Andres Victorero

Stocks considered more value oriented had another stellar day yesterday, but they dragged their growth counterparts along for the ride this time, which is why the major market averages all finished with solid gains. The second trading day of the year ends the 7-day period that determines if we had a Santa Claus Rally, and while the return was below average, it was a rally. Based on historical precedent, a positive return during this period increases the likelihood that the month of January is positive.

Finviz

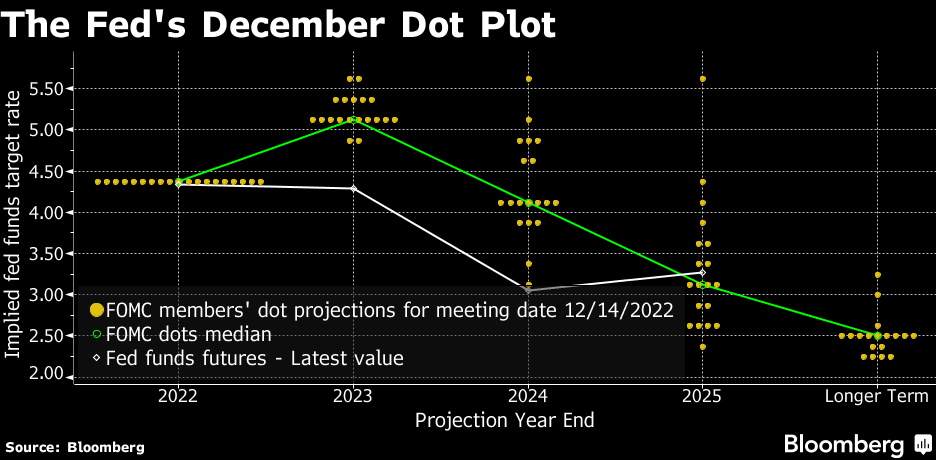

The impressive aspect of yesterday’s stock performance was that it came in concert with the release of the meeting minutes from the Fed’s last gathering on December 13-14. The minutes showed the frustration members had with market expectations for rate cuts during the second half of this year, which they felt was loosening financial conditions too soon. This explains Chairman Powell’s hawkish press conference following the meeting, which led to the sell off in stock prices during the last two weeks of the year.

Bloomberg

Yet the market does not play the rhetoric game, which is one of the Fed’s tools for managing expectations. It simply reacts to the incoming data, and the data is telling the Fed that its rate-hike cycle should end. That is why the yield curve is inverted.

Despite the lower-than-expected Consumer Price Index number for November that was reported just before the Fed’s meeting, members increased their projection for inflation at the end of 2022 from 4.5% to 4.8%. That did not make a lot of sense. Given the higher level to start this year, they also increased their projection for inflation at the end of 2023 from 3.1% to 3.5%. Members indicated that the strength of the labor market was likely to keep the rate of inflation higher for longer, which also led to their increase in expectations for the terminal rate to more than 5%.

