Torsten Asmus

The December CPI report

The U.S. Bureau of Labor Statistics will release the CPI Inflation report for December on Thursday. The consensus expectations are that the headline inflation will drop to 6.5% from 7.1%, and the core inflation will drop to 5.7% from 6%.

Trading Economics

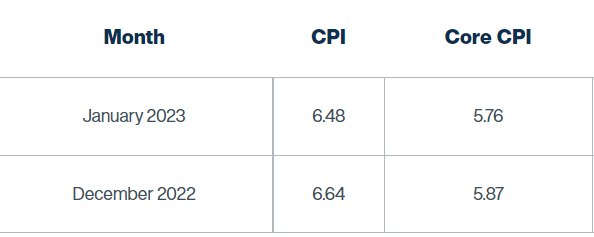

The Cleveland Fed Inflation Nowcast expects that the headline CPI inflation will be above the consensus at 6.64% and the core CPI inflation also above the consensus at 5.87%.

Cleveland Fed

The expected market reaction

The CPI Report has been the major market mover, and generally when the CPI comes below the consensus expectations the stock market rallies, and when the CPI comes above the consensus expectations the stock market falls sharply.

Based on Inflation Nowcast, the CPI will come above the consensus expectations, which will likely result in a sharp selloff in the stock market.

With that said, while the Inflation Nowcast has been fairly accurate in predicting the CPI in 2022, it was wrong for the October and November 2022 CPI data releases, when it predicted a much higher inflation reading.

This is what I noted before the November CPI report:

However, the Cleveland Fed Inflation Nowcast is predicting that the November CPI numbers will be higher than expected, with the CPI at 7.49% (7.3% consensus) and core CPI at 6.26% (6.1% consensus). Note, the InflationNowcast failed to predict the softer than expected October CPI readings, although it has been very reliable in 2022.

Note, after the release of the November CPI report and the huge miss, the Cleveland Fed Inflation Nowcast webpage did not provide an updated inflation forecast for a few days. Obviously, their model needed updating.

The question is whether the Inflation Nowcast will be wrong for the third consecutive time. Given that the Cleveland Fed likely updated their model, it is more likely that the Inflation Nowcast will be correct this time, and the CPI will come above the consensus. Thus, the stock market is likely to sell off in my view.

With that said, over the short term, the trading strategy based on predicting the monthly CPI data is a fool’s game. It is impossible to predict the monthly CPI data as a single observation.

However, over the medium term, the CPI inflation is likely to remain well above the Fed’s 2% target. Thus, fundamentally, it’s irrelevant if the Thursday’s data comes below the expectations. Yes, the CPI inflation has peaked, and it’s falling. But, given the structural issues with the labor market imbalance, it is unlikely that inflation will fall to 2% – without a deep recession. And this is a base for the bearish outlook for the stock market.

The big picture

The Fed Chair Powell has been clear in his speech at the Brookings Institute on November 30th explaining that the major inflationary problem now is the jobs-worker gap. Simply put it, there is a serious shortage of workers, which is likely to keep the wage growth elevated and thus, the service inflation elevated.

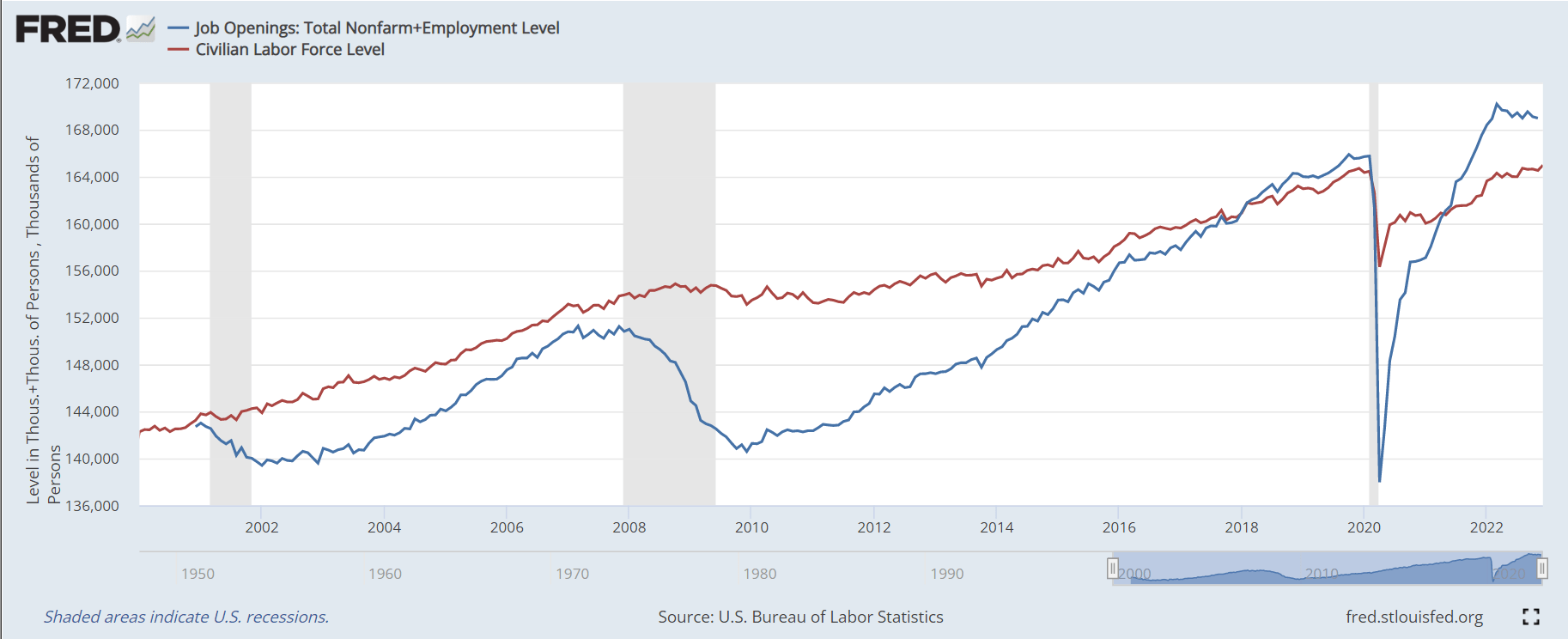

The jobs-worker gap is measured as the sum of the employed workers and the current job openings, compared to the labor force, as I illustrate in the graph below. Currently, there is about 5 million in the labor force deficit – this is inflationary.

FRED

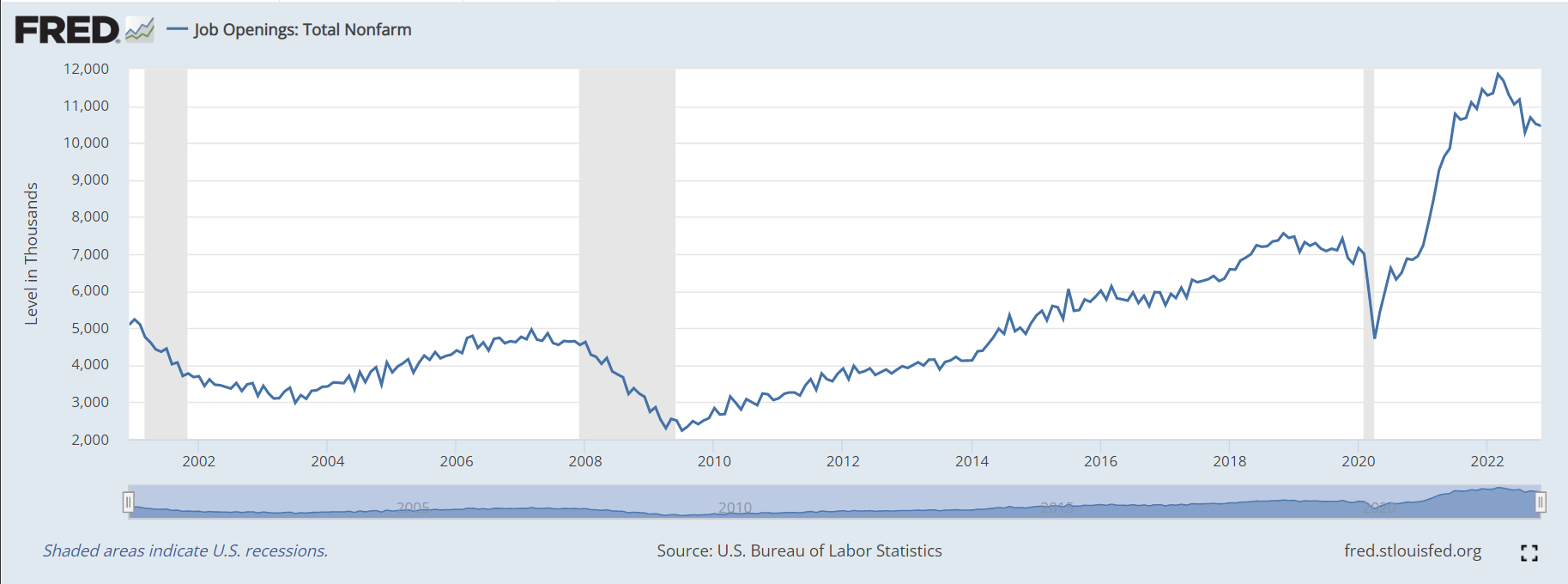

The key post-pandemic issue with the labor market imbalance is the sharp increase in job openings, which is currently above 10 million, as I show in the chart below.

