ljubaphoto/E+ via Getty Images

It’s been a while since I last visited SpartanNash (NASDAQ:SPTN), and this essential grocer has done well since my last bullish take on it in September of 2021, giving investors a 53% total return, far surpassing the 12% decline of the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock and highlight why it remains reasonably attractive for potentially strong total returns, so let’s get started.

Why SPTN?

SpartanNash is a unique food solutions company in that it is a distributor, wholesaler, and retailer with a global supply chain network. It has its own stores and also supplies independent and chain grocers, e-commerce retailers, and U.S. military commissaries and exchanges. SPTN has over 17,000 employees and distributes to locations in all 50 states and locations in the Middle East, Europe, and East Asia.

In recent years, SpartanNash has made a number of strategic investments and acquisitions to support its growth and expansion. This includes this month’s announced acquisition of Great Lakes Foods, which is an independent grocery wholesaler that serves 100 independent grocery retailers and further expands SPTN’s footprint in the Midwest.

Meanwhile, SPTN is showing no signs of slowing down amidst economic uncertainty, as net sales rose by 10.8% YoY to $2.3 billion in the third quarter. This was driven by business expansion and retail comparable sales growth of 8%. SPTN has also proven to be adept at expense management, as adjusted EBITDA outpaced revenue growth by 50 basis points, at 11.3% growth to $57 million. Importantly, growth was well balanced between SPTN’s retail and wholesale channels.

Potential to SPTN include margin pressures that may arise from a recent wage increase from $10 to $13 per hour for retail employees. However, this isn’t SPTN’s first rodeo as management is experienced on both the retail and wholesale channel, giving it valuable insights into the end-to-end supply chain. Management anticipates being able to offset these pressures through merchandising transformation and market share growth, as noted during the last conference call:

Thinking about our independent customers, one of the benefits of being a retailer and a wholesaler is that we don’t have to imagine what it’s like to be operating in the retail space. We see it every day and we operate in that way every day. It’s one of the unique benefits we bring to our independent wholesale customers. So, I would expect that our independents are experiencing the same challenges we have and it’s really another reason for us to redouble our efforts and focus on our Merchandising Transformation because frankly, when our customers win, we all win together.

We see the military is seeing a significant channel shift with performance that’s around about 10 percentage points better than market norms. In our retail and independent space, we see the unit volume performance tracking relatively similarly between our independent retail businesses. And importantly on our retail side, we’re growing share. So we’re outperforming the market with respect to unit volumes and we’re very proud of that and have plans to continue to build that going forward.

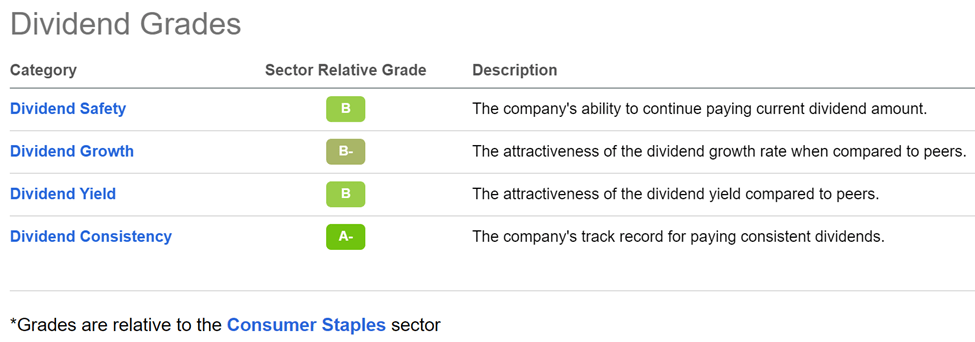

Meanwhile, SPTN maintains a reasonable amount of leverage with a long-term debt to capital ratio of 48%. Its 2.7% dividend yield is also well-covered by a 37% payout ratio, and comes with 12 consecutive years of dividend growth with a 5-year CAGR of 5%. As shown below, SPTN scores A and B grades for dividend safety, growth, yield, and consistency.

SPTN Dividend Grades (Seeking Alpha)

Admittedly, SPTN is no longer dirt cheap at the current price of $31 with a forward PE of 14, which is the same as its normal PE. However, I find it to be reasonably attractive considering the well-positioned business and business expansion. Plus, analysts anticipate robust 18% EPS growth this year, and have a consensus Buy rating on the stock with an average price target of $35, translating to a potential one-year 15% total return including dividends.

Investor Takeaway

Overall, SpartanNash is an interesting stock pick for investors with a long-term horizon. It’s growing its business and it has demonstrated its ability to withstand margin pressures thus far. Plus, having a vertically integrated retail model gives it more control over its costs and gives it insights it would not otherwise have. While SPTN is no longer cheap, patient long-term investors may reap rewards from current levels.

Be the first to comment