vm

SolarEdge Technologies, Inc (NASDAQ:SEDG) is a leading global solar technology company which sells products addressing a broad range of energy market segments and a member of the S&P 500.

Products and Services

Inverters and power optimiser

SolarEdge produce optimized inverters for solar photovoltaic (PV) systems. For a description of solar panels, inverters, and their mechanism of action, please see the section ‘Solar photovoltaic (PV) installation structure’ and subsection ‘String inverters’ of my recent Seeking Alpha article on Enphase Energy (ENPH).

SolarEdge’s primary product is their direct current (DC) optimised inverter system. This refers to a string inverter with a power optimiser present at each solar module. The power optimiser is a DC-to-DC converter which raises or lowers the voltage that leaves each module through real-time adjustments so that electricity generation is maximised for each solar panel. It cannot invert the current to alternating current (AC). SolarEdge’s inverters are sold separately to their power optimisers, but they are specifically designed to work with each other. Inverters carry a 12-year warranty which is extendable to 25-years with a cost, while power optimisers carry a 25-year warranty. This suggests that they are relatively durable.

This provides four main benefits. To begin, if one panel is shaded then the optimiser provides the best voltage and current for the centralised inverter. This prevents the centralised inverter being limited by the lowest performing module, thus generating the maximum amount of energy possible. Next, as certain functions of the inverter are shifted to the power optimiser, this means that the inverter is smaller, more efficient, and cheaper than traditional inverters. Thirdly, there is enhanced system design flexibility as strings are not required to be the same length as they are in traditional inverters. This increases the available area to generate energy. Finally, power optimisers constantly monitor and provide data to the cloud. This data can be accessed through the internet by any device and can reduce operating and maintenance costs for the system owner through identifying and locating faults. Other benefits include enhanced safety and reliability.

Other technologies

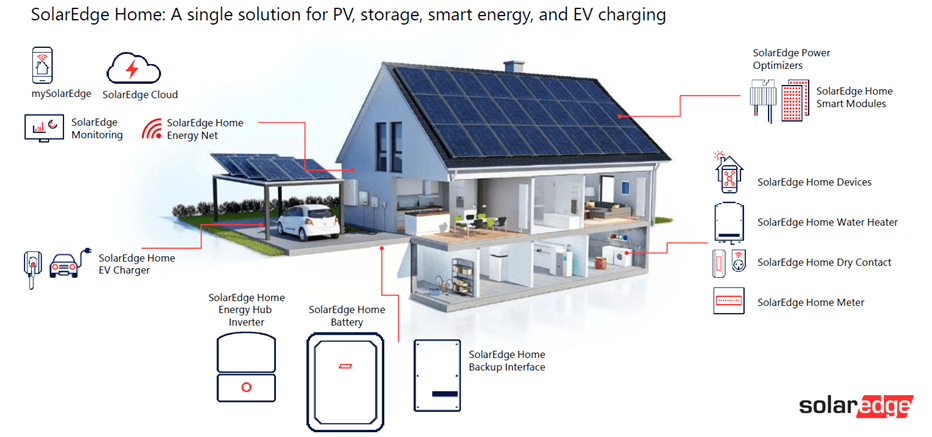

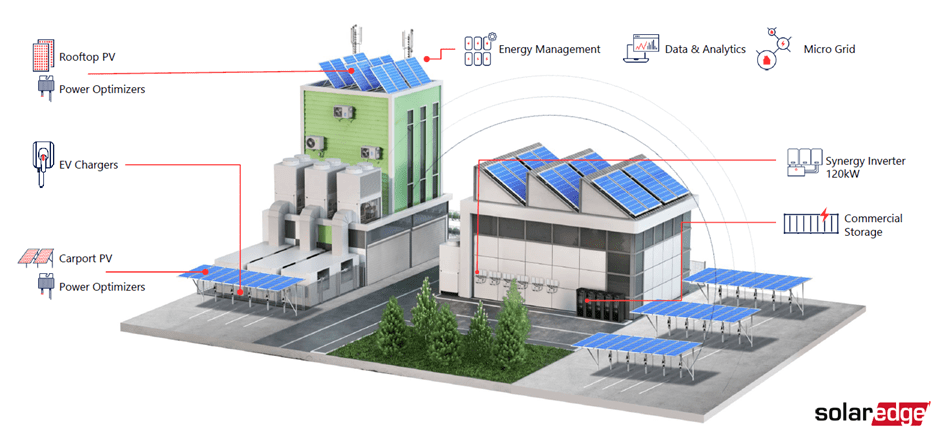

SolarEdge also produces other energy technology, shown in figure one and two. SolarEdge has compatibility between products. For instance, inverters are compatible with batteries for increased self-consumption and storage, and inverters that allow for electrical vehicle charging.

SolarEdge

Figure 1: SolarEdge residential solution

SolarEdge

Figure 2: SolarEdge commercial solution

SolarEdge produce a battery, termed the ‘SolarEdge Energy Bank’. The Energy Bank is a 10kW battery which is designed to be used with the SolarEdge inverters and the SolarEdge energy management system to maximise usage if tariffs are unfavourable. The connection between the batteries and the inverter is through DC-coupling to minimise DC-to-AC conversions to maximise energy output. This is unique among competitors. Multiple batteries can be connected to a single energy hub, and third party batteries can be connected via the SolarEdge StorEdge.

SolarEdge also provide a variety of software to be used in conjunction with their solar technology:

- The designer platform is a web-based app which aids solar professionals in planning residential and commercial solar systems.

- The mapper app allows installers to register the physical layout of the PV sites in the SolarEdge monitoring platform.

- The SetApp is used to activate and configure SolarEdge inverters during commissioning.

- The mySolarEdge app allows system owners to easily track their battery status, solar PV energy generation, household energy consumption, view inverter and battery status, and control the battery’s back-up capabilities.

In addition to this, their monitoring platform collects power, voltage, current, and system data from inverters and optimisers which lets users view module-level, string-level, inverter-level, and system-level data.

SolarEdge also produce an electric vehicle (EV) charging inverter. This uses both grid and PV charging to charge electrical vehicles up to six times faster than a level 1 charger. Level 1 chargers supply an average power output of 1.3 – 2.4kW. This is a first of a kind EV charger with a PV inverter. Through a series of acquisitions, SolarEdge have expanded into selling energy storage solutions including lithium-ion batteries, and e-Mobility products including integrated powertrain technology and electronics for light commercial vehicles, large goods vehicles, and e-motorcycles.

SolarEdge is in the process of developing and providing automation products which allow system owners to increase self-consumption through shifting energy usage to match solar PV energy generation. Tangibly, this looks like using excess solar energy to heat water, for instance. SolarEdge also sell grid services to utilities to manage supply and demand.

Business model and strategy

Strategy

SolarEdge aim to grow through three ways:

- Expand served market through new segments and applications

- Expand served market through geographic expansion

- Increase share within served market.

Revenue and cost of revenues

SolarEdge primarily generates revenue through sales of its optimised inverter. As of December 31st, 2021, SolarEdge has shipped an estimated 83.9 million power optimisers and 3.5 million inverters. The number of power optimisers recognised as revenue increased by 3.1 million units (20.3% increase) to 18.6 million units in the previous fiscal year. The number of inverters recognised as revenue increased by 125.1 thousand units (18.9% increase) to 788.4 thousand units in the previous fiscal year.

In the fiscal year ending December 31, 2021, 45.4% of revenue was generated from Europe, 40% was generated from the US, and 14.6% from the rest of the world. From the previous fiscal year, this represents a 2.5% increase for Europe, a 2% decrease for the US, and a 0.5% decrease for the rest of the world. This suggests that Europe may become the dominant market for SolarEdge.

Cost of revenue consists of product costs, shipping, customer support, product warranty, personnel, depreciation of testing, manufacturing equipment, hosting of cloud-based services, and other logistics services.

Mergers & acquisitions

In January 2019, SolarEdge acquired SMRE, an Italian electrical vehicle and powertrain company. These acquisitions allow SolarEdge to offer components for e-Mobility, automated production machines, and telematics software.

Later in 2019, SolarEdge acquired Kokam Co., Ltd. (Kokam), who provided patented technology for lithium-ion cells, batteries, and energy storage solutions.

SolarEdge also acquired Gamatronic, an uninterrupted power supply (UPS) manufacturer, and established its critical power division.

Manufacturing, supply chains and customers

Raw materials are sourced through various component manufacturers, and a variety of second and third sources are available.

Jabil Circuit (Jabil Circuit), Inc. and Flex Industrial Ltd. (Flex Industrial) are contract manufacturers. They reduce the cost of manufacturing and allow for flexibility of manufacturing products in China and Vietnam or Hungary, allowing for access to Asia, Europe, and North America. This funding arrangement is expected to continue for the future. Additionally, manufacturing capabilities are being expanded to a new site in Mexico. SolarEdge is also developing its own manufacturing capabilities.

