Zigmunds Dizgalvis/iStock via Getty Images

SunPower Corporation (NASDAQ:SPWR) is a solar company operating in both the United States and Canada. They are a provider of both storage and home energy solutions. Even though the revenues are growing quickly, it still leaves the current share price too high to make a bull case for buying right now. Because of this I think investors are better off simply holding any position and perhaps wait for a better buy point if we see a compression in valuations in the future.

Earnings Report

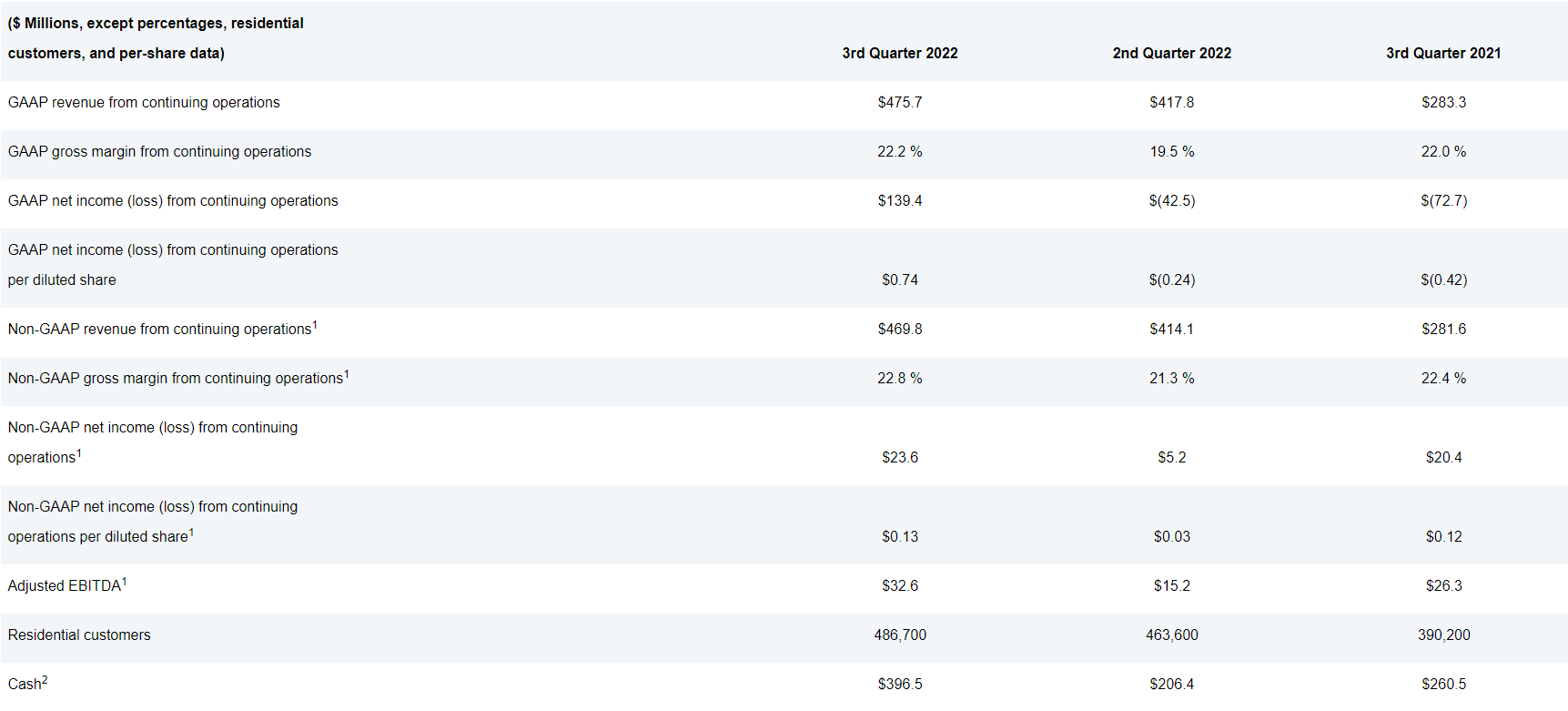

SunPower Corporation released on November 8. 2022 their third quarter earnings report. In the report I found a lot of confidence and optimism coming from the company. They reported increasing their revenues by 67% from last year’s same quarter. This is on the high end compared to a lot of other solar energy companies I have covered recently.

The challenge that comes with rapid expansion and more capital deployed is getting a good return on that. With this recent report I got a lot of confidence SunPower is on the right track to regain their margins and hopefully keep them as well.

Income Statement SunPower (Q3 Earnings Report)

With EPS coming in at $0.74 that is quite the leap from last year’s performance of $(0.49). Much of that being from increased margins and a responsible use of capital. A large bump solar companies can experience is increased costs of parts and equipment, but I think SunPower has managed to pass on those costs to the consumer.

Lasty it should be mentioned that SunPower now landed a very valuable partnership with General Motors, becoming the exclusive solar supplier to the company. With a larger increase in demand from residential homes, SunPower was able to achieve a record number of installations in the last quarter.

Growth Outlook By The Company

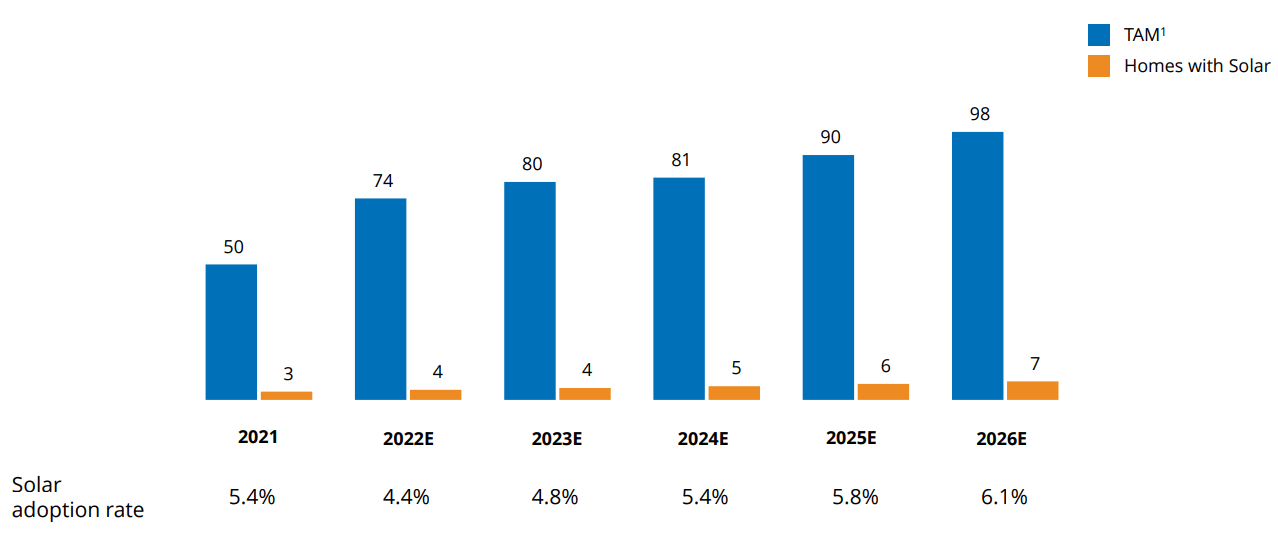

To me it’s important to read up on what a company believes to be tailwinds for them in the future. In the case of solar it’s quite simple, it’s a greener option of an energy source. But it also comes with both support from governments and increased social pressure to more quickly adopt renewable energy.

SunPower is working quite heavily in the residential part of solar adoption. This is quite an undeserved part where there is potential for a large customer base and market share to take.

The Solar Adoption Rate (SunPower Investors Presentation)

With such a large amount of American homes not using solar, the potential for SunPower to sweep in and become a larger player is there. With California being one of the larger markets where a lot of capital is ready to be used to upgrade to solar, SunPower believes they have the chance to make it big here.

They are also positive about the legislation from the lawmakers here, pushing people to see solar as a more efficient and cost saving source. Another tailwind the company expects is that EV adoption will also push people into wanting solar panels to create an ecosystem of green energy where they live.

Expansion Challenges

The largest challenges SunPower could face might not come from demand or legislation. Instead it could be internal. I know that the solar sector is incredibly capital intensive in order to have a foothold and establish yourself.

I think that SunPower will see increased demand for many years to come for their product. But I also believe that they will have a much tougher time securing capital to fund a lot of their expansion. With cheap money no longer being a thing SunPower will need to run a tight ship where they care about keeping positive cash flows and investors happy.

Another possible challenge I think they could have is getting established in smaller regions. There is no shortage of solar companies out there right now. A lot of these are small and regional. In terms of customers, they will often lean more towards a regionally based company instead. This could prove to be a difficult task for SunPower to deal with, but only time will tell.

The Company Financials

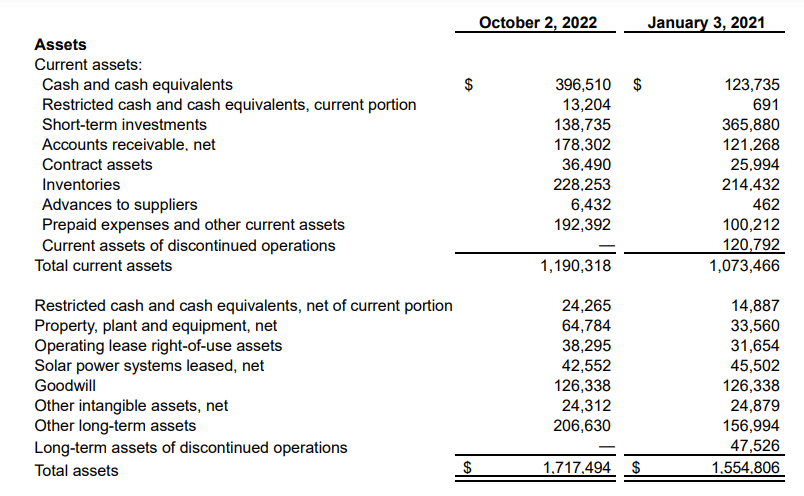

On the financial side of the company, they seem to be in a really healthy spot. Compared to many other solar companies I have recently researched, SunPower holds a large amount of cash compared to their debt. With cash coming in at just under $400 million, that more than covers the long-term debt of $72 million. A good place to be in in case we see a slowdown in the economy and in turn the demand for solar products.

SunPower Current Assets (SunPower Q3 Earnings Report)

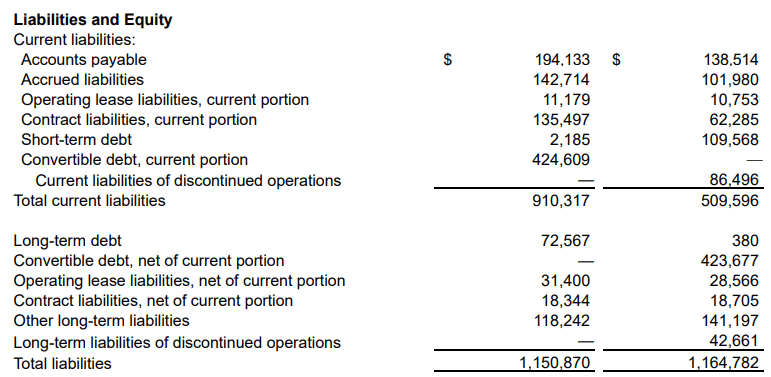

One thing I particularly liked seeing was the decrease of liabilities on a YoY basis, reduced around 1.2%. That comes at the back of assets seeing an increase of 10.4%. On a closer look however I find that a large portion of this asset increase comes from the company keeping prepaid expenses high, likely from suppliers tightening demands. For some companies this might become an issue, but I believe SunPower should be able to work around this with their large portion of cash at hand.

SunPower Current Liabilities (SunPower Q3 Earnings Report)

Let’s move on to the cash flow of the company. Another important thing to look at as it will help evaluate the risk of share dilution happening in the future. Again, comparing SunPower to other solar companies we can see that they have managed to keep their head above the water much better. Cash flows are currently positive, which should help mitigate the risks of share dilution.