FRED

The Fed has a clear target to increase the unemployment rate from the current 3.5% to 4.6%, as updated in the December projections. But this will reduce the jobs deficit by 1.5-2 million.

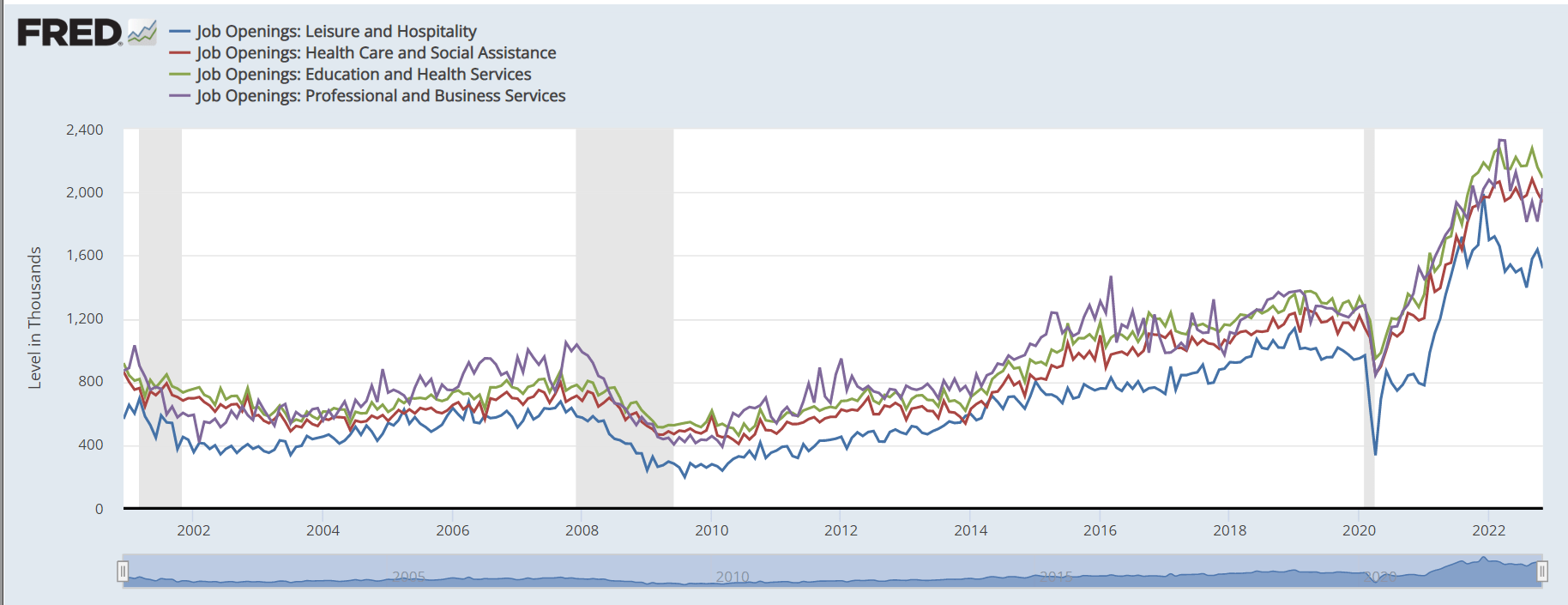

The hope is that the job openings would significantly decrease to solve the labor market imbalance, without causing more widespread job losses. However, a closer inspection of job openings reveals that there are around 2 million job openings in health service, 2 million job openings in education, and 2 million in business and professional services. These job openings have not decreased recently and are unlikely to decrease.

Basically, the US economy has a shortage of nurses and teachers, and this is unlikely to be solved with the increase in productivity, robotics, or even a recession. Thus, the Fed will be forced to push the unemployment rate probably much higher than 4.6% to solve the job-market imbalance.

FRED

The constrained resources

The Fed is probably not even concerned about the monthly CPI number, the Fed is concerned about the inflationary environment. It’s absurd to expect the inflation to drop to 2% as long as the production capacity is severely constrained, in my opinion.

As previously explained, the (service) production is currently severely constrained with the labor shortage. The Fed is aware that the service inflation can only return to a stable 2% target when the labor shortage is eliminated – either by increasing the labor supply (unlikely to happen) or by reduction in the demand for labor (recession).