The acquired subsidiary, Kokam, have their own manufacturing facility for lithium-ion cells and batteries. Kokam produced its products only in North Israel until the second quarter of 2022, when they announced the opening of a manufacturing facility in Korea. SolarEdge e-Mobility has a manufacturing and assembling facility in Italy. In 2021, a percentage of batteries for the e-Mobility division began being manufactured in Hungary.

Key components of the logistics supply channel consist of third-party distribution centres in the US, Europe, Australia, and Japan.

Products are primarily sold to large distributors and electrical equipment wholesalers and directly to large solar installers and engineering, procurement, and construction firms. These companies then sell further to solar installers.

Financials

Revenue and expenses

In the years ending 2019, 2020, and 2021, revenue from inverter sales constituted 43.9%, 44%, and 42.2% of total revenue respectively.

Expenses on research and development has increased year on year, with the previous fiscal year seeing an increase of $56,510,000. This money is used to develop new products and systems, adding new features to existing products and systems, and reducing unit costs of products and systems.

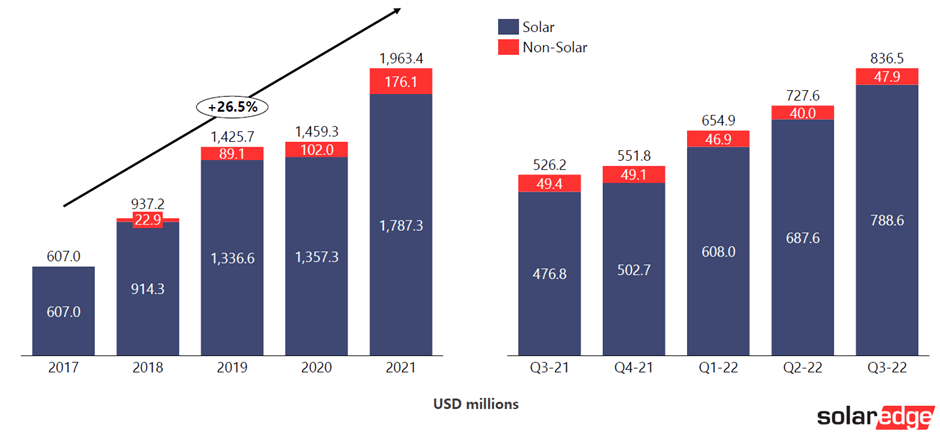

Figure 3 shows revenue by sector. Solar technology (consisting of inverters, optimisers, batteries, and cloud-based monitoring platform) constitutes the largest portion of revenue by far, however non-solar technology appears to be increasing year by year.

SolarEdge

Figure 3: revenue by sector

Risks

Legal proceedings

As background, SolarEdge has frequently engaged in litigation with other technology companies. For instance, in late 2021, the European Patent Office upheld a previous decision to revoke a SolarEdge patent, ending a lawsuit with Huawei.

1. Ampt LLC

In July 2022, Ampt LLC (Ampt) filed a complaint with the International Trade Commission (ITC) alleging that SolarEdge has infringed eight patents related to Ampt’s power optimisers. Ampt requests the court for an unspecified amount of money as damages, a ban on sales of the infringing system, and an import ban on products.

Notably, SolarEdge stated that “SolarEdge and Ampt have been litigating a dispute involving a patent family filed by Ampt before the US Patent and Trademark Office (USPTO) for many years”, and that “it appears that having lost before the USPTO, Ampt is now shopping its claims to other courts.”.

The news of litigation has already had an impact on stock price. On 28 July 2022, the day the ITC agreed to investigate the alleged patent infringement, stock price fell 1.4%. Similarly, on 19 October 2022, when the Judge stayed a proceeding based on similar allegations, stock price fell by $7.96.

The case is currently in ongoing litigation. Though it is difficult to predict the outcome, given that most of the claims outlined within the filing is similar to the claims outlined to the USPTO, it seems unlikely that this litigation will result an adverse outcome for SolarEdge.

2. Investors

In November 2022, many law firms, including The Gross Law Firm, Bragar Eagel & Squire, Levi & Korsinsky, The Schall Law Firm, Jakubowitz law, announced a class action lawsuit. This has been filed against SolarEdge on behalf of anyone who had purchased securities in SolarEdge between August 6th 2022 and October 19th 2022.

The filing claims that:

- The designs of the power optimisers, inverters, and components used to develop SolarEdge’s products were misappropriated from Ampt.

- Ampt made claims against the Company for misappropriating Ampt’s patented technology.

- Evidence existed for the allegations that SolarEdge misappropriated these patents.

- As a result, SolarEdge faced a threat of action which could prohibit the import, marketing, and sale of its power optimisers and inverters.

- This threatens SolarEdge’s ability to monetize on their solar energy systems and generate revenue.

- Revenue generated from the sale of power optimisers and inverters were potentially based on SolarEdge’s unlawful activities.

The result of this lawsuit likely depends on the outcome of the ongoing litigation with Ampt.

Competitors

SolarEdge operates in two main markets: inverters and energy storage. Thus, competitors can be categorised into these two markets.

1. Inverters

Major competitors can be categorised into the string inverter market, and the microinverter market.

The string inverter market has many competitors. This includes, but is not limited to, Fronius International GmbH, SMA Solar Technology AG, Tesla, and Huawei Technologies Co. Ltd. SolarEdge retains a distinct advantage over these competitors due to its power optimiser technology which increases efficiency of conversion, reduces costs, and increases safety.

Tigo, a company headquartered in Silicon Valley, is another threat to SolarEdge. They produce power optimisers. Tigo has two main advantages over SolarEdge. Firstly, Tigo’s optimisers do not need to be added to each module, and instead can be applied to modules which require optimisation (such as shaded panels, for instance). Secondly, Tigo’s optimisers can be used with other inverter brands whilst SolarEdge’s are only compatible with SolarEdge inverters. SolarEdge can remain competitive through providing a full-service solar installation – something Tigo lacks.

The microinverter market is primarily taken up by Enphase Energy (Enphase) and Hoymiles. These companies have similar USPs, and both sell microinverters and technology which can generate solar electricity in the absence of the grid. These companies present a larger threat to SolarEdge than the string inverter market due to microinverters having similar benefits to power optimisers.

2. Energy storage

SolarEdge has several competitors within the energy storage market. SolarEdge lies towards the middle of the range at 10.0kWh.

SolarEdge’s battery has two advantages over the rest of the market. Firstly, SolarEdge has DC-coupled technology which means that less conversions are required for electricity to be stored. This greatly reduces loss of energy. Secondly, simultaneously charging the battery and exporting it back to the grid is possible.

|

Company |

Battery capacity (kWh) |

|

SolarEdge |

10.0 |

|

Enphase Energy |

3.5 – 10.1 |

|

Tesla |

13.5 |

|

Sonnen |

5.5 – 22.0 |

|

LG Chem |

8.6 – 17.2 |

|

Generac |

18.0 |

Figure 4: battery manufacturers and battery capacity. Range of values shows capacity of different models.

Small number of outside contract manufacturers

SolarEdge require Jabil Circuit and Flex Industrial to manufacture products. Therefore, if there is a capacity constraint, or a delay, SolarEdge will be unable to sell products and the company’s revenue will suffer. To mitigate these risks, SolarEdge has begun developing its own manufacturing capabilities.

Customers

In the fiscal year ending 2021, two customers, Consolidated Electrical Distributors Inc., and Sunrun Inc. constituted 30.9% of total revenue. Two customers having such a large share of sales subjects SolarEdge to a large amount of risk if these customers choose to go to a competitor company or stop buying. This would result in a decline in revenue, and a likely decline in share price. Management state that they currently see no credit risk with this concentration of sales, and therefore are not likely to take steps to reduce this risk. To mitigate these risks, SolarEdge would benefit from forming long-term contracts with distributors, and market its products to a wider array of consumers.

Patent expiration

SolarEdge state that their patents are scheduled to expire between 2022 and 2039. SolarEdge’s business model revolves around providing innovative solutions which are protected with intellectual property rights. If SolarEdge’s key technology’s patents begin to expire, this presents issues with remaining competitive within the solar market. Patents can be renewed for up to 20 years. After this point, SolarEdge can only remain competitive through pricing, or through research and design finding newer innovative technology.

Manufacturing site in Israel

SolarEdge’s headquarters, research and development centre, and manufacturing site for Kokam are in Israel. Therefore, political and economic conditions in Israel affect the company. This could manifest as trade tariffs or sanctions being applied to trade, or in the event of a war, employees would be required to perform annual reserve duty in the Israeli military. Additionally, SolarEdge’s links with Israel may deter some clients.

Supply chain issues

See subsection entitled “Semiconductor supply chain issues” in the report for Enphase Energy.

Additionally, the automotive industry is facing component shortages. This presents a problem for SolarEdge’s e-Mobility business, as they rely on a leading automotive manufacturer as a customer. Until the shortage is solved, this will have an adverse effect on revenue.

Reduction, elimination, or expiration of government subsidies

See “Reduction, elimination, or expiration of government subsidies” in my article on Enphase Energy.

SWOT analysis

Strengths

- SolarEdge is well established and innovative.

- Power optimisers are mostly unique to SolarEdge.

- Power optimisers provide better data analytics and maximise electrical output in comparison to traditional string inverters.

- SolarEdge sell a variety of products, not limited to SolarEdge.

- Financials seem to have no red flags.

- SolarEdge’s technology is currently well protected with over 400 patents.

- SolarEdge provide a holistic approach to solar technology for both homeowners and companies.

Weaknesses

- Power optimisers are more expensive than their traditional string inverter alternatives.

- As power optimisers require more equipment on the solar installation, this increases the likelihood of a breakdown.

- e-Mobility business is currently underperforming.

- Non-solar technology is only a small percentage of total revenue.

- As a significant proportion of future revenue relies on R&D, investment returns are not guaranteed.

Opportunities

- A long-term contract with a manufacturer and distributor could allow for steady demand and reduce the chances of supply chain issues.

- A long-term contract with a customer(S) would ensure guaranteed sales.

- Increased funding for R&D would ensure that SolarEdge’s technology remains competitive.

- Increased funding for non-solar technology to promote market diversification.

- Forming long-term contracts with customers and distributors to guarantee supply and demand.

- Given the SEC’s approval, a merger between Enphase and SolarEdge, two market leaders in this field, could eliminate competition and provide benefit to both companies through a bigger set of intellectual property and better scale of economies. This would also allow SolarEdge to begin selling microinverters.

- Diversifying the supply chain would reduce delivery times for customers and help mitigate the risk of issues with key suppliers.

Threats

- Microinverters may outcompete SolarEdge’s power optimisers.

- SolarEdge may lose patents which give it a competitive edge.

- Offices and manufacturing facilities in Israel.

- Two customers currently constitute 30.9% of revenue.

- Only two external manufacturers.

- Recent patent litigation with Ampt may result in key technology not being available to SolarEdge, and thus a marked decrease in revenue and share price.

- Patent litigation regardless of outcome may result in a decrease in share price.

- Semiconductor supply chain constraints.

- Reduction of government subsidies for solar installations could reduce demand.

- Issues with international trade, such as US tariffs, could cause supply chain issues.

Comparison with Enphase Energy

While SolarEdge sell string inverters and power optimisers, Enphase sell microinverters. These technologies have similar advantages and disadvantages. Both allow for better data analytics and increased electrical output, but have increased cost, increased levels of management, and an increased risk of breakdown. However, there are minor differences. To begin, SolarEdge’s solar installation is limited to the size of the central inverter. This means that the central inverter has a fixed number of solar panels it can connect to. In contrast, Enphase’s microinverters do not have this issue. This means that consumers have more flexibility with expanding the solar array with Enphase. Next, Enphase’s inverter models are not backwards compatible, so consumers must purchase all new inverters to upgrade their solar array. Finally, SolarEdge has superior efficiency in comparison to Enphase. This, in conjunction with overheating issues with Enphase’s microinverters likely means SolarEdge has minorly better electrical output.

Both companies also sell batteries. Enphase offers the Enphase Ensemble, a 3.5-10.1kWh battery. SolarEdge offers the StorEdge battery, using LG Chem RESU batteries. Additionally, Enphase’s battery is AC-coupled which requires three conversions, in contrast to SolarEdge which uses DC-coupled batteries which only require one conversion. This increases the efficiency of SolarEdge’s batteries substantially in comparison to Enphase.

Valuation and Conclusion

SolarEdge has a Seeking Alpha Valuation Grade of D and a Quant score of 2.98 and Quant rating of “hold.” According to Seeking Alpha, Quant ratings beat the market. Since SolarEdge has a Growth score of A but a Profitability score of C-, and along with my interesting analysis above means that I would have to agree with the Quant rating of hold for now. However, the stock will go to the top of my watchlist, and as soon as the Valuation Grade or the Quant score improves, I will likely then move the rating to a Buy. I like the business model of SolarEdge and the firm has many strengths and opportunities. Clearly, though, all this appears to be already factored into the valuation for now.

In conclusion, while Enphase retains the advantage of a unique technology, SolarEdge’s slightly more efficient inverter, majorly more efficient battery, and greater spread of businesses in the energy sector makes SolarEdge the more interesting stock from an investor’s perspective, but both stocks I think are only a hold at current valuations, but should still be watched carefully to buy on a better valuation.

Be the first to comment