SunPower Cash Flow History (Seeking Alpha)

A common practice for companies when cash flows are negative is to dilute shares in order to raise capital for future projects and initiatives. As a shareholder however this can become an incredibly bad thing unless the company is able to increase their bottom line fast and steadily enough.

How Are The Competitors Valued?

The solar sector has been a very hyped part of the market the last 2 years or so. With a large amount of money coming in it’s no wonder some of the valuations these companies have are completely unrealistic. That’s why I like comparing how a certain company is looking in the face of others.

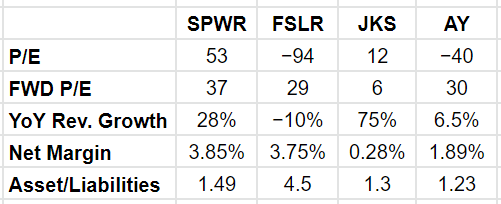

Competition Valuation (Author’s Own Valuations)

What favours SunPower perhaps more than some of the other players in the space is the good revenue growth and also impressive net margin. For me, this gives me confidence SunPower might still at least be around in the next 10 years, at least compared to First Solar (FSLR), JinkoSolar (JKS) and Atlantica Sustainable Infrastructure (AY).

A common trend among solar companies right now is to build out their assets much quicker than liabilities. A large portion of the assets are factories and properties that will hopefully be able to supply the coming demands. What I watch out for however is that these numbers don’t go too wild. With a lot of assets compared to liabilities, that usually means the company doesn’t hold a lot of debt. I think raising capital in the next few years will be very costly. Something like First Solar (FSLR) might seem great, but there’s a high likelihood they might have to resort to diluting shares to raise more capital and support construction and projects.

All in all I want to make it clear that solar companies are not a safe bet to make money from. Valuations matter and knowing if there are better options out there is important.

Valuing SunPower Corporation

Let’s get to the fun part now of setting a price target and value of SunPower Corporation. With all that we have gone through I think it’s pretty clear that they are sitting in a good spot financially and have a lot of big tailwinds ahead of them.

The push for renewable energy sources won’t stop and with such a large portion of residential homes undeserved with solar, SunPower has the opportunity to be a big player in the space. Seems like a great investment when you put it like that, but valuations matters too of course and SunPower seems to be charging a premium right now.

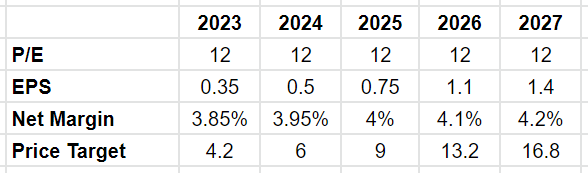

SunPower Future Valuation (Author’s Own Calculation)

These price targets might seem way too conservative compared to today’s prices. But I argue that keeping conservative estimates is important if you want safety in your investments and reduce any potential downside risks. A terminal p/e of 12 should be in line or slightly below the sector average. I think that the company will manage to increase net margins, but revenues will increase much faster and help the EPS grow as much as I expect. For the short-term I could see share dilution happening, but as the cash flow stabilizes the need isn’t there anymore.

SunPower is trading at a very rich valuation right now and I think it’s too risky buying it without losing money. I like the company and what they are doing. I think they are in a great spot financially and they continue to grow year after year. But sometimes the performance does not match the share price.

Conclusion

SunPower Corporation is a solar company that has managed to establish themselves quite well in the last few years as a great supplier of solar panels for residential properties.

With a strong balance sheet and barely any debt to pay off, SunPower I think they are in a much safer position then some of its competitors in the sector. Becoming cash flow positive this year gives me confidence that there might not be any more, or at least reduced share dilution on the horizon.

In the last earnings report the company also mentioned that they are focused on increasing revenues and the bottom line too, but also that they are confident in keeping up its current growth.

But valuations matter, especially if I want to invest into something. SunPower trades at around 55 p/e. There are few things worth paying such a premium for. Because of this I feel it’s too risky using any money to invest into SunPower at its current valuation, simply holding on might be best. If the valuation contracts and we have something more realistic then I will take a second look and reconsider the possibility of investing again into SunPower.

Be the first to comment