Joe Raedle

Shortly after its 2015 IPO, I wrote an article on SA with a skeptical view of Shake Shack (NYSE:SHAK) shares as irrational exuberance took hold of restaurant stocks. With the stock down 30% since 2015 and 67% since its 2021 peak, I decided to revisit the investment merits of Shake Shack.

While Shake Shack has grown its footprint from just 31 fully owned and operated domestic locations (and 32 licensed international locations) at the time of its IPO to 230 domestic owned restaurants (and 172 licensed international locations), growth in EBITDA and operating cash flow has been elusive.

In today’s article, I weigh the positives and negatives of an investment in Shake Shack.

Positives

To be sure, there are a few things to like about Shake Shack as an investor including:

- Potential for continued restaurant openings. At just 230 domestic locations, there is room for Shake Shack to potentially double or triple its restaurant count.

- Proactive use of technology – Shake Shack is a leader in making use of digital tools in operations. As shown below, over the past five quarters, digital sales have comprised 36-42% of Shake Shack sales in any given quarter. in addition to mobile app ordering, Shake Shack has aggressively employed in-restaurant iPad/kiosk ordering capabilities. Not only does this reduce the amount of in-restaurant labor (particularly important given rising wage costs) but it also allows for a customized ordering experience as the system can identify customers and make recommendations and lead to a higher ticket sale.

Shake Shack Digital Sales Initiatives (3Q22 Investor Letter)

- Licensing strategy to build an international business without requiring additional capital expenditure and instead provides what is essentially a royalty stream (akin to franchising) which insulates the company from some of the issues it is facing in its owned restaurants (namely inflationary pressure).

- Strong balance sheet- Shake shack maintains a net cash position of roughly $100 million which provides resources for continued expansion.

- While the company has a poor track record of producing consistent levels of operating profitability under current management, with reasonably high average unit volumes, I suspect Shake Shack could be attractive to a potential acquirer who sees an opportunity to significantly improve operating margins.

Negatives

Despite some attractive characteristics, in my view, the negatives significantly outweigh positives at this point in time. Here are my main concerns with the business:

- Shake Shack’s restaurant level operating margins are 600 basis points below 2019 levels. Shake Shack management blames inflationary pressure. While this is certainly a factor, with a high mix of digital sales (shown above), SHAK must pay hefty commissions to delivery services like Uber Eats (UBER). This ongoing cost seems to represent a structural decline in profitability.

- Intense competition in the fast food/hamburger business – in addition to the usual suspects such as Wendy’s (WEN), Burger King (QSR), McDonald’s (MCD), and Five Guys, Shake Shack faces intense competition from regional burger chains with strong regional brands and loyal customers. For instance in Western markets Shake Shack must compete with local players like In N Out and Habit Burger. In the Midwest it competes with Portillo’s and Culvers, etc. Competition limits Shake Shack’s ability to fully pass on cost increases.

- Despite the nascent licensing business mentioned above, the vast majority of Shake Shack’s revenue and EBITDA come from fully owned rather than licensed or franchised operations. Fully owned restaurants tend to be an inferior business model versus asset light franchising. As a restaurant owner, financial results subject to inflationary pressure on input costs which makes for volatility in earnings and cash flow. Intense competition makes it difficult to fully pass along higher costs. We are seeing this in current results as restaurant level operating margins have declined significantly since 2019.

- Deteriorating outlook for US consumer spending due to inflationary pressure

- Underwhelming unit economics for restaurants located outside its home NY market where it has a 20 year history/strong brand and loyal customer base. Like Portillo’s (PTLO) which I recently wrote up, Shake Shack has a marked differential between its home market New York AUVs (average unit volumes) and other markets.

Unit Economics (3Q22 SHAK earnings transcript from Seeking Alpha)

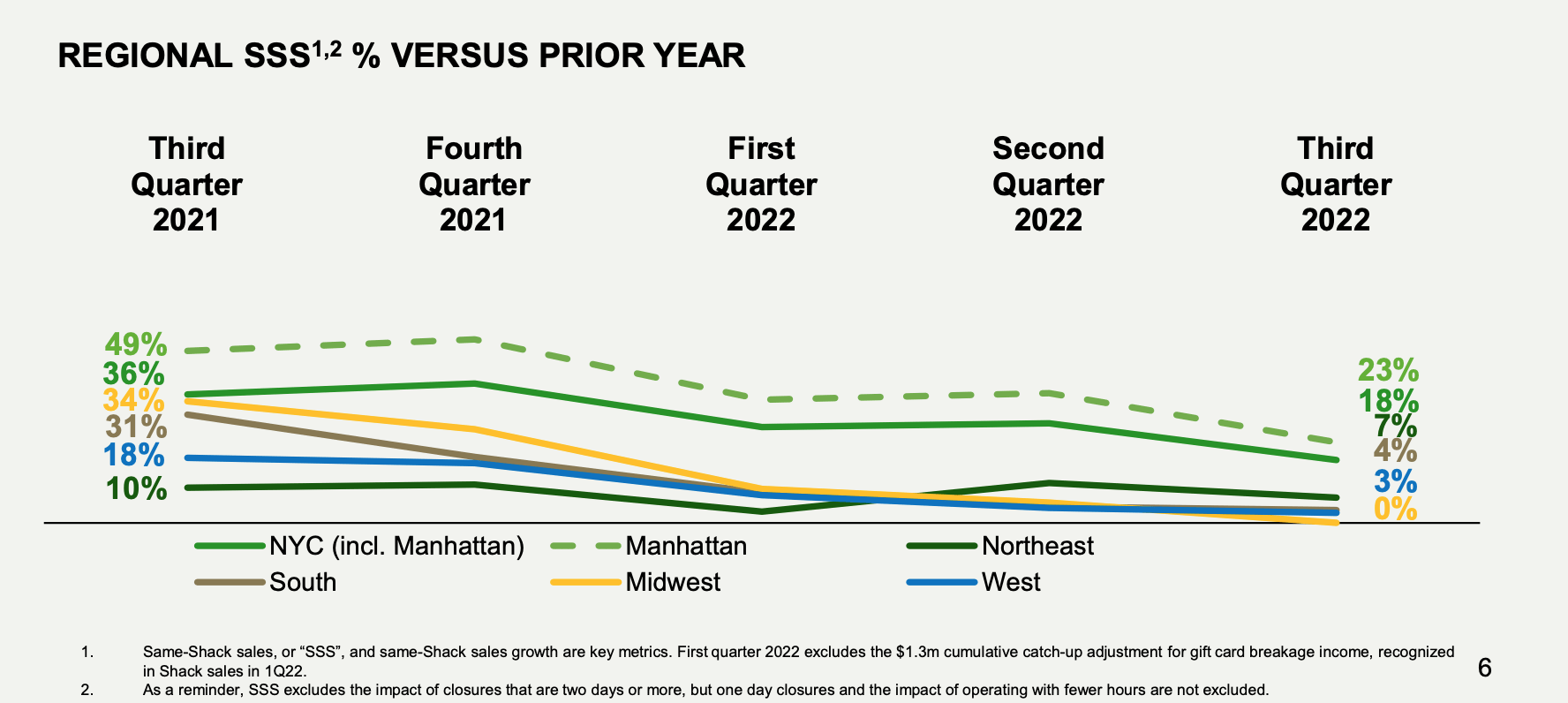

While NY AUVs are otherworldly at ~$8+ million (with well above average restaurant-level operating margins), Shake Shacks outside NY have done considerably lower volumes and margins since the onset of the pandemic (sub $3 million AUV/ estimated sub 14% restaurant level margins). This is a function of not only the lower population density outside NY but also the weaker brand positioning/competitive environment outside its home market (slew of strong regional competitors described above). Moreover, as shown below, NY restaurants have seen stronger comparable sales in recent quarters whereas same store sales trends outside NYC suggest volumes are declining (i.e. price increases appear to represent over 100% of revenue growth in these markets).

Same Shack Sales by Market (3Q22 SHAK Investor Letter)

- Disconnect between Restaurant-Level profitability and group Operating Cash Flow. While total revenues have grown rapidly due to store growth, corporate General & Administrative expenses have grown faster. For the first 9 months of 2022, Shake Shack’s corporate G&A has represented a whopping 13.1% of total revenue which is up from just 10.5% in the first 9 months of 2019. Most investors would have expected this line item to decrease as a percentage of sales. Frankly, I’m not quite sure where this money is going.

- Similar to the previous concern about profitability, operating cash flow for 2022 is on track to come in below 2018 and 2019 levels despite revenue being 50% higher.

- Last but not least, at $41 per share, as shown below, Shake Shack trades at an EV/ 2023e EBITDA multiple of 20x. My 2023 EBITDA estimate assumes Shake Shack can grow sales by a further 21% in 2023 while maintaining operating margins. I consider this to be generous given SHAK’s poor profitability history, ever expanding corporate expenses, and deteriorating unit economics.

Shake Shack Valuation (Company Filings; Author Estimates)

While Shake Shack may have growth potential, with an inconsistent operating history, I think a fair value for the company is somewhere in the neighborhood of 12-13x EBITDA, suggesting a fair value in the $27-28 range. That said, if Shake Shack were able to bring its overall EBITDA margins up to 12-13% (slightly below Portillo’s and 4-500 basis points below Chipotle both of which operate company owned restaurants as opposed to being franchisors), SHAK would be trading at roughly fair value (13x EBITDA).

Conclusion

As discussed above, I believe the negatives clearly outweigh the positives and I am avoiding Shake Shack shares. While I think that the stock is likely overvalued, I would not short shares as it is possible that the company could be acquired by a private equity group with expertise in turning around restaurant chains and restoring operating profitability (such as Roark Capital which acquired Buffalo Wild Wings in 2017).

Be the first to comment