scanrail

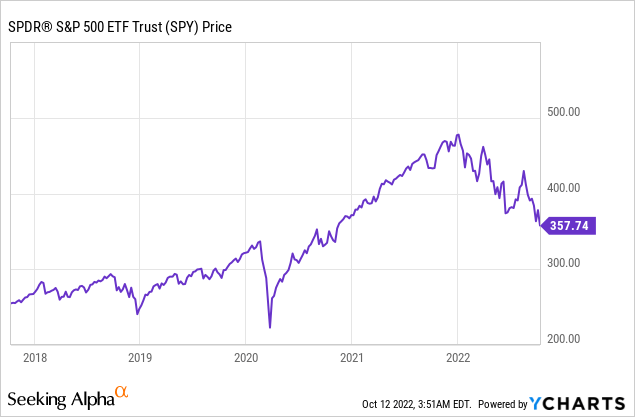

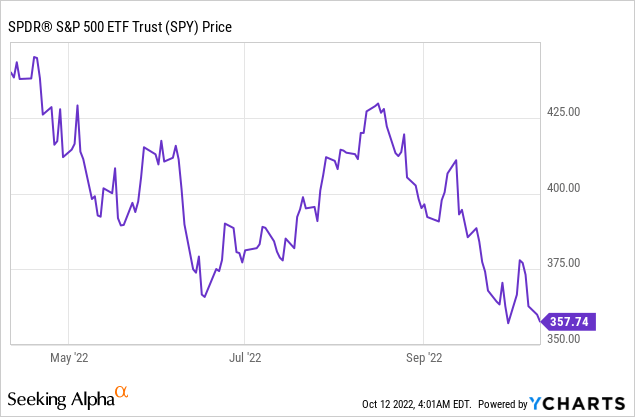

Before 2020, inflation reports were scarcely a sideshow in the parade of economic reports that come out each month. Changes in prices had been low and predictable for decades, so no one cared. But after 2+ years of soaring inflation, off-and-on shortages of goods, and soaring inflation–CPI is the most important reading for the markets in any given month. The latest installment is due out on Thursday, October 13th at 8:30 AM Eastern Time. The stakes are high. One JPMorgan analyst has called for a drop of as much as 5% in the immediate aftermath of another hot inflation report, while the VIX is pointing to a potential move of a bit less than 3% by the end of the week. Largely due to runaway inflation over the last year, stocks have plunged in 2022, unwinding all of the 2021 bull market gains and threatening to unwind 2020’s gains as well.

Will Inflation Ever Slow Down?

Likely not for the September reading–at least to nowhere near the Fed’s target of 2% annual core inflation.

Bloomberg polled a group of economists, and the expectation is for headline inflation to come in at 0.2%, while core inflation comes in at 0.4%. Core inflation at 0.4% per month is about 5% annualized, which is still more than double the Fed’s target. They clearly have work to do in raising rates, which will put stock prices under pressure. As the Fed raises interest rates, the question on the mind of every institutional investor is when they’ll stop, because that tells them what a fair price to pay for stocks is.

No one knows for sure the path of inflation and rates, but we can make some educated guesses. In previous articles, we handicapped this using publicly available econometric models and came up with a likely interest rate of about 4 to 4.5% and relentless quantitative tightening. The market has now finally priced this in. The question now is whether that will work, or whether the Fed will be forced to hike even more in the face of stubborn inflation to stop the party. In this case, the necessary adjustments are big enough that unemployment likely will not stay anywhere near historical lows, which in turn means that corporate profits won’t stay at all-time highs. The Fed can’t throw in the towel here either and just let inflation be 10% per year or more forever. Doing so would eventually cause America to lose its greatest privilege – having the world’s reserve currency and the increased standard of living that comes with it.

Tighter Financial Conditions Are Helping

The main way the Fed clamps down on inflation is by tightening financial conditions (lower stocks, higher yields, stronger dollar). August CPI, the Fed’s last “report card” was a brutal shock for stocks because it showed the Fed’s efforts were not working. But the main reason why they weren’t working was that the markets had fallen in love with the idea of a Fed pivot from June to mid-August, buying all the stocks they could get, sending bond yields tumbling and the dollar down. But markets are reflexive. With stocks up ~17% in a couple of months from June to August, people surely took the cue to ramp up spending, and the falling dollar directly made imports more expensive, leading to a bad CPI report. All of the money being bet on the Fed pivoting itself made it impossible for the Fed to actually pivot by loosening financial conditions.

Now, this has all been unwound and then some, putting downward pressure on inflation. This might set the conditions for inflation to possibly come in better than expected, or at least not as bad as feared. If this happens, everyone might go out and pour money into stocks again, only to be slapped down by a poor inflation report in a month or two due to rising markets and a falling dollar.

But They May Not Be Enough

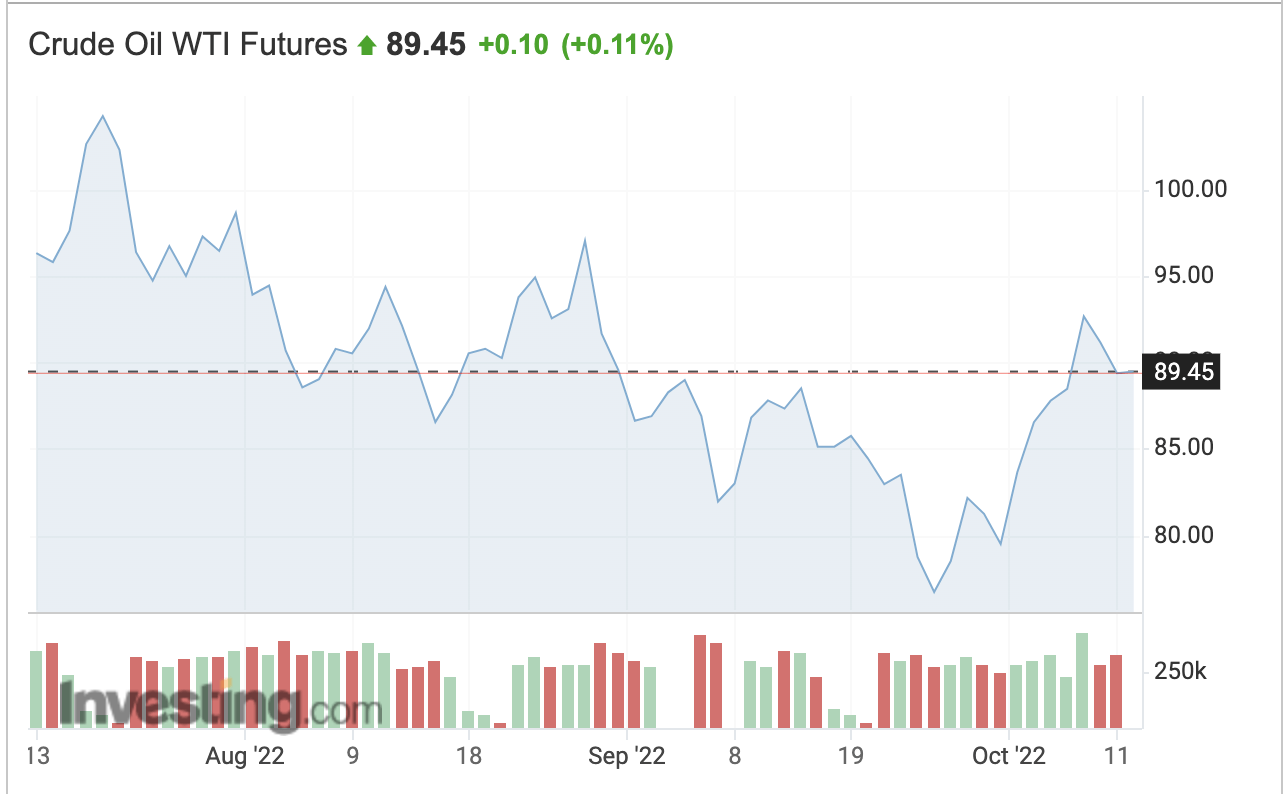

1. The Saudis and OPEC have continued their decades-long tradition of sticking it to the US and Europe, agreeing to an output cut in oil production to try to push prices back over $100 per barrel. Since almost every consumer good has to be transported from where it is manufactured to where it’s bought, this directly feeds into prices. OPEC’s defiance is a clear signal that inflation is not going to come down on its own without the US and Europe securing their own oil/gas production and eventually enough renewable energy to get a “divorce” with OPEC. This will take years, and there’s no easy fix.

WTI Crude Oil (Investing.com)

2. Labor problems. In the early phase of the pandemic, companies saw their profit margins boom as they were able to raise prices faster than employees could bargain for wage increases. This led to the stupid media trend of the “great resignation” which was really just employees going to where they could earn a market wage. Now we have tons of labor problems, particularly with unions. Unions in particular are going to claw back their relative share of gross profits, and there’s nothing the Fed can do to stop this with the unemployment rate at 3.5%. So we have ongoing negotiations, and threats of strikes in every economic bottleneck there is, whether it’s railroad employees, dockworkers, or airline pilots. And that’s just the people who work. Social Security is going to have its annual CPI adjustment (maybe 9% this year) at year-end which is going to further increase price pressures.

3. Rent renewals. Asking rents are actually falling month over month, but that’s cold comfort for many renters coming off of long-term leases now at much higher rates than previous. They don’t go into CPI until they’re paid, so this will continually put upward pressure on inflation after the lag from earlier in the pandemic.

September CPI Forecast

The Cleveland Fed has a good econometric model that I believe is more accurate than surveying a bunch of random economists. They have core CPI at 0.51% month-over-month for September and 0.53% month-over-month looking ahead to October. If these projections are right, these numbers are bad and worse than the market expects, showing that the Fed is nowhere near stopping inflation and that a hard landing is the only way down.

Another approach I sometimes like is to look at other countries that report CPI earlier in the month than the US. Since global central banks have begun to coordinate policy, hot numbers abroad have generally predicted hot numbers in the US. In September, CPI in Thailand came in better than expected, Taiwan came in worse, and the Philippines came in worse. In Europe, the Netherlands put in an awful report not just because of energy, but also in services inflation. Hungary similarly saw huge increases in the cost of services. These both are indicating that core CPI could potentially be hotter than expected.

But my best guess is that tighter financial conditions are doing enough to hold these pressures more or less in check enough to keep core CPI at 0.5% month-over-month. This said– I don’t doubt JPMorgan’s nightmare prediction that stocks will fall 5% in a day or two if core CPI comes in at 0.6% month over month. In any case, checking some econometric models and countries that report CPI before the US shows that this inflation report is unlikely to be particularly good.

What do you think about the path of inflation? Feel free to share your thoughts in the comments!

Be the first to comment