gorodenkoff/iStock via Getty Images

Investment Summary

We are initiating coverage of Simulations Plus, Inc. (NASDAQ:SLP) stock with a speculative buy seeking an initial objective of $50 per share. We are eyeing an entry with a limit order at $40. SLP operates a diversified software development business model, offering a portfolio of simulation and modelling software solutions for pharmaceutical and biotechnology R&D. This is quite a differentiated value proposition for those speculating on clinical-stage assets. Our findings indicate the company is positioned to leverage its proprietary software platforms over a broad spectrum of services, including consulting and training services to support the pharmaceutical, biotechnology and even funds management industries in their drug discovery, development, and investment processes respectively.

More specifically, the firm’s offerings are designed to reduce the time, cost, and uncertainty inherent in the R&D process and optimize the potential of new drug candidates. This has the benefit of reducing the time to market for pipeline assets with high conversion potential. Looking at the business model, SLP generates revenue through the sale of licenses for its software, alongside recurring revenue streams from maintenance and support services.

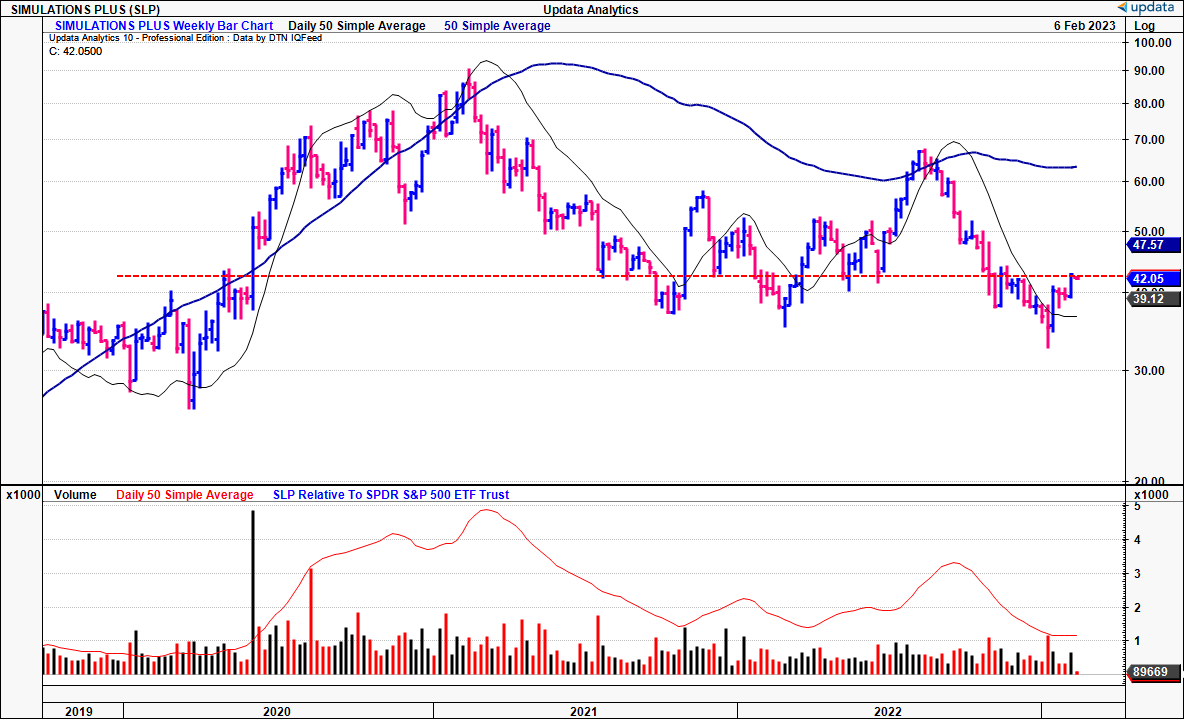

The issue to date is the company’s relatively slow pace of growth, especially over the past 2–3 years where global liquidity has driven tremendous sales growth for companies all along the healthcare value chain. The market rewards earnings growth, especially when it comes cheaply to equity holders. Whilst the latter has been true for SLP as we’ll show here, the former hasn’t – Revenues have witnessed 5-year CAGR of 15%, earnings have grown at CAGR 5.5% over the last 3 years, whereas it has booked EBIT CAGR of 2% over this same time. Free cash flows have lifted around the same pace Hence, equity performance has been lacklustre, with shares trading a shade above pre-pandemic range after a large consolidation [Exhibit 1].

