Spencer Platt/Getty Images News

Introduction: Consumer Vs. Investor Lens

Starbucks (NASDAQ:SBUX) is an example that investors shouldn’t always invest in companies in which they shop at. As a consumer, Starbucks provides an adequate value add as I am a huge fan of their product offering and branding. On the other hand, as an investor, the taste doesn’t sit with me as well as the beverages do. To begin with, Starbucks’ fast delivery endeavors could become slightly curtailed in the short term as fast delivery traffic has seen consistent negative growth quarter-over-quarter. Additionally, with the U.S. citizen’s debt building up, consumers could become reluctant to spend money on premium beverages. Secondly, Starbucks’s financials are sub-optimal, with a growing debt position and lower free cashflow margins. Finally, when considering the current interest rate environment, the company’s valuation is unappealing.

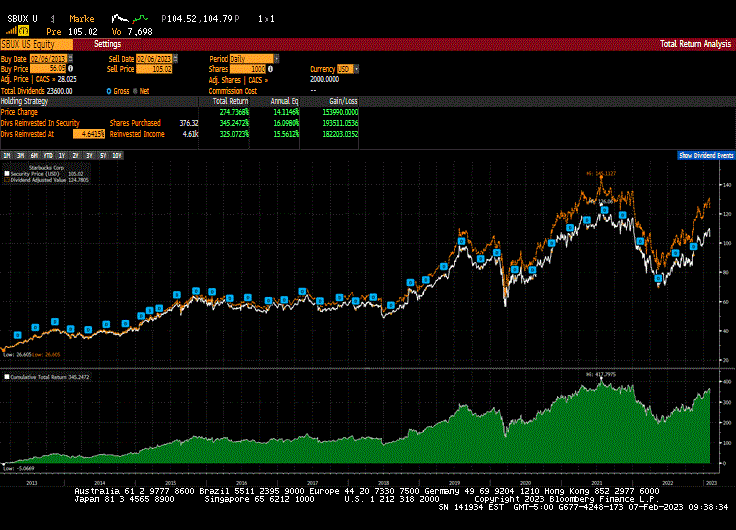

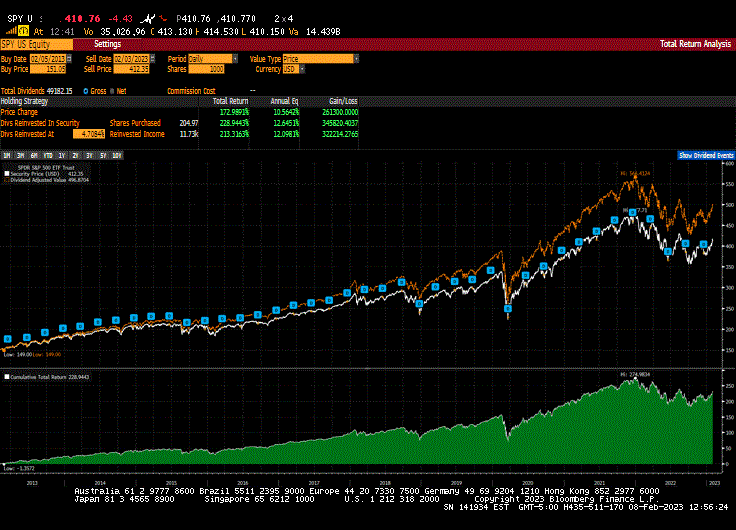

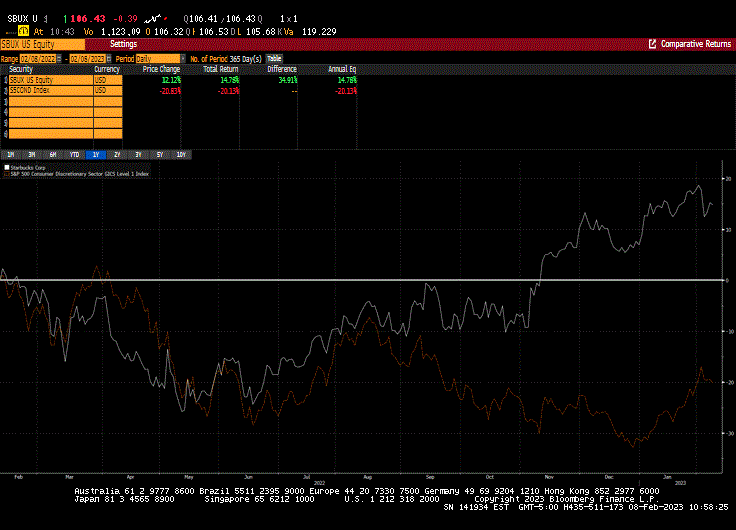

Starbucks Has Brewed Strong Long-Term Stock Price Performance

There is no doubt that empirically speaking, Starbucks has provided investors with adequate total returns. Over the previous 10 years, Starbucks has beaten the S&P 500 on a total return basis.

Bloomberg Bloomberg

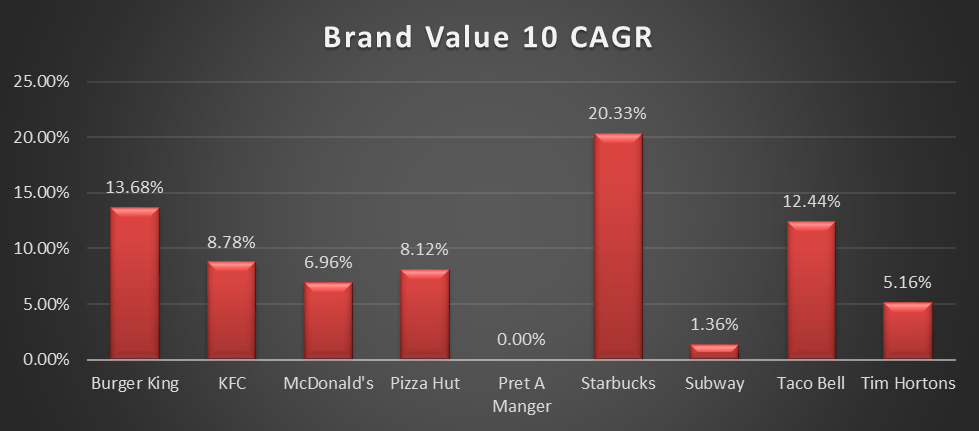

The greatest driver behind Starbucks’ previous success is its immense brand value growth obtained over the decades. Compared to its closest rivals, Starbucks has seen the greatest brand value growth over the last 10 years and by a significant margin.

Excel

Starbucks’ brand value is what has given them a competitive advantage over its competitors and what has also led to market-beating shareholder returns. With that being said, although the past 10 years have been great for Starbucks’ management and shareholders, the current valuation appears stretched when looking at the near-term hurdles that they’ve faced.

Starbucks’ Growth Could Slow As Economic Headwinds Eventuate

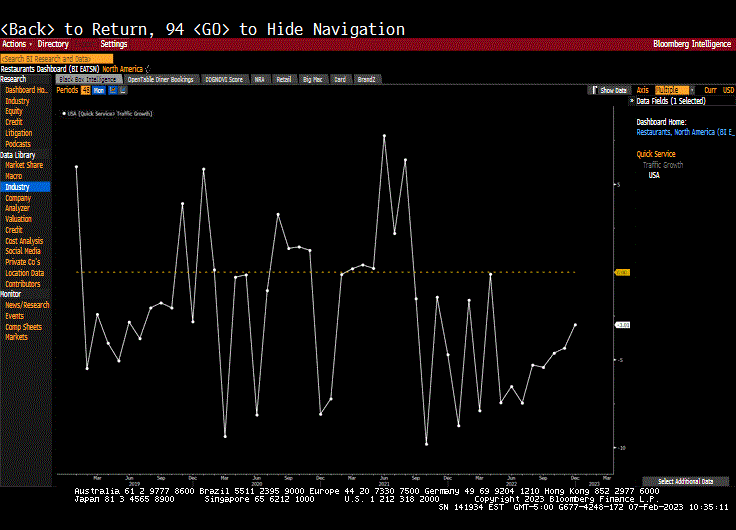

Firstly, Starbucks’ new initiative of being a quick delivery food and coffee place faces headwinds as quick delivery restaurants have been seeing a persistent decline in foot traffic QoQ.

Bloomberg

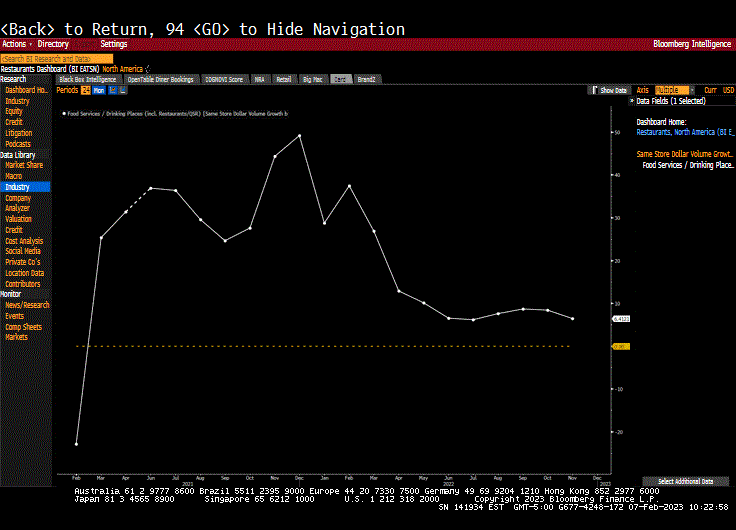

As seen in the chart, foot traffic for quick food services has been seeing persistent negative growth rates since mid-2021. Although the growth rates in foot traffic fluctuate greatly, it appears that in 2022 foot traffic growth has consistently stayed below 0%. The near-term decline in consumption of quick food services could provide some headwinds curtailing Starbucks’ ability to maximize its new convenience initiative. The second hurdle facing Starbucks affects its main pipeline, the growth in spending on food services has diminished since the 2021 highs.

