia are expected to provide growth momentum moving forward.

Despite that, worsening macroeconomic headwinds have also seen cuts in enterprise IT spending. Also, Meta (META) and Google (GOOGL) (GOOG) have announced “indefinite suspensions” in their data center expansion plans.

Revised DIGITIMES estimates suggest that the server market shipments growth could decelerate to 4.3% in 2023 (revised from 5.2% previously) after posting an expansion of 6.1% in 2022.

DIGITIMES also highlighted that China’s recovery is expected to remain languid in 2023. However, Supermicro indicated that its China revenue exposure in FQ1 was 3% and therefore, insignificant. Notwithstanding, DIGITIMES also emphasized that US-based hyperscaler demand is expected to remain robust, as “new servers featuring next-generation CPUs [is] expected to drive upgrade demand starting in Q2 2023.”

SMCI revenue change % and Adjusted Net margins % consensus estimates (S&P Cap IQ)

However, investors should note that Supermicro’s growth cadence in H2FY23 could moderate based on the revised outlook provided by management.

Therefore, investors need to expect significant growth normalization from FQ3 (the quarter ending June 2023) before the ramp on new upgrades from the hyperscalers.

As such, investors should consider whether SMCI’s outperformance could face tremendous challenges moving ahead as investors could rotate some exposure to battered stocks.

SMCI last traded at an NTM EBITDA multiple of 6.7x, below its 10Y average of 7.3x. Hence, SMCI is not expensive relative to its historical averages.

However, it remains priced slightly above its peers’ median of 6x (according to S&P Cap IQ data). As such, we assessed that SMCI is unlikely to face a steep decline, as its valuation has not surged to unreasonable heights. But it seems pretty well-balanced and not significantly undervalued.

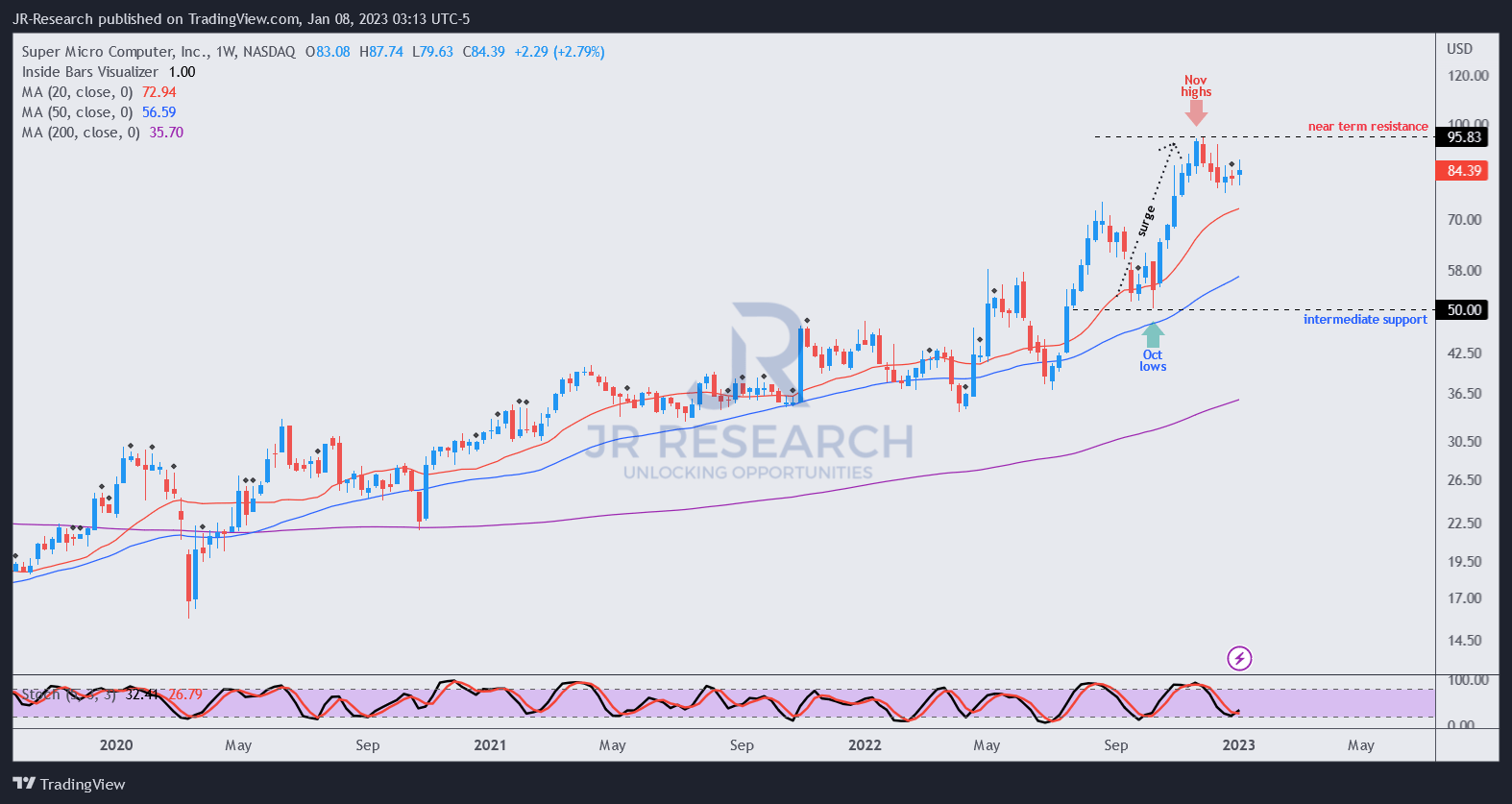

SMCI price chart (weekly) (TradingView)

Still, we urge investors to be cautious about SMCI’s rapid surge from its October lows to form its November top.

While there were no signs of a bull trap suggesting extreme caution, we believe the pullback is likely not over, even though it could continue to consolidate in the near term.

Hence, investors looking to buy can consider a deeper retracement to improve their reward/risk before adding more positions.

Rating: Hold.

Be the first to comment