DKosig

Investment Thesis: I take a bullish view on SBA Communications Corporation (NASDAQ:SBAC) due to strong growth in earnings despite inflationary pressures.

In a previous article back in August, I made the argument that SBA Communications Corporation could see further upside going forward on the basis of strong revenue growth as well as a rising total assets to long-term debt ratio.

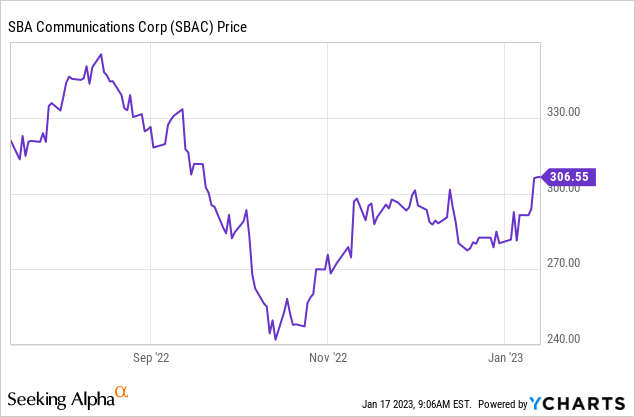

At the time of my article, SBAC stock was trading at $339. However, the stock has since declined to $306.55 at the time of writing:

ycharts.com

The purpose of this article is to assess whether SBA Communications Corporation stock has the capacity to rebound to prior levels from here, while also assessing whether my previously stated reasons for taking a bullish view on the stock still hold.

Performance

When looking at the total assets to long-term debt ratio for September 2022 – we can see that growth in assets is continuing, with long-term debt having decreased since the previous quarter.

| Dec 2021 | Jun 2022 | Sep 2022 | |

| Total assets | 9,801,699 | 10,011,937 | 9,949,014 |

| Long-term debt | 12,278,694 | 11,817,504 | 11,696,068 |

| Total assets to long-term debt ratio | 79.83% | 84.72% | 85.06% |

Source: Figures sourced from SBA Communications Corporation Q2 and Q3 2022 Results. Total assets to long-term debt ratio calculated by author.

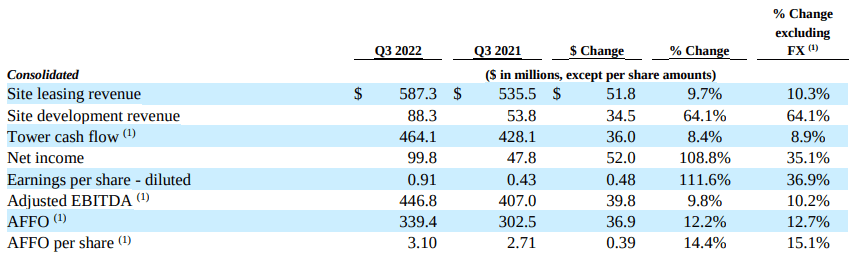

Additionally, we can see that site leasing revenue was up by over 10% as compared to that of the previous year, while earnings per share was up by over 35% along with AFFO (adjusted funds from operations) per share up by over 15% (all figures excluding FX):

SBA Communications Press Release: Third Quarter 2022 Results

From this standpoint, performance for SBA Communications Corporation has continued to remain quite strong and its long-term debt has been declining – which is an encouraging sign.

In this regard, I take the view that there appears to be somewhat of a disconnect between the company’s recent performance and its share price trajectory.

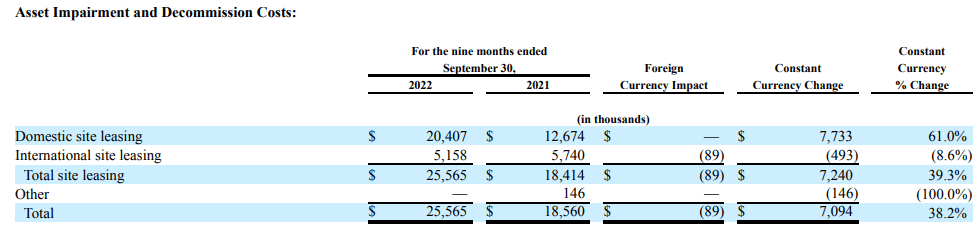

With that being said, there appears to be concern among investors regarding the impact of the Sprint and T-Mobile US, Inc. (TMUS) merger and the impact that a resulting increase in churn rates is having on asset impairment and decommission costs.

For instance, we can see that total costs on a constant currency basis increased by $7 million – which the company cites as being an effect of increased churn from Sprint.

SBA Communications Form 10-Q: Q3 2022

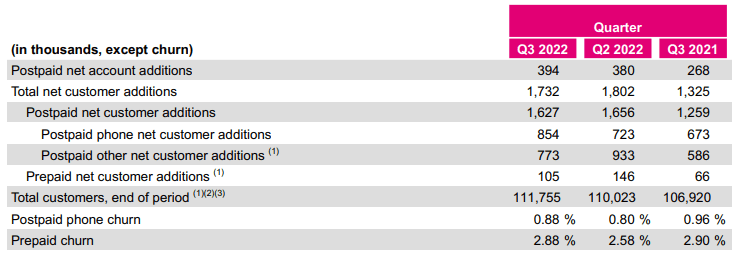

When looking at churn rates for T-Mobile US across its most recent quarterly earnings report, we can see that both postpaid and prepaid churn has increased from Q2 2022 – albeit with churn rates in Q3 2022 remaining lower than that of the previous year.

T-Mobile Q3 2022 Quarterly Earnings Release

The increase in churn also appears to have affected competitors, including Crown Castle Inc. (CCI).

Additionally, a broader macroeconomic concern may be the effect of rising interest rates. However, I take the view that while churn rates may have risen temporarily as a result of the merger – rates are still down from the previous year overall, and so the long-term trajectory for churn could still be to the downside.

Looking Forward

Going forward, macroeconomic pressures might place some pressure on SBA Communications Corporation stock despite the core business remaining strong.

For instance, telecom infrastructure is highly sensitive to rising interest rates – a trend which may continue as central banks continue to battle inflation. Rising inflation makes it more expensive for companies with exposure to this industry to continue investing in upgrading their infrastructure – due to both higher prices as well as higher interest rates increasing the cost of borrowing.

In this regard, an increase in churn rates for telecommunications companies would be of concern – as a potential drop in consumer demand would in turn lower the demand for infrastructure investment.

From this standpoint – I take the view that while SBA Communications has shown strong revenue and earnings growth as well as an encouraging reduction in long-term debt, investors will be paying attention to see whether such growth can continue in spite of the ongoing macroeconomic pressures.

Conclusion

To conclude, SBA Communications Corporation has shown strong performance in spite of macroeconomic pressures. For the upcoming earnings quarter and throughout 2023, my opinion is the focus will increasingly shift to whether SBA Communications can continue to bolster earnings in spite of inflationary pressures.

However, I take the view that the progress shown to date is encouraging and continue to take a bullish view on SBA Communications Corporation.

Be the first to comment