Ethan Miller/Getty Images News

Stellantis N.V. (NYSE:STLA) is currently trading at one time EBITDA, which is significantly lower than its peers, who are trading at 6x to 7x. As STLA keeps hitting its revenue goals, generating synergies and expanding margins, I anticipate that the stock will be revalued to match my fair value estimate of USD 50 per share, tripling its current value.

The Company

STLA was established on Jan. 16, 2021, following the merger of Fiat Chrysler Automobiles and PSA Group. With 14 automobile brands, it has become the world’s fifth-largest automaker. In 2021, despite the impact of the microchip shortage, STLA sold 6.1 million vehicles and generated EUR 152.1 billion in revenue. Europe is STLA’s largest market, accounting for 47% of its global volume in 2021, while North America and South America made up 30% and 14% respectively.

Company website

Q3 2022 Earning Results & A Preview of FY 2022 Results

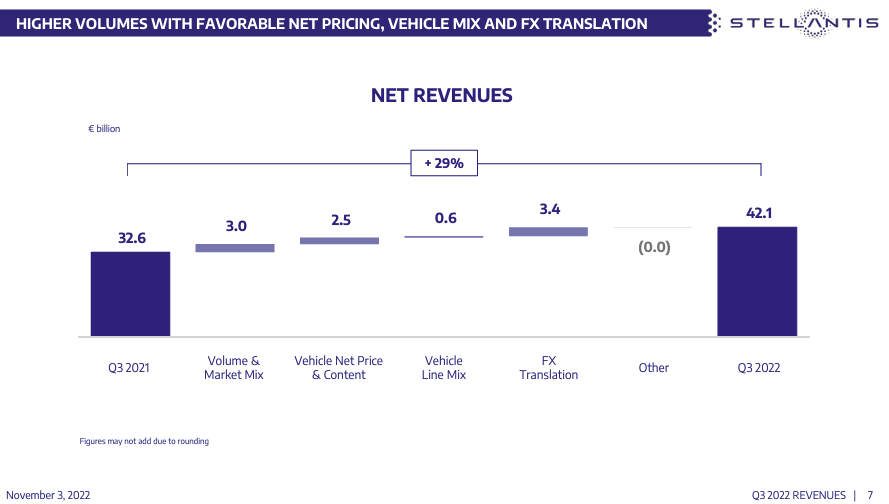

STLA reported third-quarter revenue of EUR 42.1 billion, a 29% increase from the previous year’s EUR 32.6 billion, when the chip shortage was at its worst. Excluding favorable currency impacts, organic revenue increased by 19%. STLA’s revenue was boosted by 9% points from its volume and market conditions, still affected by the chip shortage and the Ukraine crisis, but to a lesser degree. However, vehicle pricing, content, and mix contributed 10%, and average revenue per unit rose by 14% due to the company allocating chips to higher-margin vehicle production. Despite a 13% increase in unit volume to 1.3 million, the revenue increase outpaced the growth in unit volume.

Company presentation

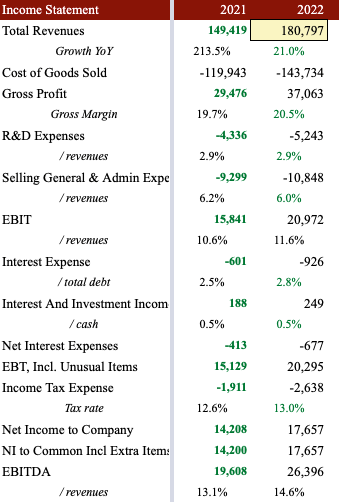

On February 22nd, STLA will be reporting 2022 results. Below are my full year expectations. Based on the below, my EPS for 2022 is $5.60.

Author estimates & Company filings

I expect the revenue growth mainly driven by China, India and Asia Pacific. The continuation of synergy capturing will expand EBITDA margins ~150 bps resulting in a net income of EUR ~17.7 billion.

Highly Competitive Industry with Cyclicality and Overcapacity

Similarly to my analysis for Nissan (OTCPK:NSANY)(OTCPK:NSANF), I do not see for STLA a competitive advantage as the automotive industry is highly competitive, with easily substitutable products, and significant swings in profitability based on moderate changes in demand. The industry experiences cyclicality that can destroy economic value for a year or more, and there is substantial global industry overcapacity, indicating limited barriers to entry. To succeed in this industry, mass-market manufacturers must consistently execute in design and development. Hard-fought market share and temporary economic profits are achieved through introducing new designs, racing to be the first to market with differentiated technology, or maintaining a younger product portfolio. While STLA has premium brands, competitors can achieve the same or better perceived brand value. Consumers in high-volume markets can easily switch among competing brands based on price, trends, technology, and other factors, making it difficult for STLA to maintain its market share.

First Year Synergies Exceed Expectations & Strong Pricing

By integrating two companies through a merger, economies of scale are improved. Management had projected that 80% of the targeted EUR 5 billion in synergy savings would be achieved by the fourth year. However, STLA has already achieved EUR 3.2 billion in the first year, ahead of schedule. The global light-vehicle inventory is low due to COVID-19 and the microchip shortage, which has led to a stronger pricing environment that should enhance margins in the near term. Additionally, the global expansion of premium brands such as Alfa Romeo, DS, Jeep, and Maserati has increased the average revenue per unit and improved profitability.

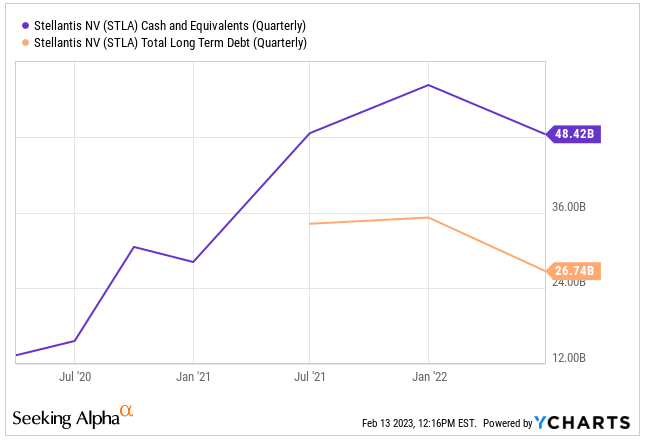

Opportunity to Optimize the Capital Structure

STLA is holding a net cash position, STLA could reduce its cost of capital by increasing its debt position. I do not expect a special dividend as they would be a higher return by reinvesting the capital in the business and accelerate the EV business.

YCharts

Valuation

My target share price is USD 55 per share, as I expect revenue to grow in the mid-single digits in the medium term, driven by increased sales of EV vehicles and strong pricing.

Company website

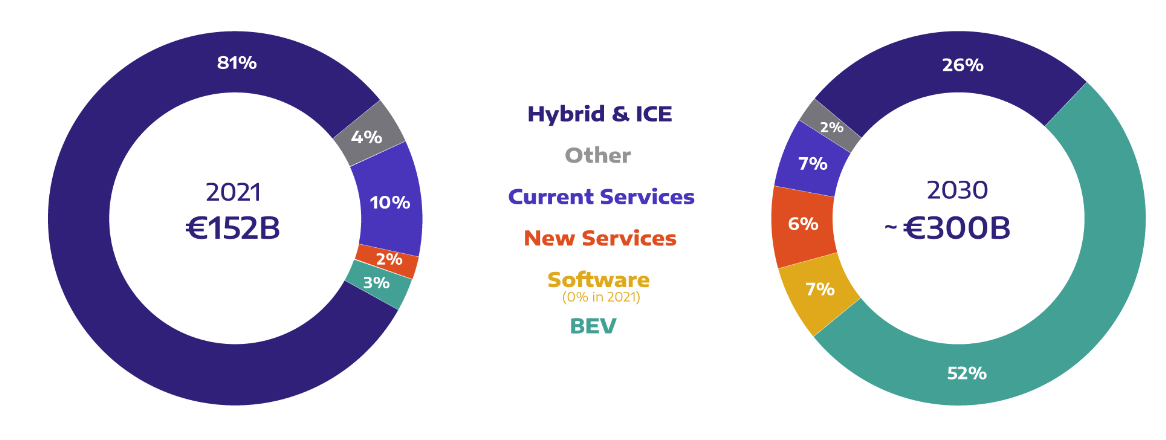

Management also anticipates doubling revenues by 2030, driven by battery electric vehicles. The synergies from the merger are expected to generate approximately EUR 5 billion in annual run-rate, mostly realized after four years.

Despite facing challenges like the chip crunch, Ukraine crisis, inflationary cost pressures, and weak auto market economies, management confirmed their 2022 guidance for a double-digit adjusted operating income margin and positive free cash flow.

Company presentation

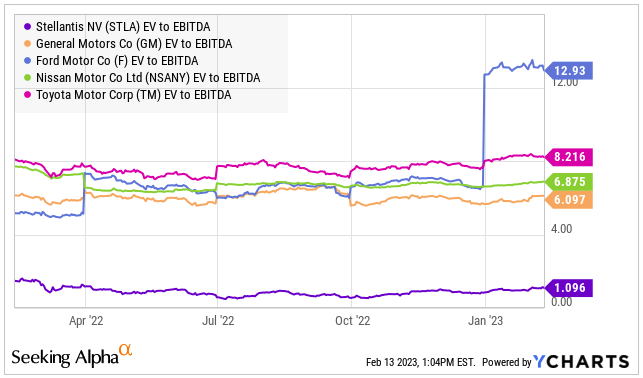

At my target price, STLA would still be trading at a slightly lower multiple, compared to comparable companies, which have been trading at a range of 6x-8x. General Motors (GM) is trading at 6.1x, Nissan Motor at 6.9x, Toyota Motor (TM) at 8.2x and Ford Motor (F) at 12.9x.

YCharts

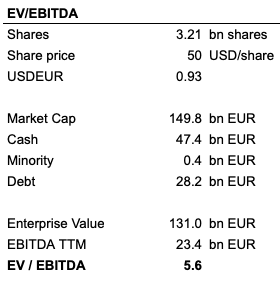

Currently, the EV/EBITDA multiple is 1.1x, but my target value would result in a more reasonable multiple of 5.6x.

Author estimates

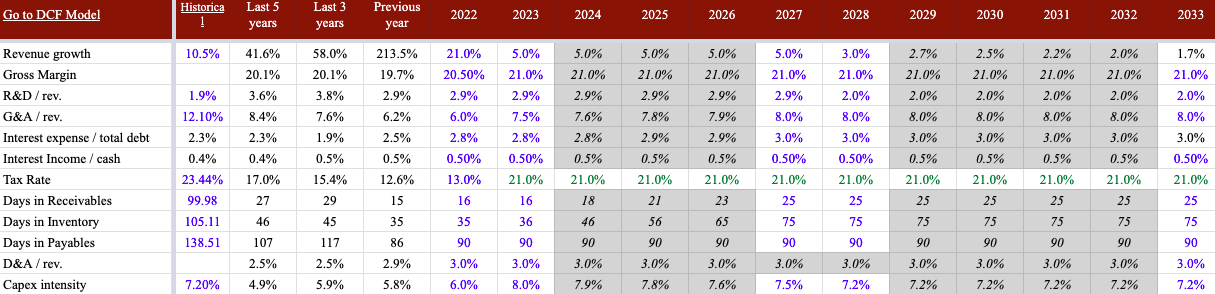

The target price is based on the assumptions in the table below. I expect revenue to grow in the mid-single digits in the medium term, driven by the increased sale of EV vehicles and strong pricing. However, the EUR 300 billion target seems a stretch and I expect it to be only EUR 225 billion. I expect marginal improvements in margins driven by pricing and capturing most of the synergies announced. The main assumptions are below.

Author estimates & Company filings

Risk & Uncertainties

STLA faces several risks, such as volatile commodity costs, a unionized workforce, the risk of execution in merger integration, and cyclical global light vehicle demand. Although the merger between STLA and Peugeot is geographically complementary, with a significant presence in North and South America, the two companies have been unsuccessful in penetrating the Chinese market. Compared to its competitors, STLA has been slower in the transition to EVs because it has had to purchase carbon credits to comply with clean air regulations. However, the recent merger with Peugeot is expected to accelerate STLA’s EV development. The global auto industry is experiencing overcapacity, which leads to pricing pressures that could negatively impact long-term economic profits.

Conclusion

STLA has surpassed its synergy savings goals in the first year of its merger, reporting a 29% increase in Q3 2022 revenue despite challenges such as the microchip shortage and the Ukraine crisis. Nevertheless, the automotive industry is fiercely competitive, cyclically sensitive, and plagued by overcapacity, which suggests that barriers to entry are limited. The shares are presently trading at low multiples, but I anticipate a re-rating closer to peers as management demonstrates its capacity to deliver on revenue growth, synergies, and margin expansion.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment