Win McNamee/Getty Images News

Definition of “Hustle” – to lure less skillful players into competing against oneself (Merriam Webster)

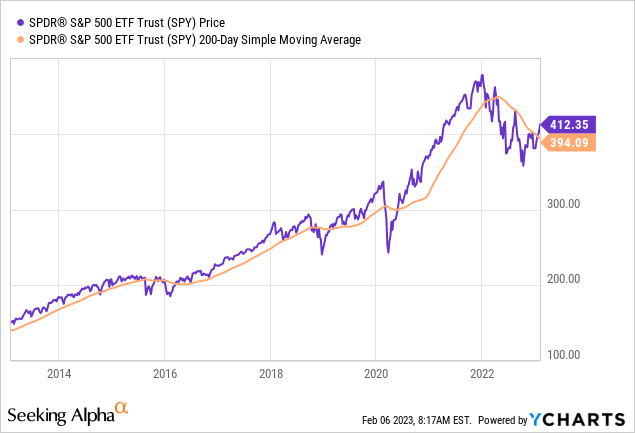

S&P 500 (NYSEARCA:SPY) has been in a bear market since January 2022. However, there were two sharp bear market rallies – the summer bear market rally, and the unfolding end-of-the-year bear market rally, which extended into the January of 2023. Both rallies were based on the expected “Fed pivot”, which still remains elusive.

The current January rally is especially deceiving since it broke the technical downtrend resistance at 200dma, luring many trend followers back into the market.

Let’s first understand the origin of the unfolding bear market:

The origin of the unfolding bear market can be traced to the Fed Chair Powell’s testimony to the US Congress on November 30th, 2021, where he acknowledged that the post-pandemic inflationary shock was not transitory, as previously expected. Powell specifically referenced “labor market” and “wage growth” as the key inflation drivers. This speech laid the groundwork for an aggressive monetary policy tightening.

Most forecasters, including at the Fed, continue to expect that inflation will move down significantly over the next year as supply and demand imbalances abate. It is difficult to predict the persistence and effects of supply constraints, but it now appears that factors pushing inflation upward will linger well into next year. In addition, with the rapid improvement in the labor market, slack is diminishing, and wages are rising at a brisk pace.

The first warning of the Fed-induced recession

The Fed eventually inverted the yield curve to restrict the financial conditions, which has historically led to the recessions and the recessionary bear markets. I fact, Powell warned that a recession might be necessary to cool off the tight labor market with the reference to “some pain” at his Jackson Hole speech in August of 2022.

While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.

The Powell speech at Jackson Hole ended the summer bear market rally in S&P500, right at the 200dma resistance.

The “soft landing” hope

Yet, the stock market continued to ignore the warnings and started to price the soft-landing thesis in October of 2022. Specifically, based on the signs that inflation has peaked, and the hope that inflation will quickly fall back to 2%, the market started to price the Fed to 1) slow the interest rate hikes, 2) the pause the hikes, and 3) cut interest rates in 2023.

However, the Fed clearly communicated that the expected slowdown in interest rate hikes is primarily to evaluate the effects of the prior interest rate hikes on the economy, which work with long lags.

The Fed was clear at the December meeting that the soft-landing expectations were unwarranted, which ended the S&P500 bear-market rally, again right at the 200dma resistance.

Minutes of the Federal Open Market Committee December 13–14, 2022

A number of participants emphasized that it would be important to clearly communicate that a slowing in the pace of rate increases was not an indication of any weakening of the Committee’s resolve to achieve its price-stability goal or a judgment that inflation was already on a persistent downward path. Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.

The change in Fed’s communication strategy

Yet, after a brief pause, the end-of-the year rally continued into January 2023, completely ignoring the Fed’s warning. Thus, the Fed changed its communication strategy, as the prior warnings were ineffective.

Specifically, Powell acknowledged that some market participants have their own forecasts, which are more optimistic than the Fed’s forecast. Yet, he did not challenge these alternative forecasts and acknowledged that “everything is possible”.

Here is the specific exchange with Robb from MarketWatch:

The Powell’s February 1st press conference Q&A session, after the FOMC meeting.

GREG ROBB. Thank you, Chair Powell. Greg Robb from MarketWatch. In the minutes of the December meeting, there was a couple of sentences that struck people as important when the Committee said participants talked about this unwarranted easing of financial conditions as a risk and it would make your life harder to bring inflation down. I haven’t seen — heard you talk much about that today or in the statement. So, I was wondering, has that concern eased among members or is that still something you’re concerned about? Thank you.

CHAIR POWELL. I would put it this way. It’s something that we monitor carefully. Financial conditions didn’t really change much from the December meeting to now. They mostly went sideways or up and down but came out in roughly the same place. It’s important that the markets do reflect the tightening that we’re putting in place. As we’ve discussed a couple of times here, there’s a difference in perspective by some market measures on how fast inflation will come down. We’re just going to have to see. I mean, I’m not going to try to persuade people to have a different forecast, but our forecast is that it will take some time and some patience and that we’ll need to keep rates higher for longer. But we’ll see.

Powell essentially invited the market participants to “place their bets” based on their forecasts and suggested to wait for the data to see who eventually turns out to be right.

The initial reaction to this statement was bullish, and the S&P500 broke the 200dma resistance, which for the technicians validated the “new bull market” thesis.

However, the bulls have been “burned” already two days later on Friday the 3rd, with the extremely strong labor report, after which the 2023 interest rate cut was essentially priced out. It didn’t take too long for the Fed to win.

Note, in gambling terms the Fed is the house – and the house always wins. Yet, gamblers continue to bet against the house, with the odds clearly against them.

Implications for SPY

The data is likely to support the Fed’s outlook. Thus, the higher-for-longer restrictive monetary policy will be required to cool off the labor market and the service inflation. The earnings for S&P 500 companies will have to contract significantly, especially if the recession is pushed into 2024 which will only prolong the pain and uncertainty. The forward PE ratio for SPY at nearly 19x is very high, and it will need to adjust lower toward 15x. Thus, there is a significant downside from here for SPY.

But the “casino” is open for investors to place their bets any way they want. I would just not bet against the Fed. Cliche.

SPY Sector analysis YTD

SPY is up 7.73% ytd, led by Communication Service (21%) and Consumer Discretionary (17%). This leadership is not sustainable in a market facing a recession. The traditionally defensive sectors are actual down ytd (Staples, Health Care, and Utilities), which could be the area for somebody who absolutely has to buy stocks now.

|

S&P 500 Index SPY |

+7.73% |

|

|

Communication Services XLC |

+21.28% |

|

|

Consumer Discretionary XLY |

+17.18% |

|

|

Consumer Staples XLP |

-1.54% |

|

|

Energy XLE |

-1.73% |

|

|

Financials XLF |

+6.99% |

|

|

Health Care XLV |

-2.33% |

|

|

Industrials XLI |

+4.72% |

|

|

Materials XLB |

+7.38% |

|

|

Real State XLRE |

+10.91% |

|

|

Technology XLK |

+13.93% |

|

|

Utilities XLU |

-3.67% |

Conclusion

The bear market in SPY is likely to continue as the “higher for longer” interest rate policy increases the chance of a deeper and longer recession, which could be pushed even to 2024, given the resilient labor market.

The current bear market really has been based on hopes for a soft-landing based on market narrative. However, the rally has been led by beaten down stocks in cyclical sectors such as discretionary and communication services, which possibly reflects retail-speculation and short-covering.

Given the surprisingly strong labor report for January, it remains to be seen whether the Fed increases the hawkishness or continues to “lure” the speculators into chasing the rally.

Be the first to comment