ratpack223

Introduction

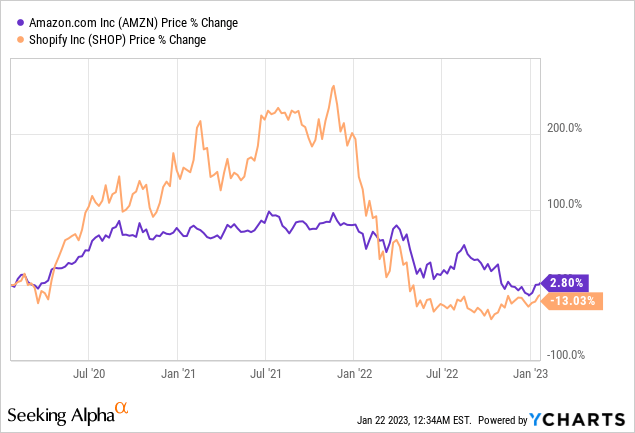

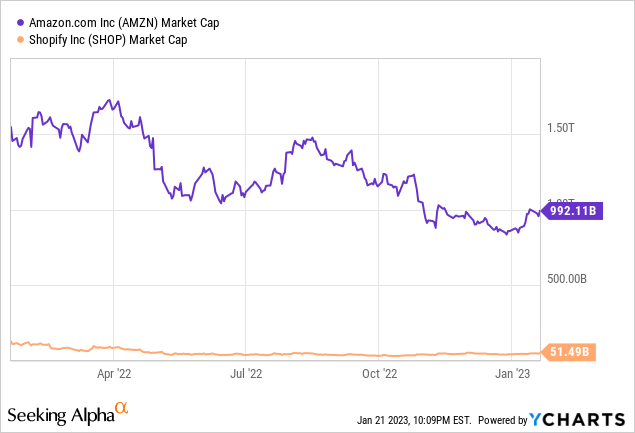

Over the last couple of decades, Amazon (AMZN) and Shopify (NYSE:SHOP) have evolved into iconic e-commerce companies by disrupting the traditional retail industry with technology. While both of these stocks have generated incredible returns for their shareholders for several years, 2022 was a terrible year, with Amazon and Shopify shares losing ~50% and ~75% of their value.

At this point, both Amazon and Shopify have given back the entirety of their respective gains from the start of the COVID-19 pandemic. In my view, three major factors drove this reset in valuations:

- A reversal in e-commerce penetration

- Elevated inflation

- Higher interest rates (quantitative tightening)

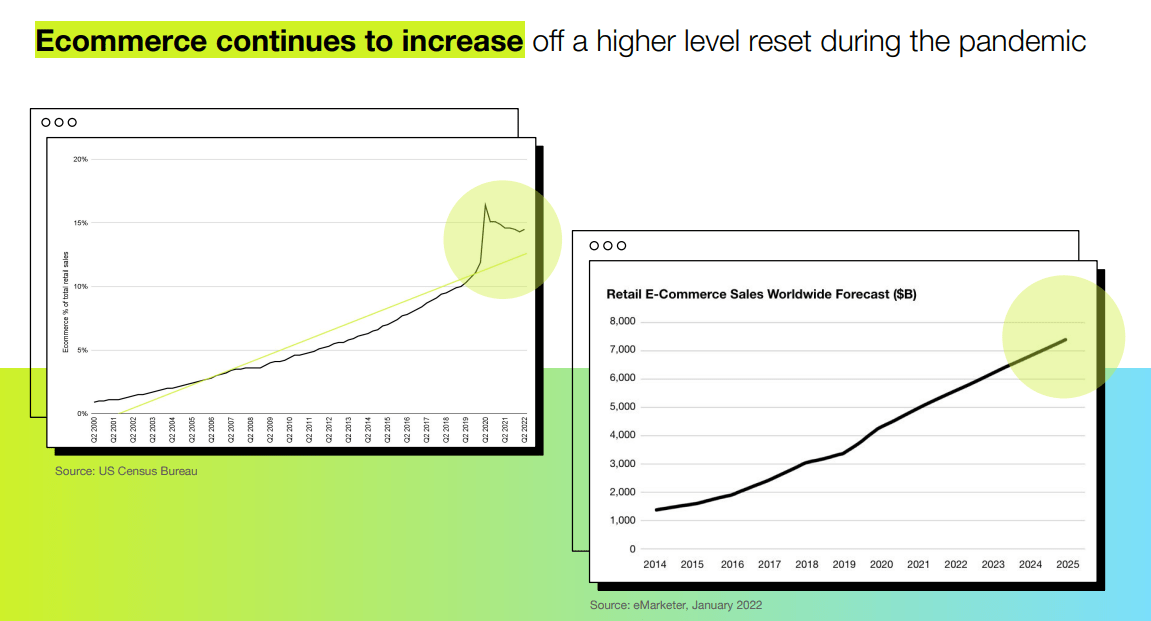

The COVID-19 pandemic led to a sharp acceleration in e-commerce adoption trends as consumers were trapped in their homes, and merchants had to embrace technology to reach them. Naturally, e-commerce enablers like Amazon and Shopify saw a massive jump in demand for their products and services. While e-commerce penetration of total retail sales (currently ~15%) is set to increase over the coming years, the pull forward caused by the pandemic reversed somewhat in the post-pandemic world during 2021-22 as the economy re-opened and consumers returned to physical stores.

Shopify Investor Relations

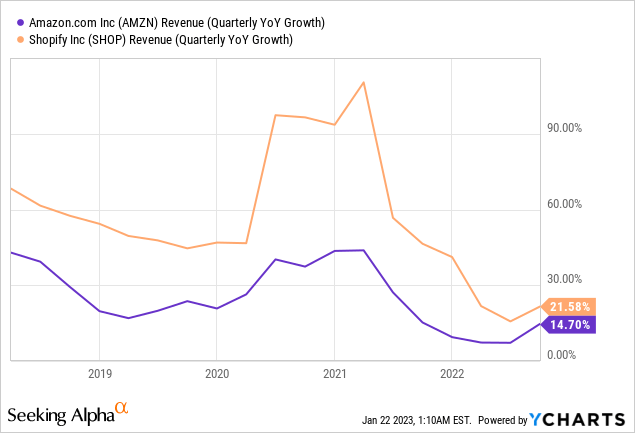

And as a result of this reversal in e-commerce penetration, both Amazon and Shopify have suffered a drastic slowdown in revenue growth:

In addition to a reversal in e-commerce penetration, elevated inflation levels and higher interest rates have contributed to this growth slowdown.

