In a recent issue of TQI’s Earnings Analysis Series, we looked at three cloud software companies in our Moonshot Growth portfolio – Snowflake (SNOW), Cloudflare (NET), and Datadog (DDOG). While these three businesses are very different from each other, all of them are tied to the secular megatrend of Cloud Computing.

Snowflake is a software platform that enables organizations to maximize the value of their data resources in the cloud across multiple public cloud vendors. Cloudflare is re-building the Internet by replacing the network piece of the enterprise stack with its global “edge” network that’s designed to make everything you connect to the Internet secure, private, fast, and reliable. And Datadog is a modern cloud app monitoring and security platform.

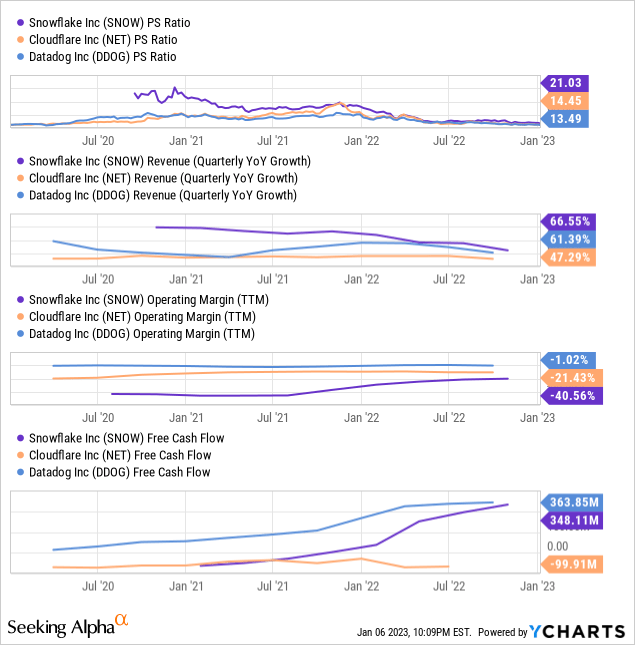

While their businesses are different, the commonality between Snowflake, Cloudflare, and Datadog is that all three of them are rapidly growing, best-of-breed platforms. And being the top dog in their respective categories has earned these three companies’ premium valuations. Despite suffering large drawdowns during 2022, Snowflake, Cloudflare, and Datadog continue to trade at P/S multiples of 21x, 14.5x, and 13.5x, respectively. This is a far cry from the days of 100x+ P/S multiples; however, we are no longer operating in a zero interest rate environment, and even current multiples are relatively high.

As you can see on the chart below, Snowflake, Cloudflare, and Datadog are growing rapidly, but growth rates are decelerating amid a challenging macroeconomic environment. All three of them have negative operating margins; however, Snowflake and Datadog are already making huge amounts of free cash flow.

YCharts

YCharts

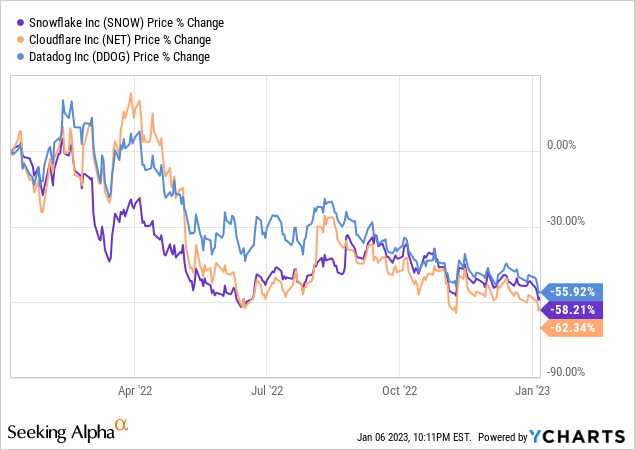

In a rising interest rate environment, long-duration asset valuations have suffered a vicious moderation. Over the last year alone, Snowflake, Cloudflare, and Datadog have declined by ~60% each. While we will limit our analysis to Snowflake’s Q3 report in this note, coverage on Cloudflare and Datadog’s Q3 reports are available exclusively at my marketplace service. I only shared information on Cloudflare and Datadog to convey the idea that Snowflake’s price decline is more about the macro environment than any business-specific issues. If you have been following my work on Snowflake, you know that I have been accumulating shares via a Dollar Cost Averaging (DCA) plan. My last research report on SNOW consists of more details on my buying strategy:

For now, let’s analyze Snowflake’s Q3 report, study its total addressable market opportunity and competitive dynamics, and review its valuation. We’ll also look into Snowflake’s technical setup in this article.

