Bet_Noire

SPDR S&P 500 Trust ETF (NYSEARCA:SPY) is up by almost 15% since the Oct 13th, 2022, intraday low at 3491. Some analysts are predicting that the October 13th bottom is the bear market low point and that stocks are currently in a new bull market.

For example, Ed Yardeni predicts that “stocks are back in a bull market as global economic outlook is improving,” mostly due to China reopening. Also, Jermey Siegel thinks that “we are on the cusp of a new bull market because inflation continues to cool.”

It is important for investors to understand the bearish and the bullish arguments, and hopefully, get enough information to make their own decisions.

So, in this article I analyze the contrarian bullish thesis and arguments that the bear market bottomed on Oct 13th, versus the prevalent opinion on Wall Street that the bear market has not bottomed yet.

The bullish October bottom arguments

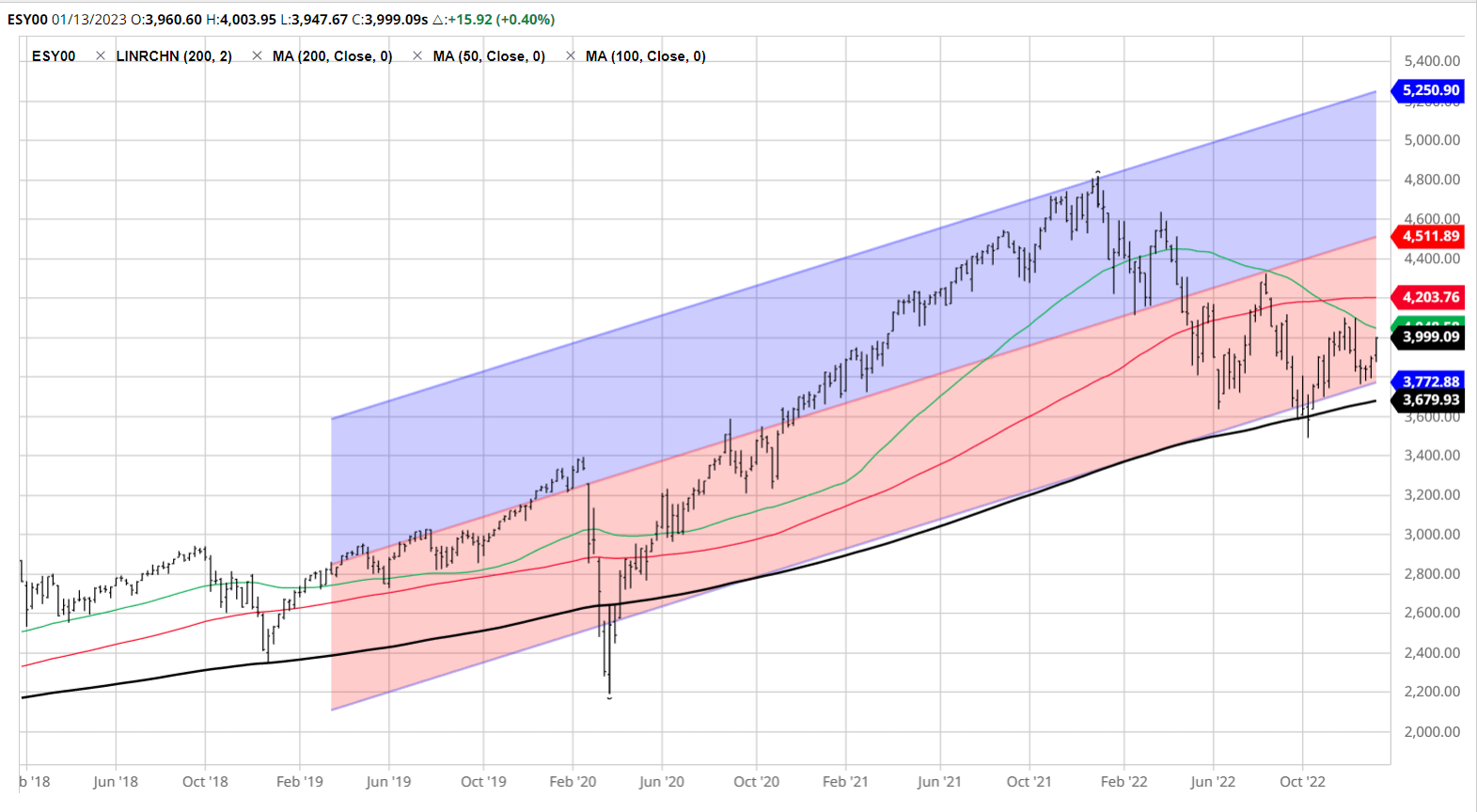

Let’s look at the weekly chart to get the longer-term perspective on the unfolding bear market in the S&P 500 Index (SP500). On October 13th, 2022, the S&P500 dropped below the key long-term support level 200wma on an intraday basis, and quickly bounced back above the support level without an immediate fundamental trigger – no major policy action on that day. Note, the breakdown below this level would have violated the long-term uptrend – thus, technically this was an important event. However, it is important to emphasize that the Oct 13th bottom was purely technical in nature, without any fundamental justification.

Barchart

