zoranm/E+ via Getty Images

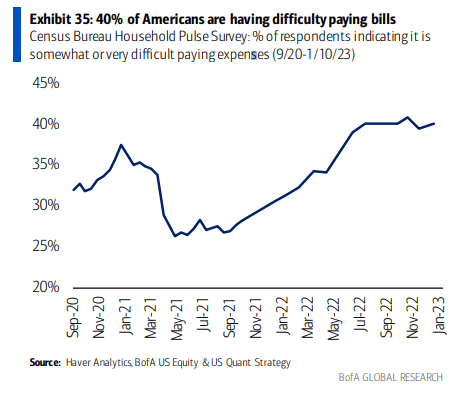

40% of Americas are having trouble making ends meet, according to a recent survey by the U.S. Census Bureau. Utility bills are usually rather high on the pecking order in terms of what gets paid first, and a recent pullback in natural gas prices no doubt helps the situation for consumers who are gradually getting more strapped for cash.

One Utilities sector company faces interest rate headwinds and is down sharply from its high during the middle of last year. Is it a value now? Let’s flip on the lights at Southwest Gas Holdings (NYSE:SWX).

Consumers On Edge

BofA Global Research

According to Bank of America Global Research, Southwest Gas Corp. is a natural gas distribution and transportation company headquartered in Las Vegas, Nevada. Its operations are divided into two segments: Natural Gas Distribution and Construction Services. Gas Distribution transports, distributes, and sells natural gas to roughly 2.0mn customers in Arizona, Nevada, and California. Construction Services offers pipe construction, maintenance, and repair services to LDCs around the country.

The Las Vegas-based $4.4 billion market cap Gas Utilities industry company within the Utilities sector trades at a high 26.9 trailing 12-month GAAP price-to-earnings ratio and pays a high 3.8% dividend yield, according to The Wall Street Journal.

Back in Q3, SWX’s Centuri business was hit more than expected as well as larger than forecast interest rate expenses dinging the bottom line. The management team had already lowered its Centuri guidance and floating-rate debt exposure. Even with an announced spinoff of Centuri, a lot must improve for the stock to warrant its somewhat lofty valuation multiples.

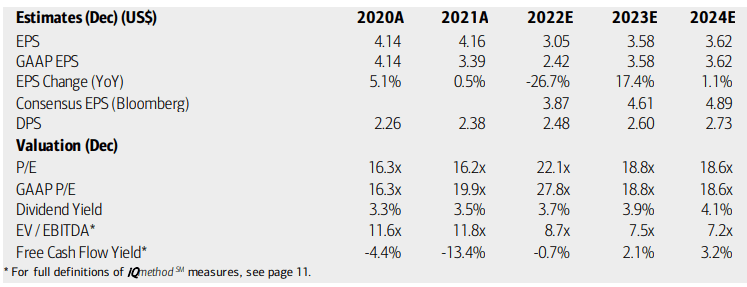

On valuation, analysts at BofA see earnings bouncing back sharply after big losses in 2022. A stabilizing interest rate environment could help the utility, but per-share profits will remain below the 2021 peak for many more quarters. By 2024, EPS growth is seen as very soft at just 1.1% while the Bloomberg consensus outlook is a bit more upbeat.

Dividends, meanwhile, are seen as rising at a steadier rate. Even with a more optimistic earnings growth scenario, Southwest’s operating and GAAP P/Es appear high while its EV/EBITDA is actually decent compared to the market average. Overall, with headwinds coming from both high interest rates and tepid growth, I’m not high on the fundamental valuation case here, and Seeking Alpha’s Quant Ratings rates the stock as worst in its industry.

Southwest Gas: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

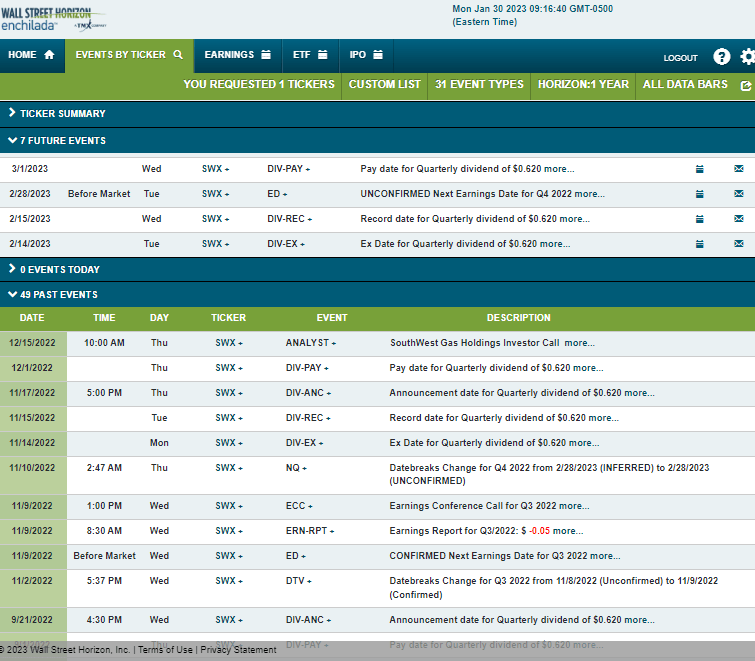

According to corporate event data from Wall Street Horizon, SWX has an unconfirmed Q4 2022 earnings date of Tuesday, February 28 before market open. Before that, shares trade ex-div on Valentine’s Day. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

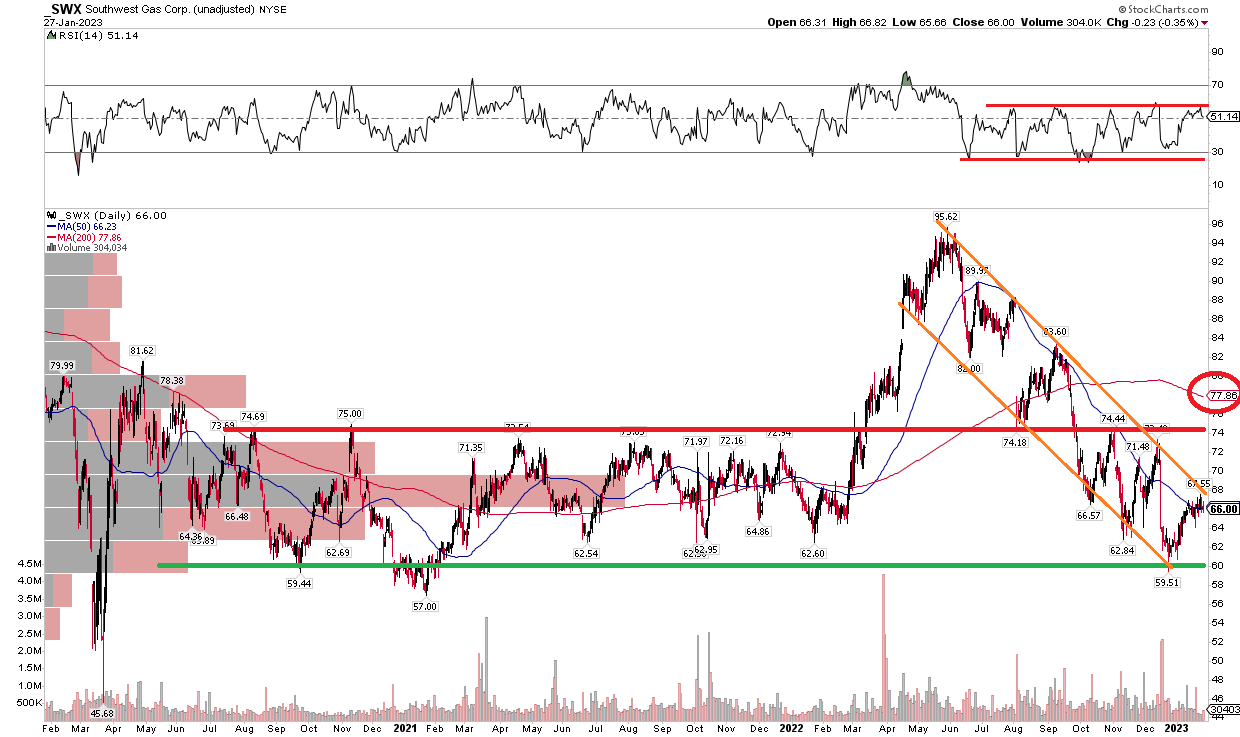

With fundamental headwinds and an unattractive valuation, the chart situation is not a whole lot better. Notice in the graph below that shares are mired in a downtrend dating back to its mid-2022 peak above $95. With a 30% pullback ongoing, there has been a series of lower highs and lower lows, but shares found support near resistance at $60.

For now, that’s a buy point, but with the downtrend and a falling 200-day moving average, the bears are in control. And that is evidenced by an RSI range that is stuck in the bearish 20 to 60 zone. The bulls want to see SWX rise above $75 on volume with an RSI breakout. There is a lot of work for them to accomplish.

SWX: The Bears Roar. Downtrend With Weak RSI

Stockcharts.com

The Bottom Line

While many Utilities feature decent charts with lofty valuations, SWX is controlled by the bears and the fundamentals do not appear strong at the moment. I would avoid the stock for now, but scooping up the shares for a bounce in the upper $50s could work as a tactical play.

Be the first to comment