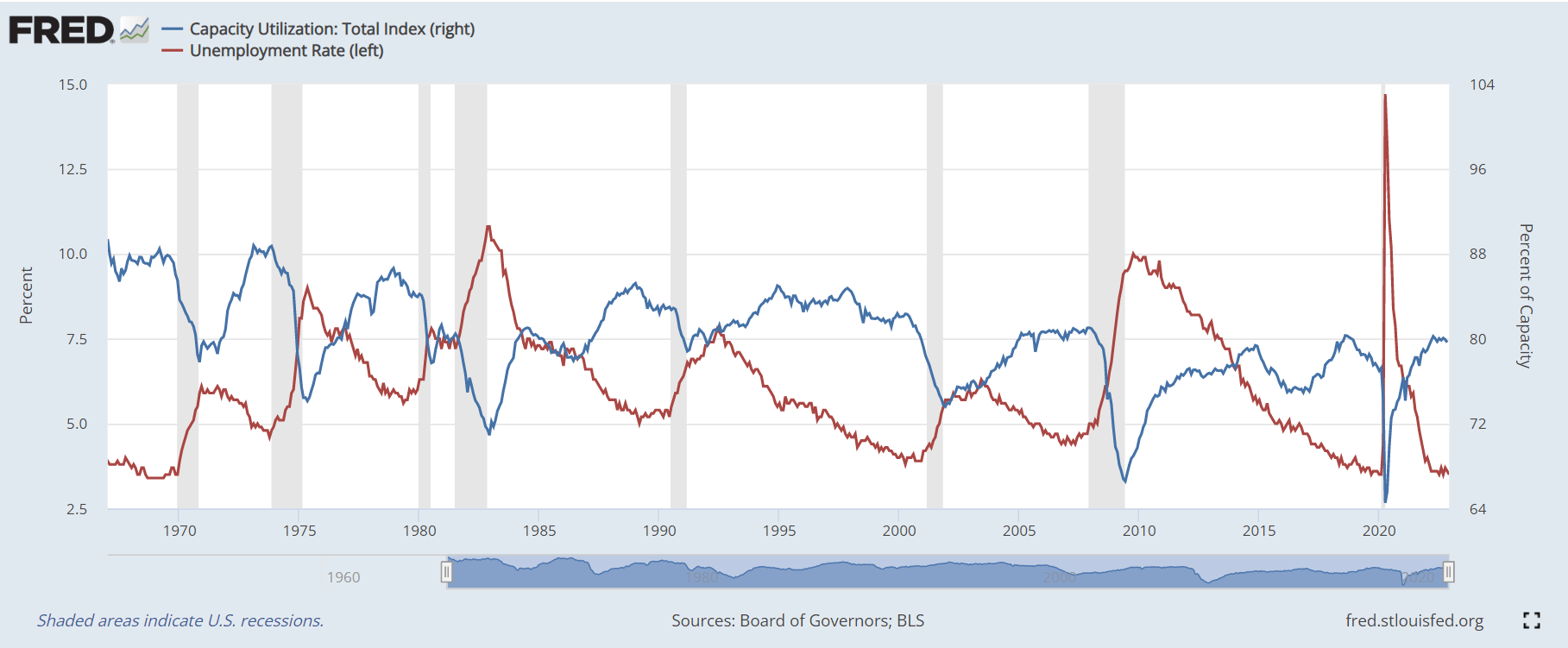

During the 1970-80s, the factory capacity utilization was the major inflationary variable. When the factory capacity reached the 90%-95% level (the current level is 90%), the Fed was forced to cool off the economy.

The graph below shows the inverse relationship between the factory capacity utilization and the unemployment rate. Before recession, the capacity utilization is very high (90-95%) and the unemployment rate is very low – these are the inflationary-constrained resources. During a recession, the factory capacity utilization drops, and the unemployment rate increases – until the new cycle starts.

FRED

We are currently at the point where the resource capacity is very limited, the factory capacity utilization is very high, while the unemployment rate is very low. The new cycle cannot start in this environment, and I think it’s absurd to believe that inflation would just fall in this environment. A recession is required to restore the price stability.

Implications

The more bullish stock market investors are hoping that inflation would just fall to the 2% target – without the need to endure a deep recession. This is absurd.

The PE ratio for the S&P 500 (SPX) (SPY) is over 20, which is overvalued and does not price the imminent recession. Whether the CPI comes above the consensus or below the consensus is fundamentally irrelevant. The price stability cannot be restored without a deep recession, which implies the continuation of the bear market in stocks – until the market prices the necessary economic damage.

Be the first to comment