DMP

Sanofi (NASDAQ:SNY) (OTCPK:SNYNF) is one of the largest pharmaceutical companies in Europe, with a leading position in the global anti-inflammatory therapeutics market.

Investment thesis

Wall Street’s indifference to France’s largest pharmaceutical company is reflected in its share price continuing to move sideways despite its rich pipeline of approved and experimental medicines, rising dividend payouts, and relatively low debt.

In my estimation, in addition to the product candidates, some of which could become “gold standards” in the treatment of autoimmune diseases, other key contributors to strengthening Sanofi’s balance sheet are innovative drugs such as Dupixent, Nexviazyme, Toujeo, Enjaymo, and Sarclisa.

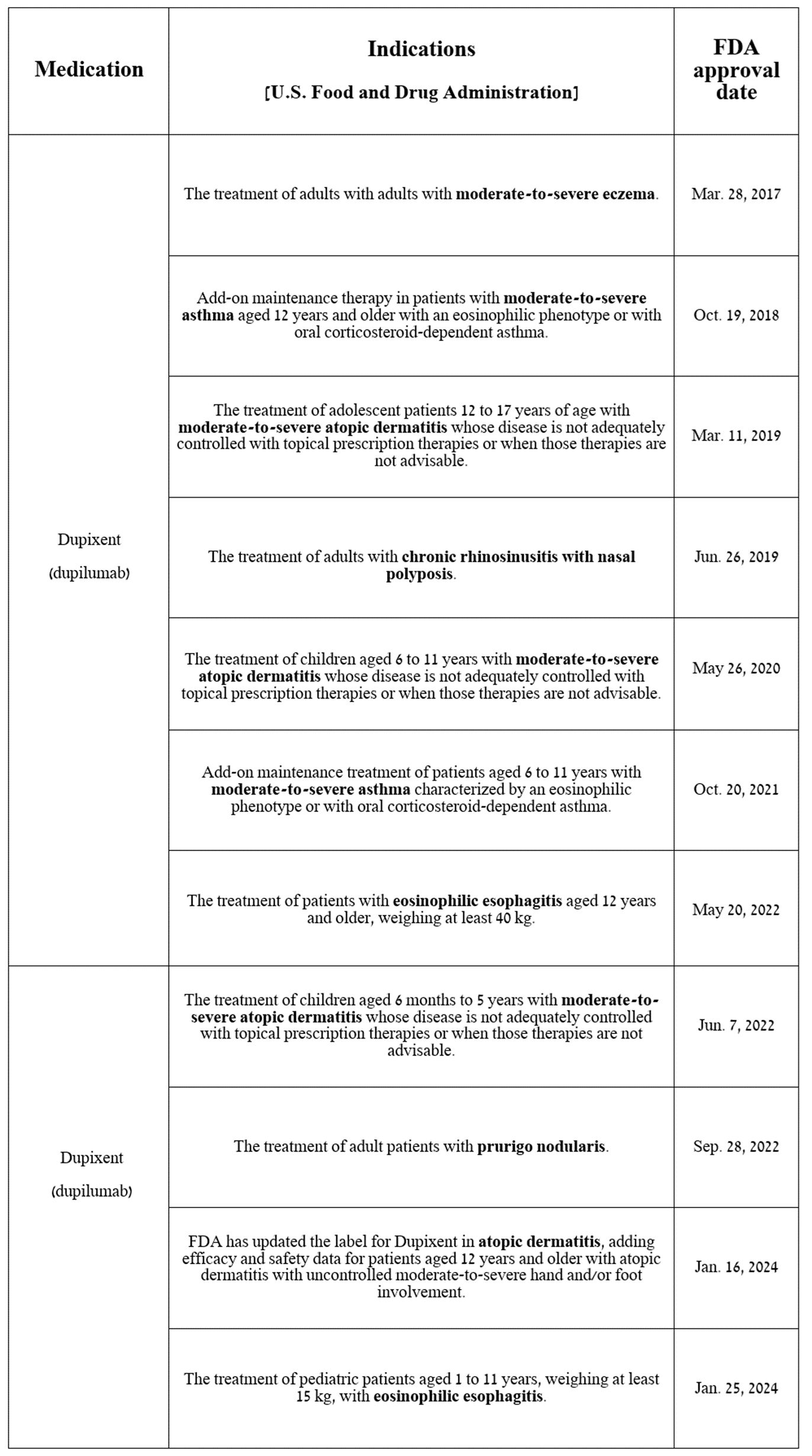

So, Dupixent (dupilumab) is a monoclonal antibody developed in partnership with Regeneron Pharmaceuticals (REGN) that is approved by regulatory authorities for the treatment of a broad spectrum of autoimmune and inflammatory disorders, including atopic dermatitis, asthma, eosinophilic esophagitis and more.

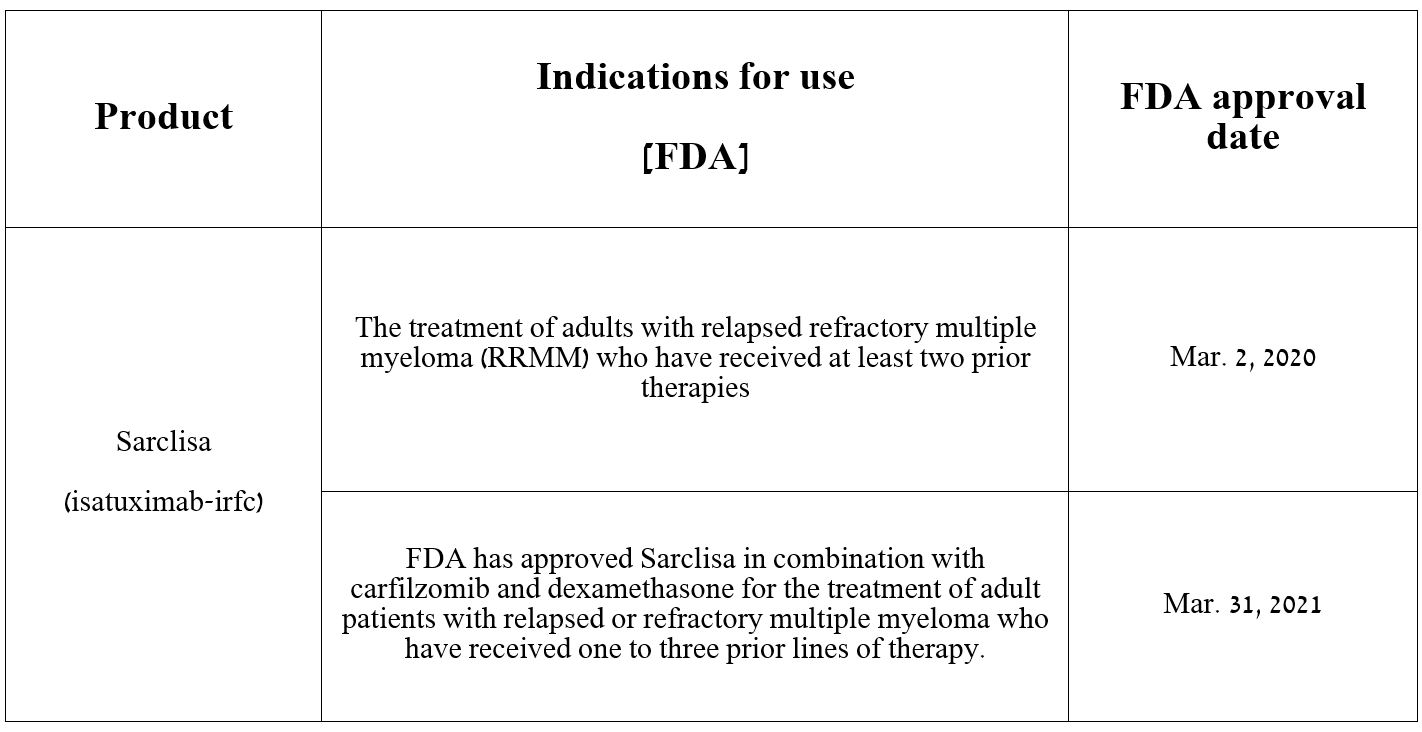

In the table below, I’ve noted the label expansions for Dupixent since it was first approved by the FDA in 2017.

Source: table was made by Author based on Sanofi press releases

How does dupilumab work in simple terms?

First of all, I would like to point out that understanding the mechanism of action of medication allows me to determine for which diseases it will be effective, as well as to assess the chances of its success in ongoing clinical trials.

Initially, Dupixent binds with high affinity to the human IL-4Rα subunit, which ultimately leads to blocking IL-4 and IL-13 intracellular signaling.

By inhibiting the actions of interleukin-4 (IL-4) and interleukin-13 (IL-13), dupilumab calms down an overreactive immune system and improves skin conditions in patients with moderate to severe atopic dermatitis, and it also helps reduce inflammation and relieve symptoms in people with asthma and other conditions.

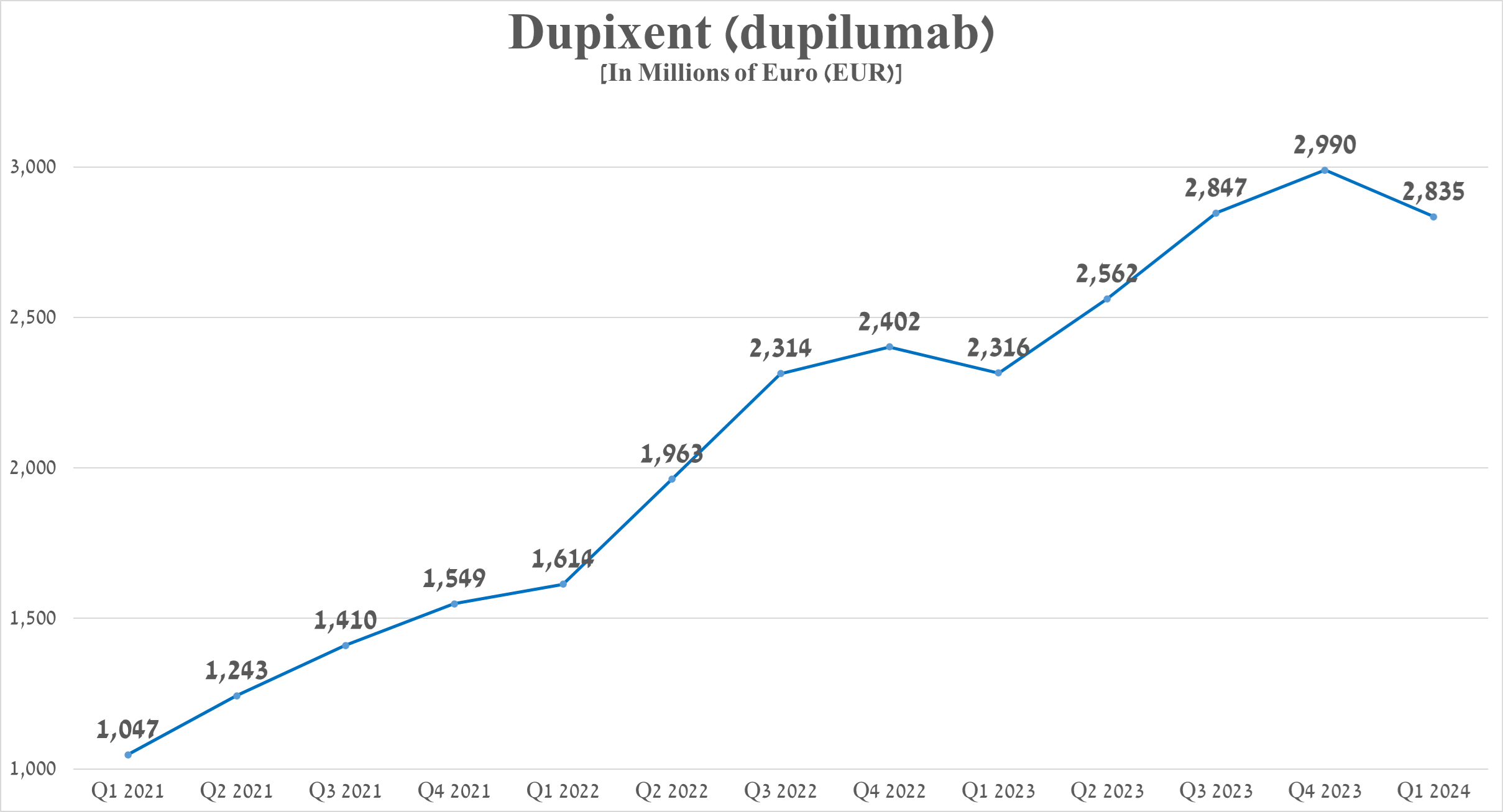

Total sales of Dupixent were about 2.84 billion euros in the first three months of 2024, up 22.4% year-on-year due to continued strong demand from patients with asthma and atopic dermatitis, as well as its label expansion in January 2024.

Source: graph was made by Author based on 10-Qs and 10-Ks

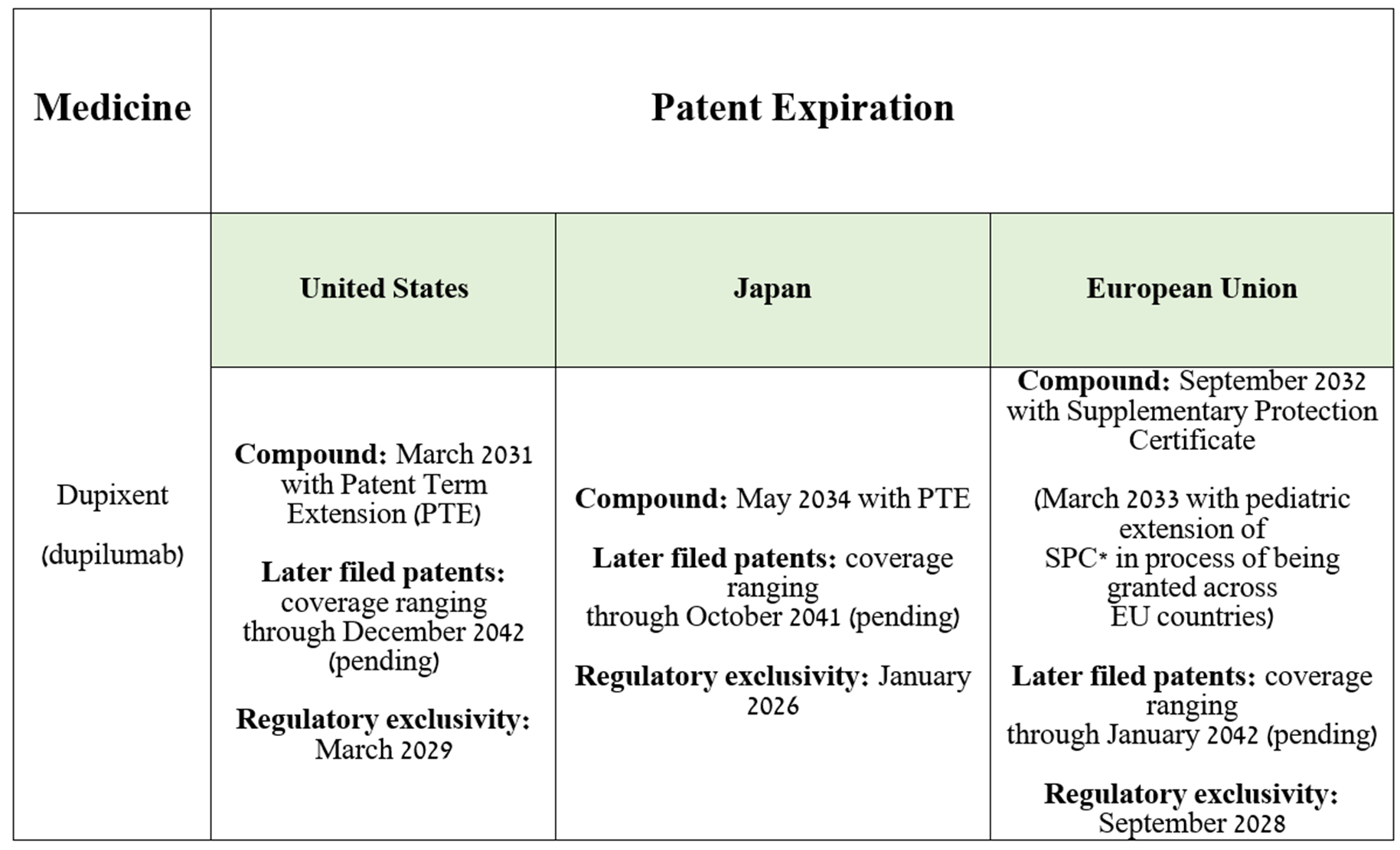

Additionally, I want to point out that dupilumab has strong patent protection. Key US and European patents protecting Dupixent from the introduction of its biosimilars will expire only in the next decade, which, in my opinion, will allow Sanofi’s medication to continue increasing its share in the global anti-inflammatory therapeutics market.

Source: table was made by Author based on Sanofi’s 20-F

Let’s move on to discuss the recent progress made in the development of Dupixent.

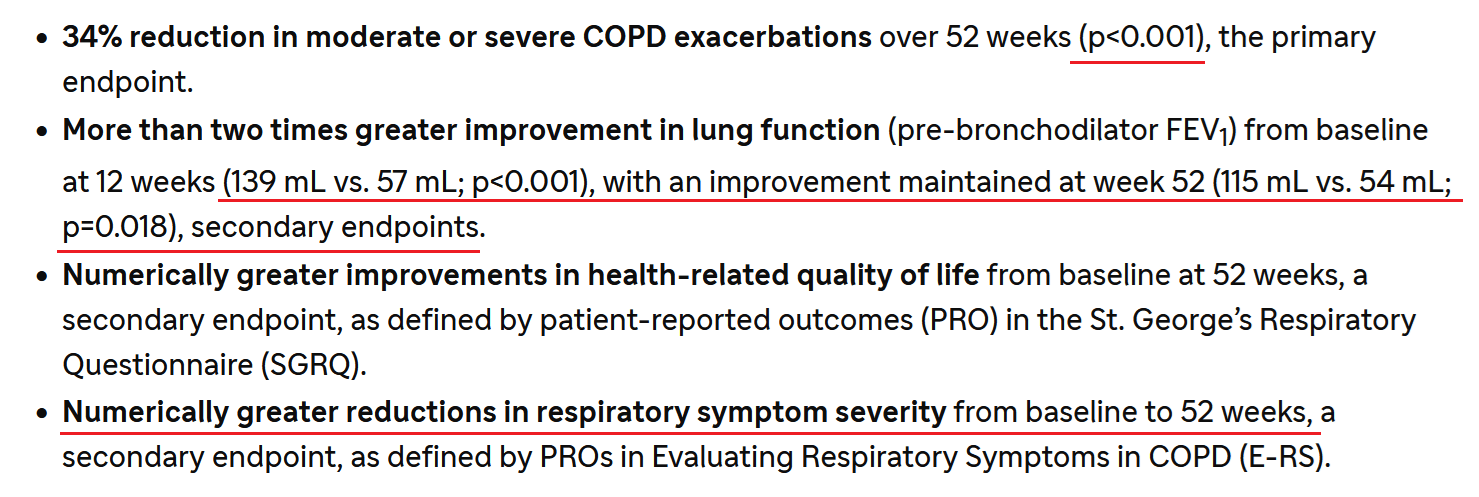

On May 20, 2024, Sanofi announced additional results from a Phase 3 clinical trial evaluating the efficacy and safety profile of Dupixent in patients with uncontrolled chronic obstructive pulmonary disease [COPD], one of the most common chronic inflammatory lung diseases.

So, taking dupilumab led to a statistically significant reduction in exacerbations of moderate/severe COPD compared to the placebo group over 52 weeks. In addition, Sanofi’s medicine helped reduce the severity of various respiratory symptoms and improved the quality of life of participants suffering from this life-threatening condition.

Source: Sanofi

Ultimately, I believe the above data were extremely promising and suggest that, if approved by regulators, Dupixent could become the “gold standard” for the treatment of uncontrolled COPD.

Already at the end of May 2024, Sanofi and Regeneron Pharmaceuticals published news, according to which the European Medicines Agency’s committee made a positive decision on the application for Dupixent for the treatment of patients with this disease. The next stage is the adoption of the EMA’s final decision, which, in my opinion, should be announced before mid-August 2024.

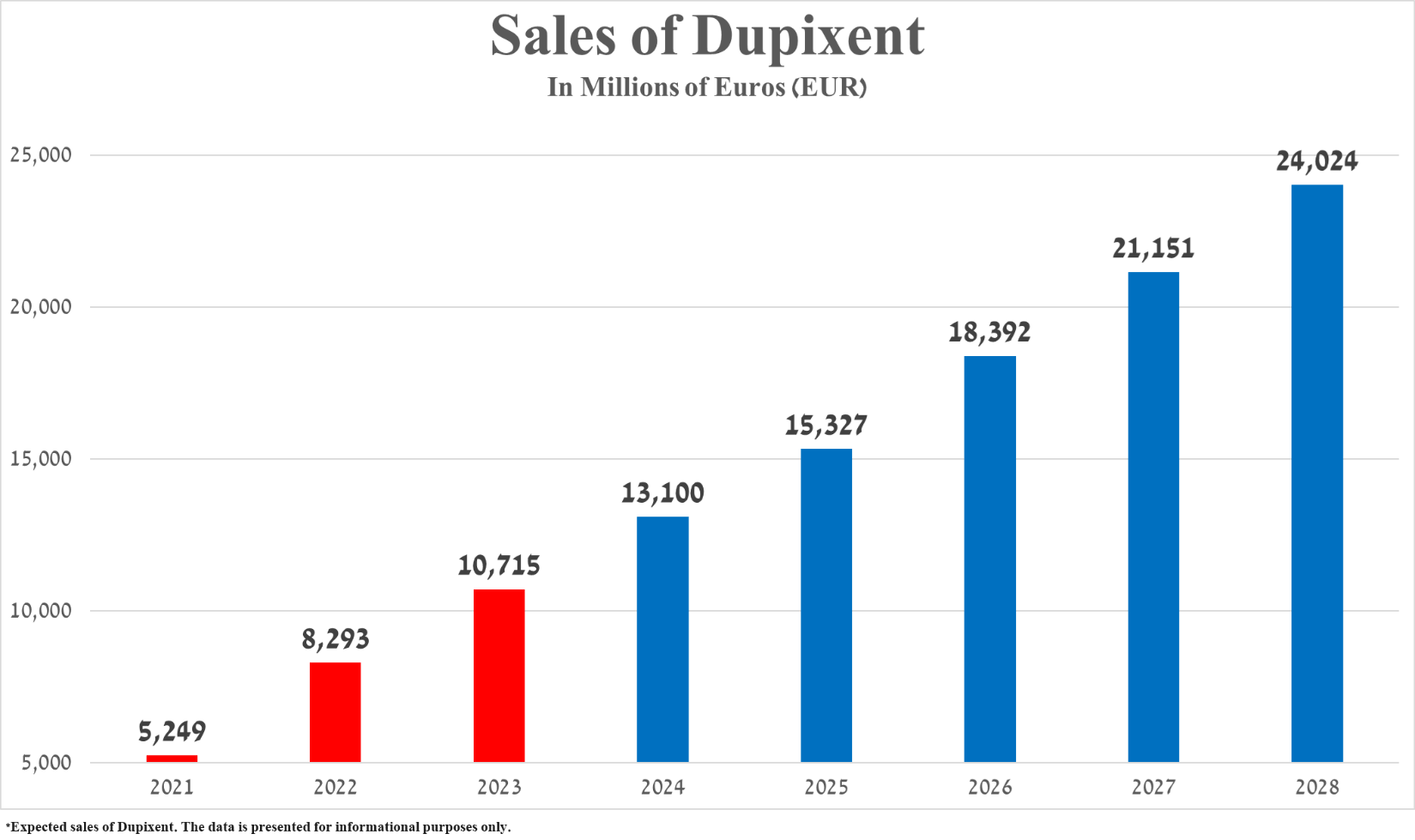

Given the historical growth rate of Dupixent sales, the anticipated expansion of indications for its use, including in the fight against eosinophilic gastritis, bullous pemphigoid, chronic spontaneous urticaria, as well as its competitive advantages over GSK’s Nucala and Novartis (NVS) and Roche’s Xolair (OTCQX:RHHBY), I expect its total sales to reach 24.02 billion euros in 2028.

Source: graph was made by Author based on 10-Ks

Consequently, I’m initiating coverage of Sanofi with a “buy” rating.

Sanofi’s financial position and the prospects for its portfolio of medications

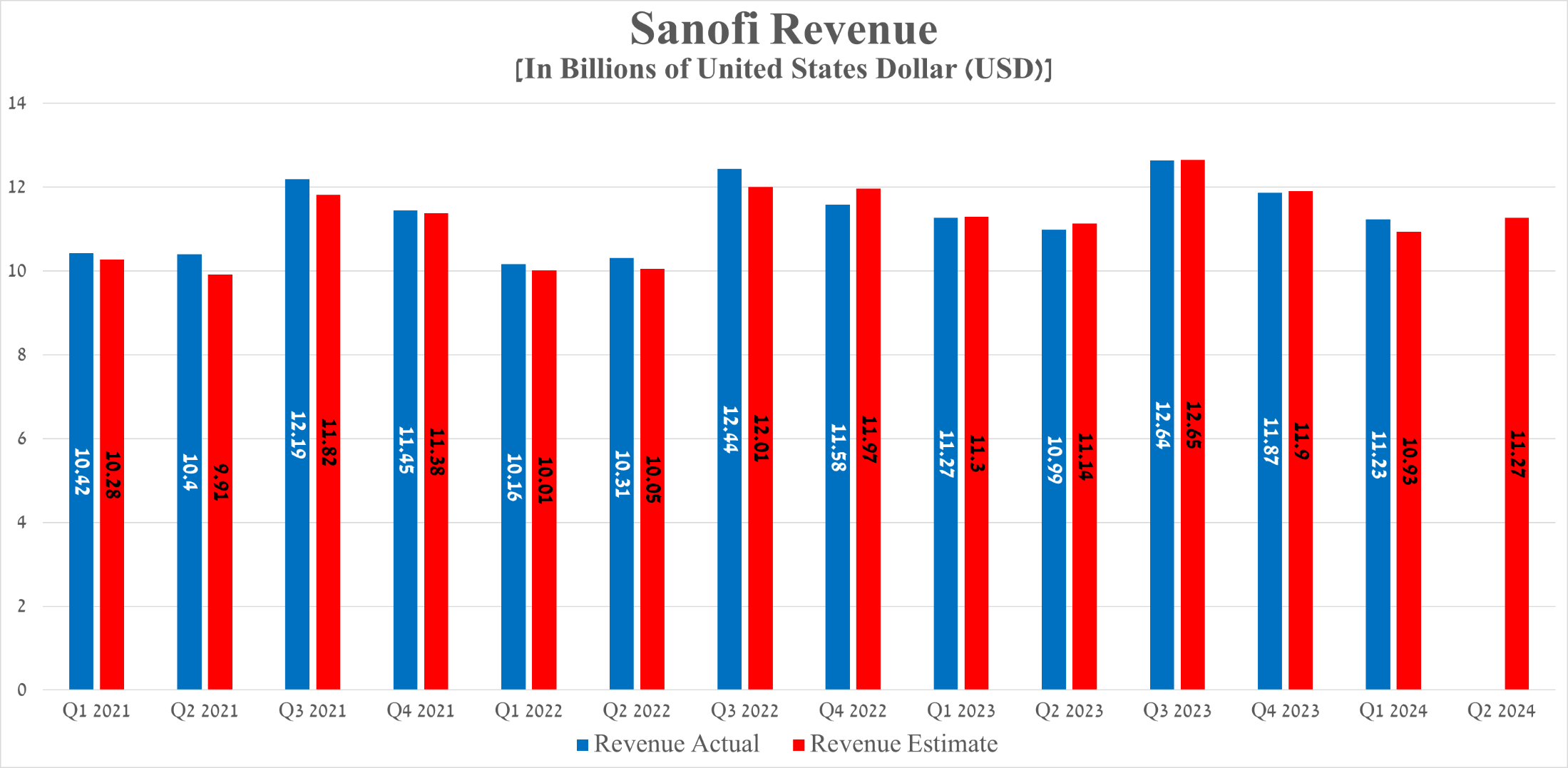

Sanofi’s revenue for the first quarter of 2024 amounted to $11.23 billion, down slightly year-on-year but beating analysts’ expectations by $300 million.

Source: Seeking Alpha

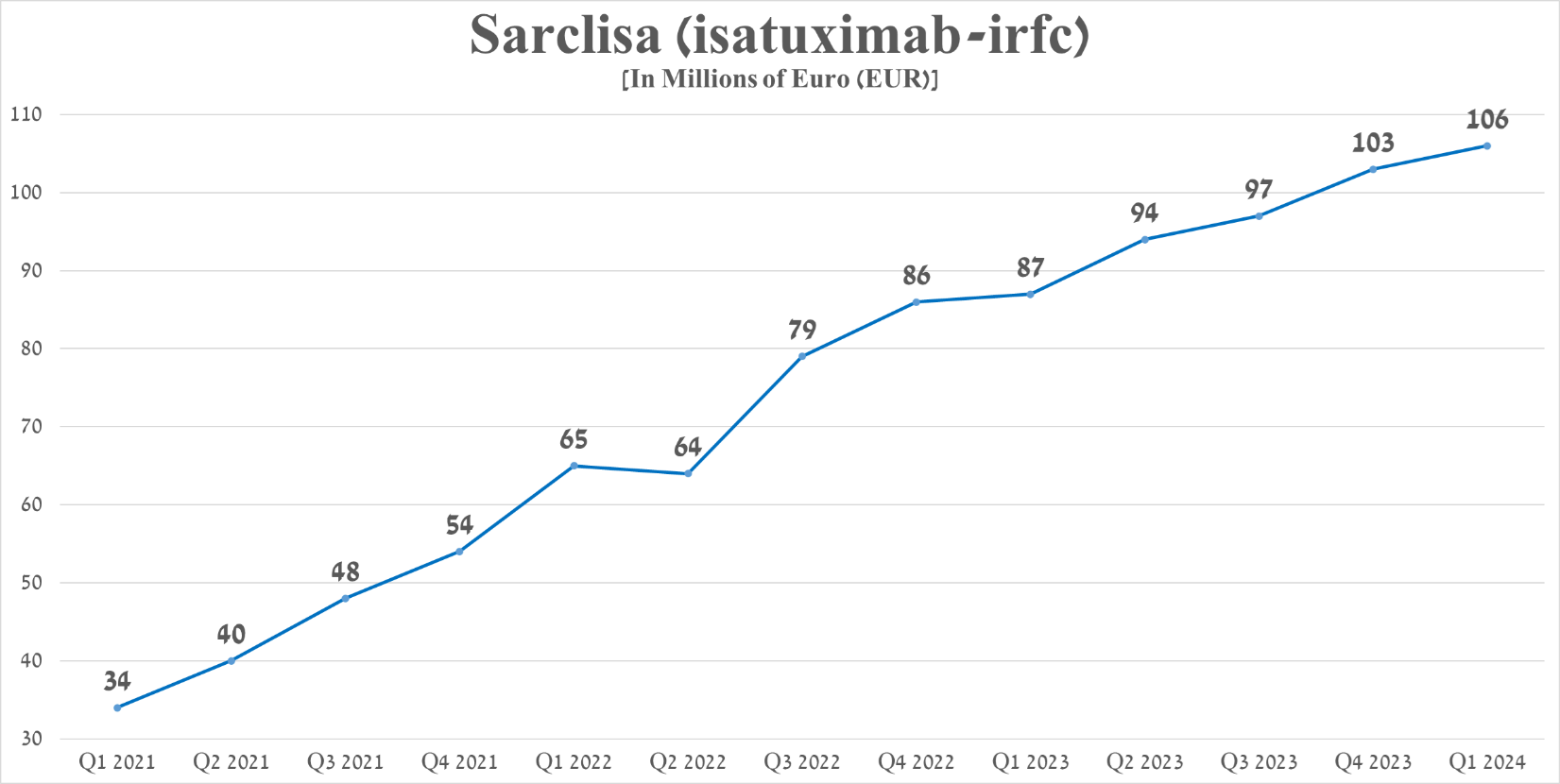

In addition to strong Dupixent sales and increased demand for the company’s vaccines, another key contributor to its year-over-year revenue growth was Sarclisa, an anti-CD38 monoclonal antibody approved by regulators to treat certain patients with multiple myeloma, a type of blood cancer.

Source: table was made by Author based on Sanofi press releases

According to Global Cancer Observatory data, the incidence of multiple myeloma will continue to grow at a rapid rate through 2050, which, coupled with Sarclisa’s promising clinical data and expected label expansion, are the main factors I highlight that will continue to have a significant impact on its demand growth.

Its sales were around €106 million in the first quarter of 2024, up 21.8% year-on-year, thanks to its superior efficacy relative to other monoclonal antibodies, including Bristol-Myers Squibb’s Empliciti (BMY), approved by the FDA and EMA for the treatment of relapsed/refractory multiple myeloma.

Before I move on to discussing an additional contributor to improving Sanofi’s financial position, I want to point out that the analysis of the efficacy of Sarclisa, Empliciti, and other medications was based on press releases from pharmaceutical companies.

Source: graph was made by Author based on 10-Qs and 10-Ks

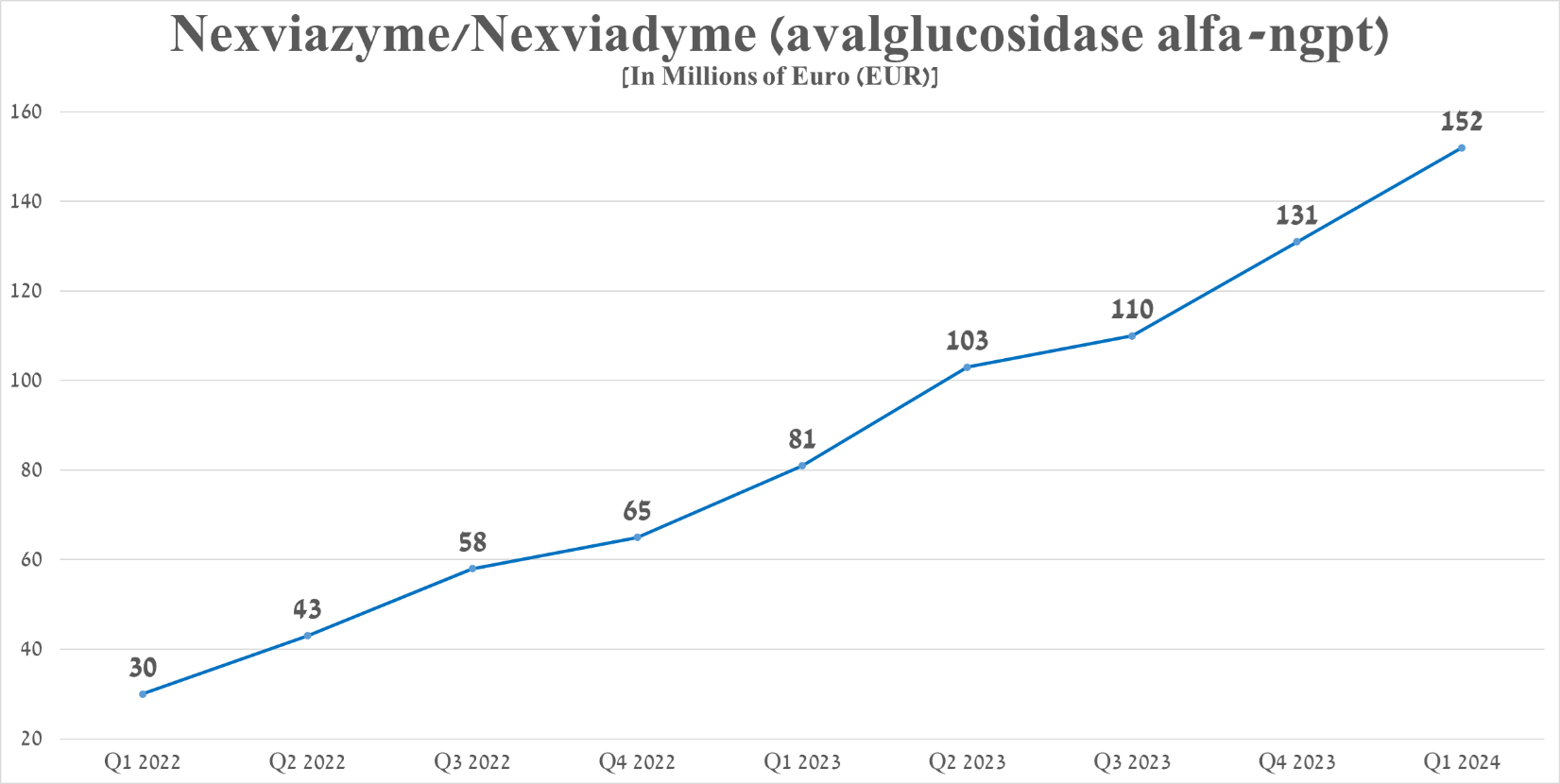

Sanofi has another potential blockbuster in its portfolio of approved drugs, called Nexviazyme/Nexviadyme (avalglucosidase alfa-ngpt). It is an enzyme replacement monotherapy used to treat patients with Pompe disease, a genetic disorder that affects one in 40,000 people in the United States.

Its sales totaled €152 million in the first three months of 2024, up 87.7% year-on-year, driven mainly by increased demand in the United States and the European Union, following promising results in a pivotal clinical trial and patient switching from Myozyme/Lumizyme to Nexviazyme.

Source: graph was made by Author based on 10-Qs and 10-Ks

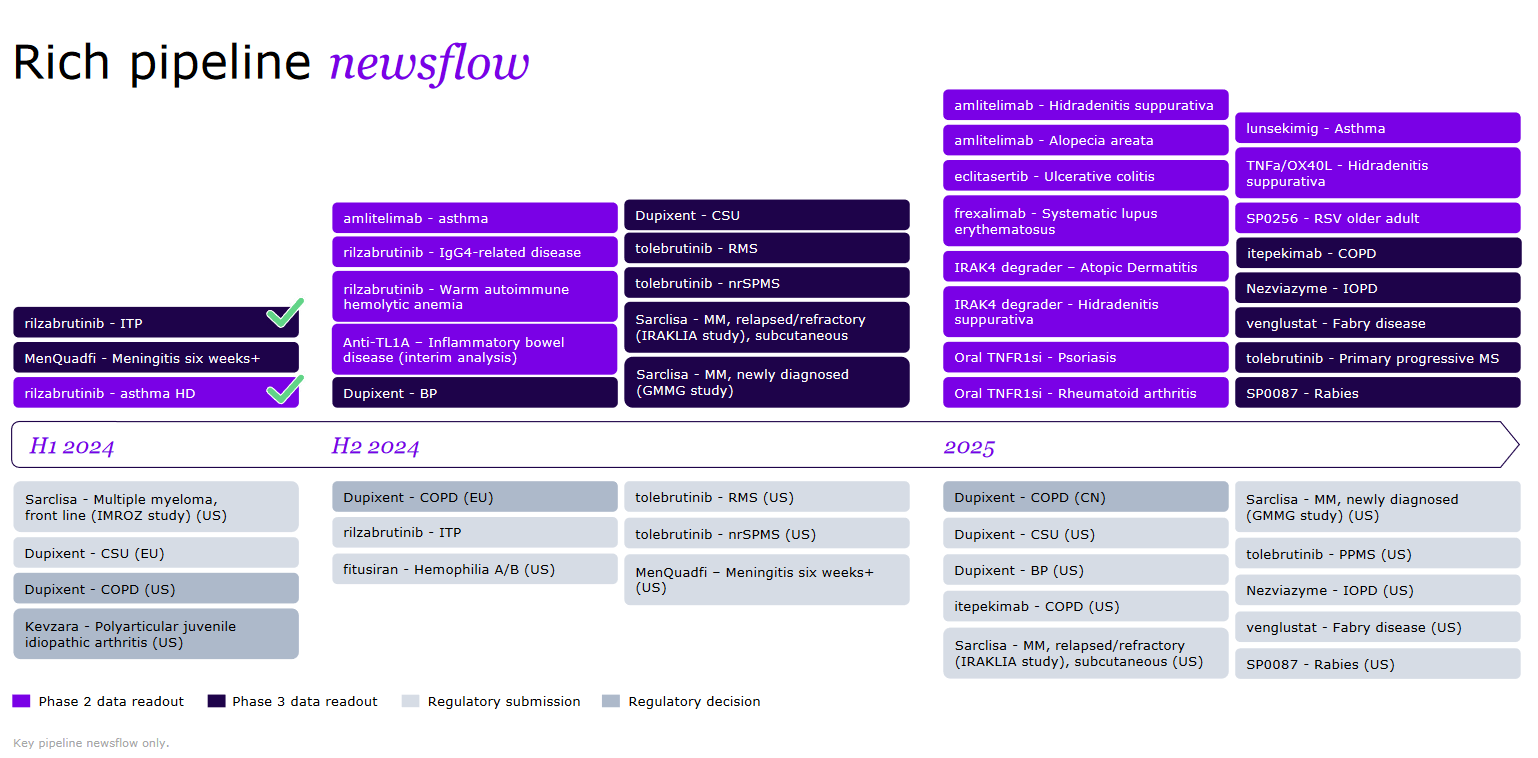

Alongside the growth in sales of Dupixent, Nexviazyme/Nexviadyme, and Sarclisa, the analysis of which was presented by me earlier in the article, I believe that the French pharmaceutical company is making great progress in rejuvenating its portfolio of experimental medications, some of which have a high chance of becoming “gold standards” in the treatment of autoimmune disorders, multiple myeloma, and solid tumors.

Source: Sanofi

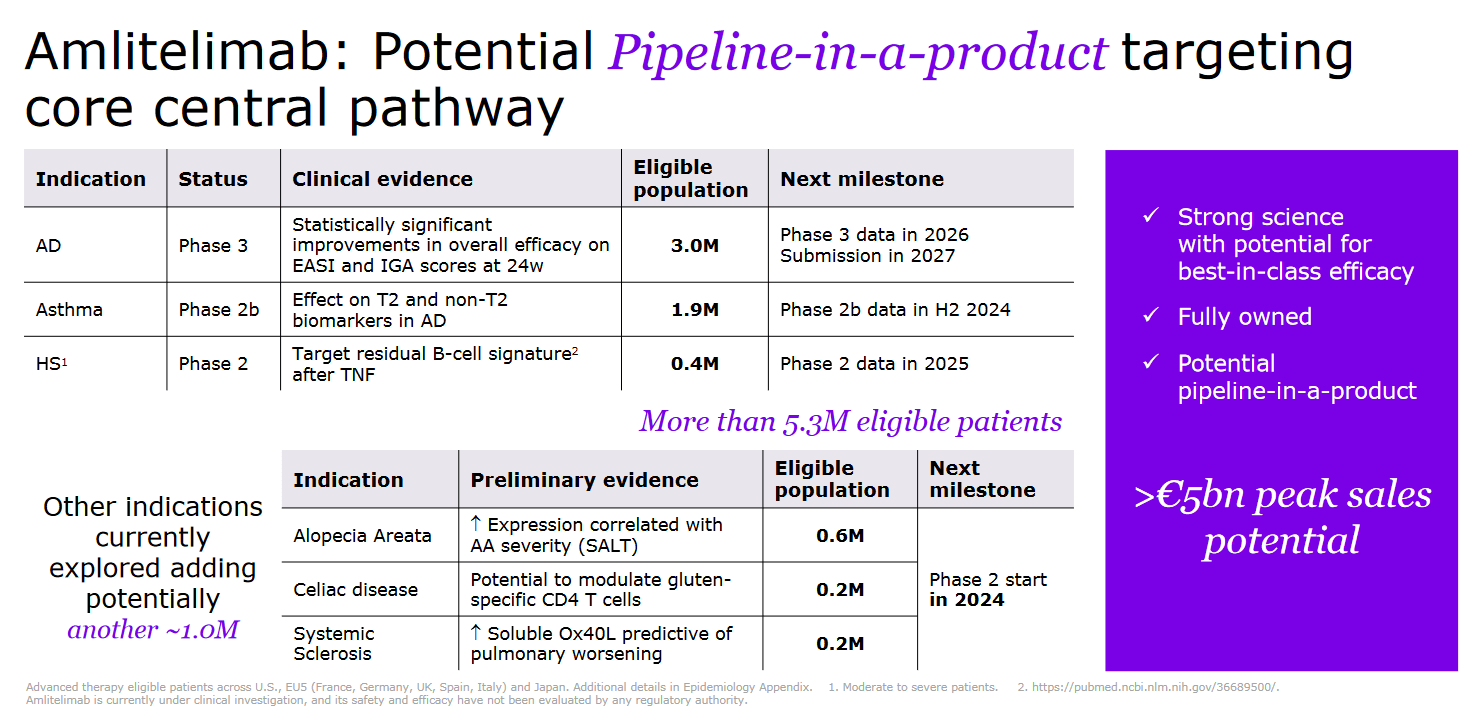

In my assessment, which is based, among other things, on an analysis of a wide range of FDA-approved drugs, as well as those being developed by Sanofi’s competitors, the company’s most promising product candidates are amlitelimab and frexalimab.

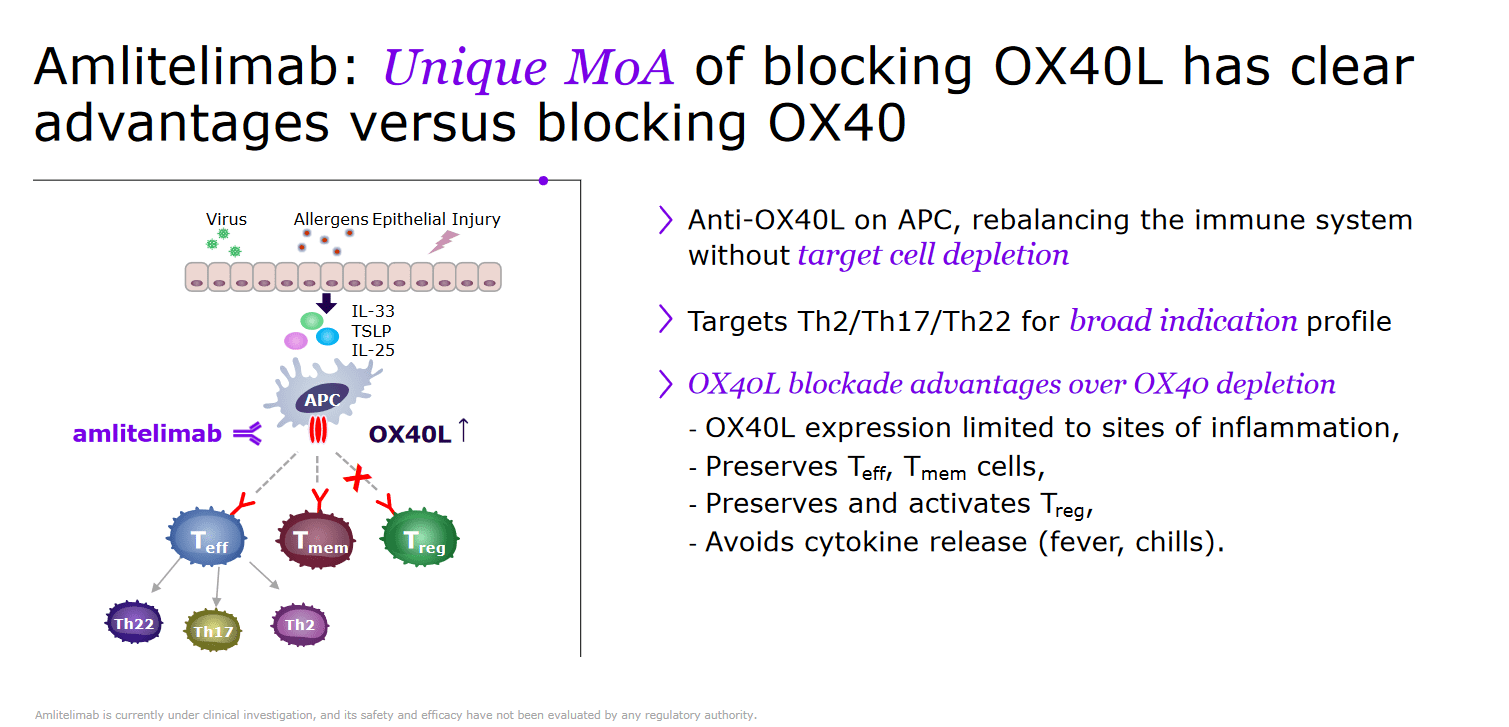

So, amlitelimab is a monoclonal antibody that binds to OX40-ligand (OX40L) and then blocks its interaction with OX40.

Source: Sanofi

Studies show that OX40 and OX40L play a key role in regulating cytokine production by NK and T cells.

In turn, cytokines, or small proteins in simple terms, are involved in regulating the body’s immune response to a broad range of stressful events.

However, in various diseases, including atopic dermatitis and asthma, cytokine regulation is disrupted, which ultimately leads to a significant increase in the level of proinflammatory and Th2 cytokines.

In preclinical and clinical studies, Sanofi’s experimental medication has shown the potential to restore the human body’s harmony between regulatory immune and proinflammatory cells. As a result, I believe this is a strong prerequisite that amlitelimab may be highly effective in combating various inflammatory disorders.

Another competitive advantage of this monoclonal antibody is its lower frequency of administration compared to most FDA-approved medicines, which is one injection every 12 weeks. Sanofi is conducting several additional clinical studies to determine the potential of amlitelimab in the fight against other inflammatory diseases, and expects its peak sales to exceed 5 billion euros.

Source: Sanofi

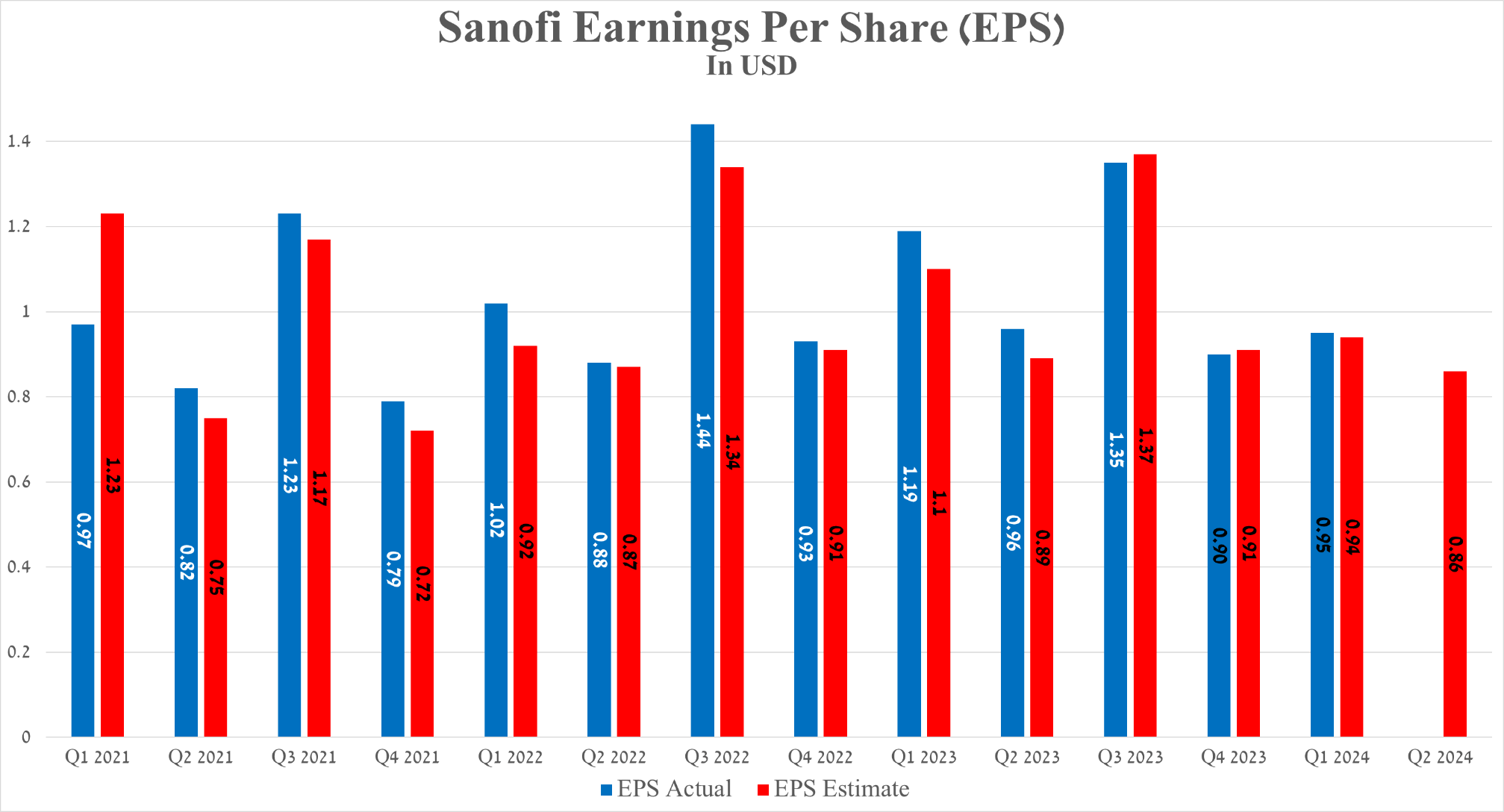

Sanofi’s earnings per share for the first quarter of 2024 were about 95 cents, slightly beating analyst consensus estimates. On the other hand, its EPS is expected to be 86 cents in the second quarter, down about 10% year-on-year, mainly due to an anticipated increase in restructuring costs and the completion of its $1.7 billion acquisition of Inhibrx on May 30, 2024.

The deal added to Sanofi’s portfolio of product candidates INBRX-101, an experimental drug that has shown extremely high efficacy in a Phase 1 clinical trial for alpha-1 antitrypsin deficiency, one of the most common hereditary disorders in adults.

Source: Seeking Alpha

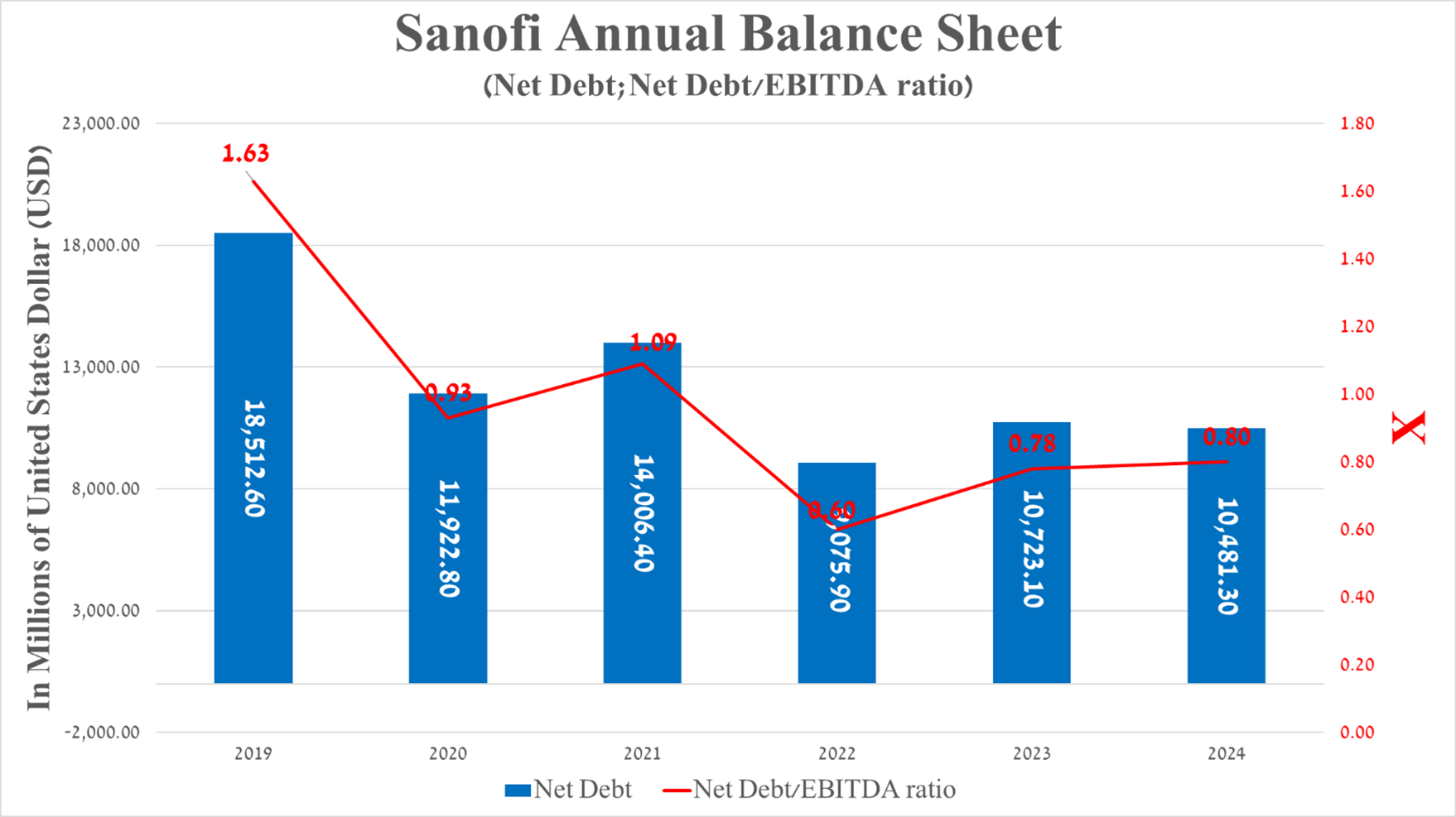

It is equally important to discuss Sanofi’s debt, which, in my estimation, not only does not pose a significant financial risk to its position but also, given its total cash and cash equivalents of €9.18 billion, will allow the French pharmaceutical company to continue to pursue an aggressive R&D policy.

