AsiaVision

StoneCo Ltd. (NASDAQ:STNE) caught the attention of investors at the time of its IPO in 2018 because of Berkshire Hathaway’s (BRK.A) investment in the company. After trading sideways till March 2020, StoneCo stock took off following the Covid crash to hit an all-time high of over $92 in February 2021, only to shed all of those gains in the months that followed. StoneCo has started 2023 on the right foot with its market value already appreciating 10%, which begs the question whether fortunes are finally turning for the better. To answer this question, investors need to evaluate a few critical aspects including the regulatory environment surrounding the Fintech sector, and the macroeconomic outlook for the Brazilian Fintech sector. The objective of this analysis is to identify and discuss the bigger picture for StoneCo – not to dive into the company’s recent earnings as this has already been done by fellow Seeking Alpha authors.

The regulatory environment is changing for the better

Fintech companies, regardless of where they are based in the world, usually face many regulatory challenges in the initial stages of their business. When it comes to emerging markets, the challenges seem far more threatening. Things are no different in Brazil but a few recent regulatory decisions suggest the country is embracing the Fintech sector, which is encouraging news for StoneCo.

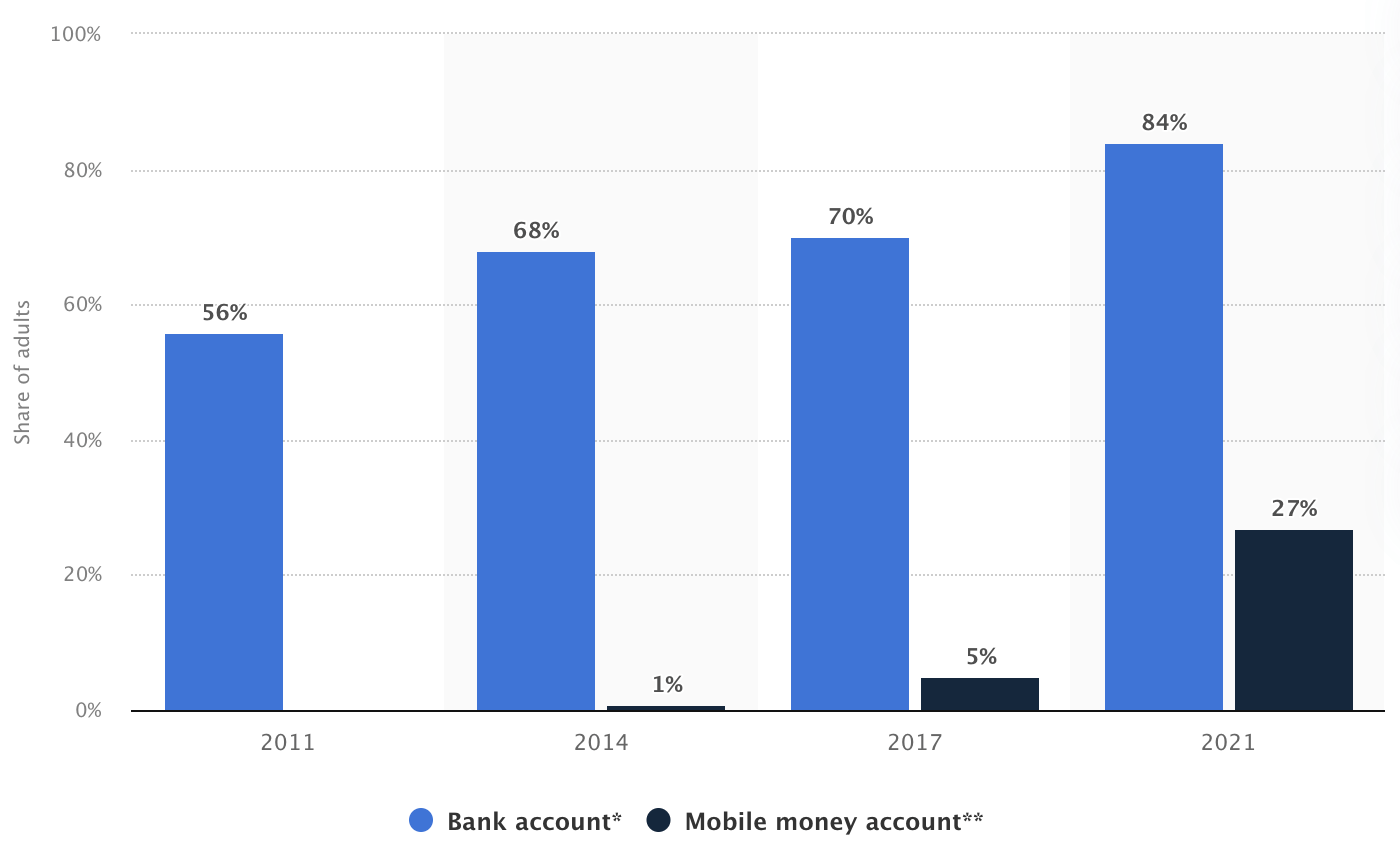

Before 2010, Brazil’s financial services sector was dominated by a few leading banks, and experts have time and again criticized these banks for catering to the affluent community in the country, leaving behind the majority of the population. By using stringent credit underwriting practices, these banks were able to rack up profits and grow, but leaving a few dents from a socio-economic perspective. Things took a change for the better after 2010 with the emergence of Fintech companies. From just 57% in 2010, Brazilians with access to bank accounts/mobile money accounts reached a high of 84% in 2021.

Exhibit 1: Share of the adult population in Brazil with access to banking services

Statista

Source: Statista

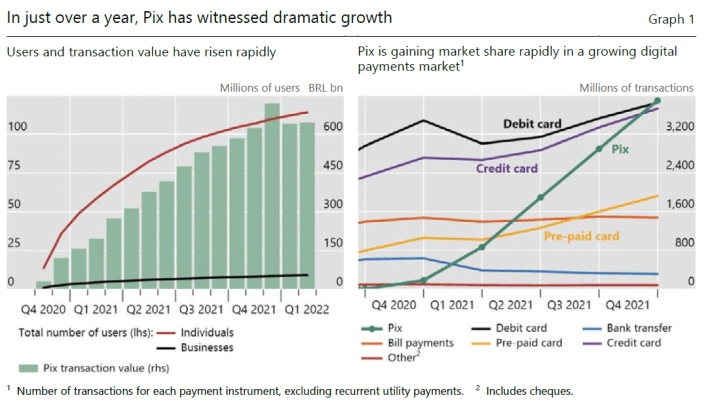

One of the most important factors that has fueled the growth of the Fintech sector in Brazil is the introduction of the PIX system. Until late 2020, Brazilians relied on cash transactions and traditional bank transfers that took around three business days to settle. PIX, the instant payment system that was launched by the Central Bank in November 2020, revolutionized the financial services sector by offering instant money transfers free of charge or at a very reasonable cost. According to data from the Central Bank, in Q1 2022, PIX handled 4.2 billion transactions, accounting for 22.9% of total transactions. In comparison, credit cards accounted for 19.3% of transactions. As illustrated in Exhibit 2, PIX became the most popular method of transacting in Brazil just one year after its launch. The rapid adoption of PIX has enabled Fintech companies to offer attractive instant transfer options to Brazilians who have never had access to any banking services previously.

Exhibit 2: PIX statistics as of Q4 2021

Conversable Economist

Source: Conversable Economist

The massive reforms introduced to the financial licensing framework are also another major step forward in creating a platform for Fintech companies to thrive. Before 2013, Brazilian payment solutions providers were required to obtain a full banking license to provide payment-acquiring solutions to businesses. This is no longer the case as Brazilian startups can now apply for several non-banking licenses that are approved faster.

The regulatory framework in Brazil is changing thick and fast, for the better. With regulatory modernization well underway, Fintech companies now have a good platform to launch into the future.

Macroeconomic tailwinds

There are two macroeconomic developments that paint a promising picture for the Fintech sector.

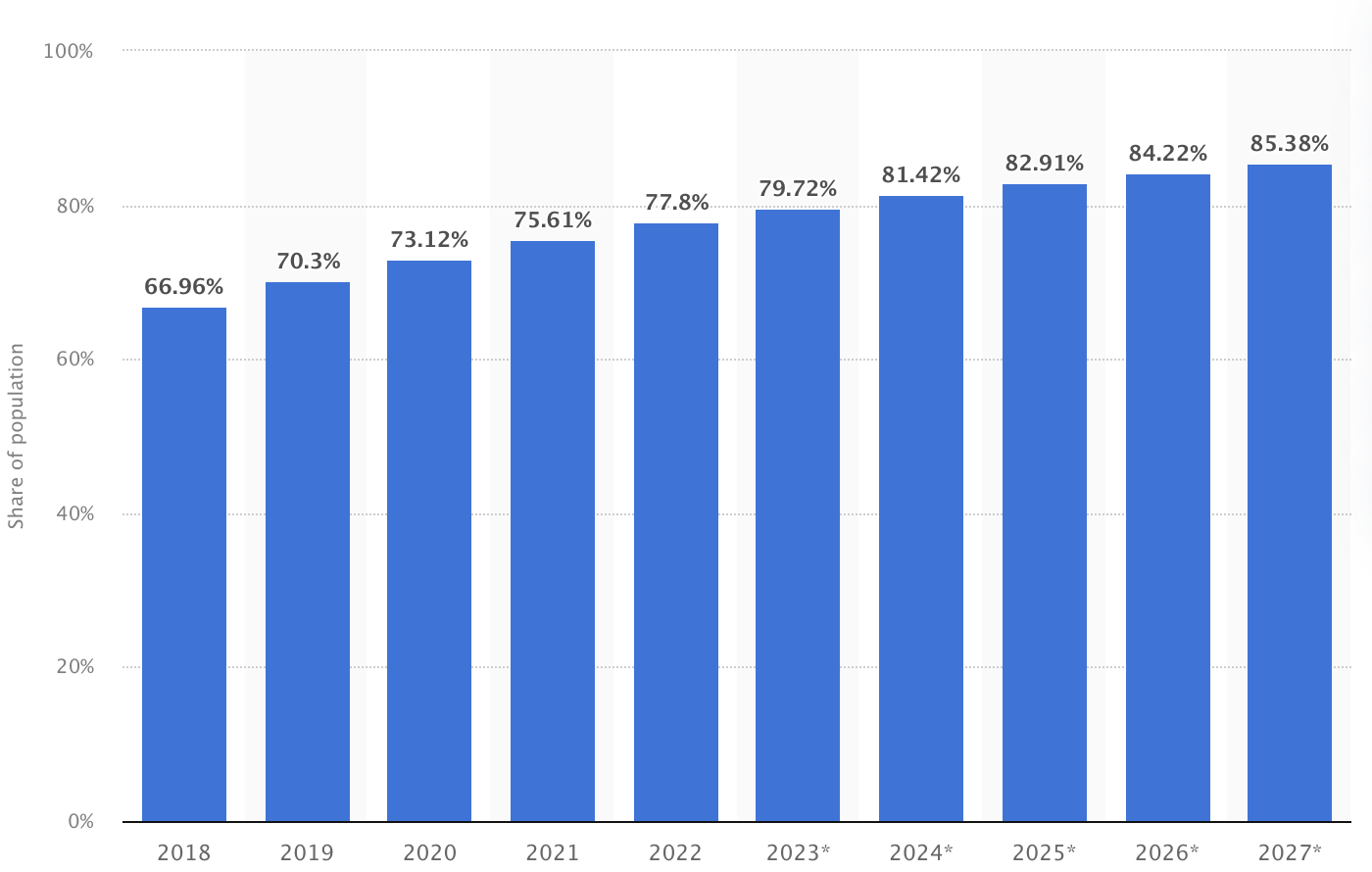

First, mobile usage in Brazil – and all of Latin America – is increasing, which is a positive development as this expands the addressable market opportunity for Fintech companies. In the last four years, the smartphone penetration in Brazil has increased from 66.96% to 77.8%, and Statista projects more gains in the coming years.

Exhibit 3: Smartphone penetration rate in Brazil

Statista

Source: Statista

Second, e-commerce is taking an increasing share of retail sales in Brazil, which paves the way for Fintech companies to aggressively onboard new clients – both SMEs and consumers. According to data from Americas Market Intelligence, e-commerce accounted for 18% of retail sales in Brazil in 2022. With Mordor Intelligence projecting the Brazilian e-commerce sector to grow at an impressive CAGR of 10.23%, the country is moving in the right direction to embrace online shopping. For Fintech companies, this is music to the ear. Payment processing software solutions providers and buy now-pay later solutions providers seem well-positioned to make the most of this e-commerce growth.

StoneCo is at the center of Brazil’s digital transformation

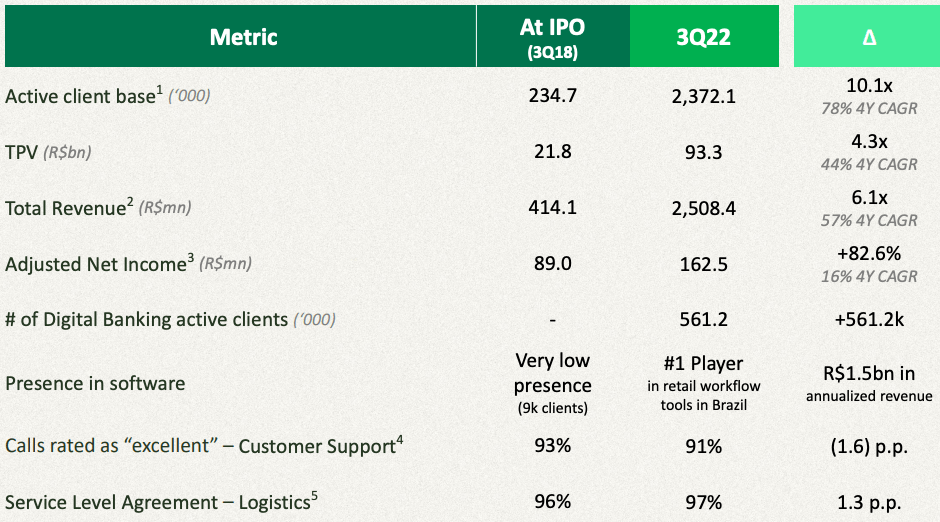

StoneCo, although is yet to obtain a banking license, offers a wide range of financial products and services to its customers including payment solutions, digital banking, and credit facilities. The company has already played a pivotal role in digitalizing many SMEs across the nation, and its recent margin trends suggest StoneCo is becoming more efficient amid positive monetization trends. The company seems laser-focused on high-margin businesses as well, which is evident from its decision to deprioritize subacquirier volumes because of their low profitability. The company’s focus, for the best part of the last decade, has been on growth, not profits. As illustrated below, the company has indeed grown by leaps and bounds in the last four years as well.

Exhibit 4: Financial performance metrics since IPO

Q3 presentation

Source: Q3 presentation

StoneCo has positioned itself as a technological enabler of the Brazilian SME sector. According to data from OECD, micro and small enterprises account for 98.5% of all legal entities in the country and 27% of the country’s GDP. Small businesses well and truly form the backbone of the Brazilian economy, and the country is embarked on a digitalization journey, meaning that the digital transformation of the country will revolve around small businesses. StoneCo, as one of the go-to technological solutions providers to this cohort, stands to gain from the digitalization drive of the country.

Takeaway

StoneCo, from a macroeconomic perspective, is well-positioned to grow. The company, however, will come under pressure in the short run because of the tightening interest rate environment in Brazil, and experts believe these challenges could extend into 2024 as well. That being said, long-term-oriented investors should focus on what lies beyond 2024 for the company. Macroeconomic pressures have so far had a big say in the collapse of StoneCo’s market value in the last couple of years in addition to poor credit practices of the company and its focus on growth at any cost. The company is getting its house in order by focusing on its margin profile at a time when the long-term outlook for the Brazilian Fintech sector is improving. Once short-term macroeconomic challenges are dealt with – which is only a matter of time – StoneCo is likely to receive a lot of love from Mr. Market. Prudent investors might want to act well before that happens.

Be the first to comment