Conchi Martínez

Perhaps no other sector was struck more instantly, defenselessly, and absolutely than hotels and lodging at the advent of the COVID pandemic. Universally, properties were shuttered, operations ceased, revenue streams evaporated, but expenses continued to accrue. If an operator was encumbered with significant debt (as many, both public and private, were), extreme triage was in order. Cash was conserved, forbearances were sought, and any life preserving accommodation was pursued.

In March of 2020, many hotel REITs found themselves in this exact predicament. From the closing of the Nation’s economy, through development of effective vaccines, through stutter-stepped reopenings, to the present recovery to regain 2019 operating levels, hotel REITs managed to survive. Sotherly Hotels, Inc. (NASDAQ:SOHO) was among them.

On 01/24/23, SOHO announced that its Board of Directors has authorized the reinstatement of payment of preferred stock dividends that had been suspended since March 2020. In response, SOHO’s common shares jumped 25.9%. In this article we will examine the state of today’s travel industry, how Sotherly Hotels is operating within it, and whether SOHO presents an investment opportunity.

Sotherly Hotels – Past, Present, and Future

We first started looking at this microcap hotel REIT in early 2012 when it was called MHI Hospitality and traded under the symbol MDH. In April of 2013, to better reflect the company’s trajectory, MHI rebranded as Sotherly Hotels.

SOHO

At that time, they were building an eclectic portfolio of southern hotel properties that would be rebranded and repositioned to create a unique hospitality experience. You can check out their portfolio here and if you want a more immersive experience, click on Sotherly Audio.

SOHO

I recall repeatedly hearing Drew Simms, then SOHO CEO, say, “I’m really more of a hotel guy than a real estate guy”. I’ve stayed at and toured a number of Sotherly properties and those visits convince me that he has consistently been a pretty good hotel guy.

Today

Fast forward to SOHO’s 3Q22 financial results and earnings call and you will learn that much progress has been made since the darkest early days of the pandemic. By many metrics, operations now exceed pre-COVID 2019 performances and margins have hit record levels. This is excellent news and very encouraging from an investment perspective, but significant uncertainty remains.

Though it was anticipated all fees related to deferred interest granted through earlier forbearance would be repaid by the close of 2022, and debt levels have been reduced by more than $50MM since December 2020, SOHO still carries a significant debt service schedule. In response to an analyst’s questions about how significantly cashflow positive SOHO would be in 2023, CFO Tony Domalski pointed out that satisfaction of all deferred and forbearance costs would free up millions of dollars in cashflow going forward. This is obviously what has enabled the reinstatement of preferred dividend payments.

Tomorrow

The economy is in such a state of flux, business forecasting is difficult regardless of which sector you are examining. Earlier this week a Wall Street Journal article described how hotels were successfully adapting to changes in the way small businesses and workers were traveling. A “Boardroom Outlook” panel at the recent 2023 Americas Lodging Investment summit described that remote work and a growing retiree population continue to drive hotel demand.

All this sounds positive for the hospitality sector but will one interest rate hike too many unravel the trend? Will the spate of tech sector mass layoffs become a contagion and spoil the hoped for soft landing?

Though Sotherly’s common shares trade at just 4.5x estimated forward FFO/share and less than 50% of estimated NAV, success under their debt levels require nearly flawless execution. An uncertain future and debt can combine to add risk to any investment proposition. I would like to own SOHO common, but choose to wait for a clearer picture.

The Preferreds

As previously mentioned, SOHO common shares soared on the preferred dividend reinstatement announcement and the preferred shares joined the enthusiasm by running up from $22 to their $25 par prices. Purchased at par, each preferred series provides a dividend yield approximating 8%, but wait, there’s more.

2MCAC

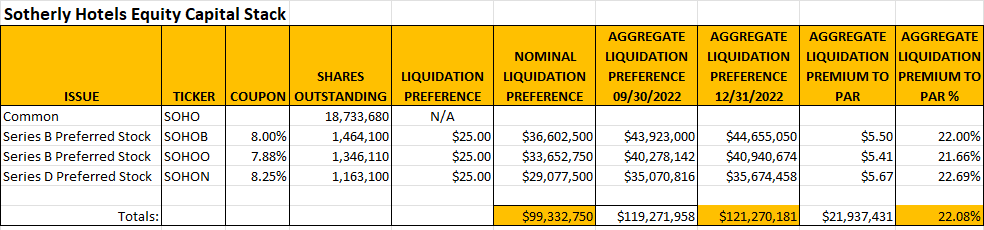

The table above describes SOHO’s current equity capitalization. The equity stack is pretty preferred heavy in that there is a nominal liquidation preference of just over $99MM of preferreds vs. an ~$47MM market cap for the common. Of particular interest to preferred shareholders today is that the dividends suspended since 2020 have accrued and the new aggregate liquidation preference now tops $121MM. The 01/24/23 reinstatement only authorized payment of a current quarter’s dividend. If and when the accrued dividends are paid, that is an additional 20% return on investment.

In Summary

All business is difficult today. While the hotel industry has shown impressive resilience in recent periods, it remains vulnerable to whichever way economic winds blow. We have taken mostly a wait and see stance on the whole sector.

Sotherly Hotels is a strong operator led by an experienced and capable management team. We will continue to monitor progress as time evolves and hold the preferred shares in the interim.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment