Darren415

I last wrote about the SPDR Portfolio S&P 500 High Dividend ETF (NYSEARCA:SPYD) back in July 2021, arguing that while the ETF was set to outperform the SPX, the high degree of volatility meant that the returns were not worth the risk. Since then, valuations have fallen significantly, but so has the opportunity cost in terms of the risk-free rate. While the SPYD will outperform US Treasuries over the long term, the equity risk premium is at record lows. Investors in the SPYD are accepting a very low premium over USTs to compensate for the higher risk in terms of downside volatility and I therefore prefer USTs over the coming months.

The SPYD ETF

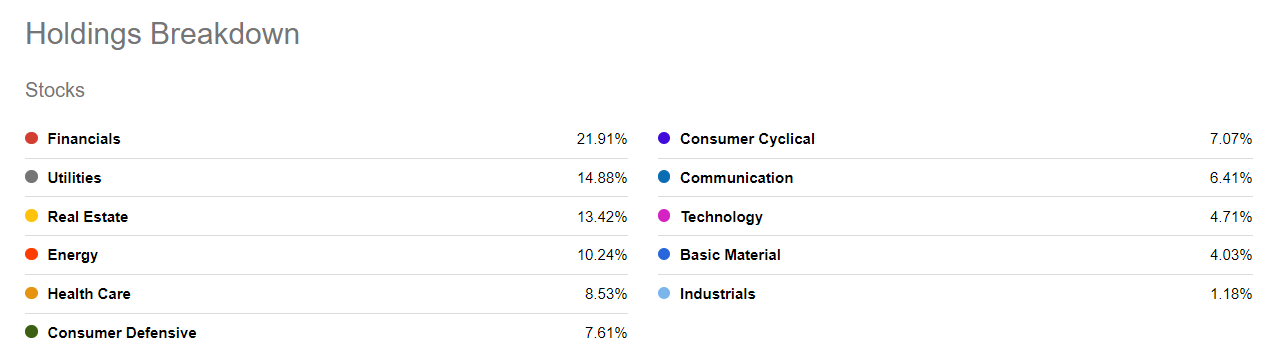

The SPYD ranks all dividend payers in the S&P 500 by indicated yield (the most recent dividend, multiplied by dividend frequency, divided by share price) and selects the top 80. SPYD does not include any of the dividend sustainability or quality screens that are baked into some peer ETFs. SPYD equally weights its portfolio while some similar, income-focused funds weight by yield. As a result, the ETF has a much higher weighting of financials, real estate, and energy relative to the S&P 500. Technology, meanwhile, represents less than 5% of the index, as one would expect given the low dividend payments in the sector. The ETF has a minimal expense ratio of 0.07% and a distribution yield of 4.7%. However, this yield will almost certainly fall, absent a decline in equity prices, as the forward dividend yield on the underlying S&P 500 high dividend yield index is just 4.0%.

Seekingalpha.com

Real Return Outlook Is Respectable…

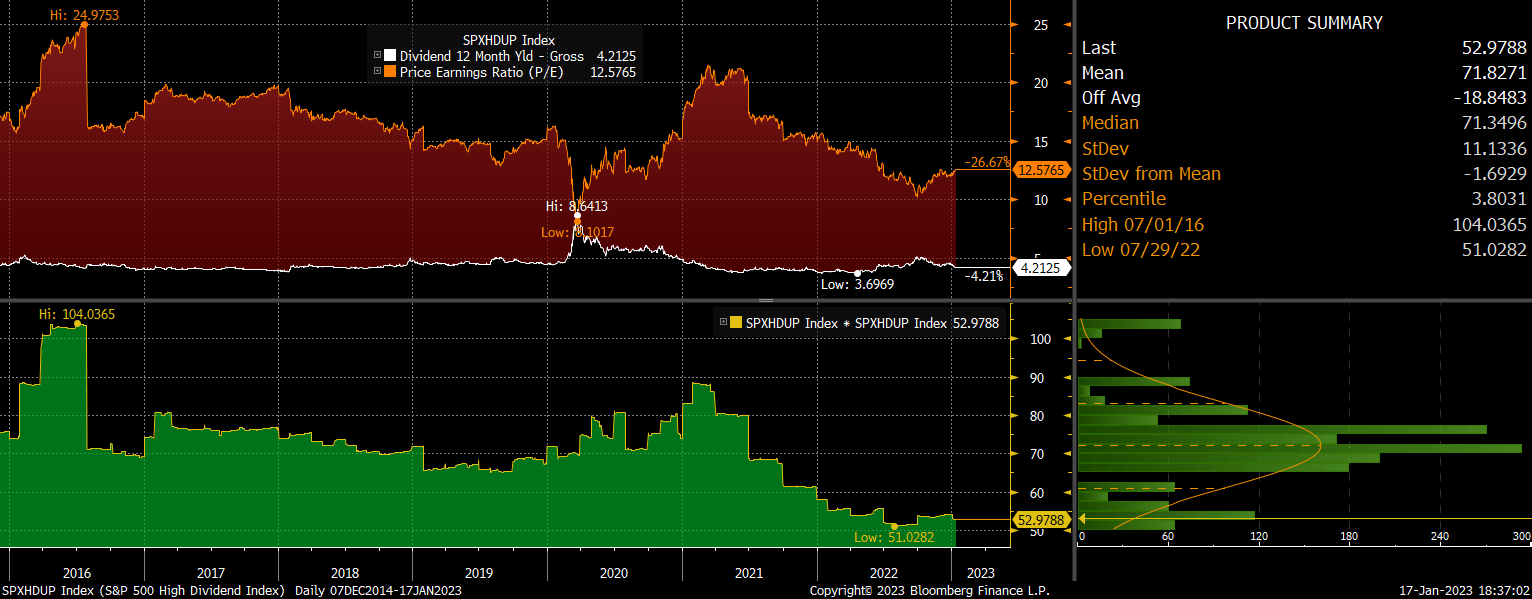

The S&P 500 high dividend yield index has risen to 4.2% from 3.9% in mid-2021, thanks to rising dividend payments. This rise in dividend payments has actually underperformed other fundamentals such as sales and earnings. As a result, the dividend payout ratio sits just above 50%, which is the lowest it has been in the data available which is from 2016. Notably, this low payout ratio does not reflect outsized profit margins, as the rise in profits has come from a rise in sales over the past 18 months.

SPYD PE, DY, and Dividend Payout Ratio (Bloomberg)

This has led to a sizeable rise in long-term expected returns. The SPX has returned roughly 8% in real terms per year over the long term when valuations have been at the level of the S&P 500 high dividend yield index currently. It could be argued then that these are the returns one should expect on the SPYD. However, these strong historical returns partly reflect strong growth seen over this period, where real GDP averaged over 3%. The real GDP growth outlook now sits at less than 1% based on trend rates of productivity and labor force growth. As high dividend paying stocks tend to grow more slowly as they are often mature companies, dividend growth is likely to be even lower than this for the SPYD. Furthermore, the long-term SPX returns have been supported by rising valuations, which has added another 1% to annual returns. Taking these factors into account, real returns look likely to be around 4% over the long term.

But The Equity Risk Premium Is Too Low

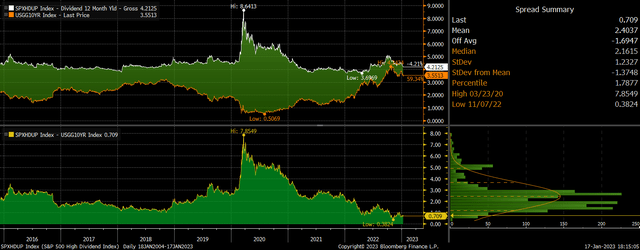

Compared with the real return outlook for the SPX, which I estimate to be around zero, this is reasonably strong, but in the context of current elevated bond yields it is extremely low. The chart below shows the dividend yield on the S&P 500 high dividend yield index versus the 10-year US Treasury bond yield. The current spread of 0.6% is the lowest on record and compares to an average of 1.9% since 2016.

SPYD Dividend Yield Vs UST Yield (Bloomberg)

It is the same story when we compare the dividend yield to 10-year inflation-linked bond yields, which show long-term returns after inflation. As stocks are real assets, they should be expected to rise with the rising price level over time, and so any comparison with bonds is better to be made with inflation-linked bonds rather than regular Treasuries. The current spread of 2.9% can be thought of as the return of excess return on the SPYD over the next decade assuming no change in valuations and assuming that dividends grow at the rate of inflation. While 2.9% per year may seem like adequate compensation for the added risk of investing in stocks, it compares with a 7-year average of 4.4% and a high of 8.7% seen at the height of the Covid crash.

SPYD Dividend Yield Vs US Inflation-Linked Bond Yield (Bloomberg)

A Track Record Of Underperformance In Bear Markets

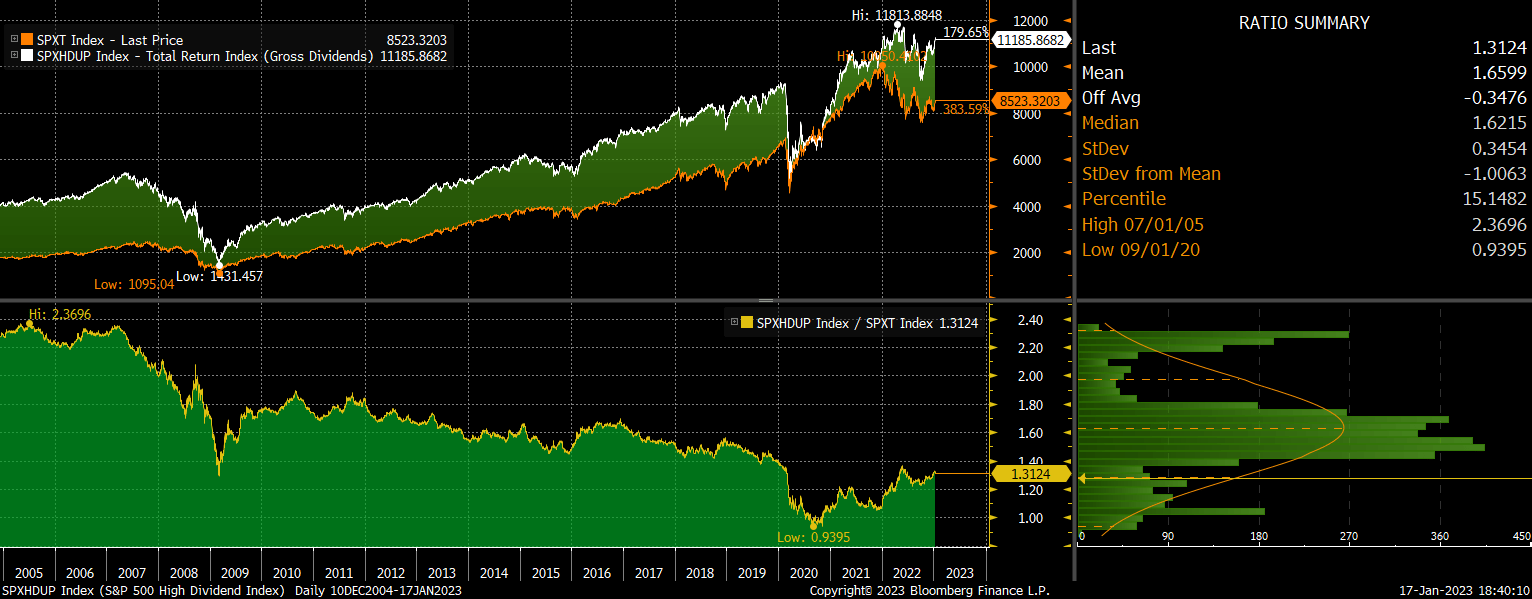

This 2.9% equity risk premium is not so attractive when we consider the performance of the SPYD during bear markets. In the Covid crash the ETF lost 47% of its value, and losses during the global financial crisis were a staggering 73%. The high weighting of financial and real estate stocks, which have a 35% weighting, makes the ETF highly susceptible to economic weakness and credit stress. As we saw during the last two major downturns, US Treasury bonds actually performed well as expectations of lower interest rates saw yields plummet. I see a growing likelihood of another rotation into bonds and away from stocks as the economic growth outlook continues to deteriorate.

SPYD Vs SPX (Bloomberg)

Summary

The outlook for the SPYD has improved over the past 18 months, and real long-term return expectations now sit at around 4%. While this is attractive relative to the SPX and is higher than the returns expected on US Treasuries, bonds represent a better risk-reward trade in the current climate due to the risk of sharp losses in the SPYD in the event of a recession.

Be the first to comment