The China reopening rumors appeared on November 4th, well after the October 13th bottom. At first, these rumors were dismissed by the Chinese government. However, subsequently, after the widespread protests, the Chinese government authorized the sudden end of the covid-zero policy and an uncontrolled reopening. The Chinese reopening is likely to cause the boost to the Chinese economy over the near term, which could benefit the regional economies as well as Europe, and broadly buffer the global economic slowdown caused by tighter monetary policy. Note, since the China reopening, the U.S. Dollar has considerably weakened, which supports the global economic recovery thesis.

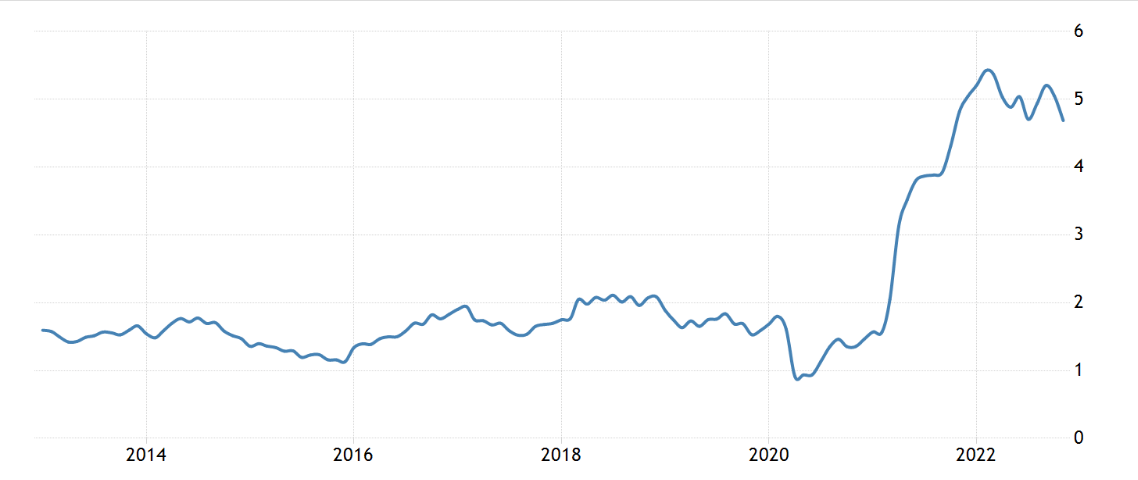

The Fed’s preferred inflation measure Core PCE peaked at 5.4% in February 2022, and in November it was at 4.6% and expected to be at 4.4% in December 2022, and 4.3% in January 2023.

Trading Economics

So, it’s correct: the inflation perhaps has peaked and it is falling. The argument is that the falling inflation will cause the Fed to be less hawkish. Currently, the Fed is signaling an increase in the Federal Funds rate to 5.1% and no rate cuts in 2023. The market is looking at the falling inflation and assuming that the Fed will hike to 4.9% by June 2023 and subsequently cut the rates in late 2023 – thus a more dovish Fed. This has also supported a weakening U.S. Dollar.

The U.S. labor market remains amazingly resilient despite the tighter monetary policy in 2022. The unemployment rate has actually decreased to 3.5% in 2022. The argument is that the Fed will conclude the monetary tightening campaign in 2023 without causing the damage to the labor market, which increases the probability of a soft landing. In other words, the Fed will pivot before the anticipated recession arrives, which opens the 1995-type super bullish scenario.