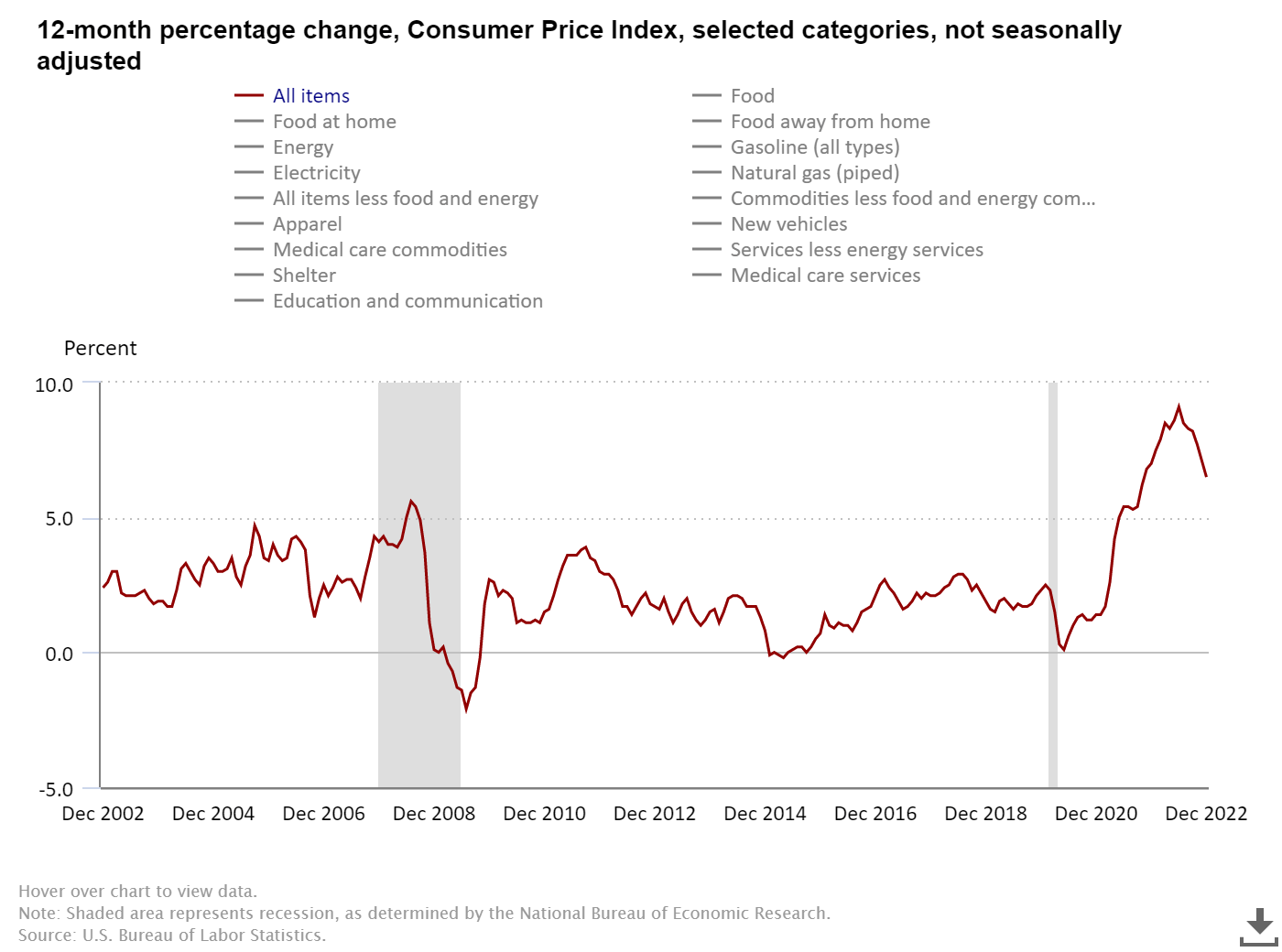

As prices of everyday essentials shot up in the aftermath of a liquidity boom, consumers saw their spending power deteriorate as stimulus money ran out over the last few quarters. The labor market is tight, and wages have been rising, but they haven’t kept up with the pace of inflation. And these inflationary pressures have caused a decline in discretionary spending.

bls.gov

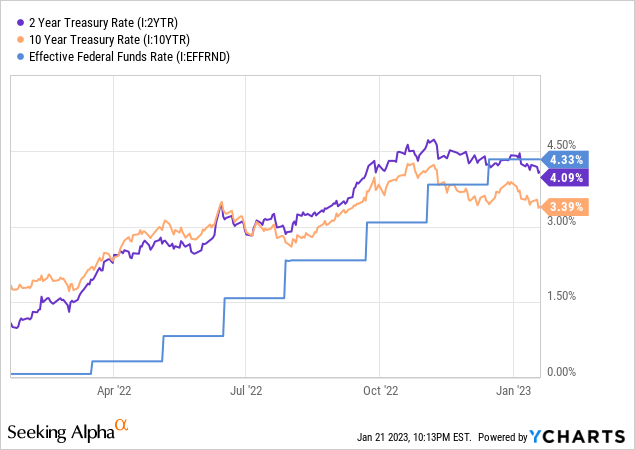

And as you know, higher interest rates, i.e., higher financing costs, temper consumer demand. In addition to creating demand pressures, elevated inflation levels reduce the value of future free cash flows for investors, and higher interest rates result in a higher discount rate (lower net present value for a given stream of cash flows) in discounted cash flow modeling.

As you may have observed, inflation has been cooling off for months now (December CPI: -0.1% m/m), and interest rates (especially long-duration treasury yields) are moderating rapidly (10-yr treasury yield is down from recent highs of ~4.3% to ~3.4%).

While two of the biggest macro headwinds for technology stocks – inflation and interest rates – are turning into tailwinds. And as we saw earlier, e-commerce continues to increase off a higher level reset during the pandemic. Suddenly the recent run-up in Amazon and Shopify shares makes some sense, right?

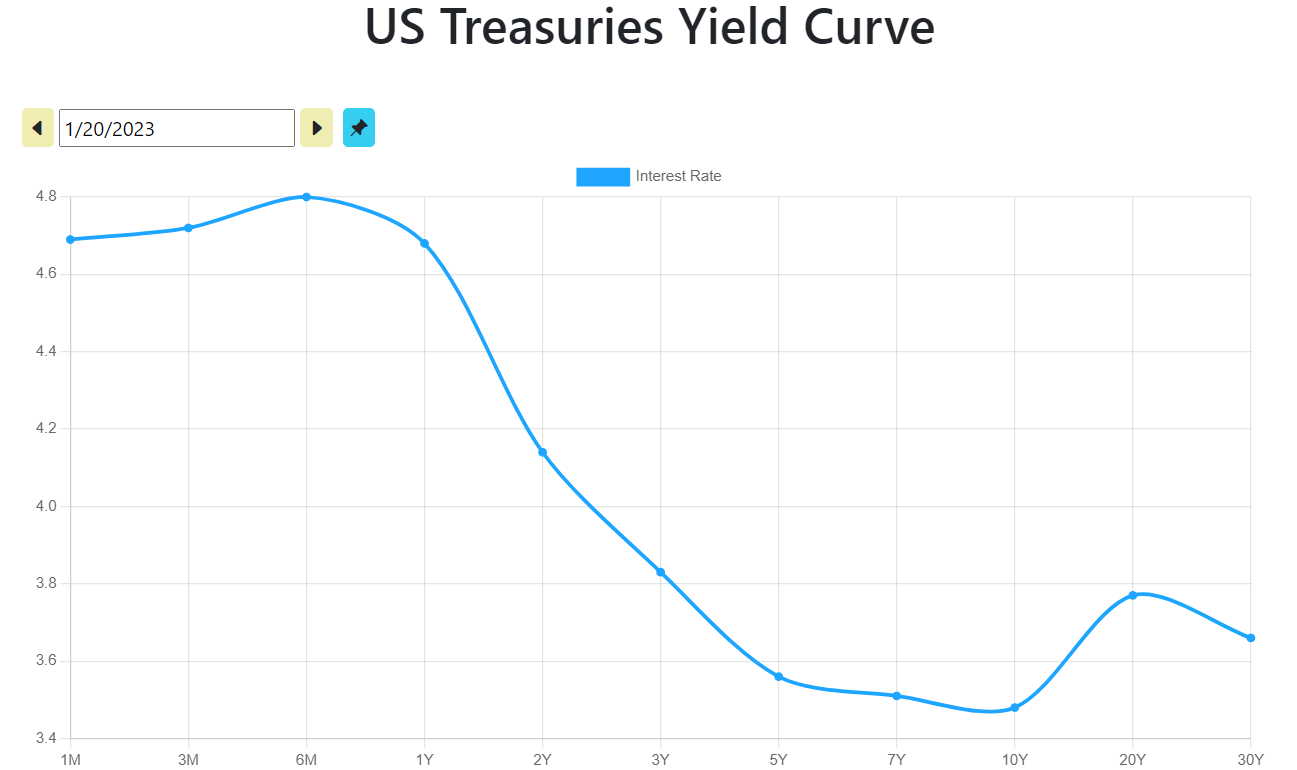

While tech stocks (and equity markets in general) have kicked off 2023 with unbridled optimism, the dark clouds of a recession loom large over us. For months, the bond market has been screaming – “Recession Ahead” – through a deeply inverted yield curve. And this curve is set to get steeper with the Fed set to hike rates again at their next FOMC meeting on February 1.

ustreasuryyieldcurve

Conference Board

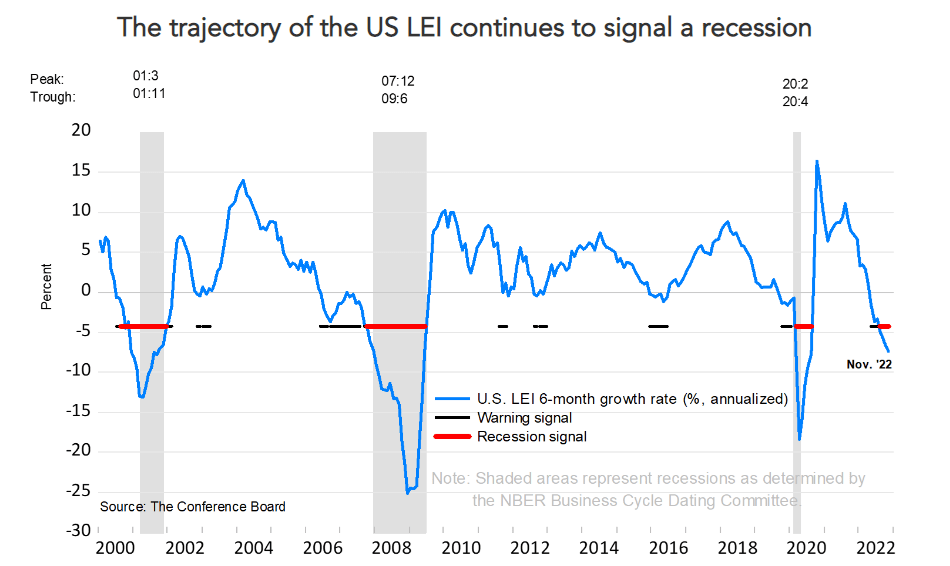

The macroeconomic environment remains uncertain, with leading economic indicators pointing towards an impending recession. As you may know, US retail sales have declined in the last 5 out of 6 monthly retail sales reports. And the outlook for e-commerce in 2023 is not that rosy:

As I see it, inflation is collapsing, and consumer demand is going with it.

So, heading into a potential recession, which is the better buy among Amazon and Shopify?

Before we answer this question, let us see if comparing these two stocks and businesses against each other makes sense.

Going by market capitalization, Amazon is roughly ~20x the size of Shopify! And as we will see in a bit, Amazon’s retail ecosystem does roughly ~80x Shopify’s revenue.

The massive gulf in scale between Shopify and Amazon would make one think that they are not real competitors; however, let’s compare these businesses first before reaching any conclusions.

Is Amazon A Direct Competitor To Shopify?

Amazon.com is the largest e-commerce marketplace in the United States, with a large moat embedded in its retail ecosystem, i.e., 1P-3P marketplace, prime subscription, digital advertising, logistics, and numerous fintech solutions like Buy with Prime.

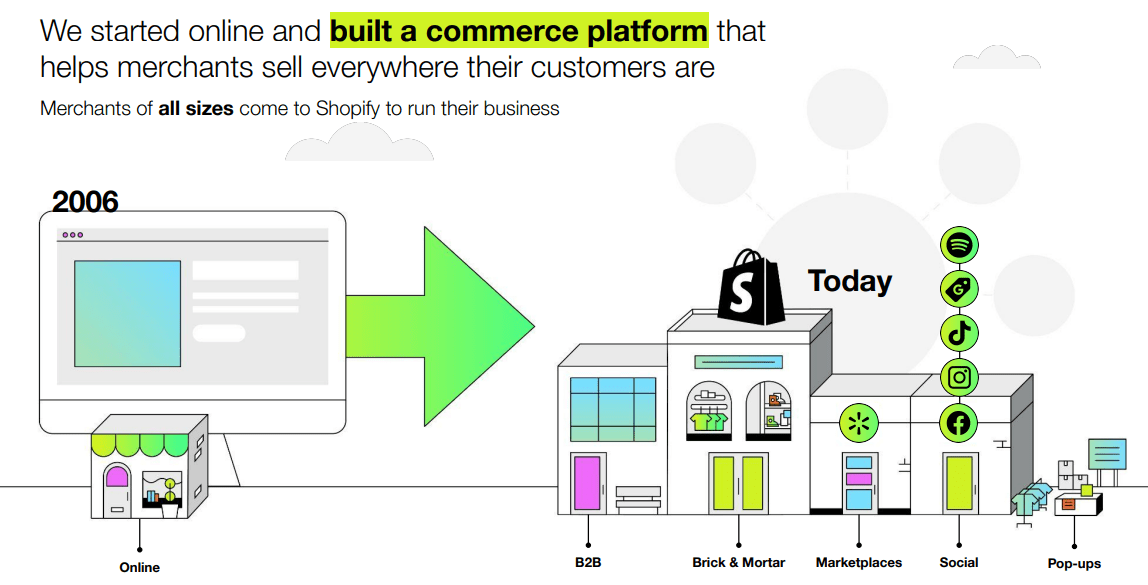

On the other hand, Shopify is the retail operating system for merchants, with a growing presence on the consumer side (through the Shop app). Over the years, Shopify has transformed into an omnichannel commerce enablement platform that allows merchants to sell everywhere their customers like to shop. By signing up on Shopify’s platform, merchants can sell through multiple channels, including direct-to-consumer from the merchant’s own website, marketplaces like Amazon, social media platforms like Facebook (META), Instagram, and Tiktok, and even physical stores!

Shopify Investor Relations

Shopify Investor Relations

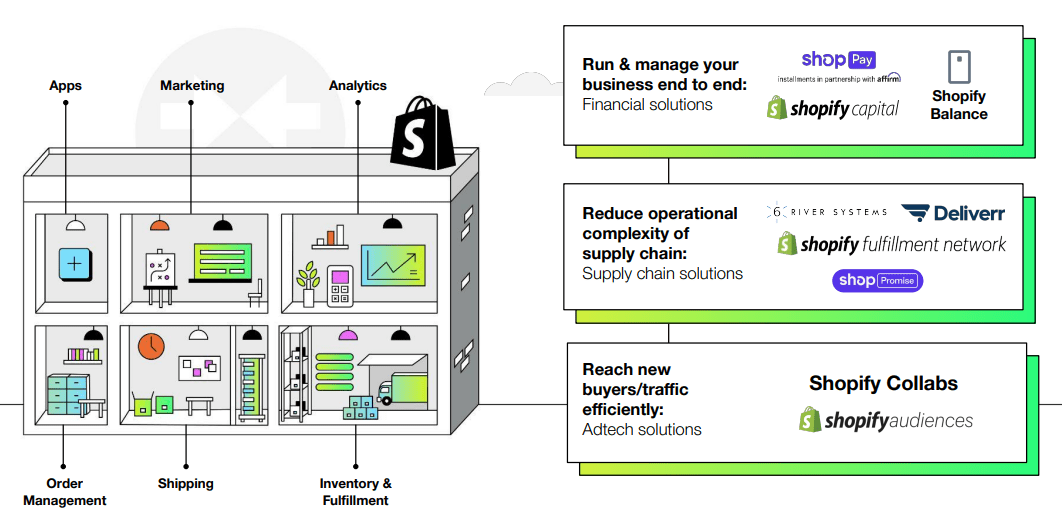

Essentially, Shopify provides the critical, end-to-end infrastructure merchants need to run their omnichannel businesses. And Amazon’s marketplace is one of those channels. According to data from Marketpulse, 40% of Shopify’s merchants sold on Amazon in 2021. While Amazon’s marketplace moat is clear and obvious, Shopify has also carved out a nice little moat for itself with its merchant-focused commerce enablement platform (and third-party developer ecosystem). I don’t know if you know this, but Amazon shut down its Shopify rival – Amazon Webstore – back in 2015 and referred customers to Shopify.

Since then, both Amazon and Shopify have come a long way, and lines are now starting to get blurred with Shopify building out its fulfillment network (which is a very costly adventure) to compete with Amazon. In response, Amazon has been opening up its walled garden by rolling out services like third-party logistics and fintech solutions like Buy With Prime to all merchants.

If we think about the retail industry as one big pie, Amazon & Shopify are approaching the same market opportunity with different strategies. Will Amazon’s consumer-focused retail ecosystem beat Shopify’s merchant-focused commerce enablement platform?

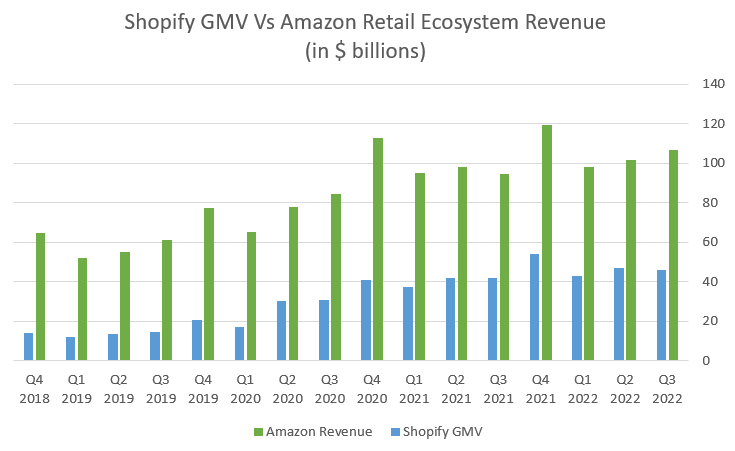

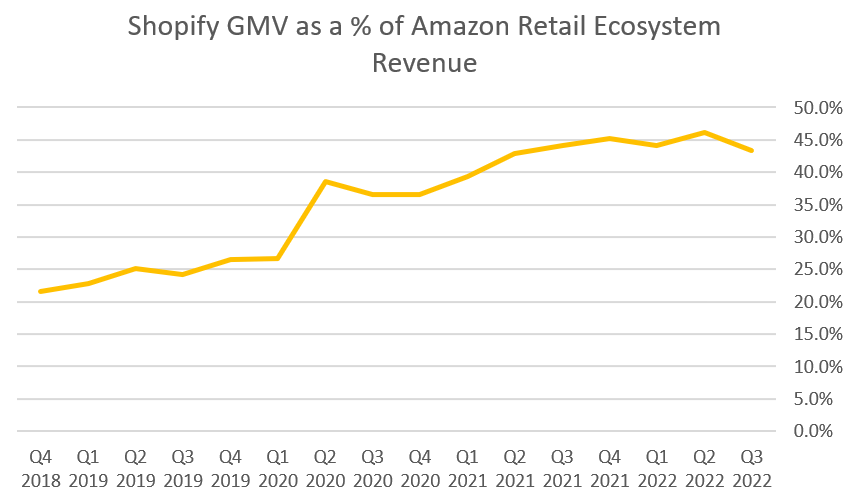

Honestly, I don’t know how this battle will play out as there’s not enough evidence to suggest a clear winner here. Shopify’s GMV has been growing rapidly against Amazon’s retail ecosystem revenue, suggesting a market share grab away from Amazon.

Author

Author

Now, I understand that looking at Shopify’s GMV against Amazon’s retail ecosystem revenues is like comparing Apples to Oranges. Unfortunately, we do not have Amazon’s exact GMV figures, and all I am trying to do here is decipher a reliable trend.

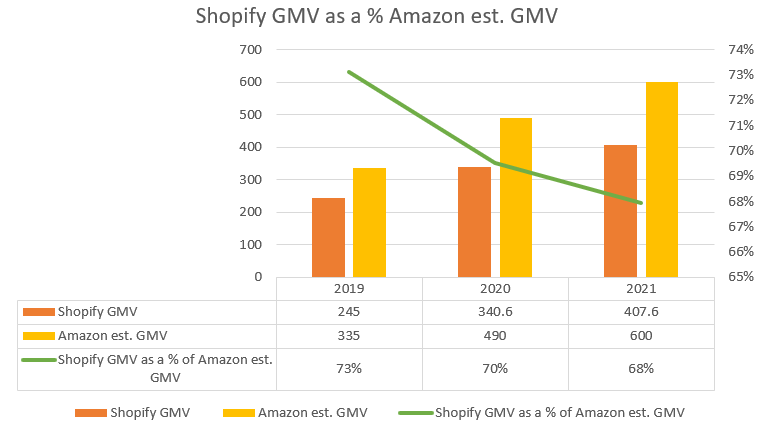

According to Marketplacepulse, Amazon’s GMV reached $600B in 2021, with 3P business making up nearly two-thirds of this GMV figure. And going by these estimated figures, you can see that Shopify’s GMV as a percentage of Amazon’s GMV is actually trending down, i.e., Amazon’s GMV is growing faster than Shopify’s GMV. Since the GMV data for Amazon is an estimate, and information for 2022 is not available, I am not sure who’s winning at this point.

Author, Data sourced from Marketplacepulse

Both Amazon and Shopify have their strengths and weaknesses, and in my view, co-existence is the most likely long-term outcome of this battle. The good thing here is that e-commerce is likely to become a much bigger portion of total retail sales in the coming years and decades, so both Amazon and Shopify have ample room to grow side by side.

AMZN and SHOP Stock Key Metrics

So far, we have compared Amazon and Shopify based on the nature of their businesses. Now, let’s take a look at some numbers.

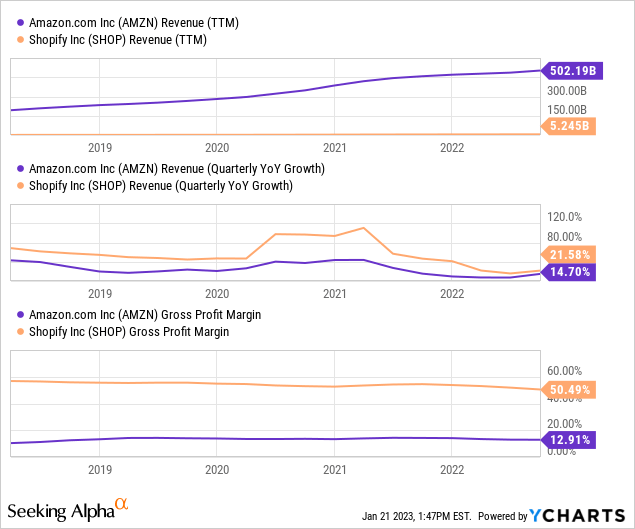

Due to having fundamentally different business models, Amazon and Shopify’s business metrics are not really comparable. That said, numbers show that Amazon is operating at a far bigger scale than Shopify, and the latter is growing faster with much superior gross margins.

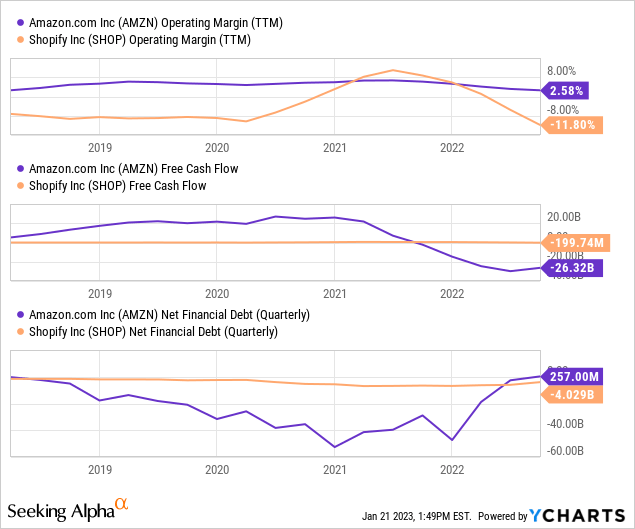

The sharp acceleration in e-commerce adoption prompted Amazon and Shopify to enter big CAPEX spending (investment) cycles; however, the post-pandemic reset in e-commerce trends has resulted in both companies suffering vicious margin contractions. In the last twelve months, Amazon recorded a negative free cash flow of -$26B, and Shopify burned nearly $200M of its cash.

Now, a lot of the pain in Amazon’s retail business is masked by its primary profit center – Amazon Web Services [AWS] (cloud). Please note that AWS is running at an ARR of ~$80B, and it is still growing at ~25-30% y/y. Additionally, Amazon’s digital advertising business is scaling up nicely (despite a broad decline in advertising budgets due to a challenging macroeconomic environment). With Amazon exiting a heavy spending cycle in 2023 (with inflationary pressures falling off), Amazon is set to deliver $20B+ in free cash flow this year on the back of continued strength in AWS and digital ads.

Shopify doesn’t have cloud business to support its growth, and yet, it is embarking upon a costly adventure by building its fulfillment network. Honestly, I don’t think Shopify can genuinely compete with Amazon on logistics for another decade or two (if ever). Fortunately, Shopify has $4B in net cash, and as the company reels in some of its operating expenses, the margins should improve in the near to medium term. That said, Shopify looks like a risky stock to own heading into a potential recession, whereas Amazon appears to be a safe haven.

Are These Stocks Fairly Valued?

To answer this question, we will run AMZN and SHOP through our proprietary equity valuation tool – TQI Valuation Model.

1. TQI’s Fair Value and Expected Returns for Amazon, Inc

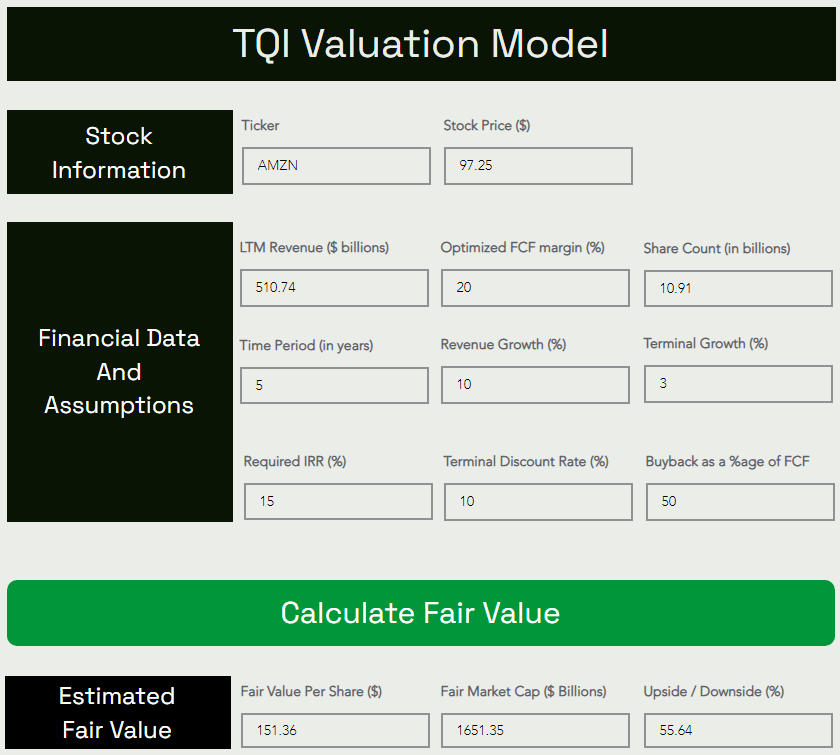

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

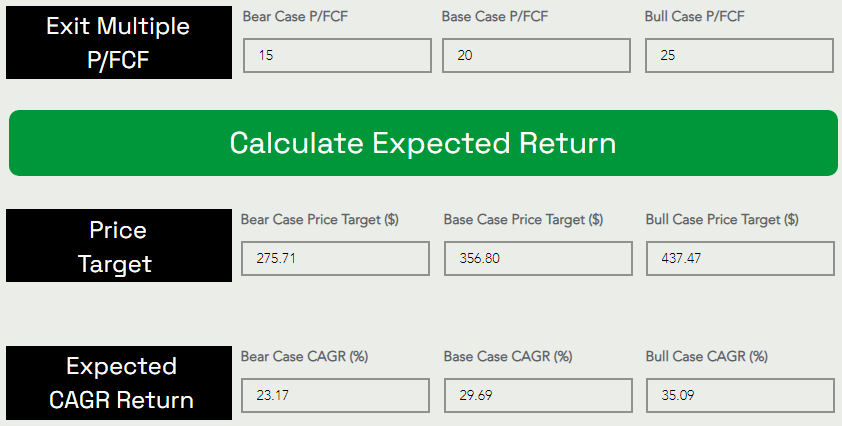

According to TQI’s Valuation Model, Amazon is worth $1.65T (or $151.36 per share), which means the stock has an upside of ~55% to its fair value. With 5-yr expected CAGR returns of ~29.7% being much greater than my investment hurdle rate of 15%, I think Amazon offers an asymmetric risk/reward opportunity for long-term investors.

To get more details about this valuation, refer to my latest note on Amazon:

Alright, now let’s take a look at Shopify’s absolute valuation.

2. TQI’s Fair Value and Expected Returns for Shopify, Inc

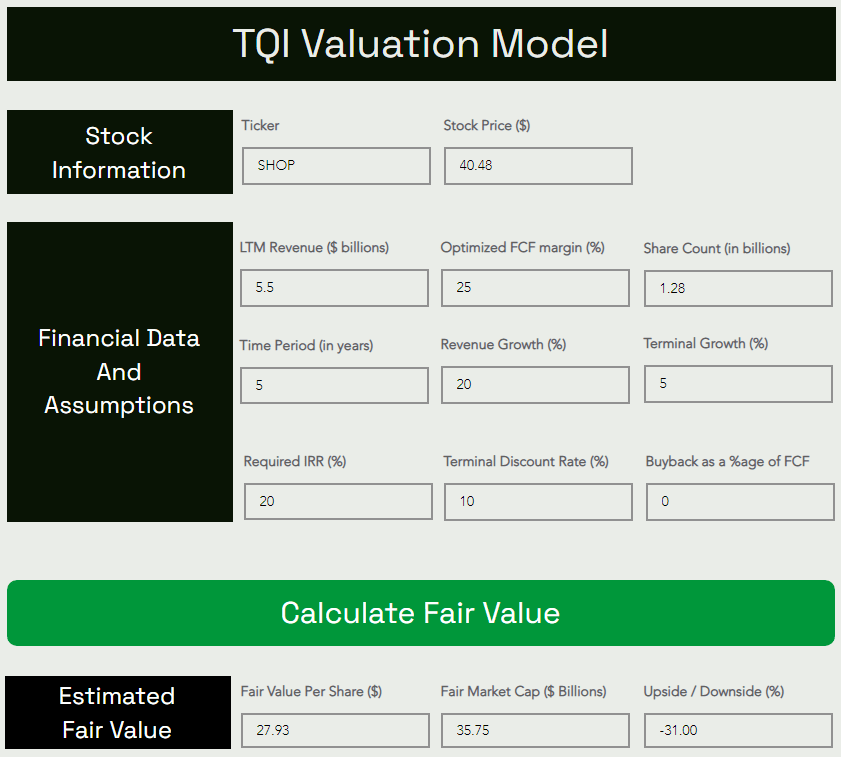

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

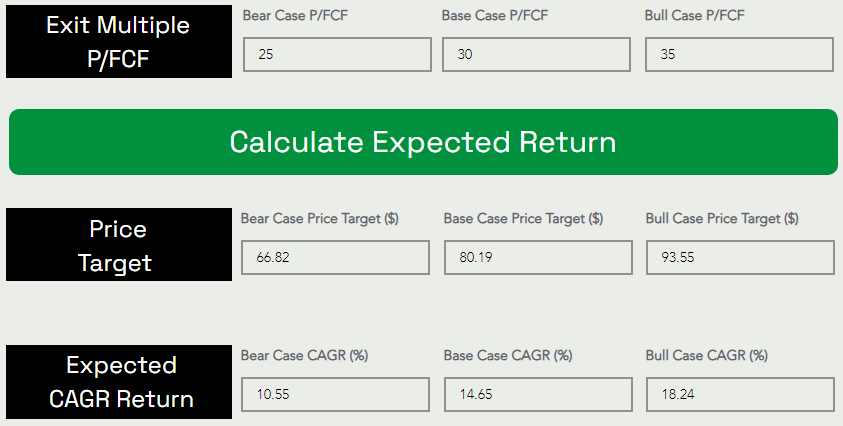

According to TQI’s Valuation Model, Shopify is worth $35B (or $28 per share), which means the stock has a downside of ~30% to its fair value. With 5-yr expected CAGR returns of ~14.65% being equivalent to my investment hurdle rate of 15%, Shopify is not an ideal buy at this time.

Analyzing Technical Charts and Quant Factor Grades For AMZN and SHOP

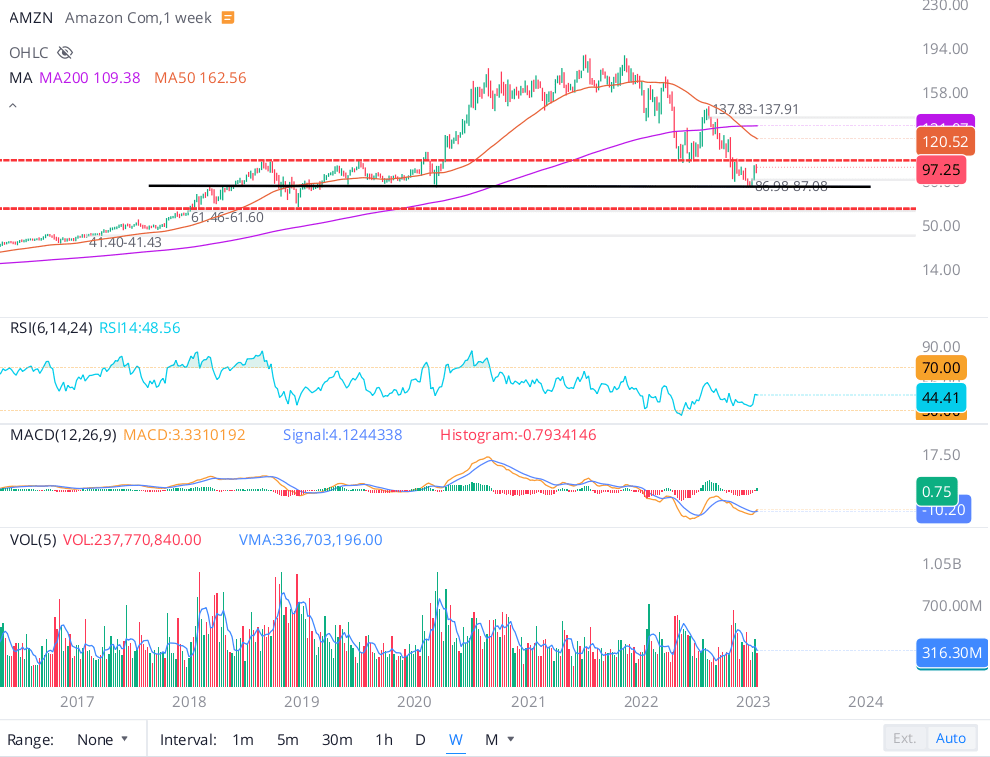

As pointed out in my previous note, Amazon’s stock held multi-year support at $80 and bounced off this level. After a sharp 16%+ YTD bounce, Amazon looks primed to re-test the $100-$105 range in the coming weeks. If the stock fails to break this level, I would expect it to remain rangebound in the $80-$100 range.

WeBull Desktop

If the support at $80 were to break down, the $60-$65 range would be the next notable support level. While the downtrend in Amazon’s stock is firmly intact, and the stock may go lower in the near term, I think the risk/reward for long-term investors getting in at current levels is highly favorable.

