Lisa Bronitt/iStock Editorial via Getty Images

I recall, several years ago, attending a conference where the CEO of one of the largest banks in America was asked whether he was worried about the large technology companies (i.e., Apple, Amazon, or Google) moving into its turf and disrupting the banking industry. The response was (paraphrasing from my memory) something along the lines of:

If the large tech companies would like to be regulated to death as a large bank…..yet potentially earn 10% or 15% on equity and low single digit revenue growth? not sure that’s an attractive business model for large tech companies….

More recently, Goldman Sachs (GS) has scaled back its ambitions in the online consumer division Marcus. The estimated cumulative losses for the unit are estimated at $4 billion. Specifically, checking accounts as well as Marcus’ Robo-advisors will be offered to selected well-to-do clients (as opposed to the initial intention to roll it out to the masses) and unsecured consumer lending is reined back as well. The high-yield saving account, however, has been successful with ~$100 billion of deposits and is expected to be maintained and cultivated. These deposits are important for the overall GS franchise. While the bank will keep credit-card partnerships, it will be very selective about adding to the list.

GS is ditching its plans not just because of ongoing losses and the absence of a clear path to profitability and returns. With the rise of interest rates, it has seen the lofty valuations of FinTechs coming down back to earth and consequently influences shareholders’ perception of GS consumer bank strategy. GS’s management team realized quickly that the consumer unit is a drag on the valuation of the stock and thus is quickly pivoting away from the strategy that seemed lucrative, only 12 months ago, when interest rates were zero.

But what does it all mean for SoFi Technologies’ (NASDAQ:SOFI) valuation?

The Retail Investors’ Versus Contrasted

I have written a number of articles with a bearish tone on SoFi (here and here). Subsequently, as I listened to the bullish narrative, I realized that many investors are thinking about SoFi as a technology company and not as a bank. This manifests in retail investors focusing on metrics such as topline revenue growth and product numbers but not necessarily cognisant of important banking metrics (capital, ROE, profitability, unit economics, efficiency, etc.), or in other words, risk-adjusted returns.

The underlying and unshakable belief of many retail investors is that SoFi is the ultimate disruptor of banks. Those growth metrics (e.g., deposits, revenue growth, market share, and product numbers) reinforce this. After all, SoFi is meeting or exceeding all the revenue targets it set out prior to IPO, right?

However, I think about SoFi as an online bank (I am putting aside the technology division for now) and assess its prospects based on metrics that are relevant to banks as well as comparability to banking peers.

These include capital requirements, cost of capital, asset mix, ROE, efficiency ratio, and competitive landscape.

Banks’ Cost Of Capital And Valuation

A bank’s cost of capital is key to its valuation. As a rule of thumb, most of the large diversified banks in the U.S. assume their capital is ~10%. In other words, if a bank generates ~10% ROE, it should trade around its book value. The market-implied cost of capital for certain banks is higher, for example, Citigroup (C) is generally ascribed a higher cost of capital compared to JPMorgan (JPM) and Bank of America (BAC). The reason for this is that Citi is perceived as a more risky bank possibly due to its more international footprint and historical operational risk issues.

An IMF paper on bank capital and cost of equity made the following useful observations:

Banks with riskier loan portfolios set up higher provisions to face losses when they materialize. Equity investors may thus require greater compensation from banks with higher provisions (higher risks), which result in a higher cost of equity. We also include a control for a bank’s quality of management, measured by the ratio of salaries and benefits to total assets. We label this variable INEFF (for inefficiency). We expect it to be positively associated with the cost of equity, as banks with higher personnel expenses per dollar of assets may be seen by investors as inefficient and penalized with a higher cost of equity. Bank earnings are closely monitored by equity investors and are expected to affect the cost of equity significantly………Additionally, larger banks may be viewed by investors as too big to fail (e.g., Deng et al. 2007; Belkhir, 2013), and the risk premiums they have to pay equity holders may be lower than those required from smaller banks.”

SoFi, in the space of 2 quarters, has transformed its assets’ profile from relatively lower-risk student loans and mortgages to a predominantly unsecured personal lending bank. The cost of capital for SoFi would now be much higher than other large and well-diversified banks. Based on market comparables in unsecured lending, I would assume SoFi’s cost of capital to be somewhere in the range of 20% currently. So, to trade at around book value, SoFi should generate ~20% return on its equity base. When I say profitability, I refer to GAAP net income including depreciation/amortization and share-based compensation. Clearly, the market would have a “view” of the future profitability and growth of SoFi, and thus ROE projection and factor it in the valuation.

Clearly, I am over-simplifying the analysis here as most of SoFi’s capital is currently allocated to its technology division. From a valuation perspective, I believe that SoFi deserves a sum-of-the-parts valuation which would include a distinct valuation for the technology division and a separate one for the banking subsidiary.

Capital Position

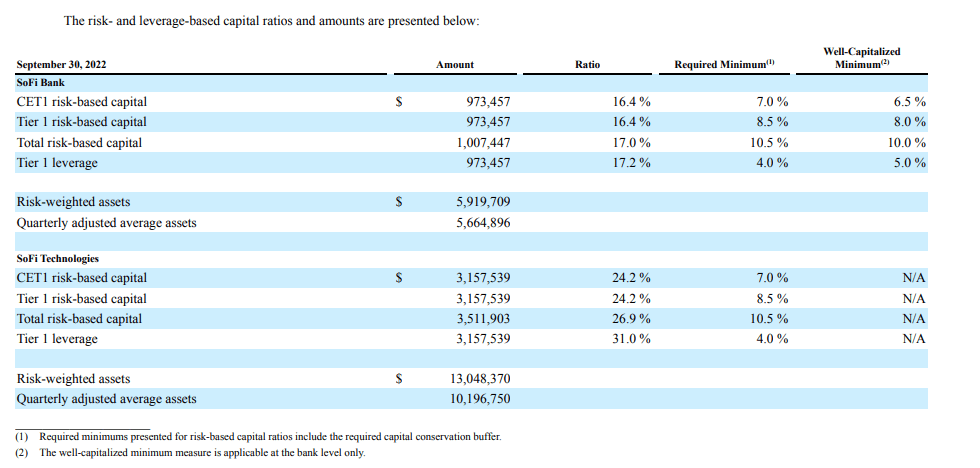

SoFi’s capital ratios are illustrated below from its latest 10-Q:

SoFi Investor Relations

It currently has ~$1 billion of capital allocated to its banking subsidiary and it is noting a required minimum of 7% for CET1 and 4% Tier 1 leverage.

It is important to understand that for an unsecured personal lender like SoFi, the ratios should be much higher. For example, LendingClub (LC) is required to maintain an 11% ratio for both. I suspect that SoFi’s regulators have not yet caught up with the change in the business model, otherwise, this would clearly be a capital arbitrage. I also note that SoFi’s personal loans are not reserved currently in line with the CECL requirements given that these are designated as Held-For-Sale. I assume, at some point, capital will be reallocated from Sofi Technologies to support the capital ratios in the banking subsidiary.

However, the important point is to understand how the capital ratios operate in practice and I will use the Student Loans versus Personal Loans as an example.

From a CET1 perspective, $100 of student loans would attract a much lower capital charge compared with a $100 personal loan. However, both will consume the same amount of Tier 1 leverage ratio. Now clearly, personal loans deliver much higher revenue as the average yield is ~13% versus ~5% for student loans. Now, the binding capital constraint for personal lenders is typically the leverage ratio and not CET1. Hence, all else being equal, personal loans would generate a much higher return on equity for banks than student loans (albeit the former are clearly riskier). So, this explains the pivot SoFi has made to personal loans. They are much more profitable per unit of capital and capital is (or will shortly become) scarce.

The other point to note is that generating returns from originating and selling personal loans is not going to be super profitable. To earn good returns, SoFi needs to hold these for longer (and we can debate how long “longer” means in the comments section!) and generate Net Interest Income.

Efficiency, Unit Economics, Profitability, Risk And Loan Loss Management

Banks are not sexy businesses. The ability to generate superior and sustainable returns largely depends on cost efficiency and risk management credentials. Acquiring market share is negative if it is not done through the lens of appropriate risk-adjusted returns. For example, if you are running an unsecured personal lending business and you are not very profitable (or showing clear unit economics) when the credit environment is benign, that’s a potential red flag. Cost (including deposits APYs) and operational efficiencies are key enablers. Risk and loan loss management are key enablers as well for the success of the bank. Currently, the SoFi management team has not yet proven its credentials in the risk management space.

Additionally, there is no real visibility of the unit economics, underlying profitability, and capital trajectory of SoFi. So, in my view, a leap of faith is required.

A Note Of Optimism

As I noted in my previous articles, I am not a perma bear. I am open-minded to change my mind if I see credible evidence to point out otherwise.

The recent acquisitions of shares by SoFi’s CEO are certainly a good sign for the bulls. The evidence that a large percentage of SoFi’s deposits are done through direct deposit channels is also encouraging. The ultimate success of an online bank, in my view, is somewhat dependent on its ability to generate sticky deposits at a low cost.

Finally, I will be the first to admit that I do not have a good grasp of SoFi’s technologies division and its prospects. I am still early in my learning curve in this space and will update my thesis accordingly.

Final Thoughts

I think the biggest mistake by investors is assessing SoFi through the lens of a growing technology company. I see it as just another online bank and assess it as such. At the end of the day, it is about the risk-adjusted returns on capital SoFi is able to generate when it scales and whether its capital trajectory can sustain this growth. There is a major difference between the revenue generated from selling loans, student loans, personal loans, and hedging income. Investors need to distinguish these from a risk-adjusted return on a capital basis.

I am far from convinced whether SoFi indeed has a sustainable moat. Banking is a very competitive industry operating on thin margins and I don’t really see SoFi doing anything special or having any secret sauce. I am concerned, though, with the lack of apparent profitability but I admit, it is largely a black box to me especially given the multi-product approach and costs allocations internally. There aren’t sufficient financial disclosures to ascertain the true profitability and return on equity prospects. Conceptually, unsecured lending should be very profitable but the overall cost structure (especially marketing efficiency) is not transparent in the financials. So a leap of faith is required.

I am also not sure that I am a fan of the scattergun approach when it comes to products. If I want to trade shares or options, I will probably use my Interactive Brokers account as opposed to SoFi’s product. Seems to me like the strategy lacks focus, and more importantly, it is unlikely to be a very profitable one.

SoFi should be valued as a bank. And if you believe it should trade at 3x tangible book, then the risk-adjusted returns on capital will need to be spectacular. The challenge to Mr. Noto is not just to deliver growth (that’s not hard to do), rather it is about generating sustainable returns well above SoFi’s cost of equity.

As far as I am concerned, the jury is still out when it comes to SoFi.

Be the first to comment