Kameleon007/iStock via Getty Images

This is my first look at Sensus Healthcare, Inc. (NASDAQ:SRTS). It is a specialty medical device company that has carved out a profitable medical device niche. It manufactures and sells sophisticated dermatological equipment utilizing a proprietary low-energy X-ray technology known as superficial radiation therapy [SRT]. Its SRT devices allow practitioners to accomplish less painful and often more effective procedures.

The company has faced its challenges. As it now (01/22/2023 as I write) stands, Sensus Healthcare, Inc. presents an interesting small cap ($157 million market cap) investment opportunity. Slides referenced below are included in Sensus’ Q3, 2022 earnings presentation.

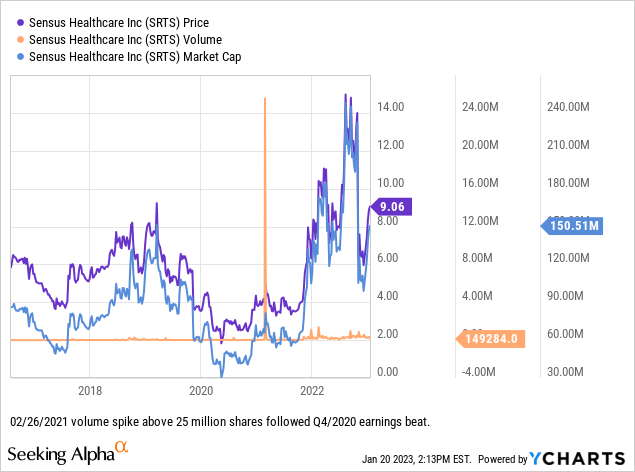

Sensus fell back sharply from its Q3, 2022 miss

Sensus Healthcare, Inc. is a relative newbie to the public markets; It went public in 2016. For several years, it traded in the doldrums, usually well below $5.00 on low volume. It closed Q4 2020 with a nice $0.13 EPS beat. Successive quarterly beats along with successful sales and reimbursement finally launched Sensus Healthcare, Inc. shares over $10 in intraday trade on 02/15/2022 for the first time, as shown by its chart below:

More recently, Sensus reported its Q3 2022 earnings after market close on Thursday, 11/03/2022. It seemed to be a good report. Its revenues were $9.01 million, up 64% from $5.5 million; its net income was $1.8 million, or $0.11 per diluted share, compared with $0.2 million, or $0.01 per diluted share. However, it missed EPS expectations by $0.02; revenues by ~$0.52 million. The market cut it no slack.

The next Friday, 11/04/2022, Sensus Healthcare, Inc. opened at $8.09 and closed the day at $6.34, down >50% from its 11/03/2022 close of $13.00. It then wandered without conviction until 12/13/2022, when it hit a low of $5.58. It has been recovering since.

Sensus preliminary fourth quarter 2022 revenues put it back on a winning track

On 01/05/2023, Sensus took an important step forward in advancing its shares following its unfortunate Q3 2022. Its preliminary read expects its Q4 2022 earnings to come in at $13 million, a quarterly increase of >44% over Q3’s $9.01 million. It expects full year 2022 revenues of $44 million, reflecting 60% growth over revenues for 2021.

Importantly and atypically for young commercial stage biotechs, its Q4, and its 2022 as a whole, are profitable. In the release reporting these preliminary results, CEO Joe Sardano advised (son Michael Sardano is President and General Counsel):

“We’re delighted to report topline momentum during the fourth quarter and to share our expectations for continued growth in revenues and profitability in 2023…

Our robust marketing programs, combined with an expanded product offering and the opening of new customer channels, are expected to contribute to our growth trajectory.”

The preliminary report gave no update on its current cash situation. Happily, liquidity has not been a Sensus problem. Sensus is a profitable organization with no debt as of close of Q3, 2022. Also its CEO has an aversion to debt as per his following quote from its Q3, 2022 earnings call (the “Call“):

… One of the things that we cherish is the fact that we do not have any debt. And going into this period of, I would say, questionable finances with inflation rates and things like that, I don’t think it would be very wise for us to incur any major kind of debt to make an acquisition regardless of how good that acquisition may be. I think that we have to make sure that we live within our means…