Bloomberg

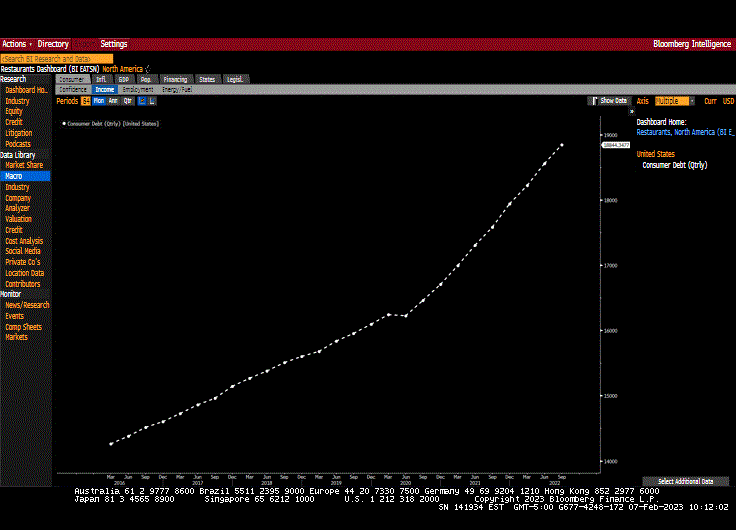

As you can see, growth in food services spending has completely been erased. When accounting for the fact that consumer debt has skyrocketed over the years, it is reasonable to assume that the trend in food spending growth could turn negative in just a few quarters. This could put pressure on Starbucks’ sales and potentially hinder revenue growth in subsequent quarters.

Bloomberg

Although I like Starbucks’ recent partnerships with DoorDash (NYSE:DASH) providing them with the national reach to provide quick delivery to all of its customers, the economic environment is leading towards an uphill battle for the firm to optimize its quick service initiative. Furthermore, the cooling U.S. economy could affect Starbucks’ main pipeline due to a distraught American consumer becoming reluctant to spend money on premium beverages.

