anouchka/iStock Unreleased via Getty Images

In early February, Seritage Growth Properties (NYSE:SRG) reached a key milestone in its multiyear liquidation plan. Using the proceeds of a string of property sales, the company successfully reduced its term loan balance to $800 million (from $1.6 billion as recently as December 2021). This qualifies it for a two-year extension of its term loan, pushing the maturity out from July 2023 to July 2025.

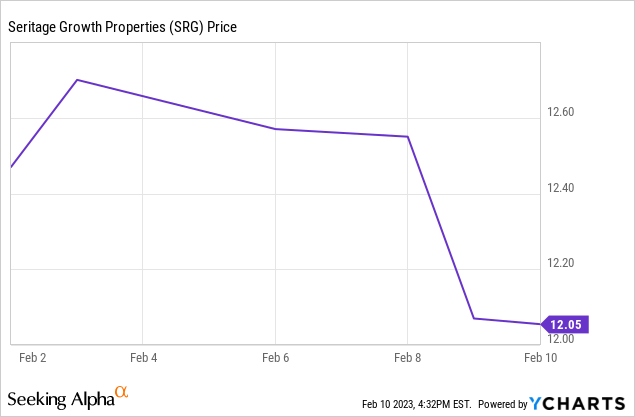

Removing near-term liquidity risk didn’t supercharge SRG stock, though. Seritage shares have actually declined slightly since the company announced its year-to-date asset sale activity and the loan paydown after the market closed on Feb. 2.

There are two likely reasons for this muted reaction. First, Seritage disclosed that its recent asset sales have come at significantly higher cap rates than what it was reporting for most of 2022. Second, management acknowledged that macro headwinds have increased further, making it challenging to sell the company’s most valuable assets.

Neither of these issues is as worrisome as many investors seem to believe. At its Friday closing price of $12.05, Seritage stock still offers tremendous upside potential over the next 1-2 years relative to risk.

High cap rates for a reason

Seritage’s asset sale activity began ramping up in Q2 2022. During that period, the company sold $102 million of income-generating assets at an average cap rate of 4.4%. In the third quarter, it sold another $75 million of income-generating properties (excluding joint ventures), this time at an average cap rate of 4.3%.

Sales of income-producing assets accelerated to $191 million in Q4 2022. But the average cap rate for those sales rose to around 7% (7.7% for fully stabilized properties, 6.0% for partially stabilized developments, and 6.6% for outparcels). And in the first five weeks of 2023 (through Feb. 2), Seritage raised $228.5 million from selling income-producing properties at a blended cap rate of 9.2% for fully stabilized sites and 9.3% for partially stabilized assets.

The sharp increase in interest rates over the past year was bound to put pressure on cap rates for real estate deals. Nevertheless, a rise in cap rates from the mid-4% range to over 9% might seem alarming.

However, comparing the cap rates for Seritage’s Q2 and Q3 asset sales to its more recent deal activity is like comparing apples and oranges. Early in the liquidation process, Seritage was selling assets that quickly got attractive offers, along with some sites that sold at artificially low cap rates because only a fraction of the space was generating rent.

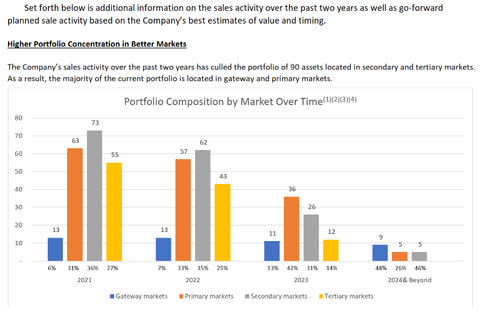

By contrast, in recent months the company has focused on selling less attractive, lower-value properties, particularly within its stabilized multitenant portfolio. Of the 35 properties that Seritage classified in its multitenant retail category as of early November, only 15 remain. Nearly all of those are located in the Northeast, Florida, and California (i.e., high-value geographies).

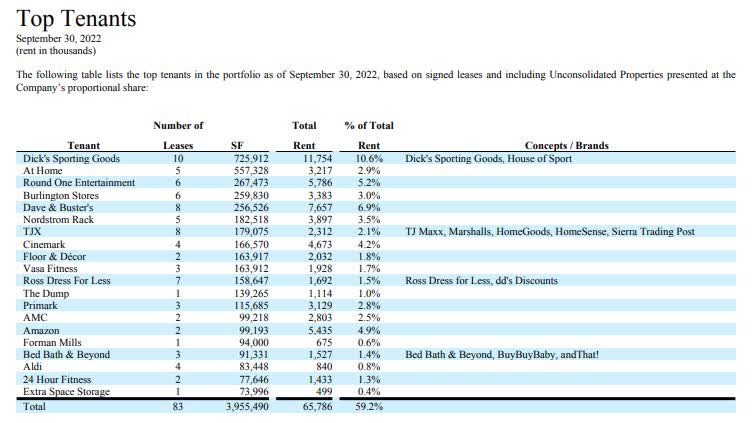

Additionally, during the past three months, Seritage has completely eliminated its exposure to three troubled tenants: AMC (AMC), Bed Bath & Beyond (BBBY), and At Home. This trio accounted for nearly 7% of its rent as of Q3 2022. Selling properties occupied by low credit quality tenants like these obviously drove up the weighted average cap rates for Seritage’s recent dispositions (particularly in 2023).

Source: Seritage Q3 2022 Supplemental, p. 11.

Thus, investors shouldn’t worry that the remaining multitenant retail properties will sell at 9%-plus cap rates. An average cap rate of around 7% is a good baseline expectation.

Assessing macro headwinds

Management’s cautionary words regarding the macro environment could also potentially explain the muted reaction to Seritage’s recent update. Seritage stated:

Over the last several months, the Company, along with the commercial real estate market as a whole, has experienced progressively more challenging market conditions, especially with respect to larger scale development sites, as a result of, among other things, the continued rise in interest rates, increases to required return hurdles for institutional buyers, availability of debt capital, higher construction and labor costs for development, decreased demand for speculative office development and slowing rent growth expectations due to potential recession concerns.

The unfavorable macro backdrop will delay the conclusion of Seritage’s liquidation. Very few new asset sales have been signed up beyond the $1.07 billion that Seritage had either under contract or with accepted offers as of Oct. 13, 2022. Since then, the company has closed deals for approximately $562 million, and as of early February it had $489 million of asset sales under contract and another $95 million with accepted offers.

However, I expect little or no impact on the ultimate proceeds to shareholders compared to what I projected three months ago. Most of the $489 million of sales under contract was likely signed up in the fall. Those deals alone would cover more than half of the $800 million remaining on Seritage’s term loan.

Seritage also continues to market many other assets: particularly its remaining multitenant and non-core properties. It expects to sell the vast majority of its real estate this year, paring its portfolio down to an estimated 19 properties by year-end. That should bring in enough cash to repay the reminder of the term loan and redeem the company’s $70 million of preferred stock.

Source: Seritage Q4 2022 Business Update.

Valuations for these properties are not likely to have fallen much in the last few months. While the Fed has continued raising short-term rates, long-term interest rates have actually fallen in recent months. The 10-year Treasury yield has declined from over 4% in early November to 3.74% at the time of writing. Equally importantly, the availability of financing for real estate has started to improve.

Maximizing value by waiting

While Seritage expects to sell the vast majority of its remaining properties this year, it is waiting for conditions to improve before marketing many of its most valuable assets for sale. Of its seven most valuable properties (those expected to sell for over $50 million), management anticipates selling just two during 2023.

Source: Seritage Q4 2022 Business Update.

Seritage’s two active premier sites (Aventura and San Diego) are likely to stay in the portfolio until at least 2024. Esplanade at Aventura is just starting to open and was only 59% pre-leased as of early November, with leasing activity ongoing for about half of the remaining space. Meanwhile, the Collection at UTC is 100% leased but not fully open yet. Moreover, Seritage is seeking entitlements for additional phases of development at the site.

Leasing more space in Aventura and securing additional entitlements in San Diego will make these properties more valuable regardless of the macro environment. Success on both fronts would give Seritage a good chance of selling those properties for a combined $400 million or more.

Seritage also expects to hold most of its premier development sites into 2024. There’s no guarantee that macro conditions will improve by next year, but there are reasons for optimism. The Fed is likely to stop raising interest rates by mid-2023 and may start cutting rates next year. Furthermore, if the Fed succeeds in cooling the economy, soaring construction costs will no longer be a barrier to selling large-scale development sites. The pandemic-influenced boom in single-family home construction has already come to a crashing halt, which should help.

Crucially, cash burn continues to recede rapidly, reducing the “penalty” for moving more slowly on asset sales. With the recent term loan paydown, the run rate for net interest expense and G&A spending combined has probably fallen below $100 million annually. (This assumes that G&A will decline significantly in 2023 due to lower professional fees and the company’s much smaller size.) That compares to an annual run-rate of around $30 million for NOI, factoring in recent asset sales and tenant openings. Tenant openings in Aventura and San Diego along with additional sales of vacant assets should reduce quarterly cash burn to less than $10 million by the second half of 2023.

Upside still vastly outweighs downside

Based on the company’s recent asset sale activity, the value of assets under contract, and the quality of its remaining real estate, I currently expect Seritage’s distributions to shareholders to total between $16 and $22 per share. A small amount of cash could be distributed in late 2023, but I anticipate the bulk of distributions to come during 2024 and possibly 2025.

The low end of that range would provide a 33% return from Seritage stock’s current price. The gains would exceed 50% if the total proceeds fall in the upper half of that range. And even if the liquidation extends into 2025, shareholders are likely to receive substantial distributions during 2024. In short, the annualized returns would be quite attractive even if total distributions came to just $16.

Even in a severe downside scenario, shareholders buying at the current price would be unlikely to lose money. With the shares on pace for strong returns over the next 1-2 years in the most likely scenarios and fairly minimal downside risk, Seritage continues to look like one of the most attractive stocks in the market today.

Be the first to comment