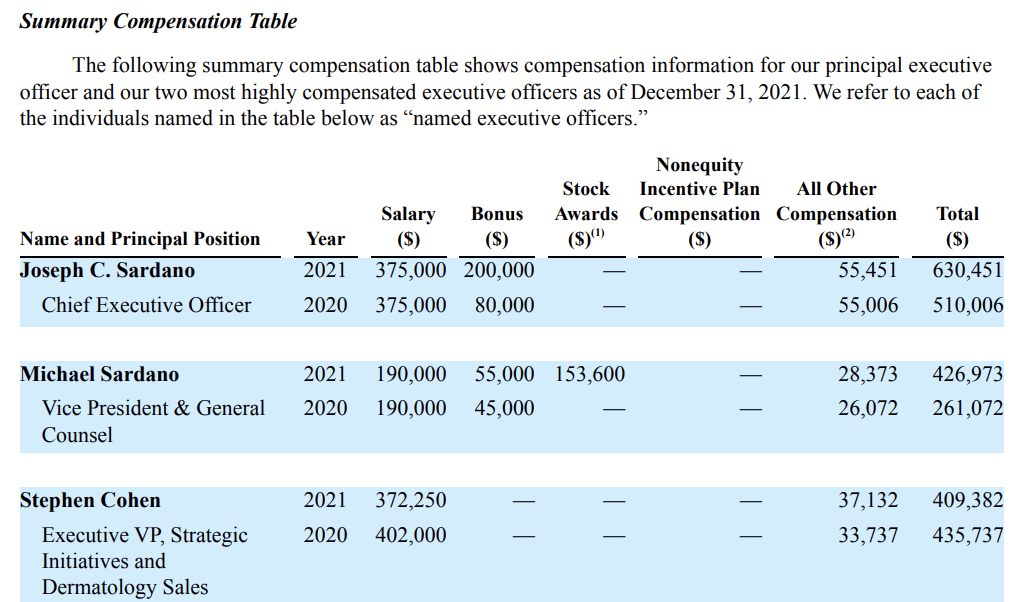

After such a ringing endorsement of fiscal rectitude, a suspicious mind might question how careful management is with its C-suite payroll. In Sensus’ case, management appears not only to talk the talk, but also to walk the walk, as reflected by its summary compensation table from its latest proxy:

seekingalpha.com

The one point that is disturbing is the father/son relationship between the CEO and the company’s VP and general counsel (proxy p. 15). Ideally, a company’s general counsel is an independent restraining force acting from long wisdom and experience. In typical families, a son lacks the cool judgment and independence one hopes to see in the general counsel role.

Sensus products span both aesthetic and clinical dermatology

Aesthetic

Sensus Healthcare, Inc. has been building its aesthetic laser devices over time. During its Q3, 2020 earnings call, CEO Sardano discussed how its Mobile Laser Aesthetics business was using lasers from other companies. His goal, which he expected to realize by the start of 2021, was to have a Sensus owned and branded product.

As described the situation in its Q4 2020 earnings call, Sensus Healthcare, Inc. was building its aesthetics laser business piece by piece. It started with its home region of south Florida market. It expected to grow it to become a meaningful source of revenue that it would build upon.

Aesthetic dermatology writ large is often thought to be highly sensitive to economic conditions because it is often a cash pay operation. During the Call an H.C. Wainwright analyst probed this issue at length in a dialogue with CEO Sardano. He asked if the economy was more apt to impact Sensus’ transdermal infusion device [TDI-slide 17] rather than its devices geared towards clinical dermatology.

Sardano advised that this was unlikely to be the case for Sensus. Sardano’s response was helpful for those considering an investment.

He made the following points:

- Sensus’ aesthetics focused TDI system is relatively inexpensive with an average selling price of ~$28,000;

- at that price a modest reduction in procedures is unlikely to impact sales given the advantages of the TDI system in terms of the patient experience;

- aesthetic procedures most apt to be impacted are truly optional ones such as microneedling for facial rejuvenation which is not Sensus target;

- TDI so obviously enhances the patient experience of patients undergoing hair restoration and hyperhidrosis (for excessive sweating) by removing the pain that it will attract new patients to a practice.

During the Call, Sardano declined to break out Sensus’ revenue sources. He noted that its aesthetics business had yet to reach a scale that made sense to break it out. He noted:

…it’s going to be appropriate someday when we have significant numbers to reflect what each one of those units have if we’re going to be over $0.5 million or over $1 million on a quarterly basis with TDI or with the aesthetic product or the laser product. I think that, that will be appropriate. Right now, just launching the new laser product, the mobile laser product and TDI is pretty early, and I don’t see the numbers as being that significant. But we will get there. We will make it significant.

Clinical

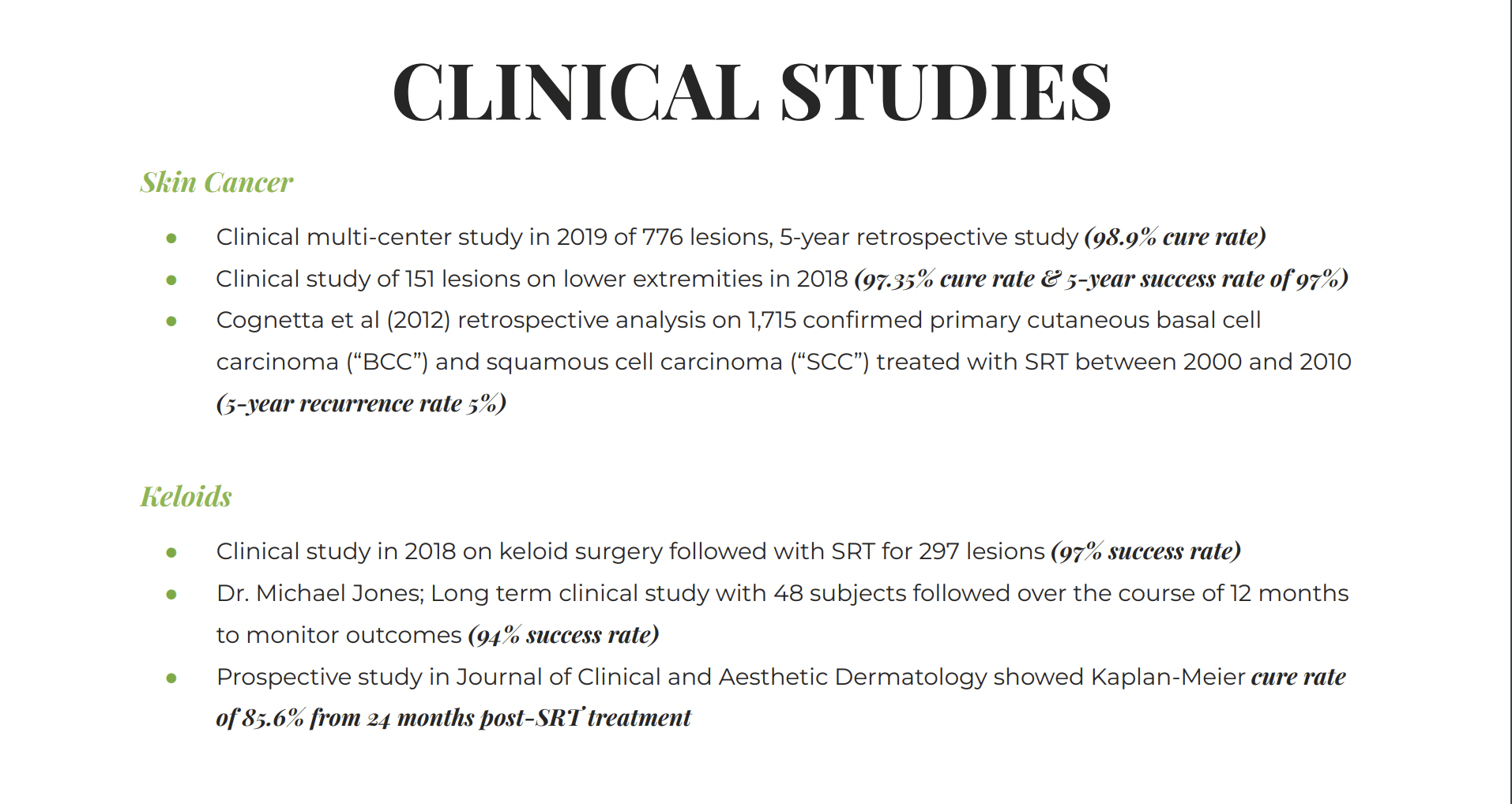

The bulk of Sensus revenues are attributable to its clinical-focused devices that aid practitioners in the treatment of non-melanoma skin cancer (slides 6- 8) and keloids (slides 9-11). Slide 12 below importantly lists the clinical study support for its cancer and keloid franchise:

sensushealthcare.com

Per slide 10, Sensus reports that it has the only FDA cleared system for treating keloids.

Conclusion

As I write on 01/22/2023, Sensus Healthcare, Inc.’s latest close was $9.15. This is far from a bargain, judging from its trading over the last year. In terms of Ratings on Seeking Alpha, Sensus Healthcare, Inc. scores a hold from Seeking Alpha authors and its quant system, with a buy from the ever-optimistic wall street analysts. Analysts give Sensus Healthcare, Inc. an average price target of $15.40, a ~68% upside.

I like Sensus Healthcare, Inc.’s story. I rate it as a buy, but I think investors should be cautious at its current price.

Be the first to comment