SusanneB

Summary

SPDR S&P 500 Trust ETF (NYSEARCA:SPY), which tracks the S&P 500 Index (SP500), has corrected considerably in 2022 from peak valuation on over earnings caused by pandemic demand and rate stimulus. However, while consensus valuation now seems reasonable at a 15.1x PE, there may be a risk to earnings as companies provide 2023 guidance. Faced with a potential recessionary environment, I think the C-suite, who look to manage expectations by under promising and over delivering, may provide “conservative” guidance. This could lead to a rash of analyst downgrades and selling pressure during the upcoming earnings season. Medium term, sector rotation away from tech mega caps may limit the SPY’s upside. The SP500 constituent weights may take time to adjust.

SPY Will Evolve

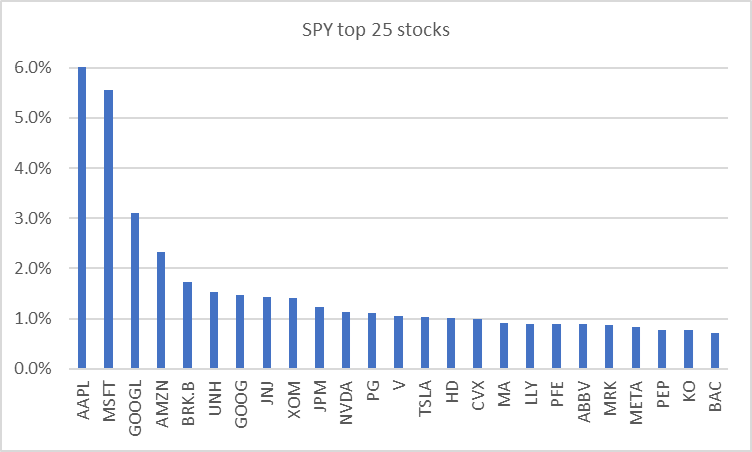

The SPY is the largest ETF in the market with US$360bn in assets. Founded in 1993 it has become synonymous with the SP500 and utilized by passive and active inventors. The ETF has evolved along with the SP500 and incorporated the large or mega cap tech stocks over the years as these gained value and importance, which displaced the other large and slower growing stocks. This tech dominance may be changing as they lose market cap relative to other constituents.

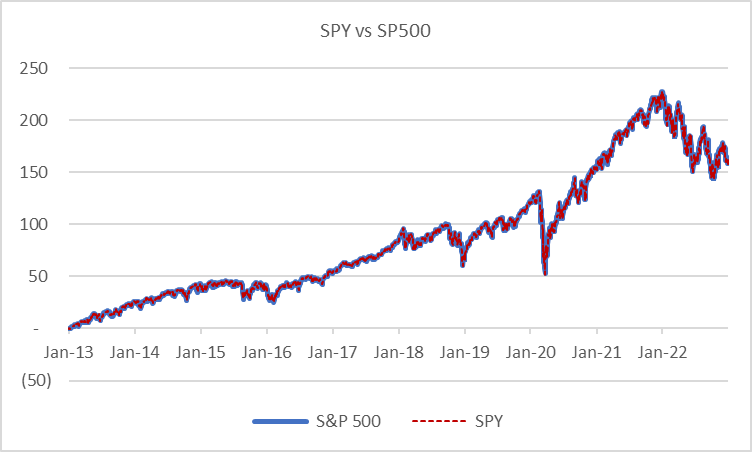

SPY and SP500 Performance (Created by author with data from Capital IQ) SPY Top 25 Stocks (Created by author with data from State Street)

SPY Bottom Up Analysis

SPY tracks the SP500 Index which attempts to diversify across sectors in more mature companies. However, the ETF still has over a 26% weight in tech related companies that may face demand risk as investor rotate to other sectors in a higher risk free/rate environment. At the same time many of the SPY constituents are slower growth and well valued companies that can weather a downturn but are arguably not great compounders.

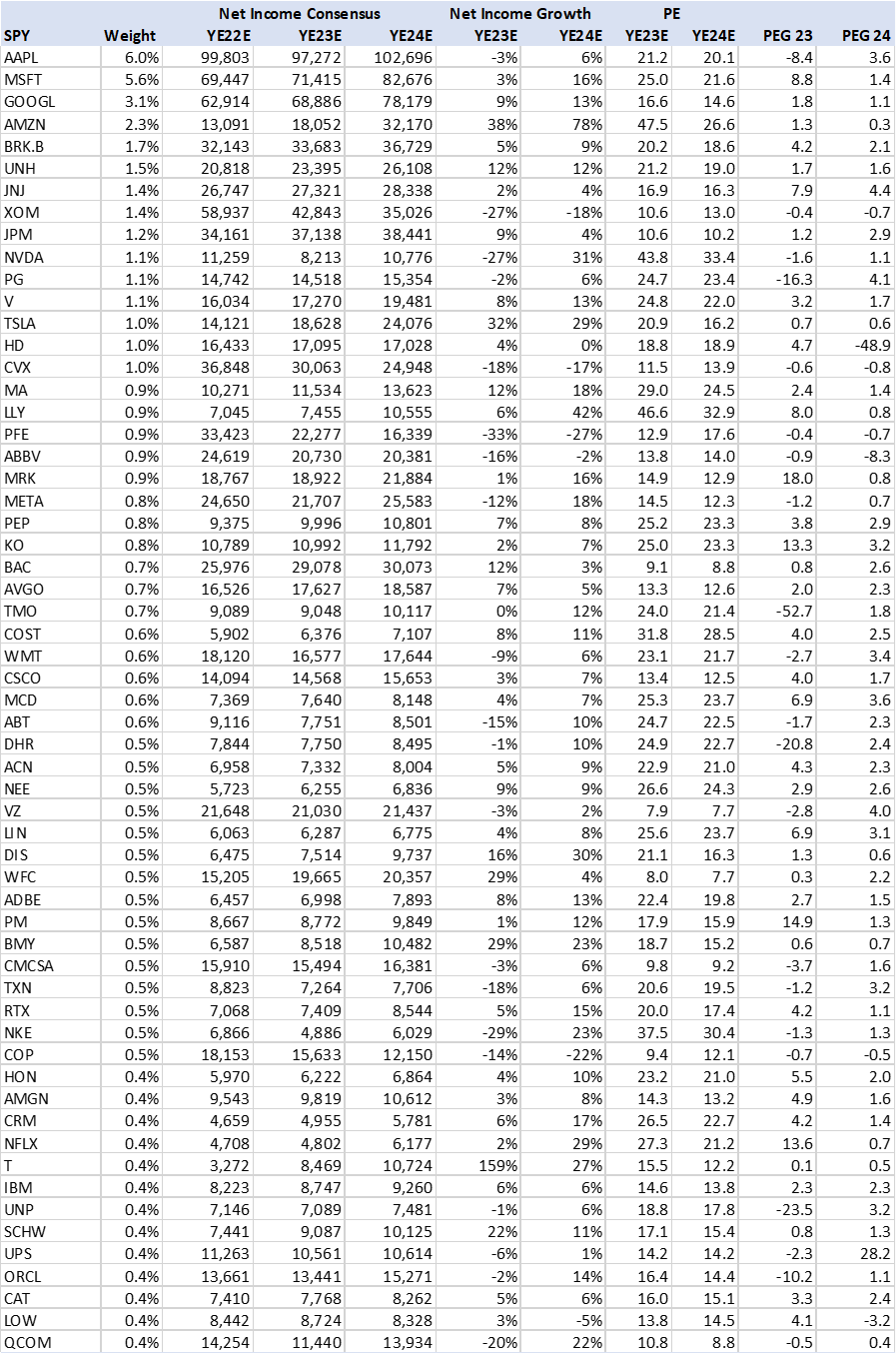

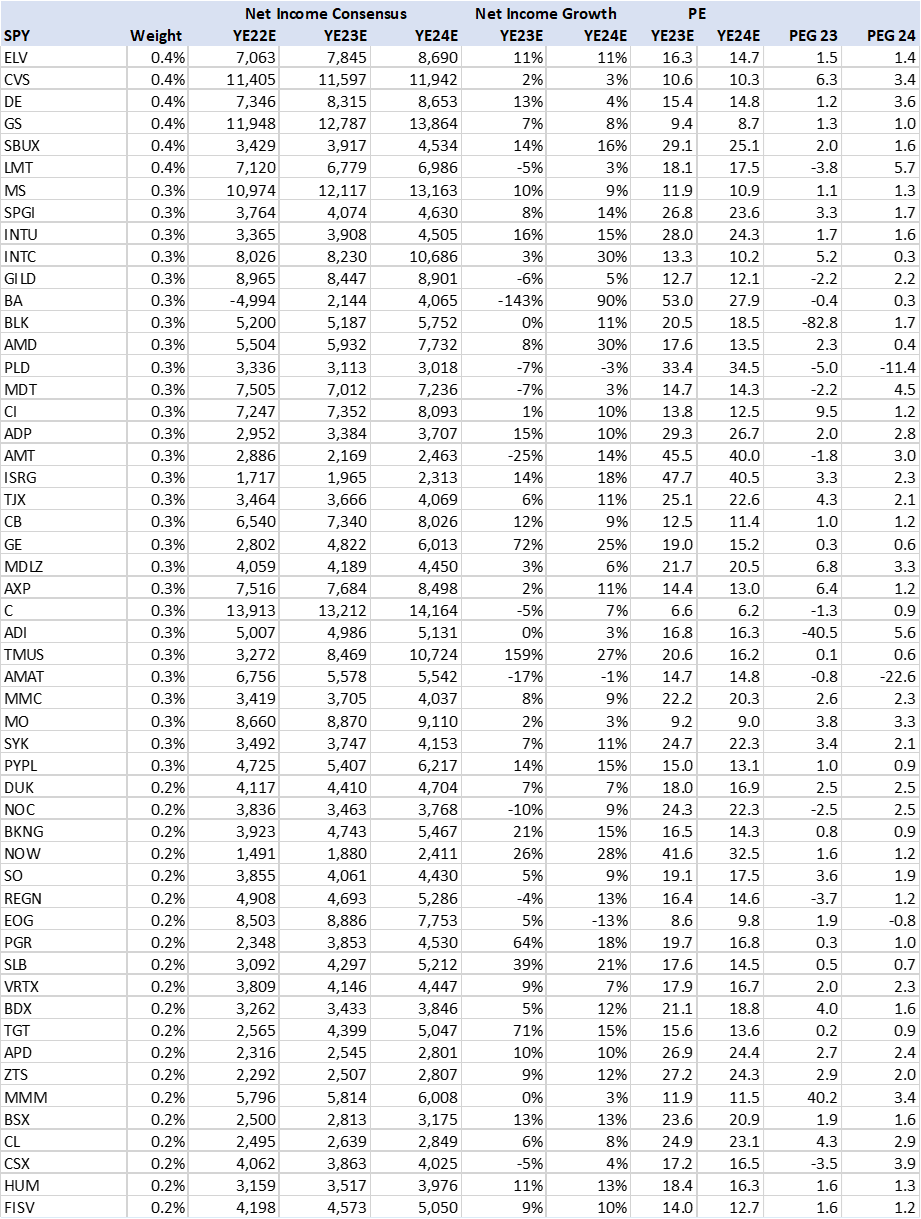

I conducted a bottom-up earnings review for 70% of SPY (114 stocks). As can be seen in the tables below, the market (sell side consensus) is forecasting 3% weighted earnings growth. This is a nominal growth rate, adjusting for inflation would cut this to 0% or -1%.

However, are these earnings realistic under an expected recessionary environment? During this earnings season it is likely that companies provide 2023 guidance, which could lead to downgrades and market selling pressure. Many companies likely attempt to manage expectations i.e., under promise and over deliver. Under an uncertain global macro scenario, it’s very possible managements hedge guidance.

As the market incorporates potentially lower earnings for 2023, the SPY could become more expensive or correct further.

SPY Valuation and Growth (Created by author with data from Capital IQ) SPY Consensus Valuation and Earnings (Created by author with data from Capital IQ) SPY Consensus Valuation and Earnings (Created by author with data from Capital IQ)

Consensus SP500

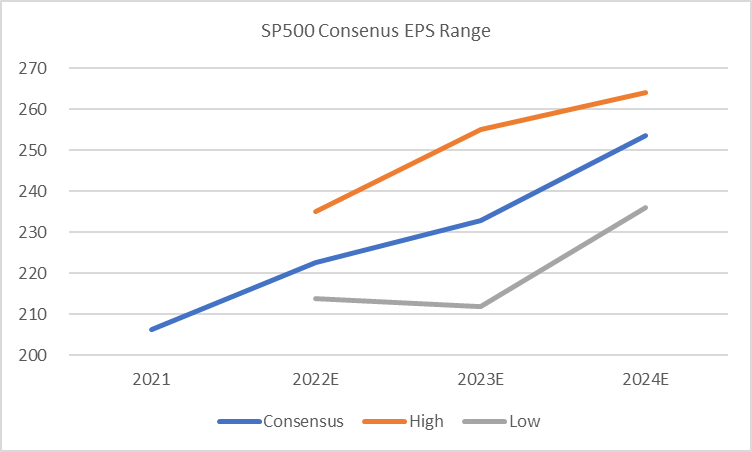

In the charts below are the EPS consensus estimates for the SP500 that have a surprisingly limited number of contributors (6) vs the data set from individual stocks that have 20 or more analysts. Despite the limitation one can see a wide dispersion from high and low end of range that suggest views and projections are not so consensus.

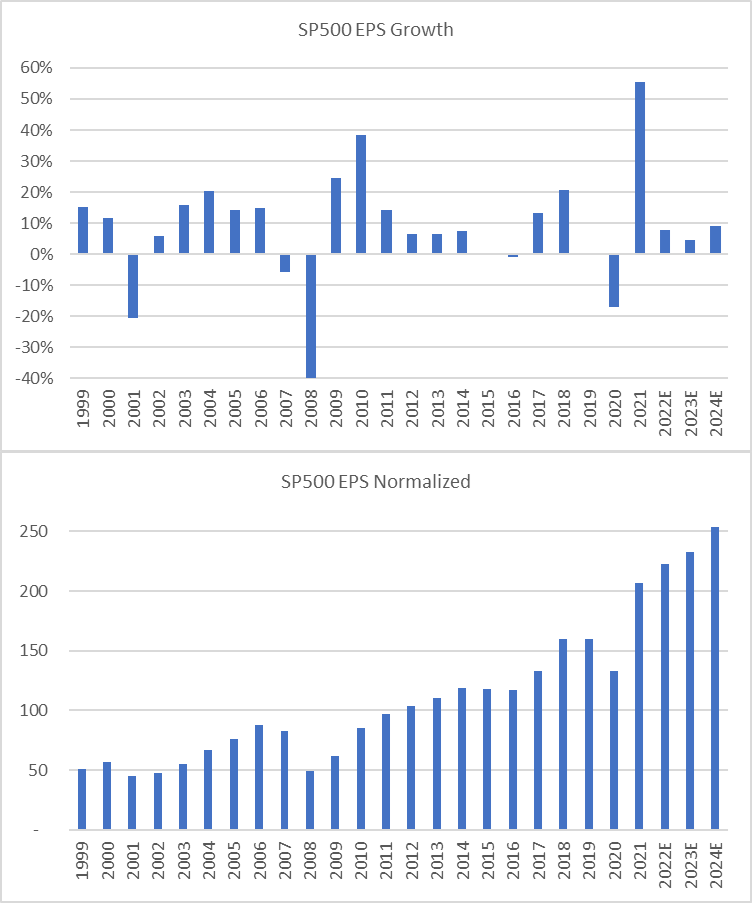

The second chart shows the EPS and growth rate since 1998 and clearly highlights the 2021 rebound plus, perhaps optimistic, 2023 expectations.

SP500 EPS Consensus (Created by author with data from Capital IQ) SP500 EPS and Growth (Created by author with data from Capital IQ)

What is fair market valuation?

This is a key and difficult concept to pin down. Valuation of any asset depends on a large variety of factors. In my view, the two most relevant factors for a broad-based market valuation analysis are earnings growth and the risk-free rate or US Treasury yields. Generally speaking, the higher earnings growth is, the more valuable the stock may be.

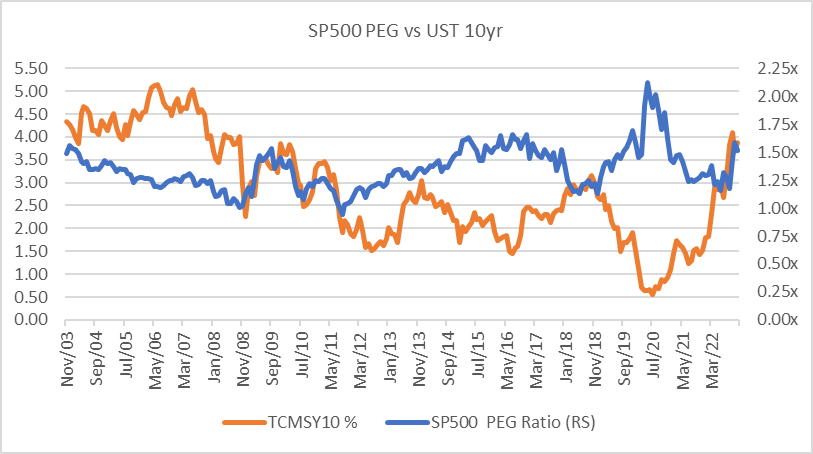

The PEG or PE/EPS Growth is a decent quick screen to gauge the value of a stock vs its growth. Value investors have used this for the last 50 plus years and a ratio of 1 is fair value, higher could be considered more expensive. The SP500 has traded at 1.4x average since 2003.

SP500 Valuation Relative to EPS Growth and UST Rate (Created by author with data from Capital IQ)

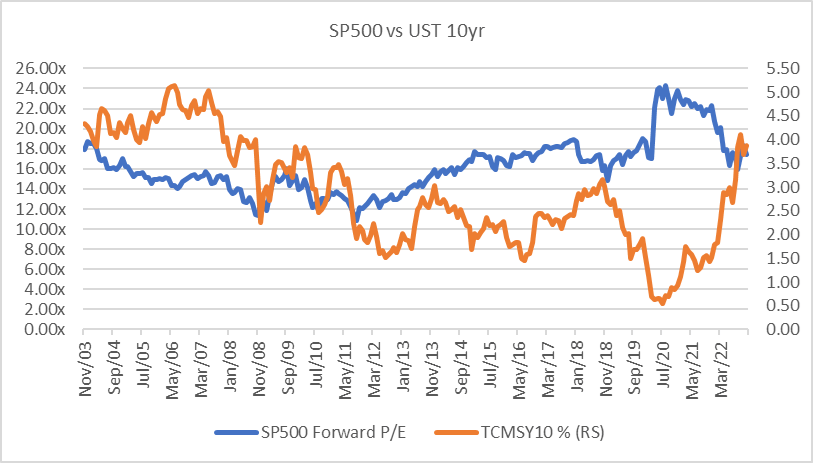

The second leg of valuation is to place it in context with the current risk-free rate as represented by a 10yr US Treasury. There are two rationals for this: One is fundamental, the higher the market rates the higher the discount rate on future earnings streams. The DCF (discounted cash flow) method relies heavily on the WACC (weighted average cost of capital) that has a risk-free rate as a core discount to future value i.e., net present value. It’s textbook finance and has its place in valuing predictable cash flow streams. However, predictability in real world dynamics, especially over a 10 year or more time frame, is rare. This make the DCF valuation method, in my view, not so reliable.

In my view, higher rates have a real word impact on assets, such as stocks, via capital flows. The higher the risk-free rate (US Treasury, CDs etc.) the lower the appetite for risk. Less capital is available to buy stocks and with lower demand comes lower prices.

That said if we look at the current SPY valuation of 15.1x PE it appears to be a bit higher than the last 20yr low of 14.5x but the PEG ratio is substantially higher on recession fears impacting earnings in 2023. On 2024 data the SPY looks more appealing on PE and PEG ratio comps. My conclusion is that there may be further downside risk if 2023 earnings come under pressure.

I believe it is unlikely the Fed begins to cut rates in 2023 as long as PCE inflation is above 2% and unemployment below 4%. A 5% fed fund rate is healthy, it promotes long term savings and reduced reckless or speculative investment.

SP500 PEG relative to UST Rate (Created by author with data from capital IQ) SP500 PE relative to UST Rate (Created by author with data from Capital IQ)

Conclusion

The SPY, despite the 2022 correction and reasonable valuation, has further short-term downside risk in my opinion, as corporations update 2023 earnings guidance that could lead to further downgrades and selling pressure.

Be the first to comment