Justin Sullivan

SoFi Technologies, Inc. (NASDAQ:SOFI) stock has pulled back from its post-earnings surge as astute market operators likely used it to cut exposure, leaving late buyers in a lurch once more.

We had already cautioned investors in a pre-earnings update in late January to abstain from chasing SOFI’s post-earnings momentum to avoid getting ensnared by such pullbacks.

Accordingly, SOFI has retraced nearly 20% from its post-earnings highs as investors assess the company’s prospects for FY23.

CEO Anthony Noto & his team lifted the sentiments of SOFI bulls as management telegraphed that the company is on track to achieve net income profitability on a GAAP basis by FQ4’23.

It’s a monumental milestone for SOFI, as we were cautious about taking exposure in SOFI, as its adjusted EBITDA gains have not translated meaningfully into GAAP profitability.

As such, with SOFI suggesting it has a line of sight toward a critical bottom line metric, it should improve the confidence of long-term investors to hold SOFI beyond just speculative exposure and potentially even as a core holding.

SoFi’s reputation as a digital finance company focusing on higher-income consumers is well-known. Therefore, the company’s decision to leverage on such customers has worked well in the harsh macroeconomic conditions, avoiding the less affluent consumer challenges seen in LendingClub (LC) or Upstart (UPST).

Accordingly, SoFi managed to deliver personal loan volume origination growth of 50% in FQ4, mitigating the impact on home and student loans. Moreover, SoFi bank also saw a significant increase in its deposit base, as total deposits grew 46% QoQ to $7.3B.

Coupled with the improvement in the securitization market, it has provided SoFi with tremendous flexibility in deploying its balance sheet, with potential leverage in the small and medium business (SMB) space in the future.

Therefore, we believe the secular tailwinds driving SoFi’s appeal as a digital finance company remains, as it continued to gain traction in the personal loan space, up to 6%.

Moreover, it also highlighted that its “Financial Services Productivity Loop” is reaching an inflection point, with a ratio of 4.9x financial services to lending products in FQ4’22, up from last year’s 3.8x. Hence, the cross-selling momentum has continued to gain traction, helping the company improve its operating leverage toward GAAP profitability.

Moreover, SoFi is also on track to significantly reduce its stock-based compensation (SBC) as a percentage of revenue toward its longer-term plans of “single-digit stock-based compensation margins.” Accordingly, the company posted an SBC margin of 16% in FQ4, down from last year’s 27.5%.

Investors should watch this metric closely, as it’s likely instrumental in its path toward GAAP net income profitability.

Therefore, with SOFI delivering a solid Q4 performance and a better-than-expected FQ1 and FY23 guidance, we weren’t surprised that SOFI surged initially post-earnings.

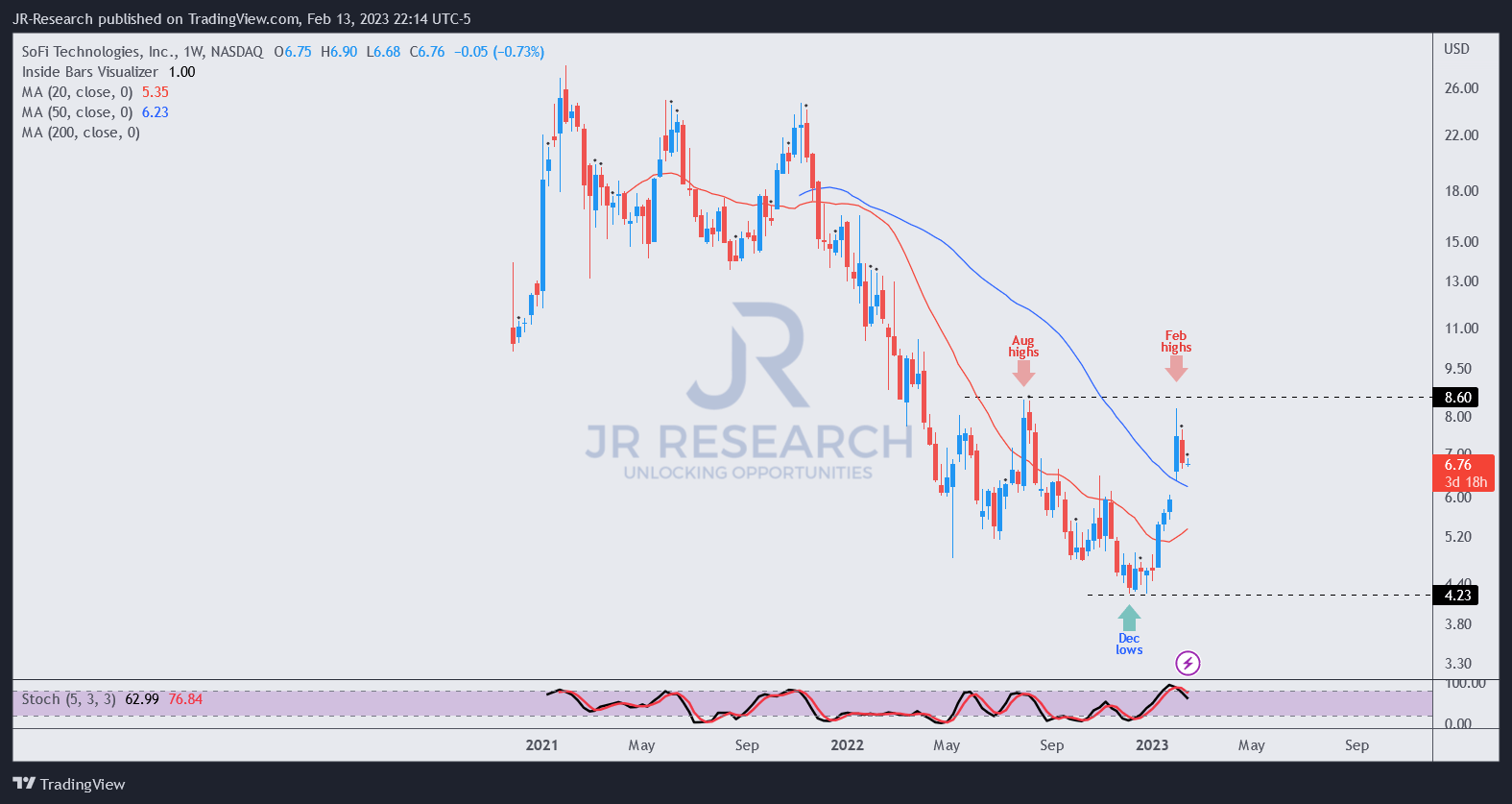

SOFI price chart (weekly) (TradingView)

A closer inspection of SOFI’s price action can help investors better understand its trajectory pre- and post-earnings.

As seen above, savvy SOFI buyers had already loaded up on SOFI in December, as it was consolidating constructively. As a reminder, we urged investors to avoid the pessimism in late November and add more exposure.

The recent surge attempted to re-test SOFI’s August highs but had yet to occur.

Despite that, we believe SOFI’s demonstrated path toward GAAP profitability likely implies that falling back toward its December lows is unlikely.

However, a period of consolidation is still healthy, allowing investors to join the savvy and patient dip-buying market operators instead of chasing sharp upward spikes.

For now, we encourage investors to remain patient as we assess the pullback and subsequent consolidation process.

Rating: Hold (Reiterated, but on the watch for a revision).

Be the first to comment