Nevertheless, we believe SLP’s diversified customer base, coupled with its expertise in simulation and modelling technology, positions it well to capitalize on the growing demand for predictive R&D solutions within the pharmaceutical and biotechnology industries. Net-net, rate buy.

Note: investors are to read the “risks” section located at the end of this report before proceeding.

Exhibit 1. SLP re-rating to the downside with absence of growth in fundamentals

Data: Updata

Brief overview of SLP offerings

We believe each of the companies offerings have potential to be a long-term cash compounder with interesting economics tied into the mix. We are most interested in three segments, GastroPlus, MonolixSuite, and the ADMET Predictor. However, there are many more on offer from SLP.

GastroPlus is an interesting segment. It utilizes mathematical programming and AI to simulate human physiology’s response to various drugs and substances. It incorporates an array of pharmacokinetic (“PBPK”) and pharmacodynamic (“PD”) models and provides a comprehensive assessment of drug metabolism and PK. GastroPlus has potential to be a first-line choice for drug companies to streamline their drug development process.

Meanwhile, the MonolixSuite software is a comprehensive platform for non-linear mixed-effects models and provides a wide range of tools for model building, estimation, simulation, and visual exploration of population PK and PD data. The software is designed to support the entire drug development process, from preclinical to late-stage development.

Finally, SLP’s ADMET Predictor integrates various in silico ADMET [Absorption, Distribution, Metabolism, Excretion, and Toxicity] prediction models and tools to enable organizations to optimize their drug development processes and reduce time-to-market. For more on each of the company’s entire suite of software offerings, see here [under software].

SLP Q1 FY23′ results analysis

Switching to the company’s Q1 FY23′ numbers, we noted several data points worth discussing here. Chiefly:

- SLP booked a YoY decrease in total revenue of 4%, marked by a contraction of 17% in software revenue and a growth of 17% in services revenue. The gross margin remained stable at 78%, with a decline in software gross margin to 85% and a concomitant increase in services margin to 70%.

- The disaggregation of software revenue saw GastroPlus contribute 50% of total software turnover, MonolixSuite with 26%, ADMET Predictor accounting for 18%, and the remaining ~6% attributed to its other software offerings. On this, SLP reported customer renewal rates were measured at 82% based on accounts and 90% based on fees.

- Expanding on this segment, we’d note that SLP deliberately aligned the software renewal timing for customers [previously announced], affecting Q1 revenue seasonality, and subsequently aiming to lift its Q2–Q4 results. MonolixSuite revenue also declined by ~100bps due to the renewal alignments and foreign exchange impact, but the company added 2 new customers and made 2 upsells. Meanwhile, GastroPlus turnover declined by ~24% also due to this renewal alignment, but it still added 1 new customer and made 8 upsells. In total, the renewal pattern looks to be progressing as expected, as SLP added 15 new customers during the quarter with 15 upsells.

- Turning to SLP’s services revenue, we noted that ~49% of revenue was generated from PK/PD services, 18% from QSP/QST services, 25% from PBPK services, and 8% from other services. A YoY increase of 14% was observed in total services projects and the backlog increased by $1mm to reach $16mm.

- With respect to OpEx, SLP booked an R&D investment of $2.1mm, equivalent to 17% of revenue, while SG&A expenses amounted to $7.2mm, representing 61% of revenue. It pulled this to operating income of ~$900,000 yielding a 700bps operating margin, and, following interest and investment income, recognized earnings of $1.2mm, otherwise diluted EPS of $0.06.

- SLP finished the quarter with fairly robust liquidity, with $132mm in cash and short-term investments, and no outstanding debt. As such, the company has also implemented a share repurchase program, with an authorized repurchase of up to $50mm of outstanding common shares. It commenced an accelerated repurchase of $20mm in January.

- Management outlined a FY23E’ full-year revenue growth targeting 10%–15% YoY organic growth. On this, it aims for diluted EPS of $0.67 at the upper end of range.

Additional forensics

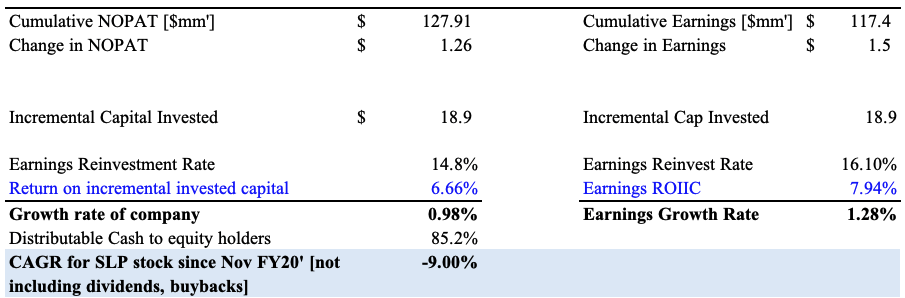

We identified earlier that SLP has been agnostic to growth over the last few years. This hasn’t been received well by the market, and investors have diverted capital to more selective opportunities offering the desired growth potential. Analysing this further, we calculated that, from August FY20′ to November FY22′, SLP generated a cumulative $128mm in NOPAT, on an additional growth of just $1.3mm in NOPAT over this time. Earnings growth has been at a similar pace [Exhibit 2]. Here, we used rolling TTM periods to provide a more extensive lookback window.

Exhibit 2. SLP cumulated NOPAT and earnings, growth, FY20–FY22′

Note: Rolling TTM periods are used to provide an 11 period lookback window, where each period is 12 months (Data: Author, using data from SLP estimates)

The return on invested capital per period has hovered ~7–8% over this time. To generate the $127mm in cumulative NOPAT, it had to invest an additional $19mm in capital to achieve that, illustrating a return on incremental invested capital of ~6.7%. Consequently, SLP’s growth has been a steady 1%. However, what’s intriguing, is that it only needed to reinvest ~15% of NOPAT [16% of earnings] to generate these numbers. We believe this leaves good headroom for the company to make additional investments to grow its bottom-line. Moreover, the company leaves ~85% of post-tax earnings distributable to equity holders, facilitating a $0.24/share annual dividend, and now, $50mm on-market buyback.

Exhibit 3. Lacklustre growth, but high distribution of cash flow to equity holders to balance the debate

Data: Author, using data from SLP estimates

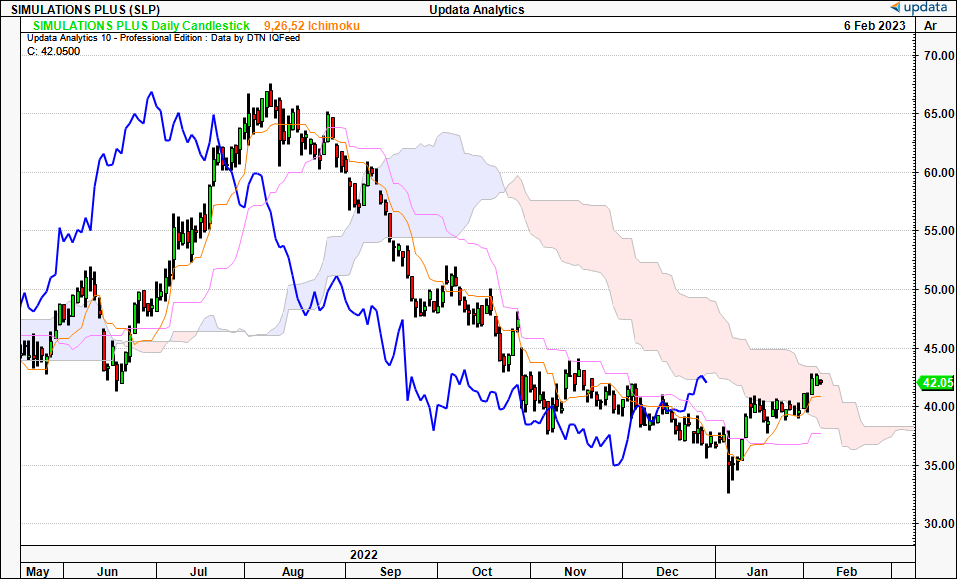

It is for these reasons that we see SLP potentially crossing up through the cloud with the lagging line in hot pursuit. We aren’t there just yet, but with further upside on the chart this could be a real possibility, and we are looking to this as a trend confirmation of our buy thesis. This is what has us at a speculative buy.

Exhibit 4. Punching up through the cloud, not quite in bullish territory at the moment

Data: Updata

Valuation and conclusion

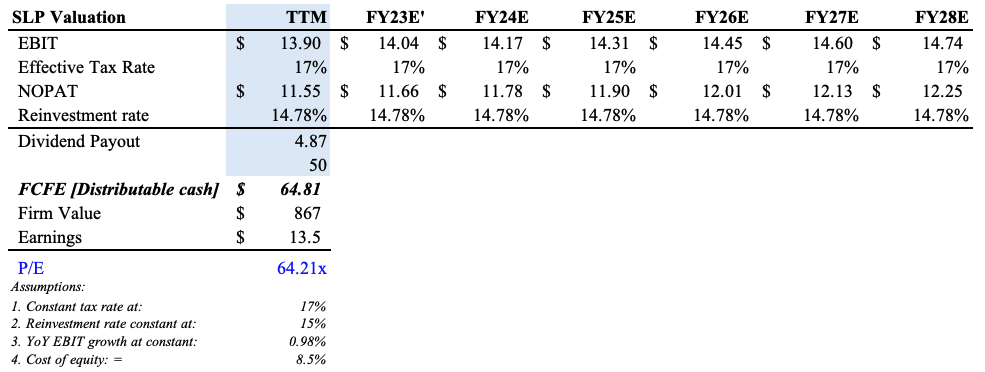

SLP is richly priced at ~65x forward earnings [non-GAAP]. However, given the calculations we discussed above, plus the dividend and buybacks, there’s a case to be made for this valuation. Presuming it can maintain a reasonably low reinvestment rate, plus, factoring an opportunity cost of capital of 8.5% [current S&P 500 forward earnings yield + current yield UST 10yr] we see the stock trading fairly at ~64.2x earnings. A pullback to $40 confirms our entry point. Note, this is still highly sensitive to the discount rate used.

Exhibit 5. Assuming SLP continues tight reinvestment, leaving high FCF to equity holders, this justifies high P/E

Data: Author’s Estimates

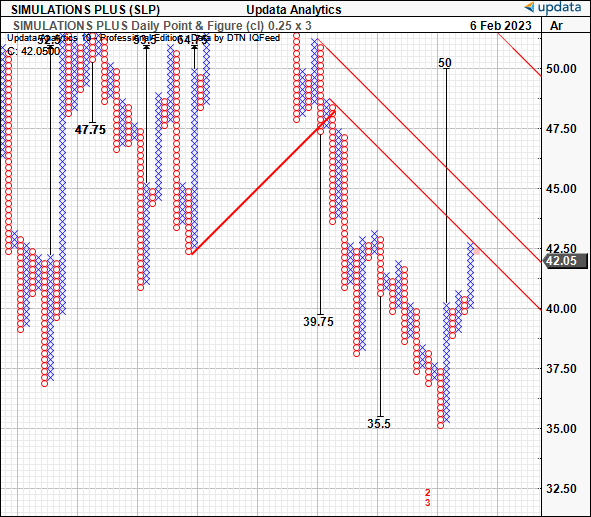

We also have upside targets to $50 from our point and figure studies giving us scope to add SLP as a speculative buy.

Exhibit 6. Upside targets to $50

Data: Updata

Net-net, we are initiating SLP as a speculative buy, eyeing upside targets to $50, around 20% return objective. Our findings indicate a potential differentiated offering that has potential to catch investor attention.

Note: There are many risks to this investment thesis. SLP is richly priced, regardless of our valuation and rationale behind this discussed above. The company has exhibited slow growth rates, and this may see it overlooked for more selective opportunities into the periods to come. Despite its differentiated offering, it is niche, and may not receive broad market recognition. Investors have also positioned more defensively in FY22’/23′ and therefore may continue to seek out defensive assets over risk assets. Given its size, the stock may endure wide volatility that doesn’t reflect market fundamentals. There is also a risk of liquidity, in that orders might not get filled at stipulated price, either buys or sells. Moreover, our valuation is sensitive to the inputs used, and utilizing a different hurdle rate changes the outcome substantially. Investors must recognize these risks before proceeding any further.

Be the first to comment