JohnFScott

Introduction

As a dividend growth investor, I seek new investment opportunities to generate income. I tend to add to my current positions when I believe they are undervalued. I also take advantage of market fluctuations by starting new positions to diversify my portfolio and increase my dividend income at a lower cost.

The consumer discretionary sector has become particularly interesting due to the possible impact of a weaker economy on consumer spending habits. Companies in this sector, which includes retailers, restaurants, and other businesses that sell non-essential goods and services, often see their sales fluctuate in response to changes in economic conditions. One company in the sector that is particularly interesting is Starbucks (NASDAQ:SBUX), which faces unique challenges due to the pandemic in China, where it has a significant presence.

I will analyze the company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company’s fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it’s a good investment.

Seeking Alpha’s company overview shows that:

Starbucks operates as a roaster, marketer, and retailer of specialty coffee worldwide. The company operates through three segments: North America, International, and Channel Development. Its stores offer coffee and tea beverages, roasted whole beans and ground coffees, single-serve products, ready-to-drink beverages, and various food products. The company also licenses its trademarks through licensed stores and grocery and food services.

Fundamentals

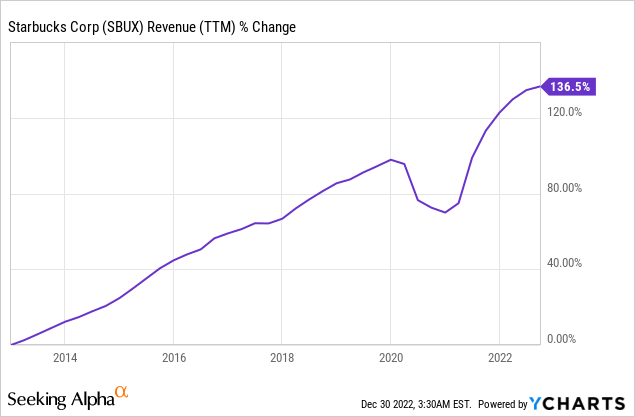

The revenues of Starbucks have increased significantly over the last decade. The 136% increase means the company has grown roughly 10% annually. It achieved this growth by opening more stores worldwide, increasing sales by offering more products, and luring consumers to spend more on every visit. In the future, as seen on Seeking Alpha, the analyst consensus expects Starbucks to keep growing sales at an annual rate of ~11% in the medium term.

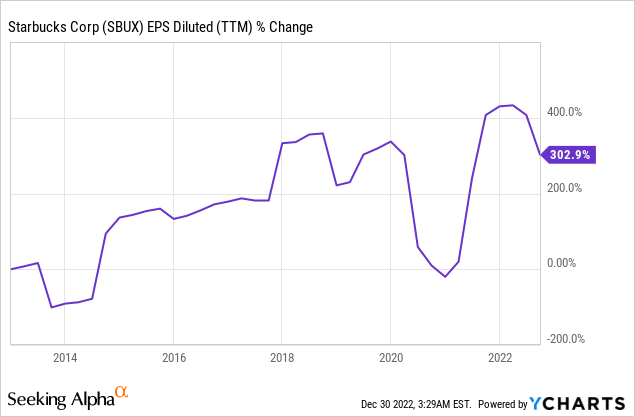

The EPS (earnings per share) has increased much faster over the past ten years. Starbucks managed to quadruple its EPS over the last decade. It combined sales growth with aggressive buybacks and margin improvements due to its investment in digital orders which allowed it to lower costs. In the future, as seen on Seeking Alpha, the analyst consensus expects Starbucks to keep growing EPS at an annual rate of ~17% in the medium term.

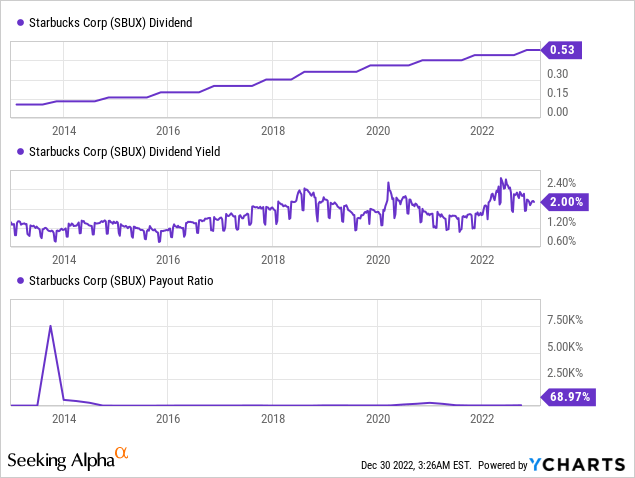

The company is still a relatively new dividend payer. It has a track record of twelve years of paying dividends. Since it started paying them twelve years ago, it has raised them annually. The current yield stands at 2%, and the payout ratio seems safe as the company pays 69% of its GAAP earnings in dividends. Investors should expect the dividend to keep growing at a double digits rate as the EPS is growing fast.

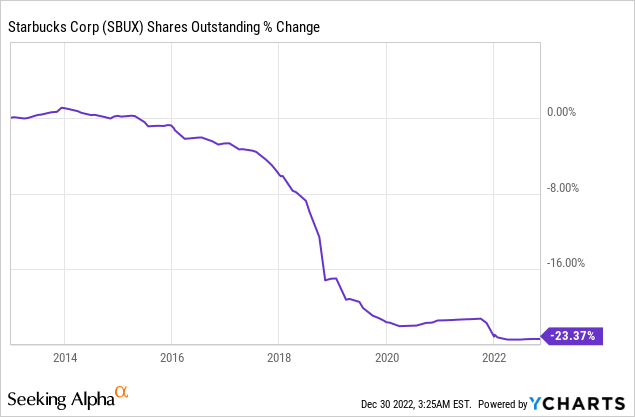

In addition to dividends, companies tend to return capital to shareholders via share repurchase programs. These buybacks support the EPS growth by lowering the number of shares. Starbucks has repurchased almost a quarter of its shares over the last decade. Buybacks have slowed since the pandemic, and they should be used especially when the share price is attractive, as every dollar can buy back more.

Valuation

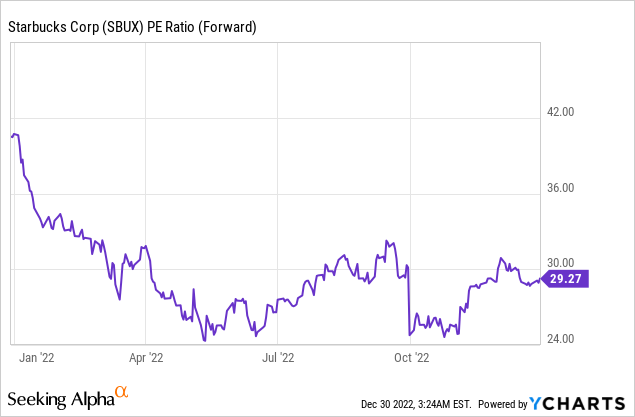

The P/E (price to earnings) of Starbucks stands at 29.27 when taking into account the forecasted EPS for 2023. This valuation is around the average over the last twelve months. A P/E of 29 doesn’t look expensive based on the chart, especially considering the forecasted growth rate. However, paying almost 30 times earnings for a company when the markets are highly volatile is challenging, especially when the company sells discretionary items.

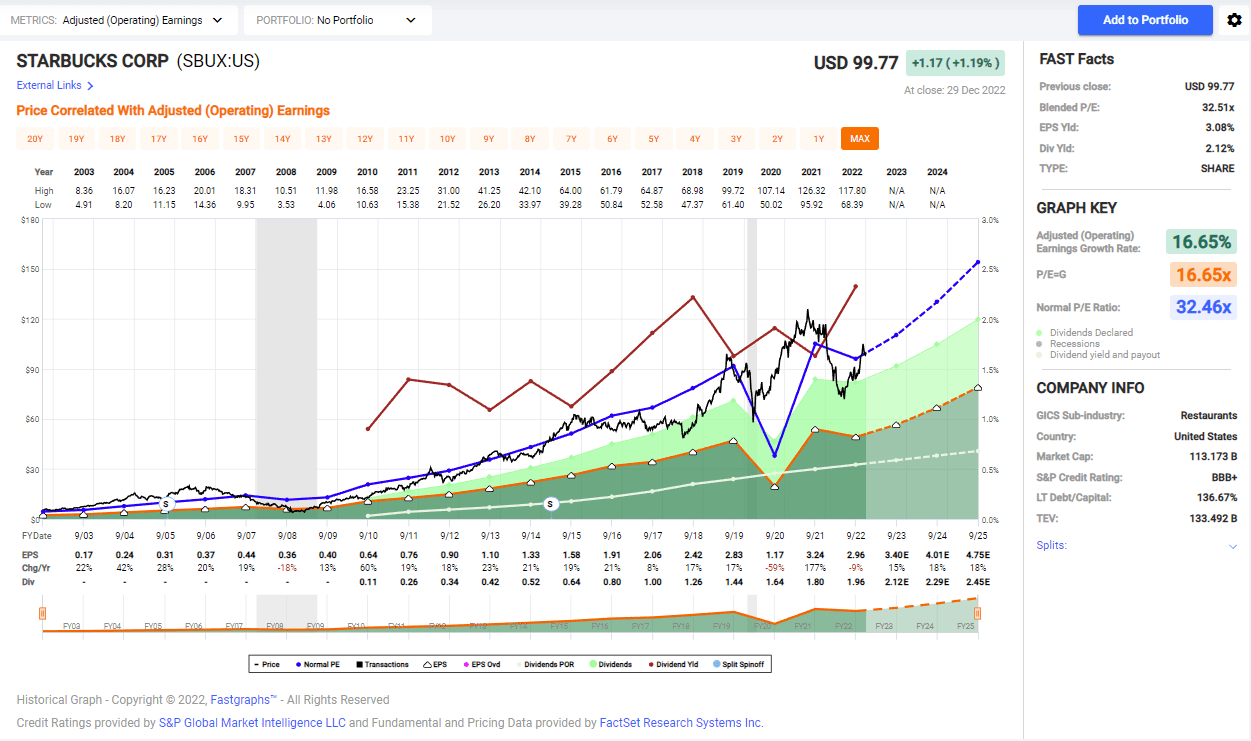

The graph below from Fastgraphs shows that Starbucks is trading for a valuation that aligns with its historical valuation. The company’s average P/E ratio over the last two decades was 32.5. Thus, the current valuation offers a 10% discount. The forecasted growth rate is similar to the historical growth rate. While the valuation is not outrageous, I am not entirely comfortable with it due to the uncertainty regarding the global economy and China in particular.

Fastgraphs

To conclude, Starbucks has demonstrated decent fundamentals and impressive growth over the years when examining sales, EPS, dividends, and buybacks. However, the company’s current valuation poses a challenge for potential investors. To justify its current price, Starbucks will need to show that it has excellent opportunities for growth and little risk of any negative impacts on its business.

Opportunities

Starbucks’ most prominent growth assets are strong brand recognition and customer loyalty. Starbucks has a well-known and highly recognized brand that has built a loyal customer base over the years. It has almost 30 million quarterly Starbucks Rewards in the U.S. alone. In China, nearly half of the orders come from the digital app supporting engagement. It provides a strong foundation for the company to grow and attract new customers.

Another opportunity for Starbucks is its diversified revenue streams. Starbucks has a diversified revenue stream, with a mix of company-owned stores, licensed stores, and other business segments such as packaged coffee and food products. Moreover, the diversification is also geographical, as the company has a significant international presence, which accounts for 21% of its sales. Diversification helps protect Starbucks from downturns in a specific region.

Starbucks’ diversification is helping it in protecting its sales streams, and it offers essential expansion opportunities. It has a strong presence in many global markets. However, there is still potential for the company to expand into new regions and markets, particularly in emerging economies where the demand for coffee and other specialty beverages is growing. China is still the most important growth market for the company. It expects new store growth of 13% there compared to 3% in the U.S. and 7% in other international markets.

Risks

Economic downturns or recessions impact consumer spending habits, which can negatively impact the sales of companies in the consumer discretionary sector, including Starbucks. During these times, consumers may be more hesitant to spend money on non-essential items such as specialty coffee drinks, which could lead to lower sales and profits for Starbucks. Additionally, the inflation we see pressures the company’s expenses. Thus, Starbucks may face increased pressure to increase prices.

Starbucks faces competition from other specialty coffee chains, as well as from fast food chains and other food and beverage providers. It can impact the company’s market share and profitability. During that inflationary period, an increase in the price may lead to a lower market share. It’s crucial to remember that the barrier to entry into the segment is not very high. Therefore, changes in consumer preferences due to pricing, the economic downturn, or new offerings from competitors pose a significant risk.

China has recently been a challenge for Starbucks, with comp sales down 24% in 2022. The country has faced several economic and health-related issues that have impacted the company’s operations. Initially, Starbucks faced challenges when the Chinese government closed many of the country’s businesses to contain the spread of COVID-19. Even after the stores were allowed to reopen, the pandemic continued to impact Starbucks’ business in China. First, many consumers were hesitant to leave their homes and go out to eat or drink. It led to a decline in foot traffic and sales for the company, and the country has suffered from high cases. Since China is the primary growth prospect, weakness there poses a risk for Starbucks.

Conclusions

Overall, Starbucks is an excellent company with solid fundamentals and a long track record of growth. The company has a strong brand and customer loyalty, diversified revenue streams, and expansion opportunities in new markets, which bode well for its long-term prospects. Additionally, Starbucks has shown a willingness to adapt and innovate in the face of challenges, which has helped it maintain its market leadership and continue growing. While there are risks to investing, it is worth noting that many of the risks facing Starbucks are mainly in the short- and medium-term, such as the impact of the pandemic or economic downturns. In the long term, the company has the potential to continue growing and delivering value to shareholders.

Based on the current situation, it appears that Starbucks is a HOLD. While the company has solid fundamentals and a long track record of growth, the current challenges in China and the ongoing impact of the pandemic have raised uncertainty about the company’s future performance. As a result, the current valuation of the company may not fully reflect the potential risks and challenges that it is facing. In March, I wrote that the stock was a BUY for $89, and I believe it is still the case.

Be the first to comment