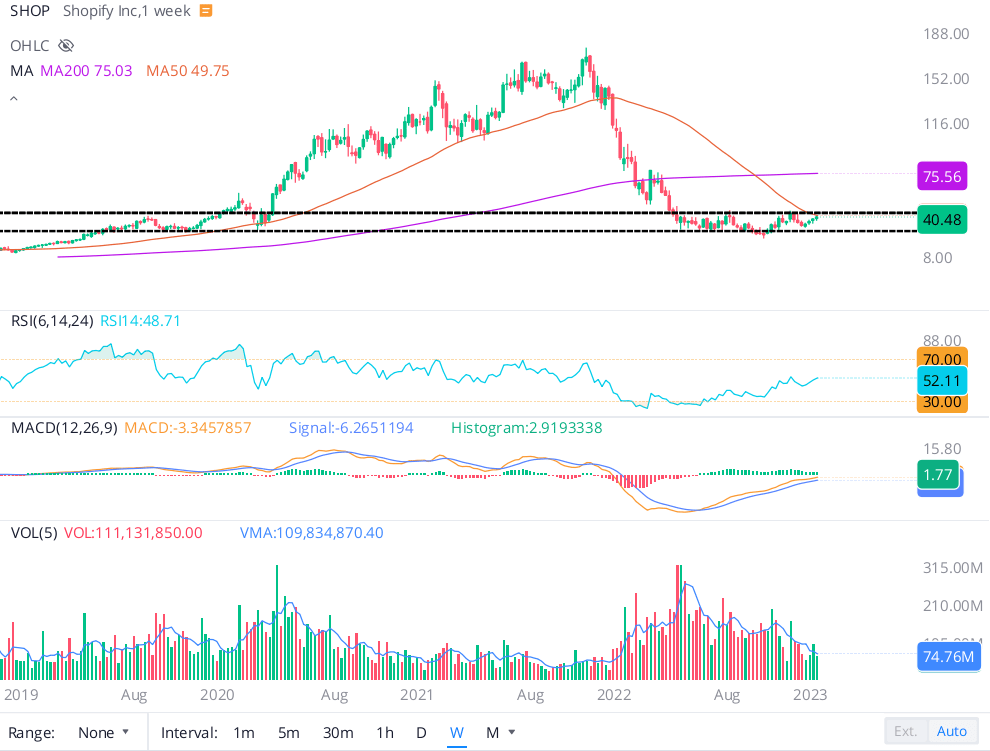

In Shopify’s case, the drawdown has been far worse. However, after suffering a catastrophic decline of ~85% from its late 2021 highs of ~$175 per share in 2022, Shopify’s stock seems to have stabilized in a Stage-I base formation pattern. And in recent weeks, Shopify’s stock has rallied up to the higher end of this base at ~$40 amid a bounce in tech stocks.

WeBull Desktop

While Shopify’s valuation and business fundamentals don’t suggest a move higher from here, the technical setup is finely poised. A break above $45 could lead to a move higher into the $60-$70 range. However, I am staying skeptical of the recent rally in Shopify’s stock, as a rejection at the top end of the base (~$45) is very much in play. Such a rejection could trigger a re-test of the lower end of the base in the mid $20s. At this point in time, the risk/reward for investors (from a technical perspective) is unfavorable.

Alright, now let’s evaluate Amazon and Shopify’s quant factor grades and analyst ratings.

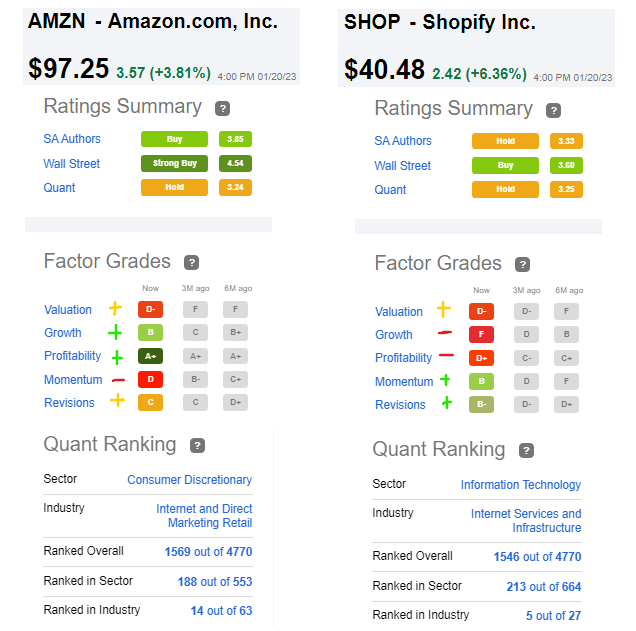

According to SeekingAlpha’s Quant Rating system, Amazon and Shopify are both rated as “Hold” with a nearly identical score of 3.25/5. While SA Authors seem to be in agreement with Shopify’s quant factor grades, they are bullish on Amazon’s stock. And as you can see below, Wall Street analysts are bullish on both stocks.

SeekingAlpha Quant Ratings

Since Amazon and Shopify fall under different sectors, their quant factor grades (relative measures) are not comparable. However, both sets of grades individually seem just about right. While Amazon and Shopify are rated as “Hold” by SA’s quant rating system, I think Amazon is a better buy than Shopify as its fundamentals-related quant factor grades (Growth, Profitability, and Revisions) are better than Shopify.

Based on a mix of fundamental, technical, quantitative, and valuation analysis, Amazon is clearly the better buy right now.

Final Thoughts: Is AMZN or SHOP Stock A Better Long-Term Buy?

Amazon and Shopify are operating in the same playground (or industry), i.e., e-commerce; however, they are not direct competitors as Amazon is a marketplace and a retailer, whilst Shopify is neither a marketplace nor a retailer. Moreover, AWS (Amazon’s cloud business) is the major profit center at Amazon, and it makes up a big chunk of Amazon’s intrinsic value. Hence, Amazon and Shopify are not comparable businesses or stocks.

That said, we evaluated both companies on the merits of their respective businesses. And here’s a summary of this comparison:

| Current Price | TQI’s Fair Value Estimate | TQI’s 5-YR Expected CAGR Return | Status | |

| Amazon (AMZN) | $97.25 | $151.36 | 29.69% | Undervalued |

| Shopify (SHOP) | $40.48 | $27.93 | 14.65% | Overvalued |

Source: The Quantamental Investor

Clearly, Amazon is the better buy at current prices. Now, Shopify is a great company, and I think it is the only player that can realistically dethrone Amazon from the pedestal of the e-commerce space. However, Shopify’s 5-yr projected returns fall short of my investment hurdle rate, and this is why I am not enthusiastic about the stock at current levels.

I am a buyer of Amazon, but to be frank, my investment thesis is centered around Amazon’s AWS (cloud) and Ads (digital advertising) businesses (not on its retail business). To learn more about my investment thesis for Amazon, refer to TQI’s detailed research coverage on Amazon.

Key Takeaway: I rate Amazon (AMZN) a “Strong Buy” at $97.25 and Shopify (SHOP) “Neutral/Hold” at $40.48

As always, thank you for reading, and happy investing. Please feel free to share any questions, concerns, or thoughts in the comments section below.

Be the first to comment