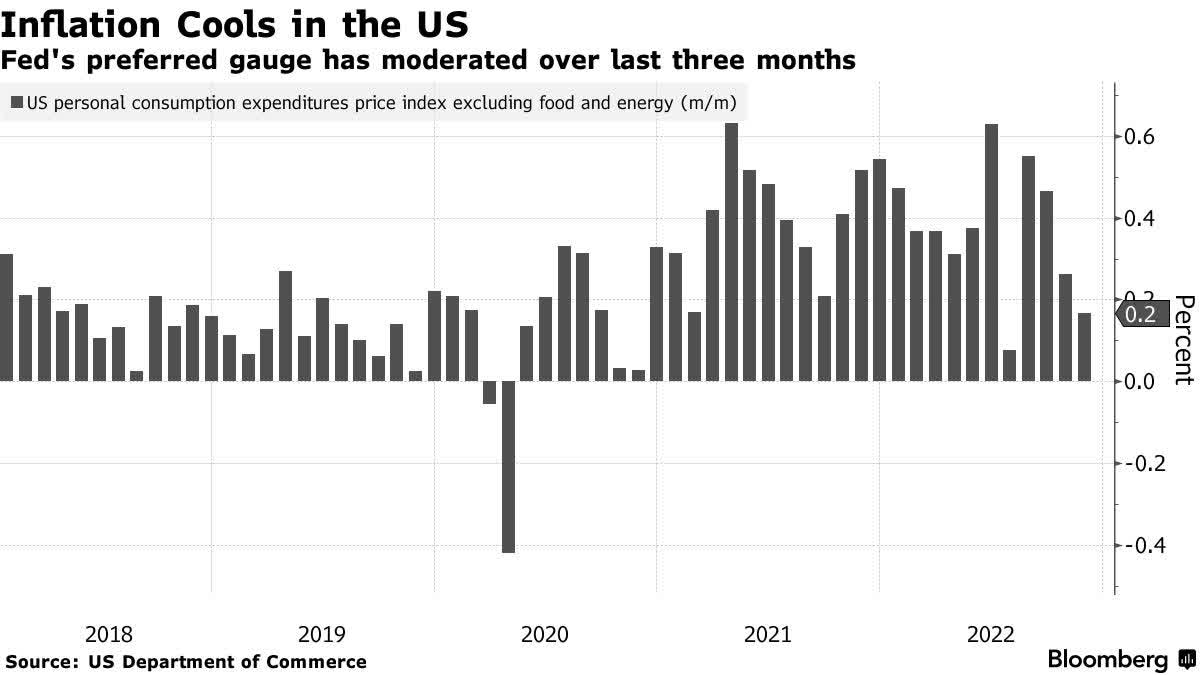

Again, their revisions at the December meeting ran counter to the incoming data, which was further confirmed by a weaker-than-expected PCE index for November after the meeting. Ignoring this data, I think the Fed was simply trying to quell the enthusiasm for risk assets that was brewing as we approached year end. That is what was loosening the financial conditions they have been trying to tighten.

Bloomberg

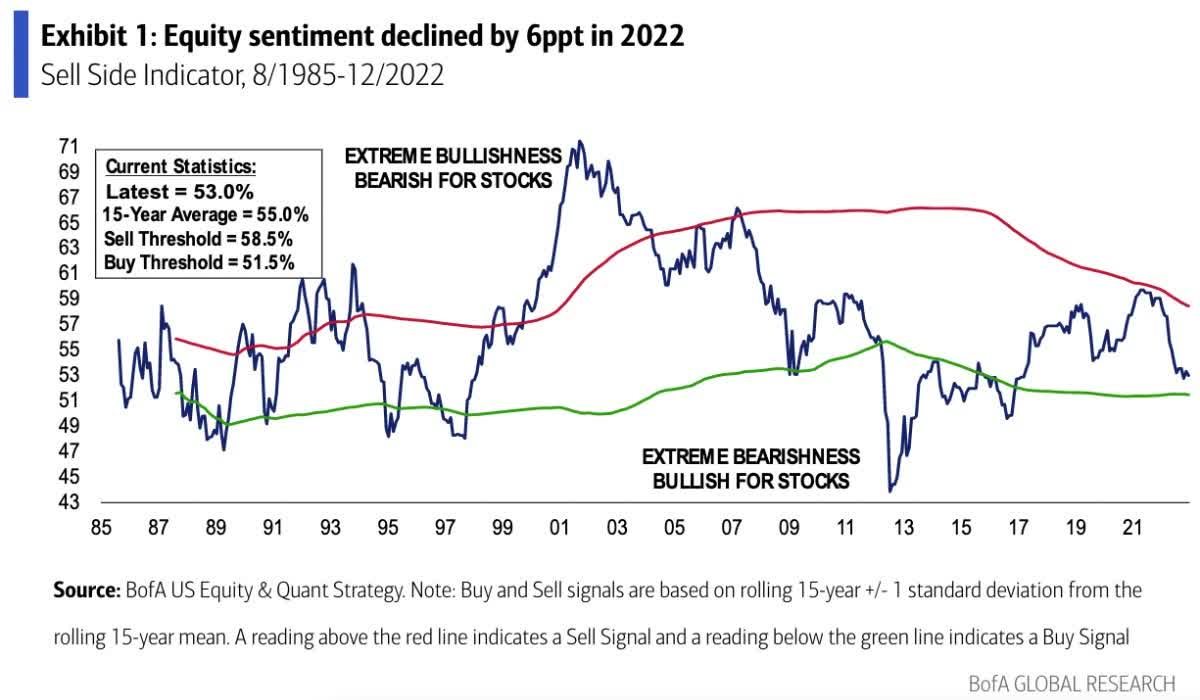

But another better-than-expected inflation report for December, which we should have before the Fed’s next meeting on February 1, should force members to acknowledge that their inflation and terminal rate targets are too high. I think the next inflation report will show that we ended 2022 with a core PCE rate of 4.5% rather than 4.8%. That would increase the odds that inflation ends this year well below 3.5%. If this is the case, investors are clearly not positioned for it based on sentiment. According to Bank of America’s “sell-side indicator,” when it has fallen to its current level or below, the market has been at a higher level 95% of the time one year later. The average gain was 16%.

Yahoo Finance

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment