naphtalina/iStock via Getty Images

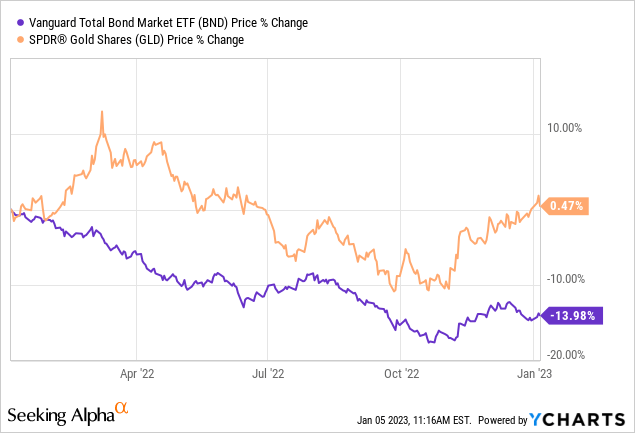

With traditional hedging tools like bonds and gold having suffered in 2022, it is important to think differently. For this purpose, since November, the Vanguard Total Bond Market ETF (BND) and the SPDR Gold Shares Trust (GLD) both have started showing signs of recovery, but the most recent jobs report points to higher wage inflation, signifying that the Fed will have to continue to tighten monetary policy. However, there are dissenting voices even within the Fed itself that point to inflation being under control.

In these circumstances, instead of predicting the future and buying bonds or gold, this thesis will focus on another strategy that worked well in 2022. This was to short the broader market, namely through the Direxion Daily S&P 500 Bear 1x Shares ETF (NYSEARCA:SPDN), which delivered gains of nearly 18%. More specifically, I will assess whether it still makes sense to short the S&P 500, as well as elaborate on how this exchange-traded fund (“ETF”) can be used to hedge an existing portfolio consisting of bonds and gold.

I start by painting a picture of current market conditions.

Market conditions in 2023

First, after a difficult year for most asset classes, investors have been eagerly seeking guidance as to what 2023 has in reserve for them. To be realistic, it is extremely difficult to predict the market in current circumstances when the Federal Reserve remains adamant in its fight against inflation on the one hand and the increased probability of a recession hitting the U.S. on the other.

Second, even if you do not have much trust in the U.S. central bank after its inaccurate “transitory inflation” narrative in the first half of 2022, you will agree that the unprecedented pace at which it hiked interest rates may have had some effect on inflation, albeit at the expense of economic growth.

In fact, there has been a noticeable economic slowdown, which has somewhat slowed down the runaway inflation and put an end to the upward spiral in prices as the demand outlook has become more uncertain. Thus, inflation fell from 9% in June to 7% this November, but, according to Fed’s Chairman, it will take much more evidence for inflation to be considered as easing.

In its forecasts, the U.S. central bank envisages rates at 5.1% this year, compared to 4.6% in its September forecast, and is aiming for a long-term trend of 2.5%. However, in no case should these expectations be taken as guidance for investment purposes because of the spiraling nature of inflation where higher wages can result in prices going up.

Still, after slowing the percentage by which it is hiking from 75 basis points to 50, the Fed may have to pivot sometime in 2023, and the timing (whether in the middle of this year or later) will depend on inflation measurements. Here, while goods inflation is under control as a result of lower commodity prices feeding into manufacturing, it is wage inflation that should remain high, especially in the services sector.

In these conditions, with persistently high inflation, there is a strong likelihood that the stock market behaves more or less the same as in 2022, except for a drastic economic slowdown or a recession after so much liquidity has been removed from the monetary system. This further increases the appeal of SPDN as a shorting tool.

Shorting with SPDN

The ETF seeks daily investment results of 100% of the opposite of the performance of the S&P 500 Index (SP500). It charges net fees of 0.49%, lower than alternatives like the ProShares Short S&P 500 ETF (SH), which comes at an expense of 0.89%. Lower charges become more attractive when you have a longer investment span, as is the intent here, either for shorting or hedging.

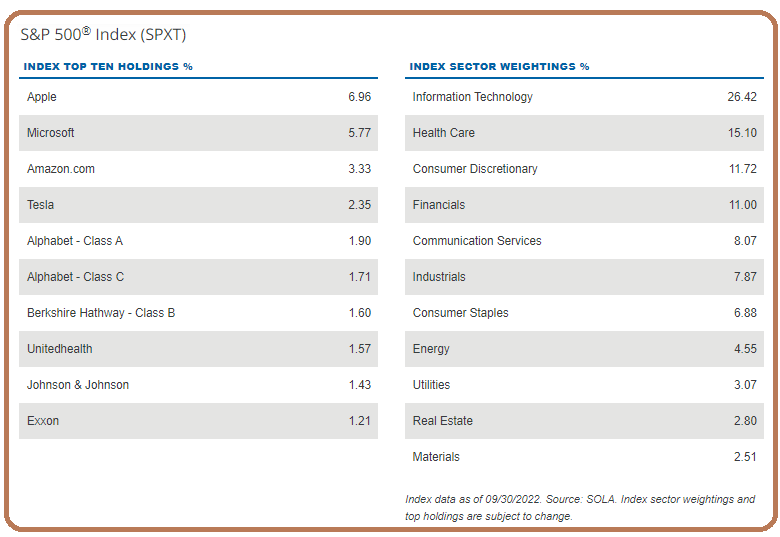

Going deeper, Standard & Poor’s (the Index managers) have selected the stocks comprising the index on the basis of factors like market capitalization, the financial viability of the company, and the public float. Another important factor is liquidity. This is what is termed a float-adjusted and market capitalization-weighted index, and as a result of filtering stocks based on these two metrics, the following list of top holdings is obtained.

Top Holdings of SPXT (www.direxion.com)

Therefore, when the stocks of these world-renowned mega caps go down, expect SPDN to go up, and this is what has been happening during the past month when the ETF gained 5.45%.

Now, these stocks going down when the U.S. economy is still producing jobs may appear to be highly contradictory. Well, it is not. The reason is that it is the services sector exemplified by restaurants and travel which is driving the economy currently, not tech. As a matter of fact, large companies like Tesla (NASDAQ:TSLA), Apple (NASDAQ:AAPL), and Google (NASDAQ:GOOG) have been announcing big layoffs due to demand uncertainty. This is explained by the tightening of monetary policy contributing to higher borrowing costs, in turn dampening the appetite of corporate executives to spend more money on business expansion.

Pursuing further, Healthcare is also impacted by high inflation as per a report by consultancy firm Deloitte entitled “Inflation Signals unrest ahead of healthcare.” As for the Consumer Discretionary play, Amazon (NASDAQ:AMZN), which also has a huge IT cloud infrastructure business, is reducing its labor force by more than 18K, compared to an earlier announcement of 10K, again because of economic uncertainty.

Against the above wave of pessimism, the only bright spot appears to be Financials, as, in sharp contrast to the Great Financial Crisis of 2008, U.S. banks are well-capitalized according to recent stress tests carried out by the Fed. However, only 11% of SPXT’s assets are dedicated to the financial sector, outweighed by IT, Consumer Discretionary, and Healthcare, which represent a combined weight of more than 52%. This implies that there are more chances of a downside and, with its inverse relationship to SPXT, SPDN should see an uptrend, possibly to the $17.6-$17.8 range, which has been its resistance level for the last six months, and even higher in case of a recession.

After shorting, I now highlight the hedging aspect.

Hedging with SPDN

Now, for those who have not sold all their financial assets (equities, bonds, and precious metals) and are not all in cash, it makes sense to hedge. Traditionally people used a portfolio of equity and bonds in a 60:40 or 70:30 ratio, as it provided some protection in case of acute stock market fluctuations. The main rationale was that bonds were relatively sparred by volatility and provided fixed income.

However, 2022 showed us that volatility is highly contagious, even in bonds, and the combination of yields going down and falling prices resulted in low total returns. Now, bonds are also appealing when recession risks outweigh the effects of rising interest rates on treasuries. However, I remind investors that only the chances of a recession that have gone up and worst (for the bears), according to St. Louis Federal Reserve Bank President James Bullard, there are still prospects for a soft landing, which implies fewer hardships for the market.

Pursuing further, another asset class used for hedging is precious metals, symbolized largely by gold seems to be working as shown in the orange introductory chart above, but the question is for how long? There are uncertainties here also in case the greenback rises rapidly on the back of rising interest rates, and a deterioration in the European conflict. A strong dollar is unfavorable to the commodity asset class in general.

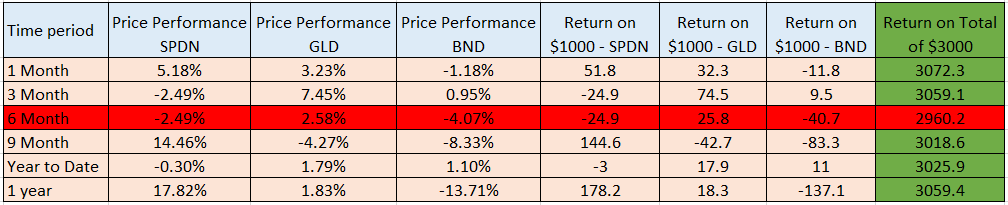

Therefore, again coming back to my previous rhetoric, it is extremely difficult to predict the market and, it makes sense to hedge your portfolio of bonds and gold. For this purpose, using data for different time periods spanning into the last year, the table below built using the price performances, shows that using SPDN, the returns as shown in green are mostly positive. In this case, an example portfolio split equally between GLD, BND, and SPDN to the tune of $1K each has been considered, and the returns were all above $3K, or the initial amount invested, except for the six-month period.

Translating price performances into returns based on an investment of $1K in each (seekingalpha.com)

Hence, based on historical data, this hedging strategy works and could work again given that the level of uncertainty has remained high despite the calendar year change.

Conclusion

This thesis has made the case for a position in SPDN, either to short the market or hedge for your current portfolio of bonds and gold in case you anticipate negative returns. However, Direxion insists on the short-term, as the inverse ETF is designed to capture the opposite/inverse price movements of its benchmark index on a daily basis, and, as such, investment results should be tracked over periods not exceeding one day.

Still, this thesis is making the case for owning it over a longer period, varying from one month to one year. The reason is that it does not employ leverage, which considerably reduces the return-impacting compounding effect when compared to leveraged inverse ETFs like the ProShares UltraPro Short S&P 500 ETF (SPXU). Moreover compared to SH and the ProShares Short QQQ ETF (PSQ), which is used to short tech stocks, SPDN also pays higher dividends.

Finally, uncertainty reigns, and this is where tools like SPDN become attractive. This said, Direxion Daily S&P 500 Bear 1x Shares ETF is not suitable for the average buy-and-hold investor, as it requires continual portfolio monitoring and courage to exit with a stop loss in case the Fed succeeds in taming inflation while not harming the economy.

Be the first to comment