SDI Productions

Preferred stocks often don’t get a lot of love from the investment community, but they are an interesting income generator. I feel we should get into what preferreds are. Preferred stocks are equity securities that, unlike common stocks, have a hybrid of stock and bond characteristics. Preferred stocks have a level of priority that common stockholders on the capital structure don’t. For example, if a company pays a dividend, holders of preferred stocks might receive that dividend first, and the amount might be fixed (rather than variable) and higher than the dividend paid to common stockholders.

Preferred stocks also have priority to a company’s assets first in the event of liquidation, after the claims of creditors such as bondholders (but before common stockholders). In addition, such stocks might grant a right to vote, but this is typically limited or non-existent. The higher dividend and more stable price feature of preferred stocks often appeal to income-oriented investors who seek a hybrid combination of higher, more dependable yield similar to that of bonds, as well as the participation in corporate ownership that stockholders might seek.

Cool? Now, of course, you don’t have to pick preferreds one by one. You can consider any number of ETFs that invest in preferreds with their own unique approach. One fund that has a different take on creating a preferreds-filled portfolio is the Global X SuperIncome™ Preferred ETF (NYSEARCA:SPFF). This fund does one thing and one thing only – it invests in 50 of the highest-yielding preferreds in the US. Simple.

A Look At The Holdings

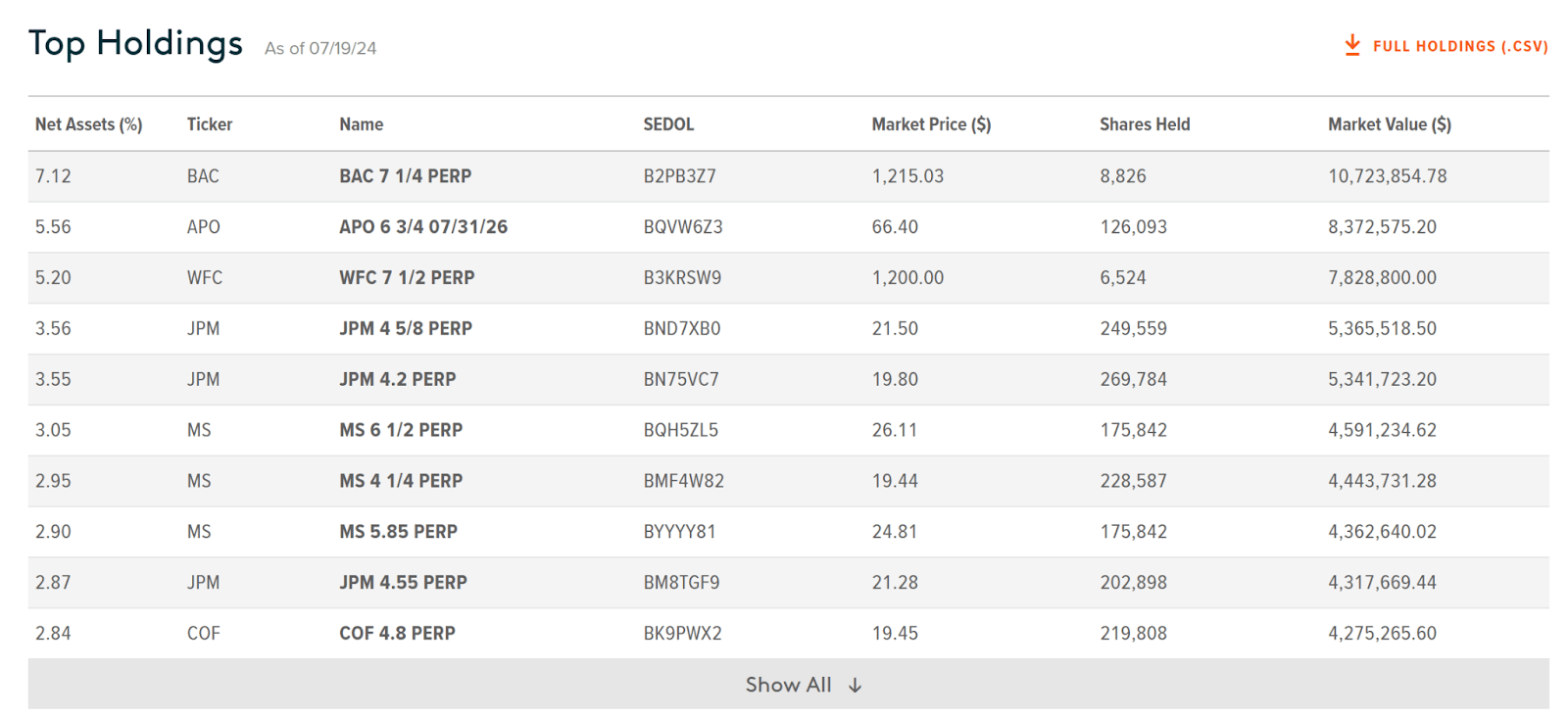

When we look at the top 10 positions, we find some high concentration here, with the largest position making up 7.12% of the fund. That preferred comes from Bank of America Corporation (BAC).

globalxetfs.com

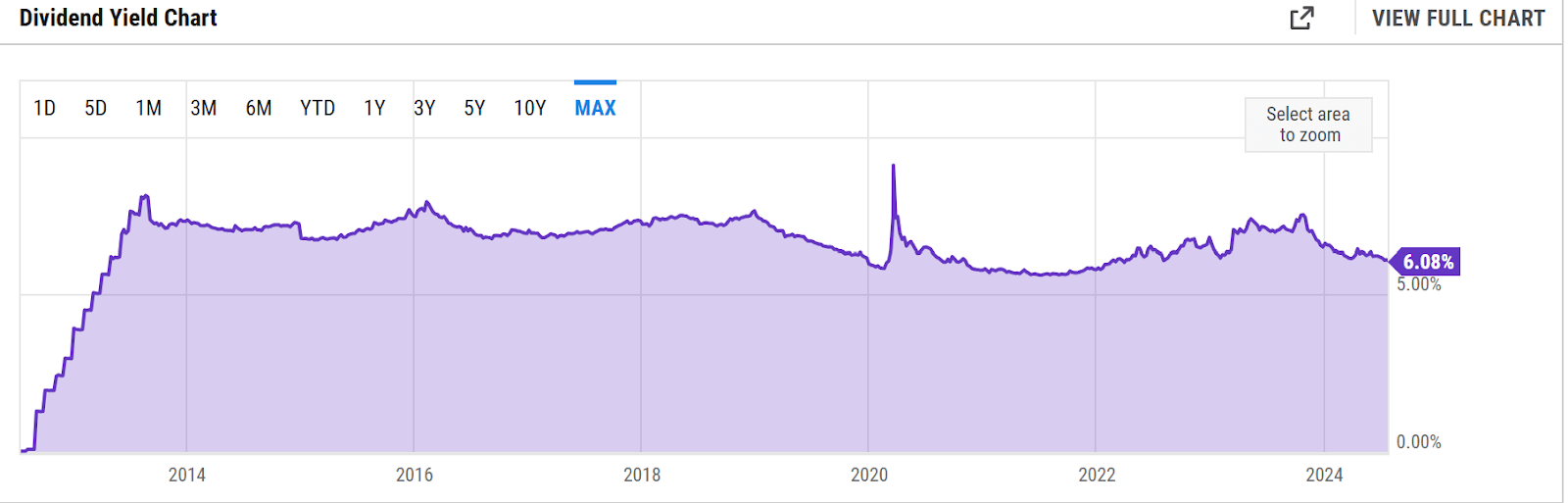

What kind of yield history do these companies provide? A pretty high and consistent dividend yield, presently at 6.08%.

YCharts.com

Sector Composition and Weightings

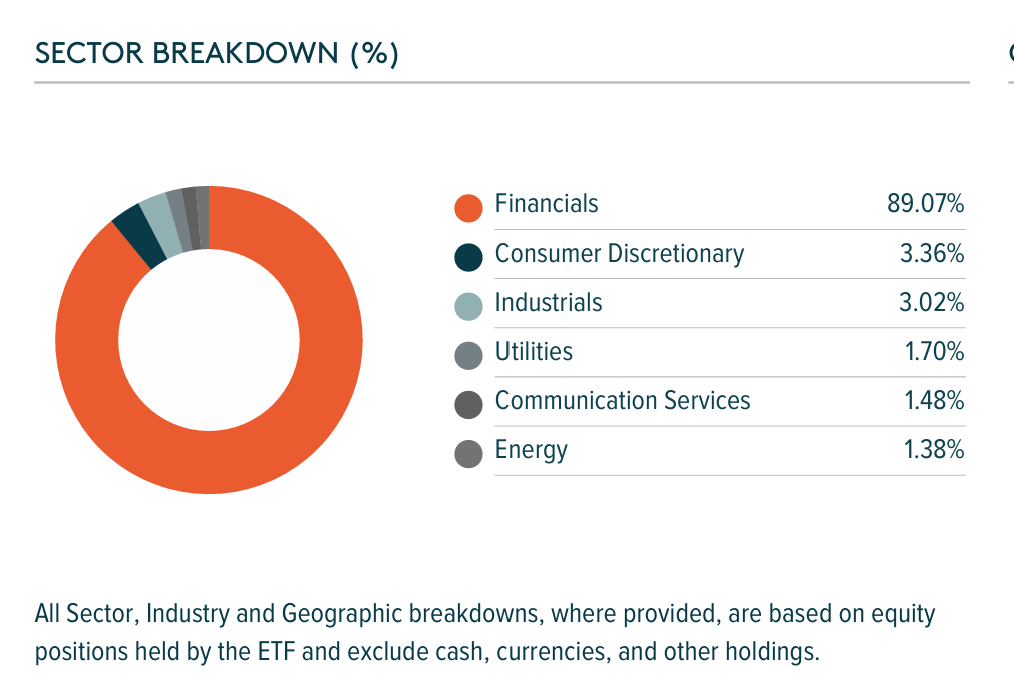

You may have noticed the top 10 names seem to be skewed by the banking sectors. That’s because preferreds, as a universe in general, tend to skew towards financials. Roughly 90% of the fund is in bank preferreds, with the rest split among Consumer Discretionary, Industrials, Utilities, Communication Services, and Energy.

globalxetfs.com

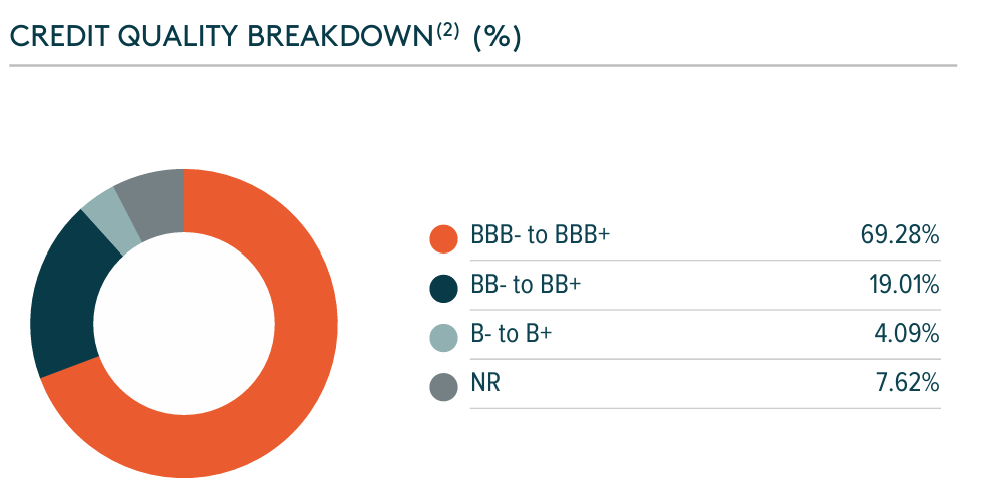

What matters is the credit quality of the preferred issuer, of course. Nearly 70% of the fund from a credit rating perspective is ratted BBB- to BBB+. A good sign. The remainder is clearly lower rates (with 7.62% not rated at all). Remember – preferreds have seniority over common stock, but not bondholders. So there is credit risk to consider here that is conceptually different from credit rates on bonds.

globalxetfs.com

Peer Comparison

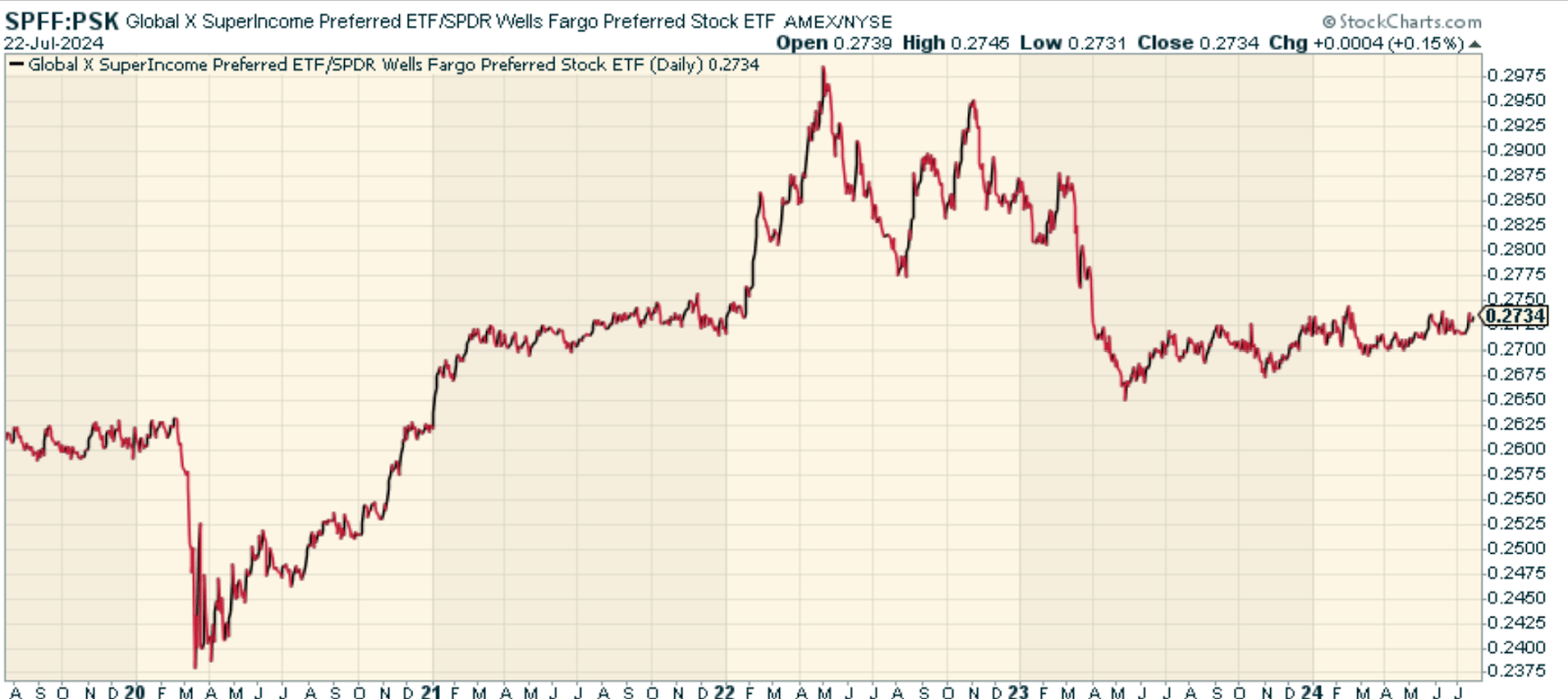

One fund worth comparing this against is the SPDR® ICE Preferred Securities ETF (PSK). PSK tracks an index of preferred securities across various sectors. When we look at the price ratio of SPFF to PSK, we find that SPFF has outperformed overall, and seems to be trending higher. The high yield, it would appear, is resulting in better relative momentum.

StockCharts.com

Pros and Cons

On the plus side, of course, is the income here. Investors searching for high yield can get in SPFF the highest-yielding preferred stocks in the United States. In addition, there is potential for preferential tax treatment. Income from preferred stock can be received as qualified dividends, which can provide investors with a more favorable tax treatment than regular interest income.

The biggest downside is the concentration risk in Financials. Again – not unusual, but this is one of the risks when it comes to considering preferred stocks in a portfolio. In addition, should credit risk matter for investors again and the economy hit a recession, preferreds likely would struggle purely because investors would question the likelihood of those preferreds not having a major claim on assets in a bankruptcy proceeding. And remember that preferreds will never typically come close to the upside potential of common stocks, as they trade for a set yield (unless dividend cuts are involved). You’re essentially giving up some capital appreciation potential in exchange for the steady stream of monthly income.

Conclusion

For yield-seeking investors and those who can handle the sector concentration risk within their portfolio, SPFF might be worth considering. For me personally? I think if I’m looking for high yield, I might just go into high-yield junk debt, or some of these option-writing overlay ETFs out there. Not a bad fund from what I can tell, so long as we don’t go through another financial crisis, of course.

Be the first to comment