Snowflake Q3 FY2023 Earnings:

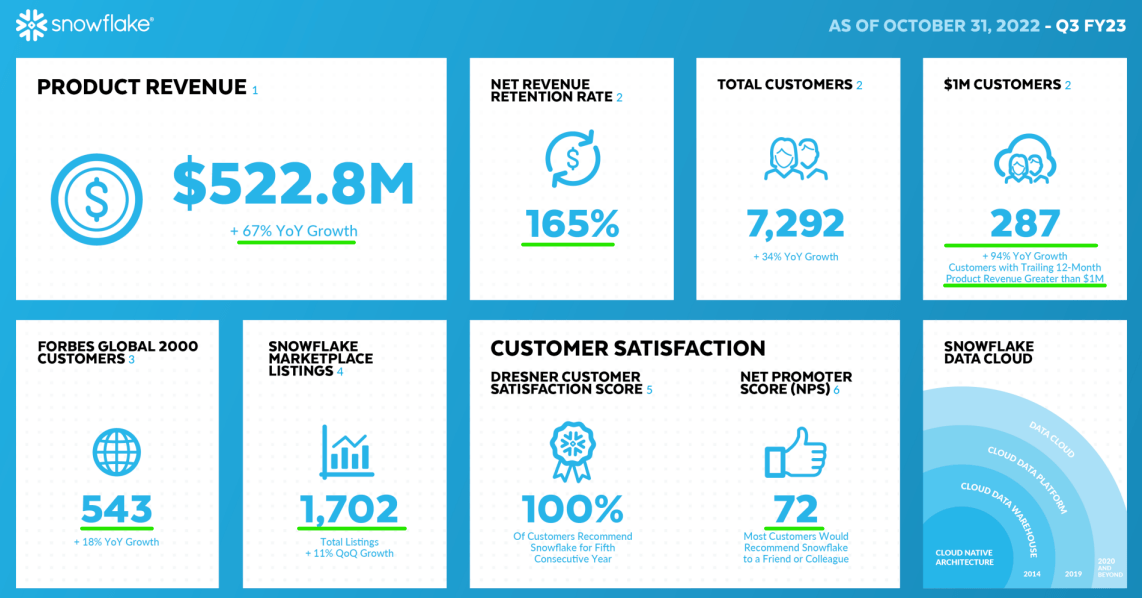

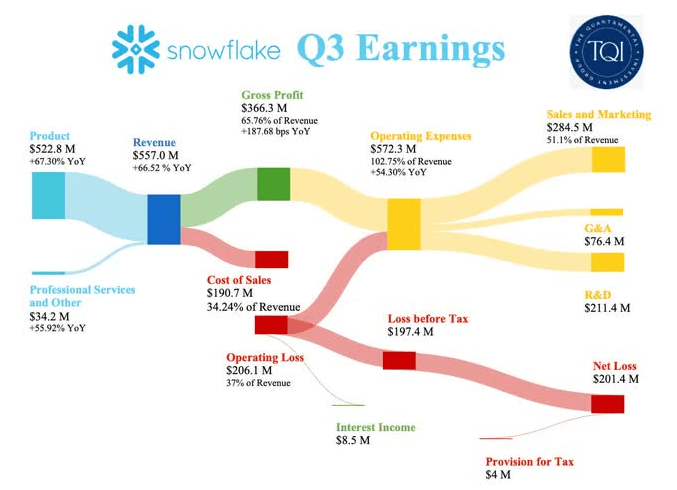

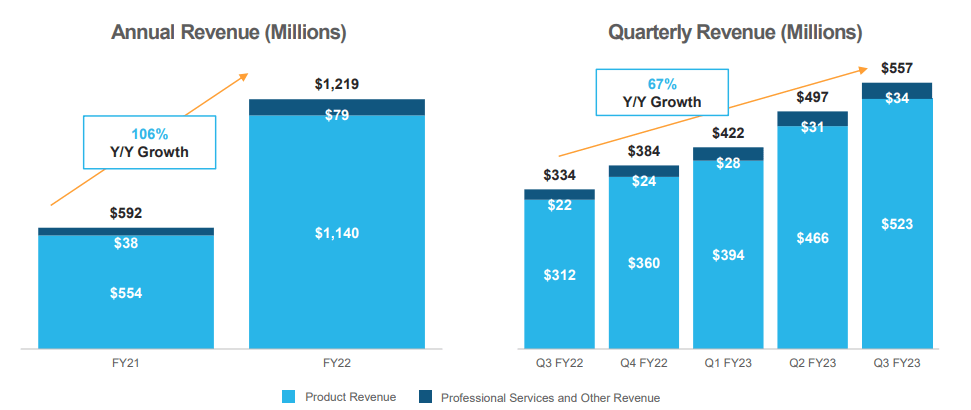

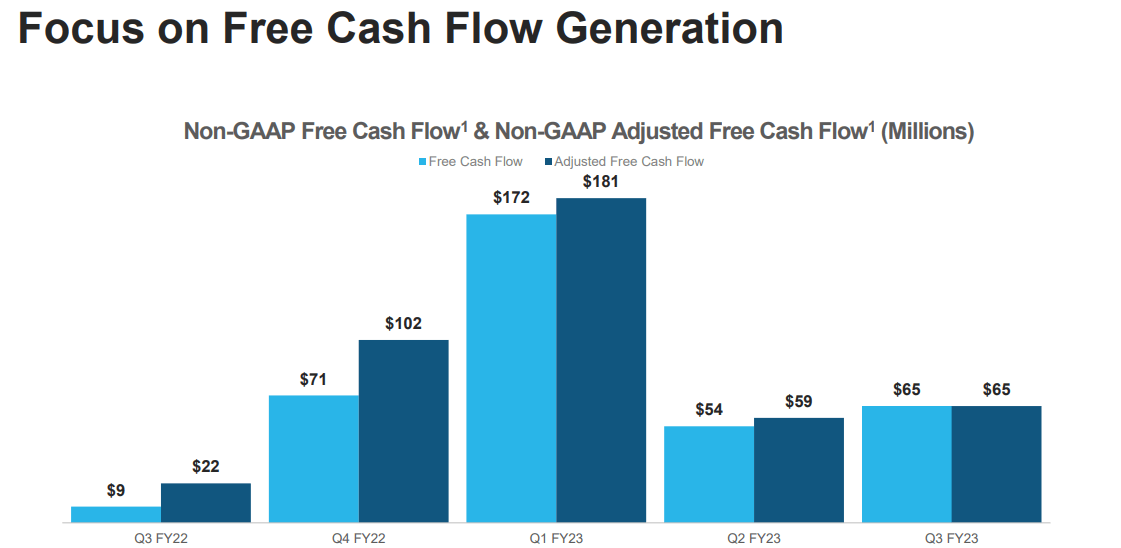

In Q3, Snowflake reported quarterly revenues of $557M, a figure that reflected ~66.5% y/y growth. Of these, product revenue made up $522.8M, with professional services making up the rest. In this quarter, Snowflake’s adj. FCF margin came in at +12%, resulting in adj. FCF of $65M. Furthermore, Snowflake continued winning large enterprise customers at a healthy clip whilst generating massive growth from within its existing customer base.

Snowflake Q3 ER Presentation

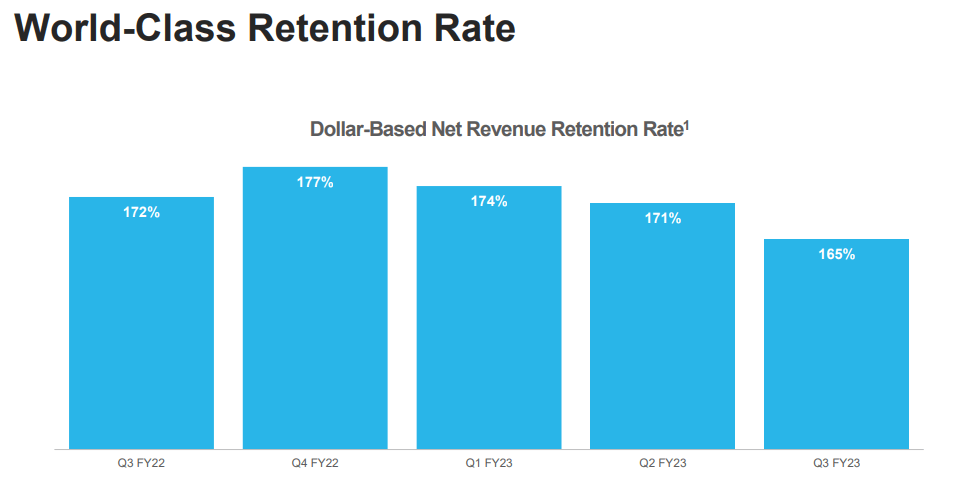

Despite some moderation in this key metric, Snowflake’s net retention rates [NRR] of 165% are indicative of robust demand from existing customers. With an NPS score of 72, Snowflake’s offerings are certainly meeting and exceeding customer expectations.

Management commentary on Q3:

During Q3, product revenue grew 67% year-over-year to $523 million. Our non-GAAP product gross margin came in at 75%, and we continue to drive strong growth at scale, coupled with strength in unit economics, operating profit, and free cash flow. Snowflake’s Data Cloud maximizes the power and promise of data science and artificial intelligence, a high priority in the modern enterprise.”

– Frank Slootman (Chairman and CEO, Snowflake)

Author

While Snowflake is still operating at a loss, it is growing revenues rapidly at scale whilst generating positive free cash flow. Unlike most other cloud software companies, Snowflake’s business showed little impact due to the current macro environment in Q3.

Now, Snowflake’s management highlighted weakness among its SMB customer base during the Q3 earnings call. However, SMBs make up less than 10% of total revenues, and having little exposure to them is playing in Snowflake’s favor in this challenging business environment. Furthermore, nearly 95% of Snowflake’s revenue is invoiced in US dollars (80% of revenue is generated in the US), which has shielded Snowflake’s business from currency fluctuations.

