LIgorko/iStock via Getty Images

Investment Thesis

Steel Dynamics (NASDAQ:STLD) will remain highly profitable in 2023, despite all the worries affecting steel companies.

In fact, ironically, it appears that the worries holding back Steel Dynamics in the past several weeks may have been overblown, as steel prices are already climbing higher.

What’s more, Steel Dynamics continues to return substantial capital back to shareholders via its share repurchase program. Case in point, last quarter, STLD repurchased 3.3% of the company. And it doesn’t appear to be slowing down.

Next Thursday, before the market opens, STLD will hold its conference call. After which, I suspect that analysts will revise their financial models for the coming year.

There’s much to get excited about. So let’s get to it.

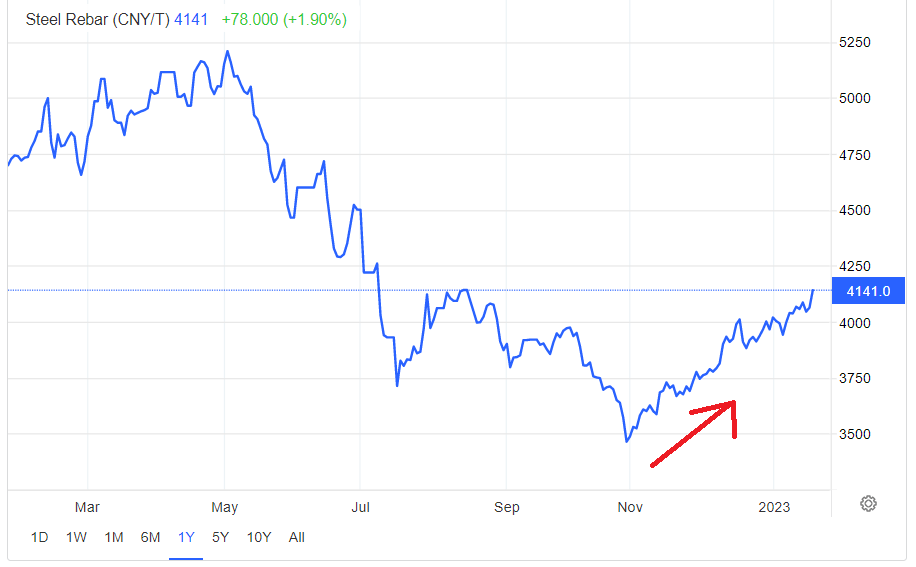

The Most Telegraphed Recession

For months we’ve heard about the late 2022 recession. No, my mistake. I meant to say the early 2023 recession. No, even then, this may turn out to have not taken place.

And while I don’t know exactly when this recession will ultimately show up, what I can tell you is that we all know it’s expected.

And if I know it’s expected and you know it’s expected, that means it’s already priced into steel’s spot market price.

Trading Economics

Indeed, this does not appear to have slowed down the recent appreciation in steel prices.

Consequently, I believe that either steel commodity traders didn’t get the memo. Or perhaps, professional traders did get the memo but they are already looking beyond this?

Steel, For the Great Energy Transition

Next, we’ll discuss the other catalyst facing STLD. The great energy transition, particularly, in the US.

Steel will see a strong increase in demand over the next 3 to 5 years. As countries double down on their energy transition, steel demand is going to go up.

Whether that’s from steel used in offshore wind turbines or solar panels, steel will play an important role in all renewables, especially solar and wind.

Other sectors that will see an increase in steel demand include EVs, onshoring of global supplies, and warehousing building for direct-to-consumer companies (for instance, Amazon (AMZN)).

While every country will have its own preference for its own energy security requirements, countries require steel. And lots of it.

Next, we’ll get down to US Steel’s valuation.

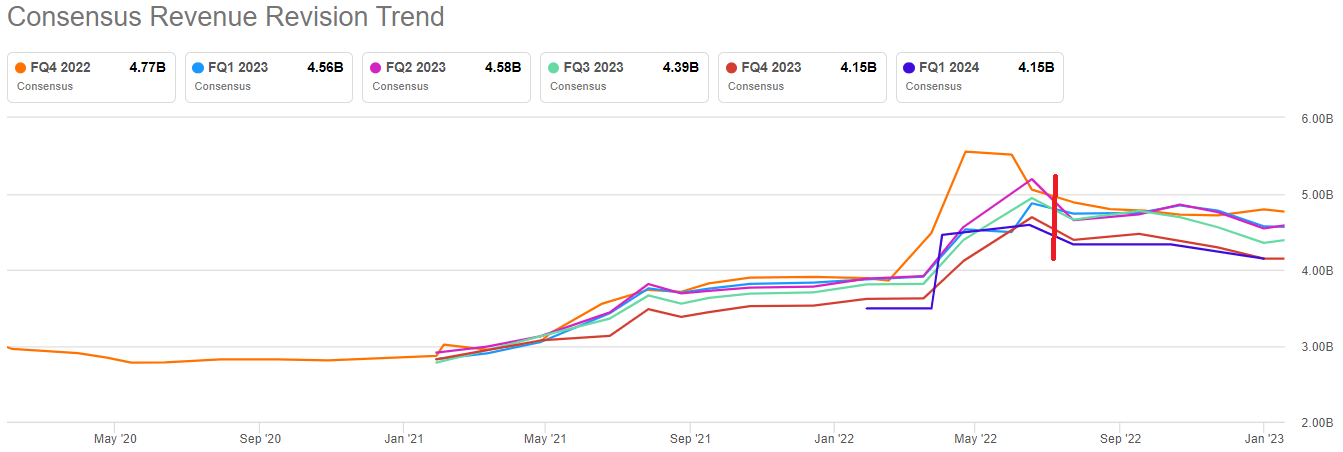

STLD Stock Valuation – 6x 2023 EPS

What you see in the graphic that follows is that analysts stubbornly refuse to upwards revise their estimates for STLD’s revenue targets for the upcoming quarters.

STLD revenue estimates

Even though we can see from the analysis presented here that steel prices are evidently on the rise.

And now get ready for my most shocking hypothesis of all. I believe that it’s entirely like that STLD earnings in 2023 could actually edge higher than the record EPS figures we witnessed in 2022!

What makes me say so? Several things.

- China is the biggest consumer of steel. With China’s real estate market finding support, what was a headwind in 2022, will become a tailwind in 2023.

- To embark on the Great Energy transition we must ramp up our energy infrastructure (this was already discussed above). Notable steel uses include onshore wind turbines and solar panels, but there’s much more.

- Steel prices are already climbing higher.

- STLD is repurchasing significant amounts of its own shares.

The Bottom Line

No investment is without risk. Here are several risks worth noting.

- One overhanging risk is that steel is a commodity.

- The other noteworthy risk is that with energy prices in Europe taking a breather, there are going to be a lot of idled factories eager to resume production. That may cause this tight market to become oversupplied.

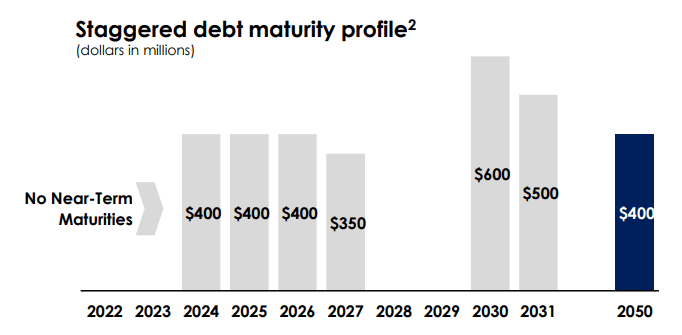

On the other hand, there are ample reasons to be bullish. For example, STLD has no material near-term maturities.

STLD presentation

And the debt stack that STLD has soonest, in 2024, amounts to $400 million, which is easily dealt with since STLD is making more than $1 billion of free cash flow every 90 days.

In sum, this is a cheaply valued cyclical stock that isn’t been appreciated by analysts and investors.

Be the first to comment