Laurence Dutton

Recommendation

My recommended rating for SolarWinds Corporation (NYSE:SWI) is neutral. Even though SWI is the clear frontrunner in the field of network performance monitoring, there are many things I’m not comfortable about with the company right now and in the near future. Key issues that I see would weigh on the stock and growth prospects are the slowing customer growth, the challenging competitive environment, the business transition, and the stigma from the cyber security incident. Even more so, SWI is up against stiff competition from larger vendors who are increasingly including network monitoring as part of their comprehensive product suites. Overall, I see few near-term catalysts, and it’s unclear if SWI can successfully complete its transition and overcome the bad reputation situation in order to reaccelerate growth to historical levels.

Latest earnings highlights

The $187 million in sales were flat year over year but up 2% in constant currency terms. This was higher than the $183 million forecast and the $180 million expected by the market. Management also guided for 1Q23 sales to be between $177 and $182 million. Revenue from subscriptions increased by 45% year over year, totaling $50 million, which was significantly higher than the $41 million expected by consensus. ARR from subscriptions increased by 30% year over year to $175 million, outpacing the 1% increase seen in total ARR. Profits totaled $74.5 million, with an adjusted EBITDA margin of 39.8%. The LTM renewal rate for SWI maintenance has also increased, reaching 93%.

Review of 4Q22 earnings

Objectively, my assessment of 4Q22 earnings was not-too-bad. To start, the renewal rates for LTM maintenance have returned to their long-term averages, which is excellent news. Second, up- and cross-selling are becoming more successful, as evidenced by the rising number of customers spending over $100,000. Last but not least, SWI has made considerable headway in implementing a subscription-based business model. In addition, SWI’s management has stated that the company’s hybrid cloud observability solution is gaining traction, which, in my opinion, may bode well for its future growth as customers weigh the pros and cons of making the transition to the cloud in light of the current economic climate.

Growth ahead

The fact that SWI targets a $40-$60 billion TAM is probably the most noteworthy thing about it. A key factor in SWI’s ability to effectively target this TAM is the company’s ability to efficiently cross-sell by capitalizing on its large customer installed base. As digital transformations and the cloud lead to ever-more-complex IT environments, I believe there will be increased demand for IT Operations and Monitoring vendors. However, I continue to worry about the short-term (business transitions impact) and long-term growth prospects. Concerning the latter, I see rising competitive threat from cloud-native vendors and the possibility that customers are avoiding SWI due to the stigma from the cyber security incident.

Analyst and Investor Day on November 2021

Focus for FY23

In FY23, I anticipate a greater emphasis on leveraging partners and system integrators to increase sales focusing on new products and also cross-selling within SWI’s customer base. The success of this strategy would improve the key indicators that I am looking for (worried for as well): Customers ARPU, LTM retention rates, growth.

For me, the bull case is that SWI will increase its market share in its targeted segments due to its position as a lower cost provider in an increasingly budget-sensitive spending environment. But here is another problem, while this is the time for SWI to capture share since its value proposition is “cost savings”, management FY23 guidance implies they are unlikely to do it. Management is expected to be cautious with their investments, protecting margins. Which means shareholders are already “prepared” for 40+% EBITDA margin. If SWI were to pursue market share and margins come out weaker than guided, the stock is likely to tank.

Valuation

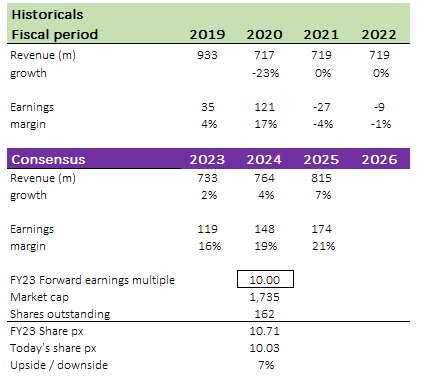

Using consensus estimates, I believe SWI is worth $10.70 in FY24. I believe the weak revenue growth is underpinned by the significant headwinds that I expect SWI to face in the near-term. While I agree that growth could re-accelerate back to historical levels, there are just too many uncertainties in the near-term.

I also do not see any near-term catalyst that could help to push the valuation up given all the uncertainties. Before this rally, SWI was trading at 10x forward earnings, which I expect it to trade at in FYE24.

Author’s own calculations

Risk

Competition

The problem is that there are a lot of well-funded competitors in these categories, so SWI really needs to innovate (which I have little faith given larger and better capitalized vendors are coming for SWI targeted segments).

Summary

In essence, SWI is facing challenges in the near-term with issues such as slowing customer growth, a challenging competitive environment, a business transition, and a negative reputation from the cyber security incident. Despite some positive indicators such as increasing renewal rates and successful cross-selling, the competition is strong and there are few near-term catalysts that could push the valuation up. I believe SWI’s focus in FY23 will be on leveraging partners and system integrators to increase sales, but there is a risk that margins may come out weaker than guided (if SWI goes for market share).

Be the first to comment