Snowflake Q3 ER Presentation

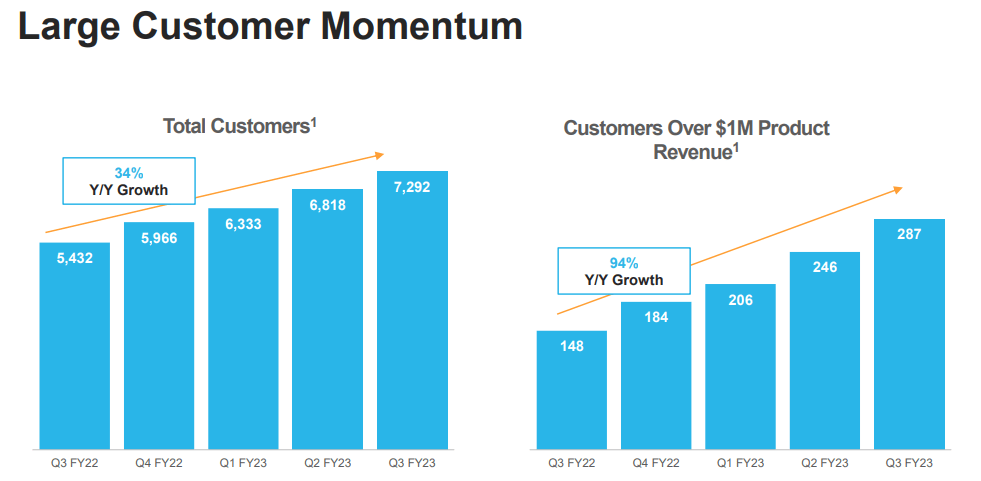

The current macro environment is uncertain; however, Snowflake is still landing customers at a healthy clip of +34% y/y. As of Q3, Snowflake’s “Customers over $1M Product Revenue” count stood at 287 organizations. During their latest earnings call, Snowflake’s management said that – “In the long run, such large enterprise customers could conservatively spend $10M or more on its platform annually.”

Snowflake Q3 ER Presentation

Snowflake Q3 ER Presentation

Moreover, a lot of Snowflake’s enterprise customers are scaling up their spending on its platform. This is reflected in SNOW’s net retention rate of 165%. As you know, very few companies enjoy such ridiculously high NRRs, and that puts Snowflake in rare air.

Snowflake Q3 ER Presentation

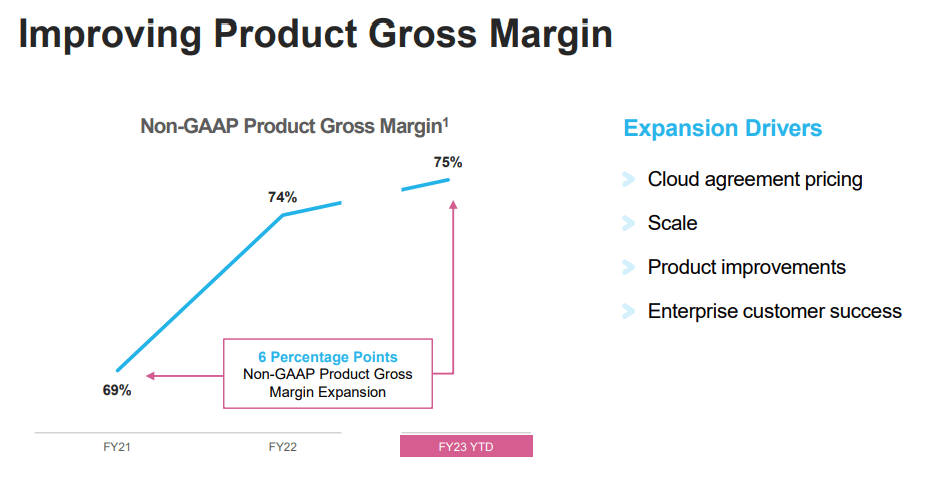

The strength of Snowflake’s platform increases with scale, as it could negotiate better deals from cloud vendors, and better prices mean more and more customers will choose to join Snowflake. In Q3, SNOW’s product gross margin improved to 75% (up +100 bps y/y).

Snowflake Q3 ER Presentation

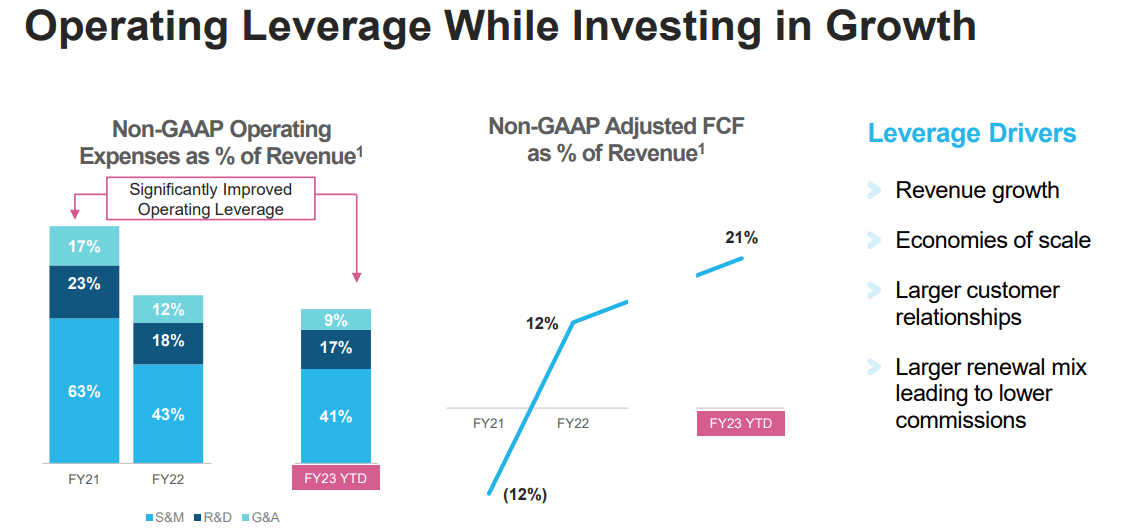

With revenues scaling up and gross margins expanding, Snowflake is delivering robust operating leverage and generating significant amounts of free cash flow.

Snowflake Q3 ER Presentation

Snowflake Q3 ER Presentation

For Q4, Snowflake is projected to deliver Product revenues of $535-$540M (growth of ~49% y/y), and this represents a sharp deceleration. On this subject, Snowflake’s management said that Q4 tends to have a higher number of holidays, and since 70% of Snowflake’s revenues are generated by humans interacting with its platform, revenues tend to be weaker in this quarter.

Snowflake Q3 ER Presentation

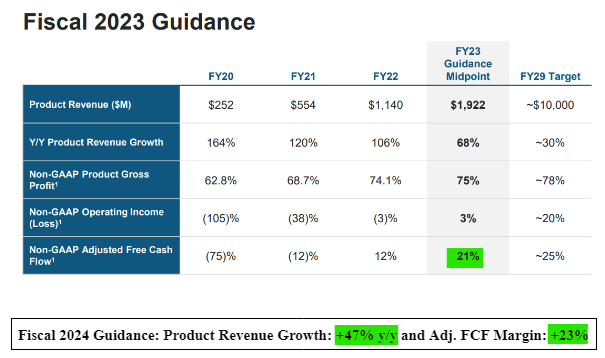

The good news here is that Snowflake’s management guided for ~47% y/y growth in 2023 based on their current consumption patterns (despite a poor macroeconomic environment).

Now, Snowflake is not yet profitable. However, with a cash (plus investment) position of $4.9B and no debt, Snowflake’s balance sheet is a fortress. In my view, Snowflake is an envious position heading into a recession, and this is one of those companies that can come out of a downturn stronger and bigger than ever before.

Competitive Dynamics And Snowflake’s Positioning

Despite Snowflake’s robust financial performance, there’s been a lot of talk about a changing competitive landscape, potentially stopping Snowflake’s rapid growth in its tracks. While the noise has certainly revolved around private competitors like Databricks, Snowflake’s real competition is big tech!

And here’s some commentary on competition from Snowflake’s CEO:

I would say that the competitive dynamic, you know, is substantially unchanged. You know, we’re — I think the balance of partnership versus competition shifts, you know, marginally from one period to the next. I think we’ve said publicly that, you know, our partnership with AWS Amazon has been incrementally stronger and less competitive over time and that continues.

Microsoft has been healthy and with Google GCP, you know, has been about the same. Most of our competitive reality, if you will, is really dominated by the public cloud companies, and that’s been true, you know, for as long as we’ve been here.

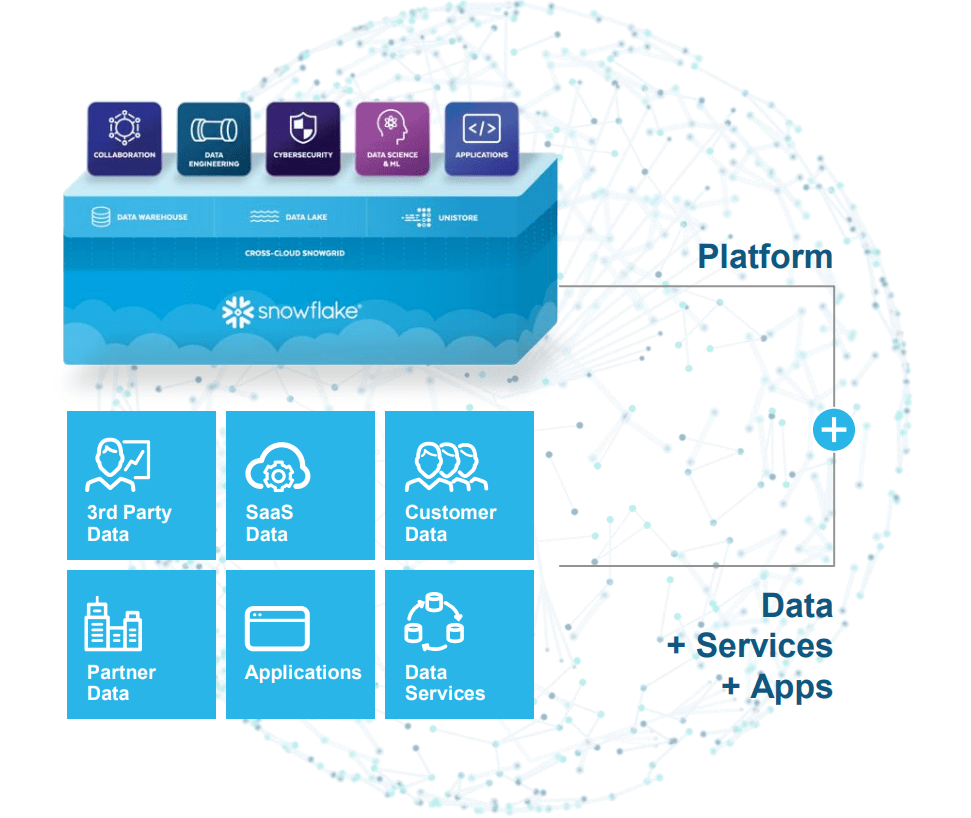

According to Snowflake’s website –

Snowflake is pioneering the Data Cloud – a global network where thousands of organizations mobilize data with near-unlimited scale, concurrency, and performance. Inside the Data Cloud, organizations unite their siloed data, easily discover and securely share governed data, and execute diverse analytic workloads. Snowflake delivers a single and seamless experience across multiple public clouds. Snowflake’s platform is the engine that powers and provides access to the Data Cloud, creating a solution for applications, collaboration, cybersecurity, data engineering, data lake, data science, data warehousing, and unistore.”

Snowflake Investor Relations

That’s a lot of technical terminology. Simply put, Snowflake builds software (for managing the use of cloud infrastructure) that sits between organizations and public cloud vendors. Also, Snowflake is building a marketplace for data providers (sellers) and organizations (buyers) – Data Cloud. As investors, all we need to know is that both of these platforms are gaining traction.

Snowflake Investor Relations

Amid a challenging macroeconomic environment, Snowflake continues growing like a weed, and it is doing so whilst improving margins. As we saw today, Snowflake is not yet profitable; however, it is already producing massive amounts of free cash flow.

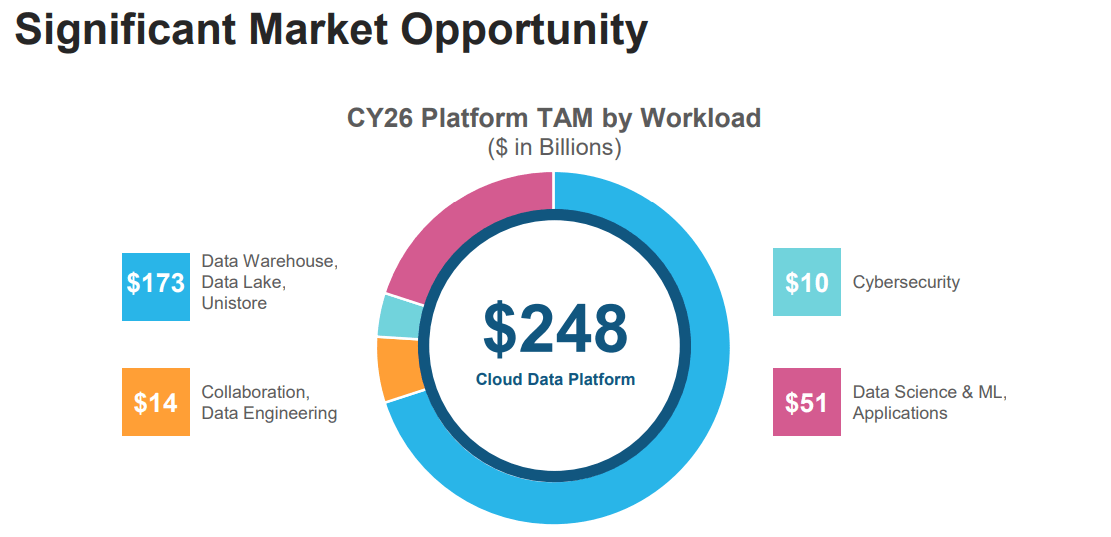

Having a cash (plus investment) balance of ~$4.9B and no debt should provide management with added flexibility to remain aggressive during the impending downturn to capture market share. Snowflake is positioned to win big, and its total addressable market opportunity is expected to grow to $248B by 2026. With all of this in mind, let’s calculate Snowflake’s fair value and expected returns.

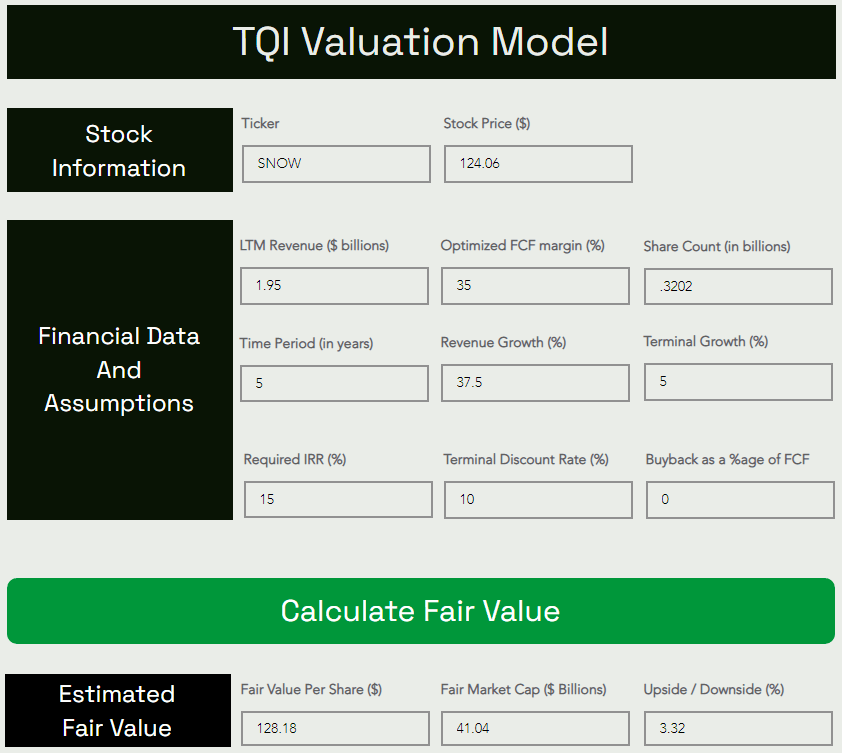

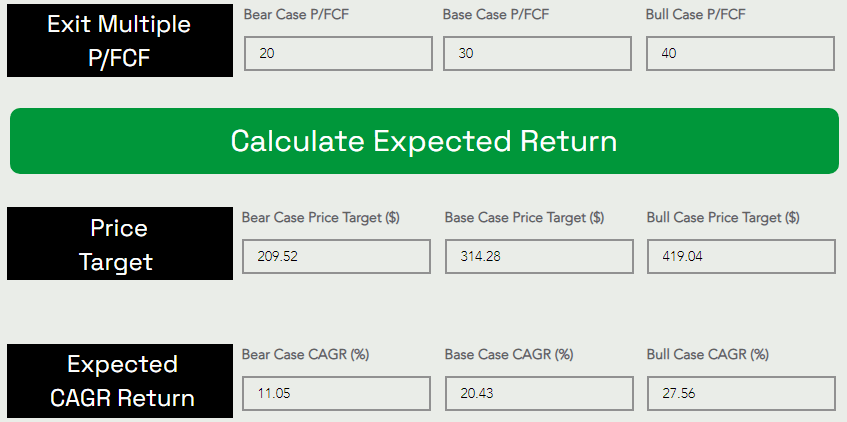

Here’s my updated valuation for Snowflake

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

Summary of update:

Old FV estimate: $118.14, New FV estimate: $128.18

Old Base case PT (5-yr): $290.91, New Base case PT (5-yr): $314.28

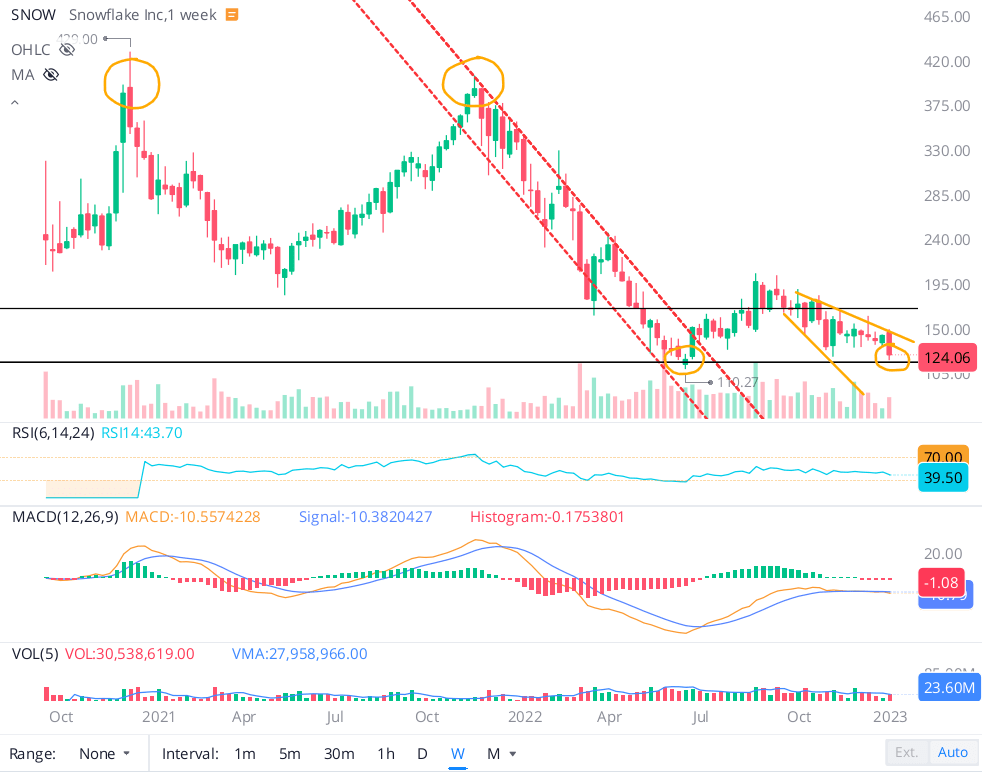

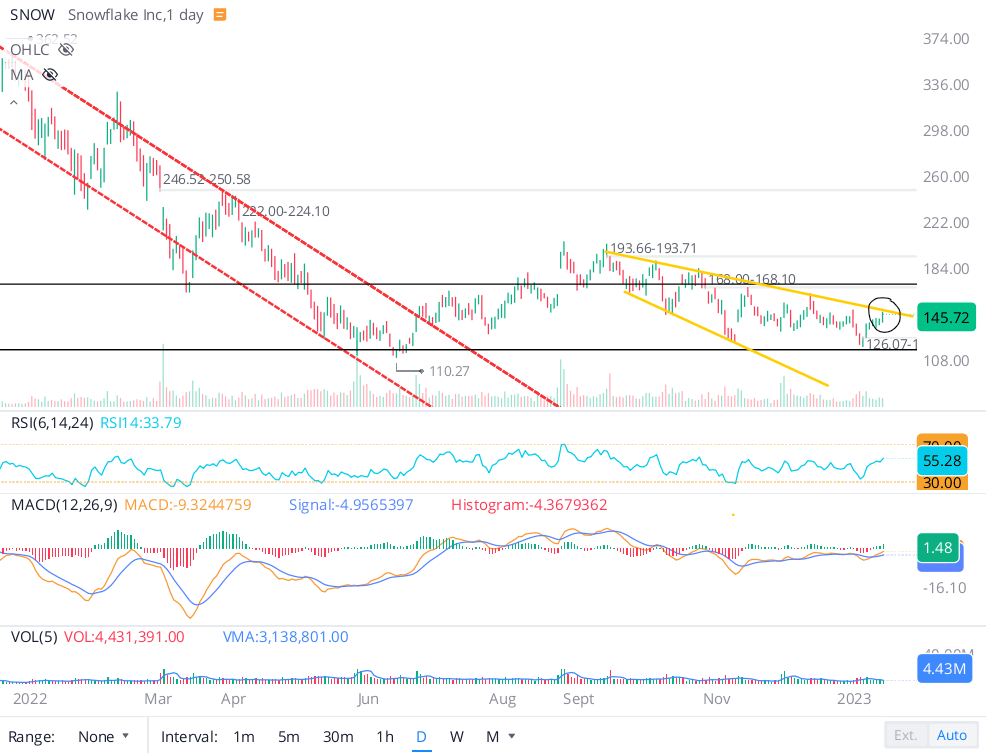

Snowflake’s relatively-short history as a publicly-traded company has been filled with wild swings. After its IPO at $120, the stock started trading at $240 in late 2020 and rallied up to $429 in a matter of weeks during late 2020 (and then again in mid to late 2021), only to suffer a significant drawdown in 2022. From a technical perspective, Snowflake’s stock appears to have entered a Stage-1 base formation.

WeBull Desktop

After hitting a new 52-week low of $110.27 per share last summer, SNOW climbed back up to ~$200 during the July-August bear market rally. However, this move has reversed in the last five months or so, and SNOW’s stock is now trading at the lower end of the apparent base. If we see a bounce around the $100-$120 level, we will get a confirmation of the formation of a base.

In the last week or so, SNOW’s stock bounced up from the ~$124 level, and I now view the $120-$170 range as the Stage-1 base for the stock. Currently, we are sitting right in the middle of this base, and if the recent rally extends, SNOW could test the upper end of the base at $170.

WeBull Desktop

As you can see on the chart above, I have drawn a megaphone pattern on the right side. Snowflake’s stock has turned back down from the upper trendline (drawn in yellow) for several months now, and this could happen again. Hence, a re-test of $120 (lower end of the base) is the more likely outcome for SNOW.

If we do see a decisive breakdown of the $100-$120 range, I would expect Snowflake to correct much further. This is why I suggest slow accumulation at these prices.

Final Thoughts

Given a poor macroeconomic backdrop, equities [especially the long-duration, richly valued ones like Snowflake (~85x P/FCF)] could remain under pressure in 2023. More than 90% of Snowflake’s revenues come from large enterprises, and most of its revenues are committed and billed before consumption. Hence, I am not too concerned about Snowflake’s usage-based business model failing in a recession. That said, SNOW’s stock is unlikely to be immune to the broad market conditions, and hence, we could very well see weakness persisting in this counter for the foreseeable future.

From a technical perspective, Snowflake’s stock is not inspiring at all despite its recent +20% jump. However, a long-term investment does make sense here due to strong fundamentals and a fair valuation [SNOW is not a cheap stock]. As Warren Buffett said, “I would rather buy a great company at a fair price than a fair company at a great price“. Overall, I like the idea of accumulating shares in Snowflake for a 5+ years investment at ~$145 per share using a DCA plan to perform staggered buying over 6-12 months.

Key Takeaway: I rate Snowflake a “Buy” at $145.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment