Hleb Usovich/iStock via Getty Images

The construction and home improvement market surged in 2020-2021 as government stimulus, low-interest rates, and extra free time among people (due to lockdowns) created a goldilocks market. Many real estate and construction stocks surged as corporate profits skyrocketed. However, the sharp rise in interest rates last year quickly ended the housing boom. Home sales have plummeted, and developers are racing to reduce inventory and halt new projects.

This pattern has brought most construction-centric stocks along for a very tumultuous ride. One notable example is Stanley Black & Decker (NYSE:SWK), which sells tools for home improvement hardware and related items. The stock doubled in value from 2016 to 2021 as many people and companies looked to upgrade items, and overall construction and home improvement activity rose. Since reaching its 2021 peak, the stock has quickly lost over half its value and is now trading slightly below its 2020 crash minimum.

Stanley has been hit by multiple negative catalysts simultaneously. The rise in material, labor, and energy costs has negatively impacted the firm’s profit margins. Additionally, demand for the company’s tools has declined dramatically, with construction levels falling and household real disposable incomes collapsing. To make matters worse, the company dramatically increased its financial debt in 2020, giving it excessively high-interest expenses and leverage this year. Today, Stanley is sitting with high inventories, low cash, and falling sales, which could lead to bankruptcy if prolonged too long. Of course, if the severe financial strain is avoided, SWK may be trading at a discount today and could be seen as an opportunity for “fire sale” oriented investors. Still, bullish investors may want to consider the significant economic risks facing the firm that are primarily outside of Stanley’s control.

An Economic Storm Hits Construction Market

Stanley’s largest segment is its outdoor tools segment ($12.8B in sales), while its smaller business-oriented industrial segment makes up around $2.5B in annual sales. Nearly half of Stanley’s outdoor tools sales come from power tools, the company’s most important product segment. Power tools are sold both to households and construction-centric firms. The company has become highly consolidated with brands including DeWalt, Stanley, Craftsman, Black & Decker, and more.

Power tools are higher-cost items that most buyers will only purchase once every decade or more. When the property market slows, construction activity stalls; when construction activity stalls, power tool sales collapse. While Stanley sells many products not directly tied to the broader construction market, its business model is exceptionally cyclical since most power tool buyers can delay purchase indefinitely in times of strain.

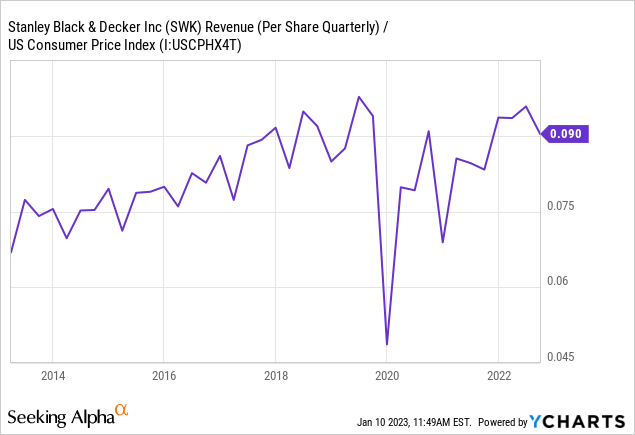

The past two decades saw significant improvement in many power tool technologies (cordless battery technology) that sufficiently aided demand growth to offset cyclical risks. Today, there are far fewer new large technological jumps in the power tools industry, so there is less of a growth cushion to offset cyclical risks. Indeed, this exposure may also be elevated due to the larger scale of Stanley’s operation and potential competition among its brands (considering it owns various brands that sell essentially the same products). As you can see below, inflation-adjusted sales of the company’s products have been stalled since around 2018:

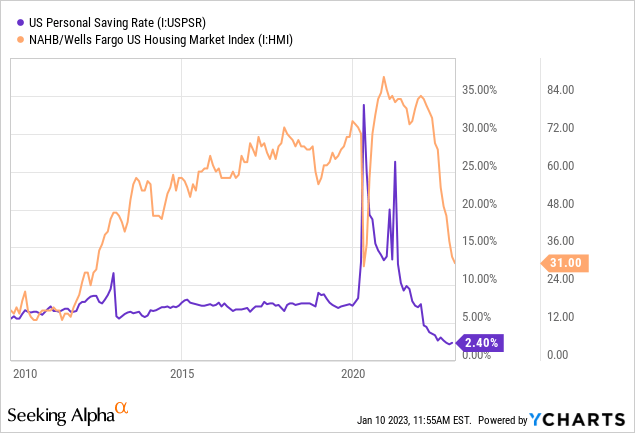

After a significant sales decline at the beginning of 2020, Stanley saw real sales recover to pre-pandemic levels. The firm’s quarterly real sales per share are still near all-time-high levels but are no longer growing at the pace they were before the pandemic. Further, economic trends signal a likely decline in demand in 2023. On the consumer front, falling real wages and rising living costs have caused personal savings to decline to extreme lows, meaning most people will likely avoid unnecessary larger purchases. On the construction side, plummeting home sales have led to a massive decline in homebuilder confidence, indicating low forward demand for tool upgrades. See below:

These trends will likely persist or worsen in 2023 as interest rates remain high and the US economy probably enters a recession. I believe Stanley’s sales are likely to decline more during a recession than in 2008 due to a decrease in endogenous growth factors (i.e., technological improvement) and the increase in consolidation that drives competition between products sold by the company. Of course, negative cyclical periods can be suitable buying points as companies can turn around faster than anticipated. However, Stanley’s internal business carries risks that may hamper its recession cushion.

Beware of High Debt and Falling Margins

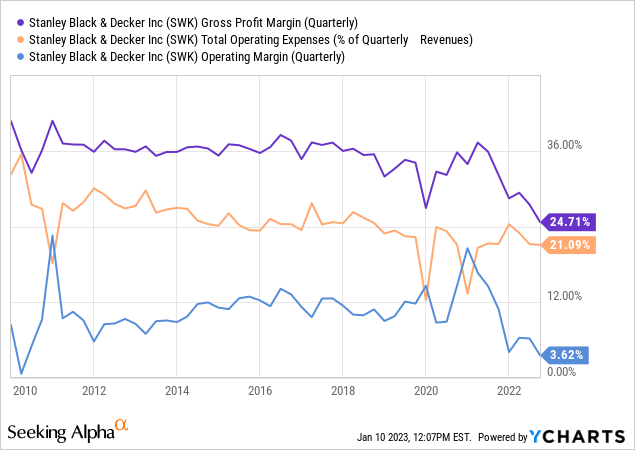

Typically, economic recessions do not jeopardize firms as sales are expected to recover quickly after GDP growth returns. However, Stanley is entering this period with high inventories, low cash, and falling profit margins. These issues extend from ongoing supply chain turbulence and rising production costs. Raw material costs, industrial worker wages, and energy (including transportation) costs have risen dramatically, creating multiple strains on Stanley’s gross and operating margins. See below:

The company’s gross margins have decreased over the past decade, with substantial declines starting in 2019 (indicating the trend began before COVID). Operating costs-to-sales declined during much of the 2010s, offsetting gross margin declines. However, the company appears unable to improve operating efficiency any further while its gross margins are falling even faster, causing its operating margin to collapse to only 3.6%.

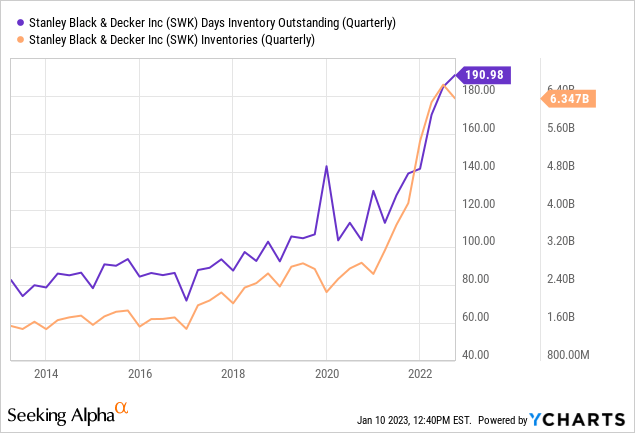

According to the company, its gross margins plummeted last quarter as it pursued discounts to reduce its total inventory level. In my view, investors should not consider that a “one-time” issue since its inventory remained elevated at the end of the quarter and its sales slipped, indicating the discounts were not necessarily significant enough. The trend in Stanley’s gross margins appears to be correlated to the pattern in its Days Inventory Outstanding ratio. The firm’s inventory-to-sales have risen over the past decade but has seen immense acceleration since 2018-2019. See below:

In my view, these financial data paint a relatively clear picture that the firm is struggling to keep up with competitive, economic, and industry-specific pressure. To grow and maintain sales, Stanley has had to reduce prices compared to production costs but has still seen inventory levels rise disproportionately. Today, the company has a higher inventory level, creating jeopardy if the firm is indeed facing a recessionary situation.

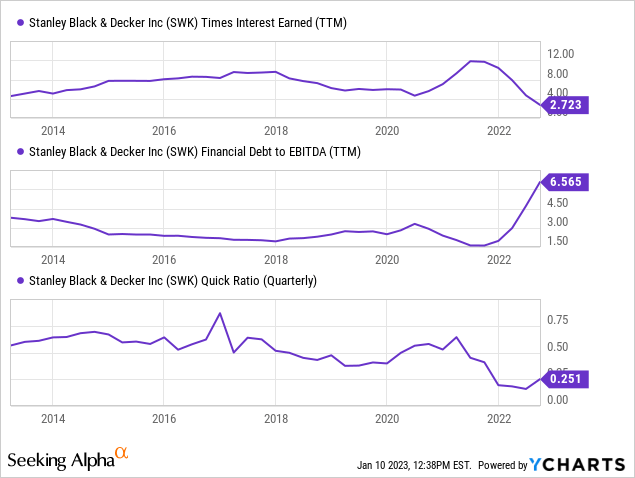

Even more, its Times Interest Earned (EBIT to interest costs) has crashed, its financial leverage has risen, and its liquidity has collapsed over the past year. See below:

Stanley Black & Decker’s debt level rose dramatically last year as the firm borrowed to offset negative cash flows while pursuing strategic divestitures. The company’s financial debt to EBITDA level remains excessively high at 6.5X, and it is paying much of its EBITDA to interest costs now that interest rates are rising. The firm aims to reduce its leverage this year, which may be difficult due to its low cash levels compared to current liabilities (quick ratio) amid its decline in profit margin. The company also suffered a credit downgrade last month as Moody’s reassessed the firm’s elevated credit risk level.

The company’s management is aware of its core issues, most of which stem from its vast size. Stanley’s managers are looking to reduce the number of SKUs to avoid product competition and improve manufacturing and supply-chain efficiency. The firm is also reducing its headcount and pursuing strategic asset sales to improve profit margins. While these are all positive changes, I believe they may prove “too little too late” as the company must strengthen its margins dramatically to offset likely sales declines if a recession occurs. Given the state of its balance sheet, it may not have sufficient liquidity if operating cash flows remain negative and inventories do not decline. While the firm can pursue financing options to improve its liquidity, I believe it is at relatively high restructuring risk if the global economy enters a prolonged recession.

The Bottom Line

SWK has declined by over 50% from its peak and has carved out a support level around the $80 price point. The stock stopped falling around October, coinciding with the inflation data turnaround. Hypothetically, if economic trends shift to support demand and lower producer cost inflation, Stanley may be trading at a decent valuation today. That said, even if the company returns to its peak annual EPS level of ~$10, its forward “P/E” today would be ~8X. In my view, that is not necessarily a low valuation for a highly cyclical and leveraged company.

I believe it is significantly more likely that cost-push inflation trends continue to strain Stanley’s margins while recessionary dynamics may cause its sales to decline. Under this scenario, SWK would likely fall from its current valuation as the company must improve its cash and inventory position, meaning equity sales, new debt, and dividend cuts are likely. Indeed, I would not be surprised to see Stanley slash its dividend in the immediate future if its position worsens again in its upcoming earnings report.

Overall, I am bearish on SWK and believe it will likely decline in value over the coming year. Fundamentally, I do not believe SWK is trading at a true “discount” today since its valuation is not sufficiently low, even under the best-case scenario. In my view, the company’s financial position is not strong enough to come out of the recession without permanent impairment. Still, I would not short the stock at its current price as it may rise from its support level if it garners sufficient technical support. That said, if SWK’s trend reverses to the downside, it may become a short opportunity due to its high cyclical risk exposure.

Be the first to comment