piranka/E+ via Getty Images

Thesis

I am bullish on Similarweb (NYSE:SMWB) stock as I believe the company will see sustained multi-year tailwinds from the demand for web-traffic and data analysis. The company’s stock is down more than 50% YTD and long-term investors might appreciate the share-price weakness as a buying opportunity. In the short-term, SMWB stock could definitely see further price depreciation, as the market’s bearish sentiment does not seem to have found a bottom yet. This, however, should have nothing to do with the company’s fundamentals, including an attractive value proposition and strong market opportunity. Based on an EV/EBITDA multiples valuation, I calculate a base-case target price of $21.24/share—indicating almost 200% upside. I initiate with a Buy recommendation.

About Similarweb

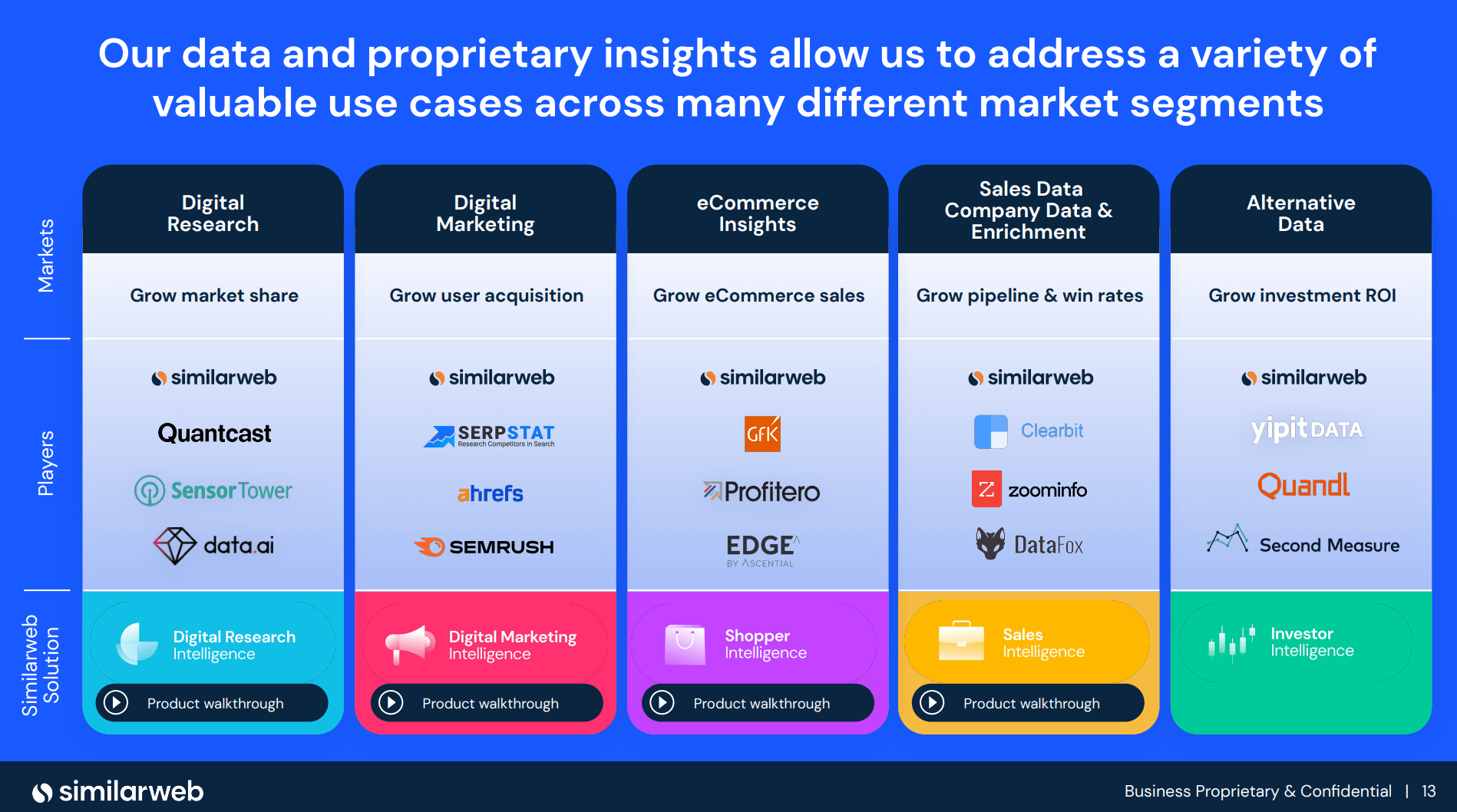

Similarweb is an Israel-based data analysis and web-traffic intelligence company founded in 2007. Similarweb operates a platform that allows companies to discover and analyze website traffic insights, such as keywords, traffic volume, engagement metrics, etc. While alternative platforms such as Salesforce and Google Analytics mainly provide insights to the company’s own data, Similarweb also gives insights on competitors, partners and prospective customers. This offers companies the opportunity to support multiple high-value use-cases such as digital research and digital marketing.

Similarweb Investor Presentation

Similarweb’s Opportunity

Similarweb’s value proposition is poised to benefit from a multiple-year tailwind from the demand for data-intelligence and website traffic analysis. At this point, it is widely recognized that digital presence and strength is a key-driver for business success. At the same time, the value for digital data insights to fuel digital strength is undisputed. That said, since Amazon’s Alexa Web has closed operations in May 2022, Similarweb is well-positioned to become the leading address for companies to discover and anlayse web-traffic insights.

According to the company’s management team, Similarweb’s total addressable market is currently estimated at $34 billion. The company derives this measure by multiplying the number of qualified customers (companies meeting certain qualifications) with Similarweb’s own insights on the market-size weighted contract value. As of March 2022, Similarweb serves more than 3,700 customers, including notable brands such as Google, Adobe, Roche, Walmart, Adidas, DHL and more.

Similarweb Investor Presentation

The company’s biggest competitor is Semrush (SEMR). Personally, I have used both Semrush and Similarweb and feel the companies value-propositions are quite similar. I argue Similarweb might have an advantage from a user-friendly perspective, while Semrush’s data-insights are slightly ahead. But the overall similarity in value proposition is something that investors should note and monitor. If the two companies were to merge, which is plausible, I would turn ultra-bullish on the combined entity.

Financial Performance

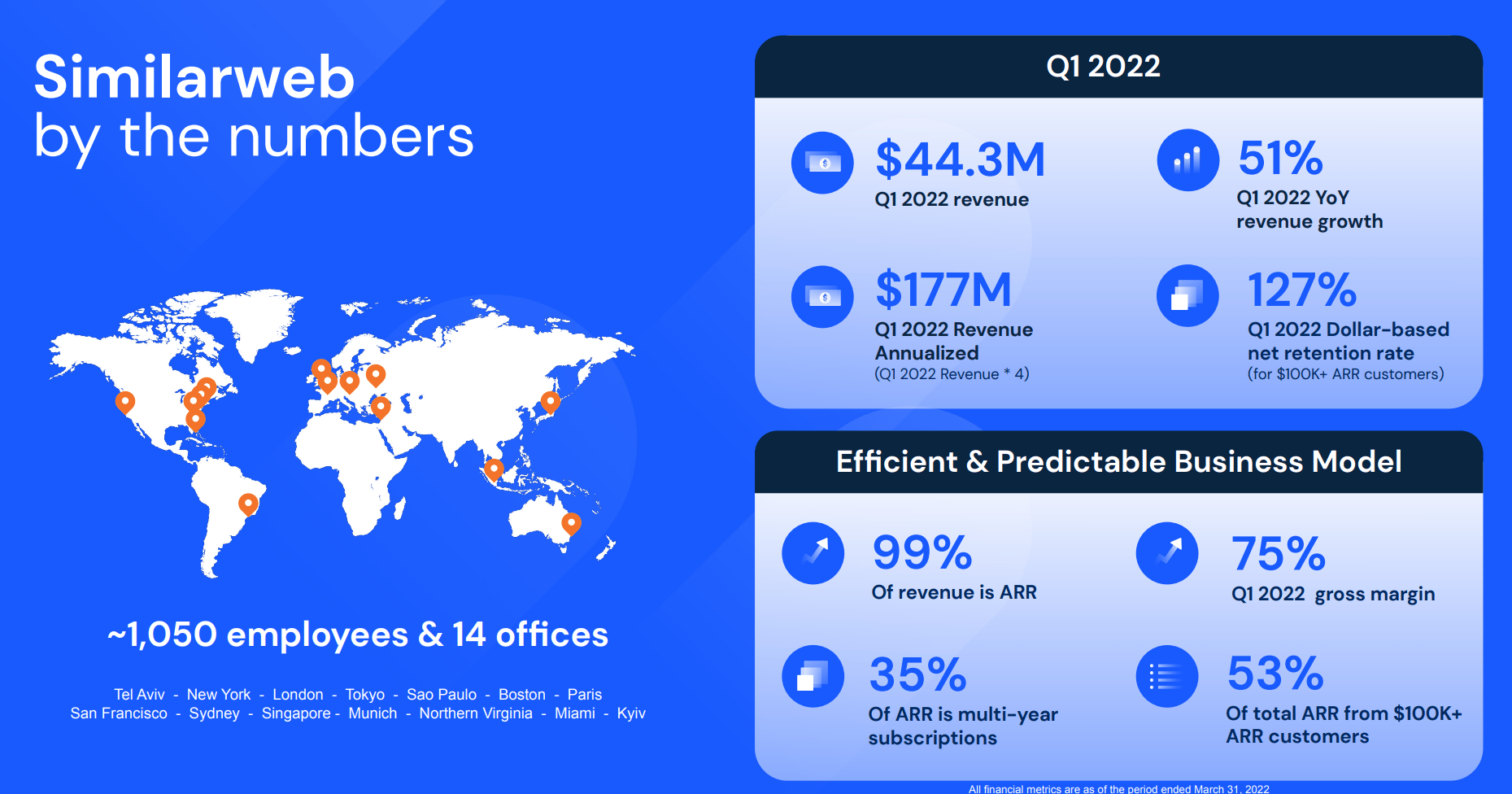

Similarweb’s business monetization is accelerating as the company recorded a year-over-year revenue increase of more than 45%–jumping from $93 million in 2020 to $137.6 million in 2021. Moreover, the company’s Q1 2022 results recorded an even stronger quarter-over-quarter increase of 51% ($177 million annualized). Most notably, 99% of the revenues are classified as recurring revenues, with approximately 35% based on multi-subscriptions. Operating income, however, is still negative as the company is investing in customer acquisition and business development. In 2021, Similarweb generated a $105.9 million gross-profit (>70% margin) and a loss from operations of $66.1 million, as the company was spending $127.6 million in marketing/sales and $44.4 million in R&D.

Similarweb’s balance sheet is strong. By the end of 2021, the company recorded $128.9 million of cash and short-term investments and no debt. Cash from operation was negative at $27.6 million. That said, Similarweb could approximately sustain the same burn-rate for five more years, before new funding would be required. But even then, given the company’s no-debt position, Similarweb should easily be able to raise debt funding—without diluting shareholders.

How analysts see it

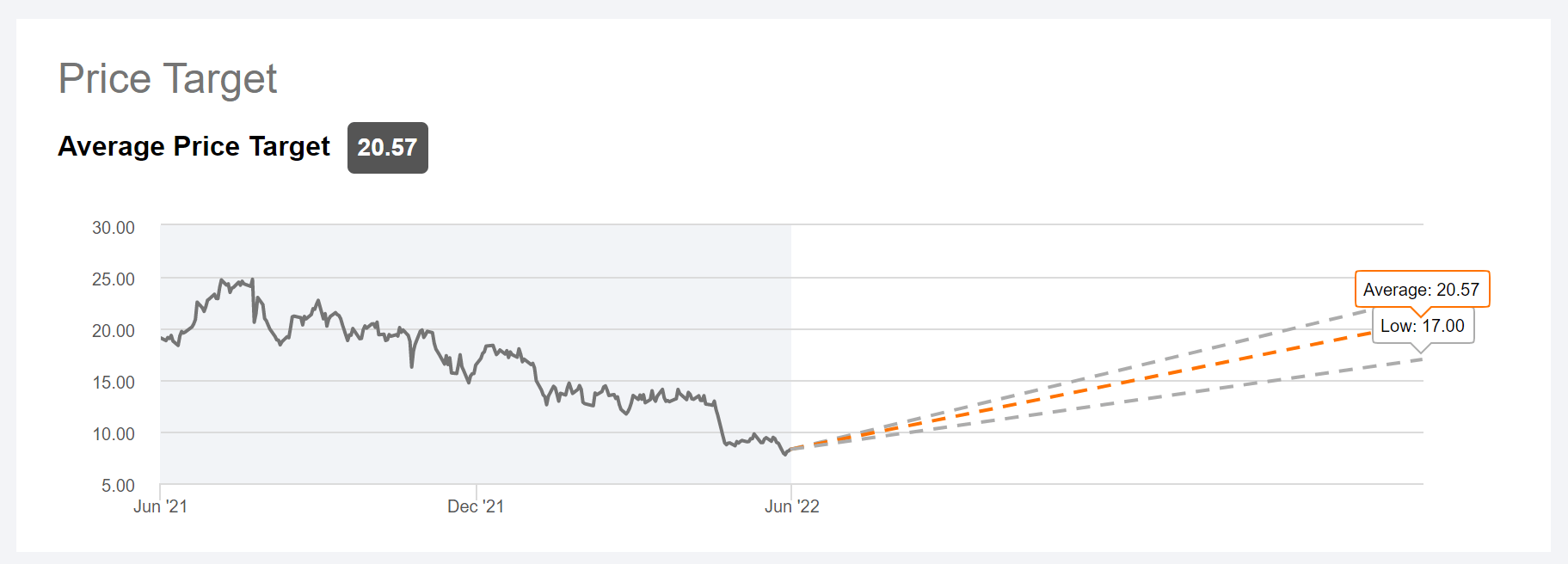

In general, analysts are very bullish on Similarweb, with an average consensus target price of $20.57/share. Most notably, this target price would indicate approximately 200% upside. According to the Bloomberg Terminal, as of June 2022, analyst see Similarweb’s revenues in 2022, 2023 and 2024 at $196.37 million, $266.38 million, $351.67 million, respectively. This would equal a 3-year CAGR of more than 20%. Respectively EPS are estimated at $-1.15, $-0.97 and $-0.61 for the same period.

Seeking Alpha

Valuation

To value Similarweb stock, I propose using multiples, as the company is not yet profitable and visibility for profitability remains limited. However, please note that I am not a fan of multiples valuation. Thus, this section should only be regarded as a reference point to anchor a valuation estimate. That said, I suggest applying the average 1-year EV/EBITDA multiple of the two industry leaders Similarweb (x3.4) and Semrush (x5.9), equal to x4.65. If we apply this multiple for Similarweb’s 2024 revenues of $351.67 million, we calculate an EV of $1.64 billion and an equity value of $1.76 billion, or $21.24/share.

Risks

I would like to highlight the following downside risks that could cause Similarweb stock to materially differ from my price-target:

First, Similarweb is writing losses. There is no guarantee that the company will achieve significant profitability in the next few years, if ever.

Second, a worsening macro-environment including inflation and supply-chain challenges could negatively impact Similarweb’s customer base. If challenges turn out to be more severe and/or last longer than expected, the company’s financial outlook should be adjusted accordingly.

Third, investors should monitor competitive forces in the industry, as I have highlighted the similarity to Semrush. If competition increases more than what is modelled by analysts, profitability margins and EPS estimates for Similarweb must be adjusted accordingly.

Fourth, much of Similarweb’s share price volatility is currently driven by investor sentiment towards risk and growth assets. Thus, investors should expect price volatility even though Similarweb’s business outlook remains unchanged.

Finally, inflation and rising-real yields could add significant headwinds to Similarweb’s stock price, as the higher discount rates affect the net-present value of long-dated cash-flows.

Conclusion

Balancing the risk/reward for Similarweb, the company deserves a buy recommendation. I believe Similarweb is poised to benefit from an accelerating demand of high-quality web-traffic analysis. Moreover, the stock appears cheaply valued, as my valuation framework based on EV/EBITDA multiples indicates almost 200% upside. I assign a Buy recommendation with a base-case target price of $ $21.24/share.

Be the first to comment