The bearish arguments

As already explained, the October 13th bottom was purely technical in nature, without any fundamental justification. Subsequently, the China reopening emerged as one of the key bullish variables, along with the falling inflation.

- The recession is inevitable

However, the recession is inevitable because the Fed needs the recession to restore the price stability at the 2% inflation target. Yes, the inflation is falling, but it is likely to stop falling at a level much higher than the 2% target level, because:

- There is a significant labor shortage, as measured by the jobs-worker gap, which ensures that wage inflation will remain elevated and keep the service inflation elevated as well. The Fed is committed to increasing the unemployment rate to at least 4.6%, which by definition creates a recession.

- The capacity utilization is at the 90% level, which historically caused the Fed to induce a recession.

- The China reopening is likely to cause the higher commodity prices over the near term, which will only complicate the falling inflation narrative.

- The Russia-Ukraine war is still unfolding, and the energy shock probability is still high.

- Longer-term, the unfolding trend of de-globalization and reshoring/onshoring is inflationary.

The inverted 10Y-3mo yield curve is signaling the upcoming recession, and this has been historically a reliable leasing indicator of a recession – the link to the NY Fed includes the economic theory and the empirical evidence.

S&P500 is currently trading at a P/E ratio of 20.8, and PE20 ratio of 29.4, according to the data provided by Schiller. The forward P/E ratio is near 18. Thus, the S&P500 is not priced for a recession, and it’s trading at the historically high valuation.

Also, consider the fact that the “E” part of the P/E ratio is overestimated – the earnings are likely to decrease up to 20% in a recession, and this is not priced in. Thus, as the recession approaches, the earnings likely will have to get downgraded, and the valuation multiples likely will have to contract.

The P/E ratio is a proxy for growth – high P/E ratio can be justified when growth is expected to be above normal, and/or interest rates are expected to be very low. Note, even after the recession, it’s unlikely we will get a large fiscal stimulus, or even a large monetary stimulus, given the recent political changes and the post-pandemic inflationary dynamics. Further, due to de-globalization, growth is unlikely to be boosted by trade. Thus, even after the recession, growth is likely to be below the recent experience over the last 20 years, which does not support the high valuation multiple.

Implications

The bullish investors proposing the “October bottom” thesis are: 1) fighting the Fed, 2) ignoring the economic theory and empirical evidence with respect to recessions, 3) buying overvalued stocks, and 4) getting excited by the technical bounce.

The bearish investors expecting the bear market to continue must consider the power of trend followers and cut the bearish positions above the 4200 level. The Fed did lose credibility, and they do seem to be confused. Thus, the market is sniffing the Fed “weakness” and hoping to win against the Fed.

At this point, I am still bearish and recommending a sell on SPY.

SPY Sector performance YTD

The popular SPY ETF that tracks the performance of S&P500 is up by 4.16% YTD in 2023. The ETF started the year lower, but it bounced following the slowing growth in wages, which is consistent with the expectations of the falling inflation and dovish Fed in 2023.

The rise in SPY YTD has been led by the Communication Services and Consumer Discretionary sectors, up by 9% and 8% respectively. Within these sectors, there was a significant bounce in the heavily shorted airlines, casinos, cruise ships, and streaming services. All of these sectors perform poorly in a recession; thus, the bounce seems to be short covering.

The materials and real-estate sectors also bounced by 7%, which also makes little sense in an economy facing a recession. Note, the cross-current from China reopening could boost the materials over the near term, as well some travel related stocks.

|

S&P 500 Index |

+4.16% |

|

|

Communication Services XLC |

+9.09% |

|

|

Consumer Discretionary XLY |

+8.16% |

|

|

Consumer Staples XLP |

+0.25% |

|

|

Energy XLE |

+2.84% |

|

|

Financials XLF |

+5.61% |

|

|

Health Care XLV |

-0.29% |

|

|

Industrials XLI |

+4.33% |

|

|

Materials XLB |

+7.87% |

|

|

Real Estate XLRE |

+7.12% |

|

|

Technology XLK |

+4.86% |

|

|

Utilities XLU |

+1.18% |

Be the first to comment