Feverpitched

Thesis

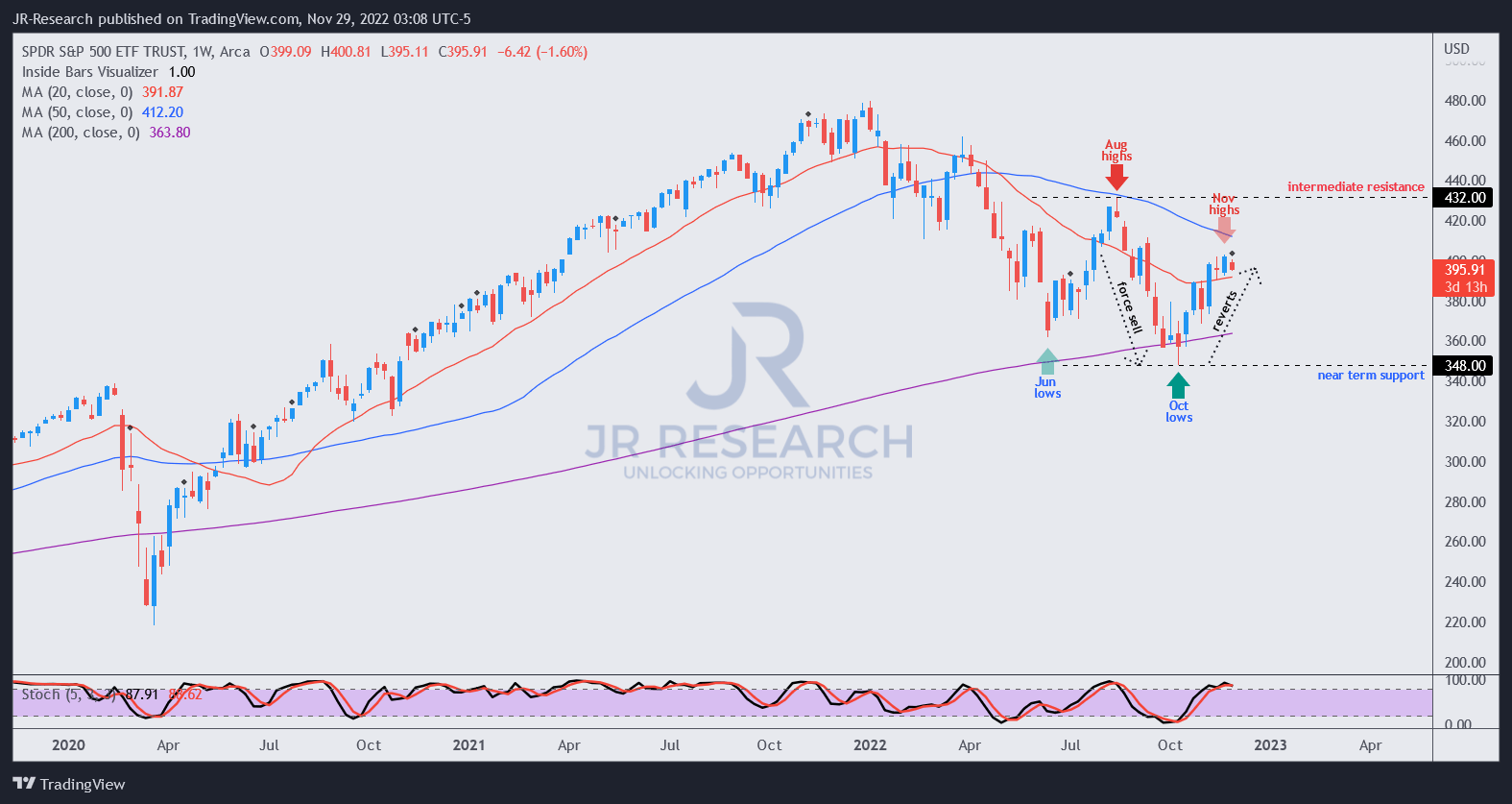

We updated investors in our previous update to ignore the market pessimism in October. We postulated that the market forced a steep selloff from the SPDR S&P 500 ETF’s (NYSEARCA:SPY) August highs, leading to a potent double-bottom bear trap predicated against June’s lows.

Accordingly, the SPY recovered nearly 16% from its October lows toward its November highs. As such, we believe it’s appropriate for investors to pause and assess whether the current levels still represent attractive reward/risk through a potential recession.

The recovery is also in line with the SPY’s 5Y and 10Y total return CAGR of 11% and 13.1%, respectively. Notwithstanding, its YTD return remains well in the red at -14.3%.

Fed Chair Jerome Powell is also due to speak on November 30 at a conference on “Economic Outlook, Inflation, and the Labor Market.” All eyes will therefore be on Powell as investors parse for clues in the Fed’s updated dot plot. In addition, investors expect a slower rate hike cadence in its upcoming December FOMC meeting, which we believe has already been reflected in the recent recovery.

Hence, investors’ focus has justifiably shifted to whether there’s a need to reprice the Fed’s median terminal rate higher than anticipated. Recent commentary from Fed speakers sounded more hawkish than preferred. Given the SPY’s near- to medium-term overbought levels, we believe caution is warranted.

Hence, we believe moving to the sidelines from here is appropriate, as we anticipate a healthy pullback before another attempt to re-test August highs.

Revising from Buy to Hold.

All Eyes On Powell Next

The recent release of the Fed’s minutes corroborated the market’s expectations of a slower pace in rate hikes moving forward. Therefore, the market has already priced in a 50 bps hike, with a probability of nearly 70% as of November 28 (down from 75% in the previous week).

Therefore, there wasn’t any noticeable uplift from the release, as SPY had already bottomed out in October. Hence, we postulate that the recent rally has already appropriately captured the less hawkish hiking cadence.

The Fed Fund rates (FFR) forward curve indicates a 5% terminal rate exiting H1’23 before falling below 4.4% exiting Q1’24. As such, the market will assess whether the updated dot plot could suggest a terminal rate higher/lower than what the market has priced in.

However, recent commentary from Fed speakers highlights that the Fed could remain in a hawkish stance for longer as it continues to combat stubbornly high inflation rates.

The Fed’s James Bullard also reiterated that the terminal rate needs to rise to at least 5% but could potentially be higher. Hence, Bullard cautioned investors that inflation remains the Fed’s number one priority, and the work is far from done.

Therefore, investors are urged not to rule out higher terminal rates than currently reflected, which could impact the economy in 2023. Edward Yardeni also cautioned in a recent briefing:

In our opinion, inflation is the one key variable that clearly will determine the economic and financial outcome in 2023. If it moderates without a hard landing of the economy, as we expect, then 2023 will be a better year all around than 2022. If it has peaked but remains persistently high, the Fed will have no choice but to continue tightening until a broad-based recession ensues. – Yardeni Research November 28 morning brief

SPY: At A Critical Juncture

SPY price chart (weekly) (TradingView)

The SPY bottomed out at its October lows, as we postulated in our previous article.

However, the momentum has reached a standstill recently at its November highs. We believe the market’s positioning is justified, with SPY’s NTM P/E around 17.4x, in line with its 10Y average of 17.7x. A further re-rating is unlikely for now as the market parses the possibility for a repricing or shifting of the FFR’s forward curve.

SPY’s August highs remain the critical impediment, which we believe remains its intermediate resistance level. Based on an implied NTM P/E of 18.7x, we think it’s within reach subsequently if the market doesn’t anticipate a severe recessionary scenario. We assess that analysts’ estimates on the S&P 500 have already been revised downward markedly to reflect a mild-to-moderate recession, likely reflected at SPY’s October lows.

Hence, we believe SPY’s October lows should hold robustly, but a pullback to de-risk the Fed’s positioning in the upcoming December FOMC is likely.

Revising from Buy to Hold for now, as we anticipate a pullback.

Be the first to comment