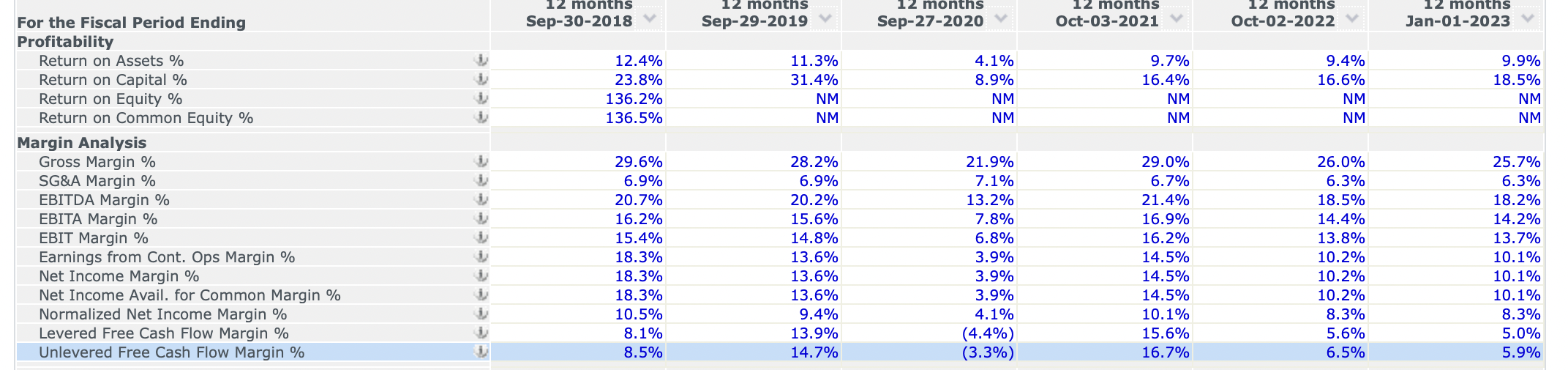

Uncovering Starbucks’ Financial Performance

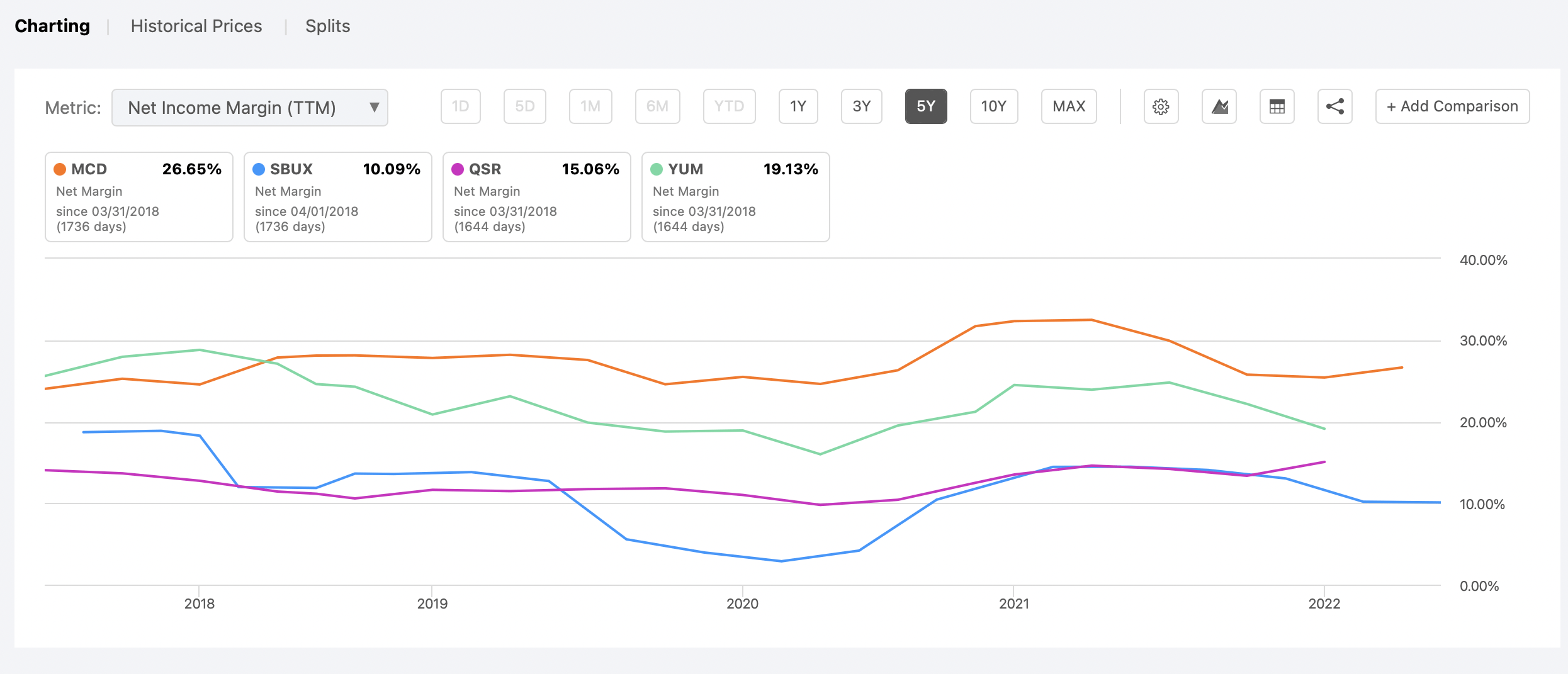

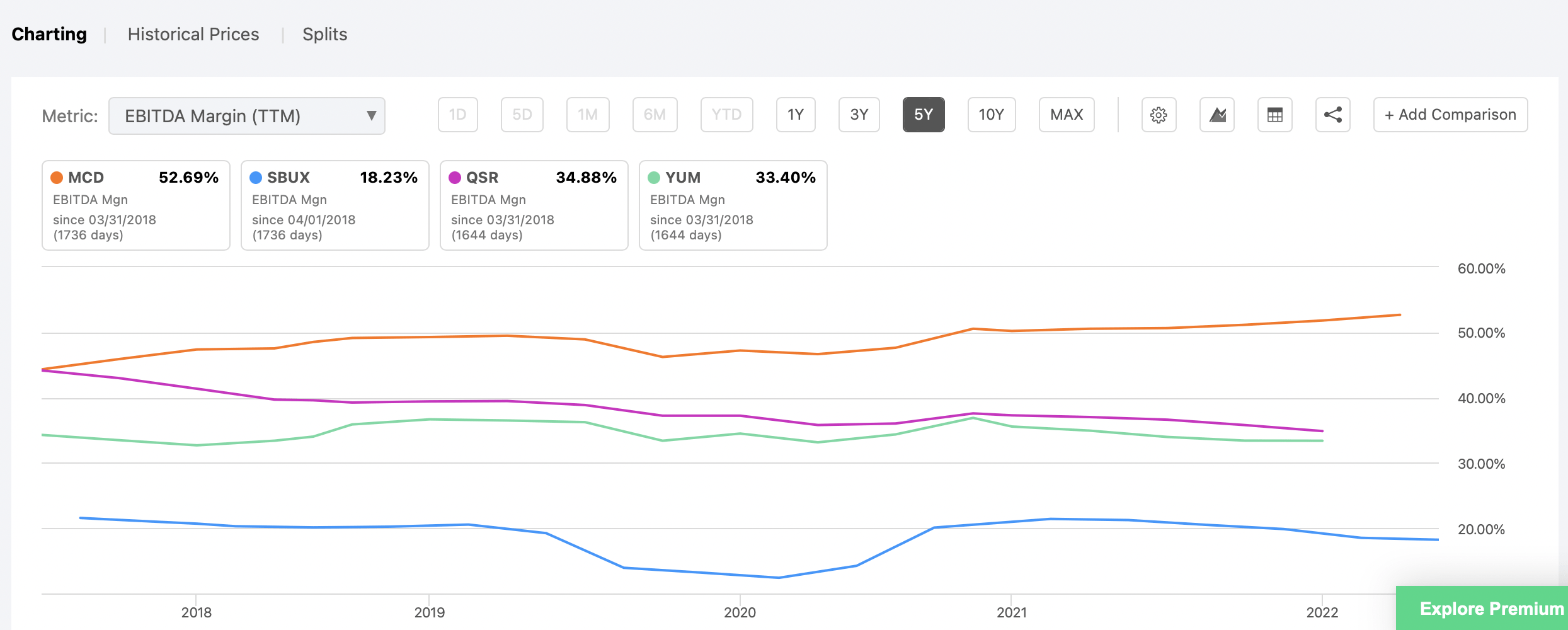

Starbucks’ financial performance leaves a lot to be desired, especially when conducting a time-series analysis comparing their financial situation to prior years. Let’s first look at Starbucks’ profitability, the charts displayed show the company’s net income and EBITDA margins compared to its closest peers.

Seeking Alpha Seeking Alpha

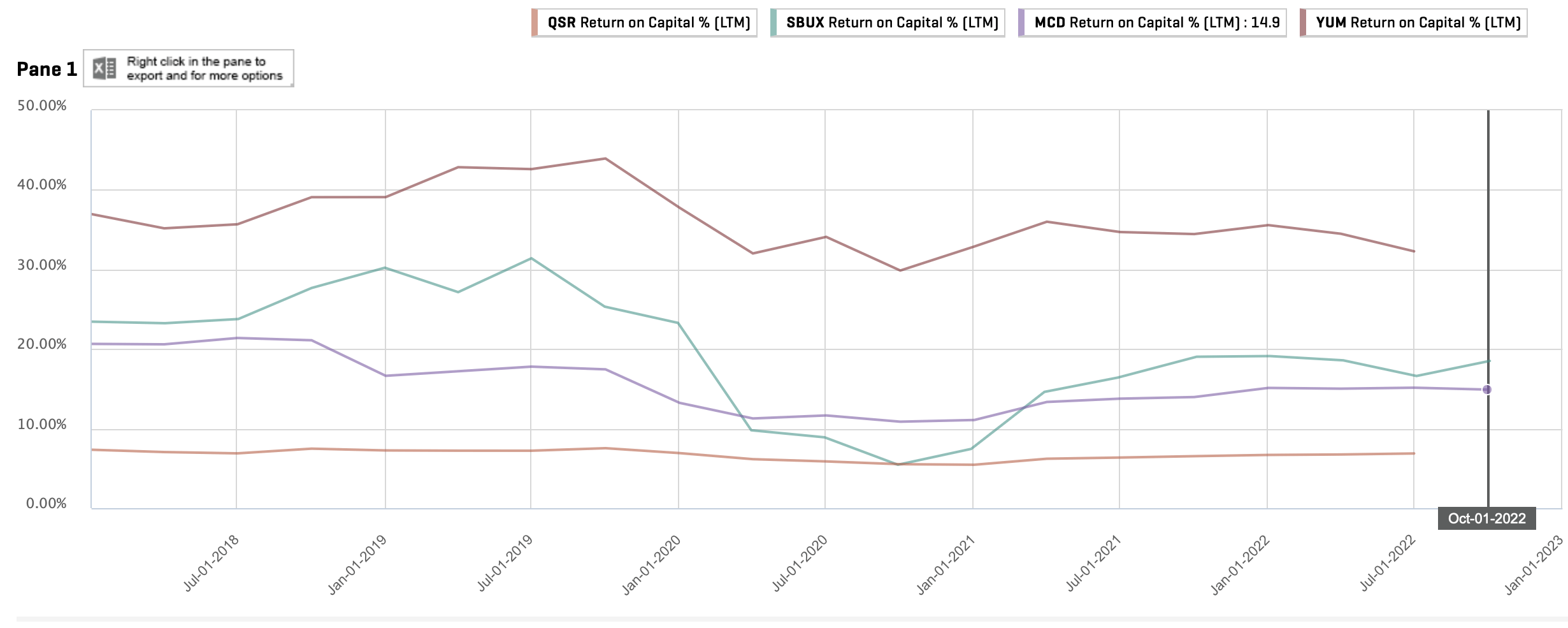

As you can see, Starbucks’ net income and EBITDA margins are inferior relative to its closest rivals. Notably, Starbucks’ EBITDA margins have been consistently lower than their closest peers. Although Starbucks may be able to grow its brand significantly, they have not been as good at yielding a profit for every dollar that they generate. Moving on from margins, Starbucks’ return on total capital has been consistently average when compared to its closest peers. However, given Starbucks’ rich valuation, you would think that they’d be superior to the competition.

Capital IQ

Next, we will assess Starbucks’ balance sheet. A big positive about Starbucks is that they’ve consistently returned cash to shareholders not only through dividends but through a reduced share float. Over the previous 5 years, Starbucks has reduced its share float the most on an annual basis relative to its closest peers.

Excel

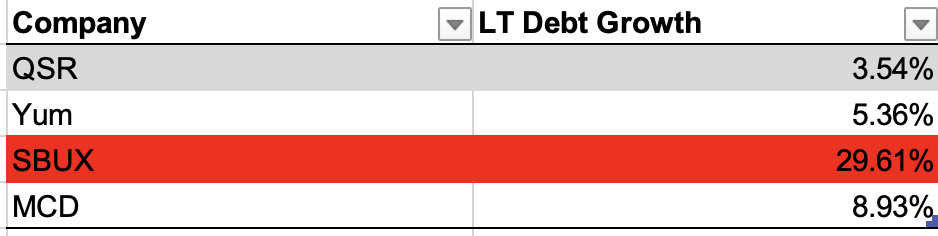

However, it is important to note that while servicing these buybacks, dividends, and various other capital expenditures, the company has been racking up debt at a massive pace. The following is the 10-year long-term debt growth of Starbucks and its peers.

Excel

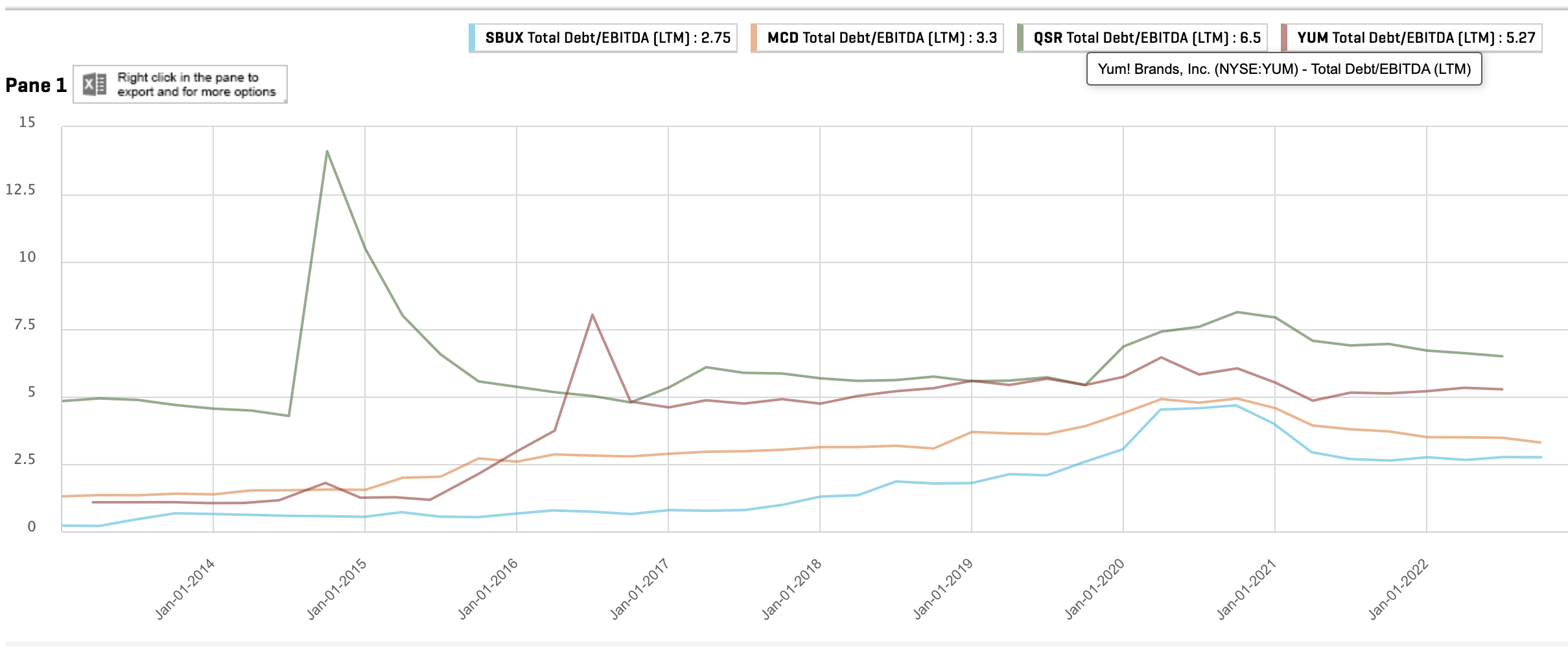

Although a lot of companies felt comfortable with a debt-heavy balance sheet due to interest rates remaining low for so long, Starbucks in particular has ballooned its long-term debt load over the recent years. Fortunately, even with the company’s highly increasing leverage, its solvency remains superior to its rival firms when looking at Total Debt-to-EBITDA.

Capital IQ

Although Starbucks’ solvency hasn’t shown too much vulnerability through its solvency ratios, investors should not ignore the massive debt load the company has brought on, especially if you are seeking for dividend growth. Finally, we have the cash flow statement. Starbucks’ free cash flow margin has been declining every year when you exclude 2020.

Capital IQ

The combination of lower free cash flow margins and higher leverage has made Starbucks’ financial position more distraught than in previous years. This should be concerning for investors since part of the marketability of Starbucks shares are cash returns to shareholders. Any declines in these shareholder rewards could lead to a negative material impact on its share price. Overall, Starbucks’ financial position is modest at best.

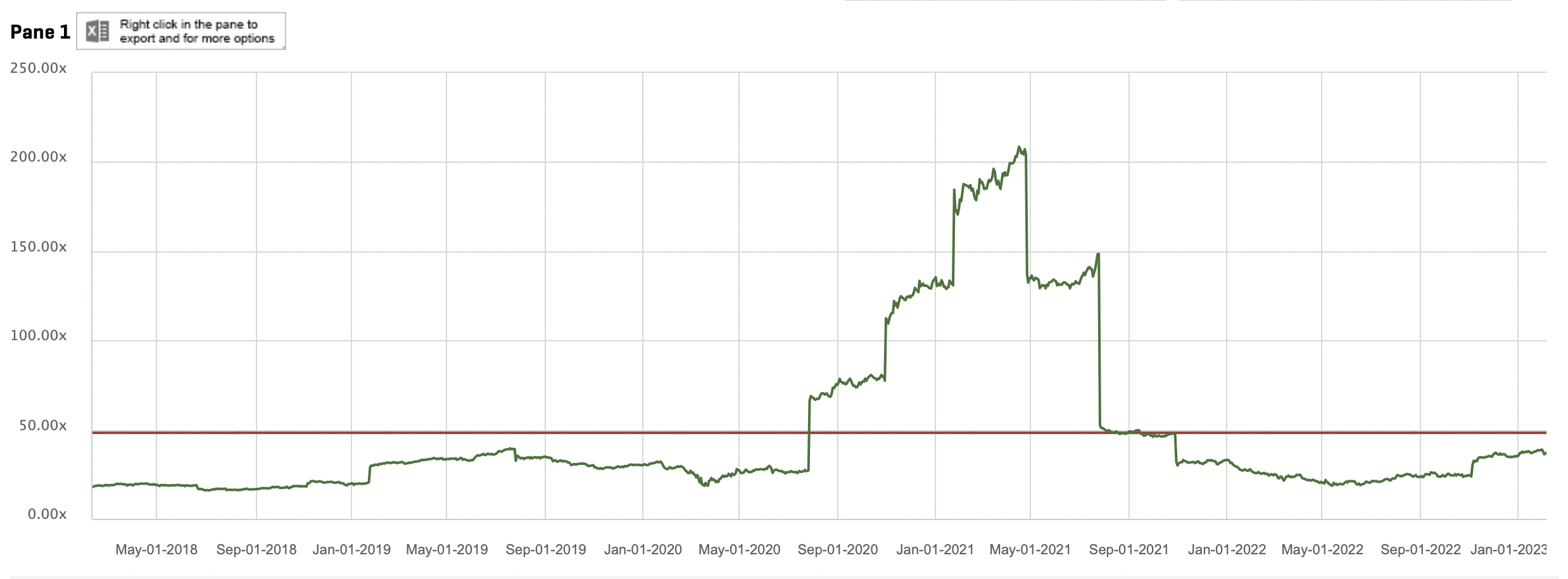

Valuation: Overpriced All Factors Considered

When looking at Starbucks’ current price-to-earnings multiple over a historical basis, one might think its shares are fairly priced considering its 5-year mean P/E ratio is above its current P/E multiple. The thesis behind this would be that because Starbucks is trading at a lower multiple than usual, its shares must be undervalued.

Capital IQ Starbucks

However, when considering that interest rates are significantly higher than in previous years, I still think that Starbucks’ P/E multiple is too high. Trading multiples and interest rates are negatively correlated, and interest rates are significantly above their 5-year mean, whereas Starbucks’ P/E multiple is only slightly below its 5-year mean. On top of that, despite a sub-optimal financial position and deteriorating data in the food services sector, Starbucks shares haven’t been slumping as much as the rest of the food services sector. In fact, there has been some short-term divergence.

Bloomberg

This points to further evidence that mean reversion is a high possibility for Starbucks shares. Therefore, Starbucks shares are overpriced.

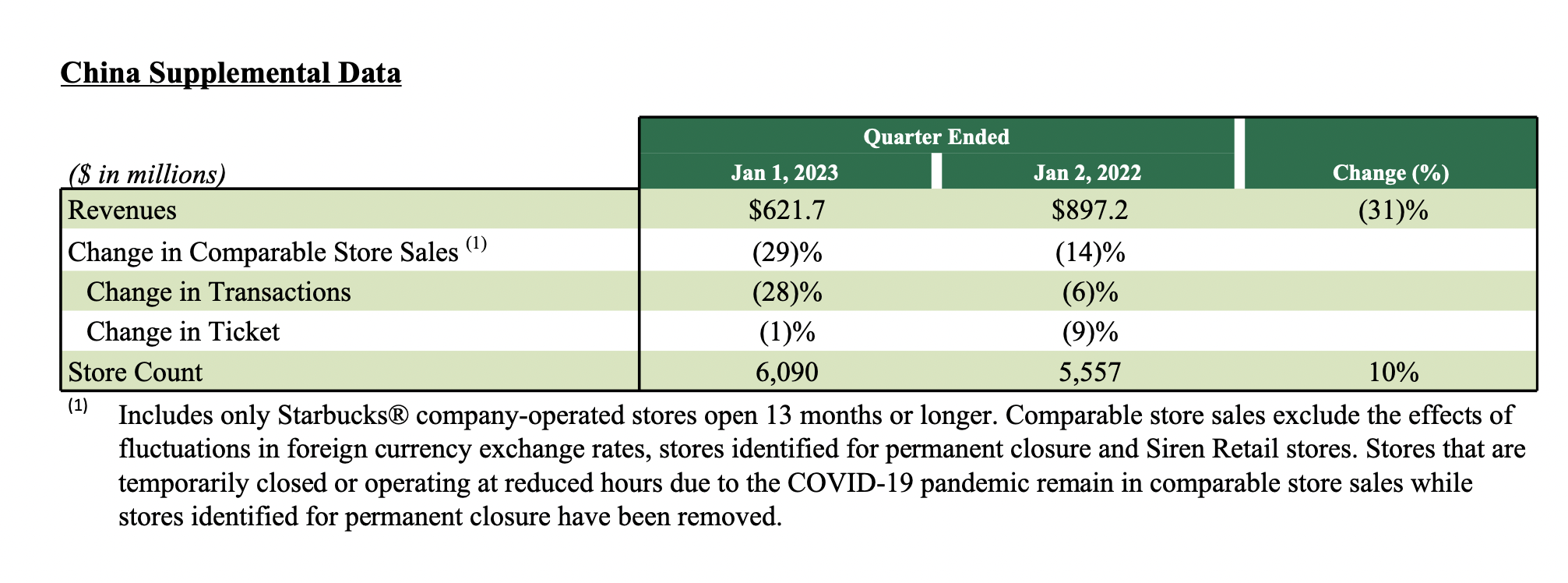

Risk To The Thesis: China Reopening And Solid Q1 All Things Considered

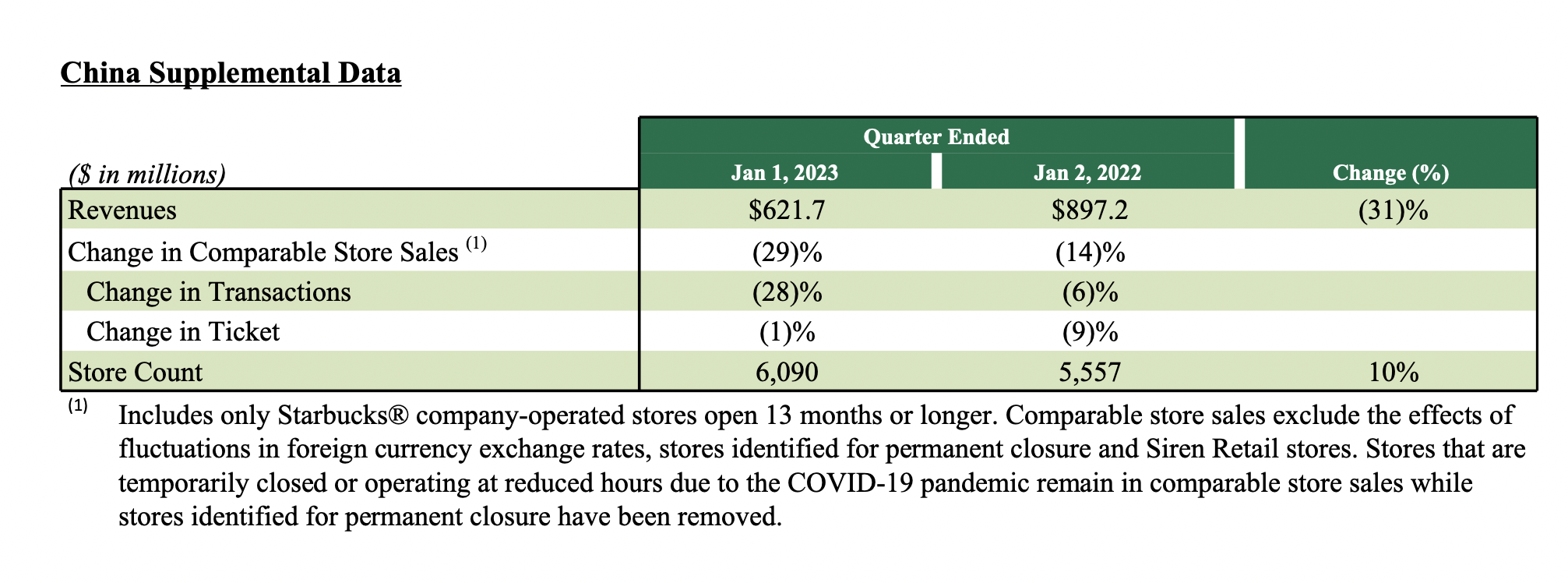

Despite the modest earnings miss in Q1, Starbucks provided some positive forward-looking catalysts. To begin with, growth in China was curtailed by locked-down restrictions which now appear to be easing. Meanwhile, the company obtained an all-time weekly active customer base with 100 million weekly customers.

Starbucks

Furthermore, Starbucks’ rewards program has seen significant growth of 15% YoY. Finally, Starbucks had the second most holiday gift card activations of any U.S brand. Discounting the China lockdowns, Starbucks’ business thrived in Q1, indicating that the business is under no real duress. In my opinion, this is what has been supporting its triple digit share price because management has reaffirmed its 2023 guidance, reassuring shareholders.

Conclusion: Great Business, Great Previous Returns, Not So Great Timing

To conclude my dive into Starbucks, the company has impeccable brand recognition and is an overall fantastic business. That being said, the valuation appears to be a stretch, especially when their financials aren’t as good as in previous years. Additionally, when you consider the fact that Starbucks is still trading at a high multiple when investors no longer need to seek yield, the company is overvalued. I’m staying out of Starbucks for now, but I’m open to give it another look in the future if there’s a drawback. Starbucks offers a great product and has very robust long-term industry economics. That being said, 2023 is not the year to be buying Starbucks shares.

Be the first to comment