Source: Seeking Alpha

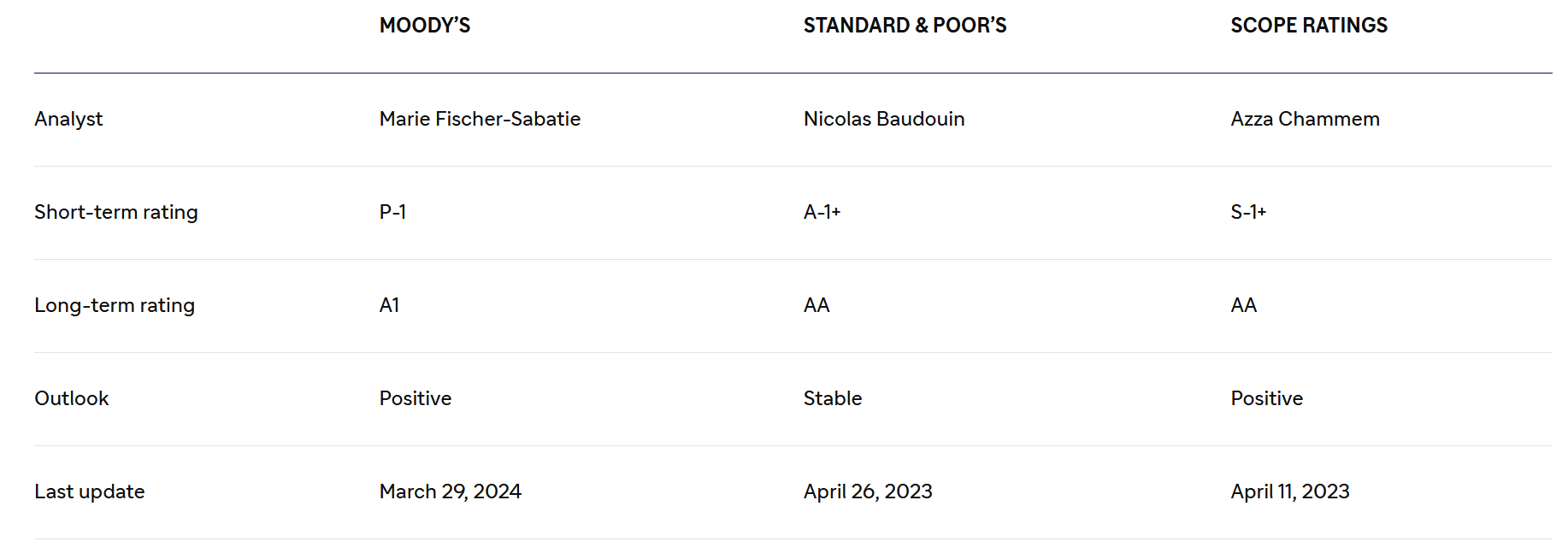

So, its net debt amounted to about $10.48 billion at the end of March 2024, slightly decreasing compared to 2023. Also, I want to note that Sanofi’s net debt/EBITDA ratio continues to remain below 1x, which is also reflected in its investment-grade credit rating.

Source: Sanofi

Risks

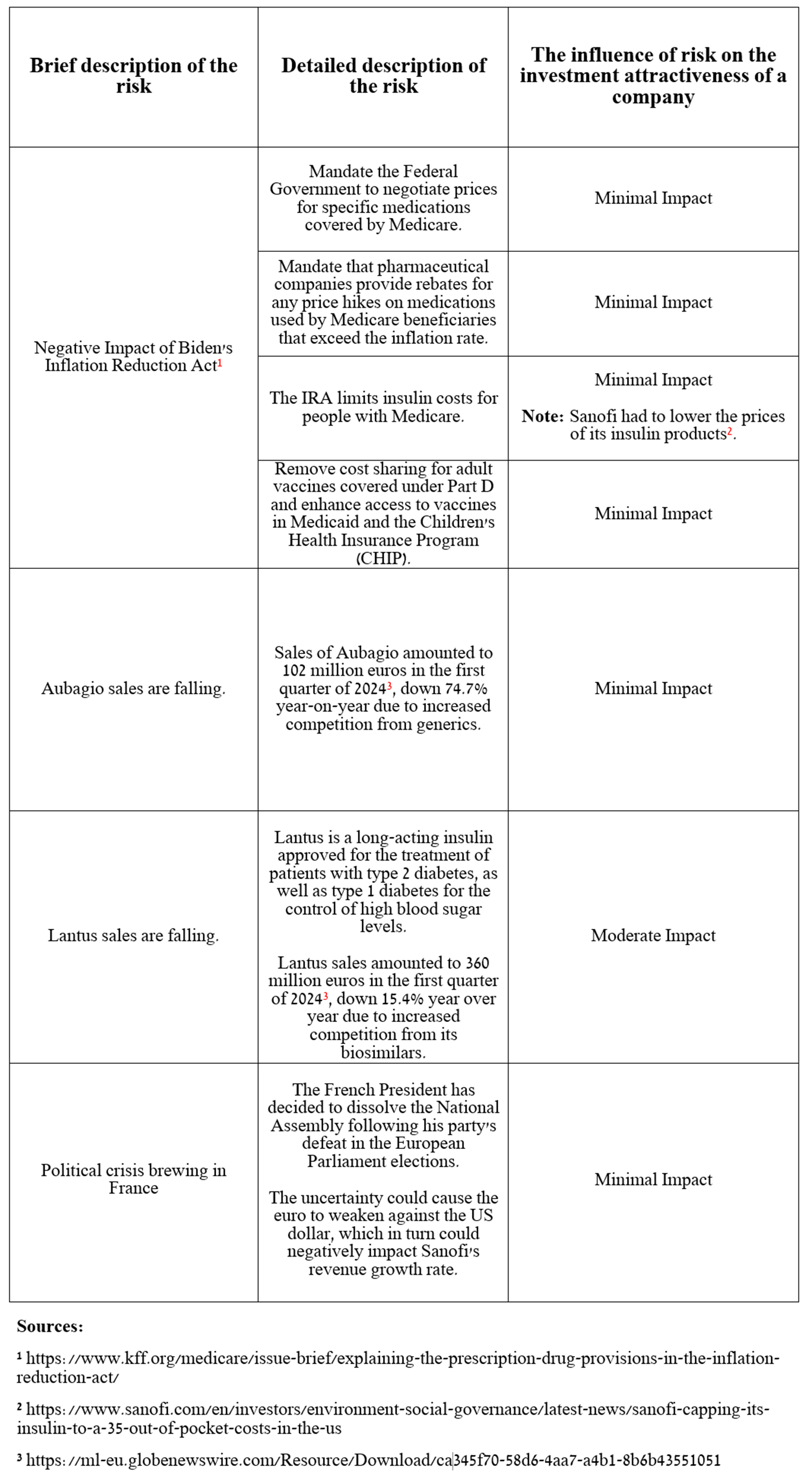

Before moving on to the conclusion, I would like to note the following risks that may negatively affect the investment attractiveness of Sanofi in the medium and long term.

Source: table was made by Author

Takeaway

Sanofi has pleased investors in recent months with strong growth in sales of its key blockbusters, and continues to make significant progress in developing its rich portfolio of product candidates.

So, one of the company’s most recent achievements was the publication of the results of a pivotal clinical trial on June 3, 2024, which demonstrated the extremely high efficacy of Sarclisa in the treatment of transplant-ineligible adults with newly diagnosed multiple myeloma [NDMM]. These results were beyond my expectations.

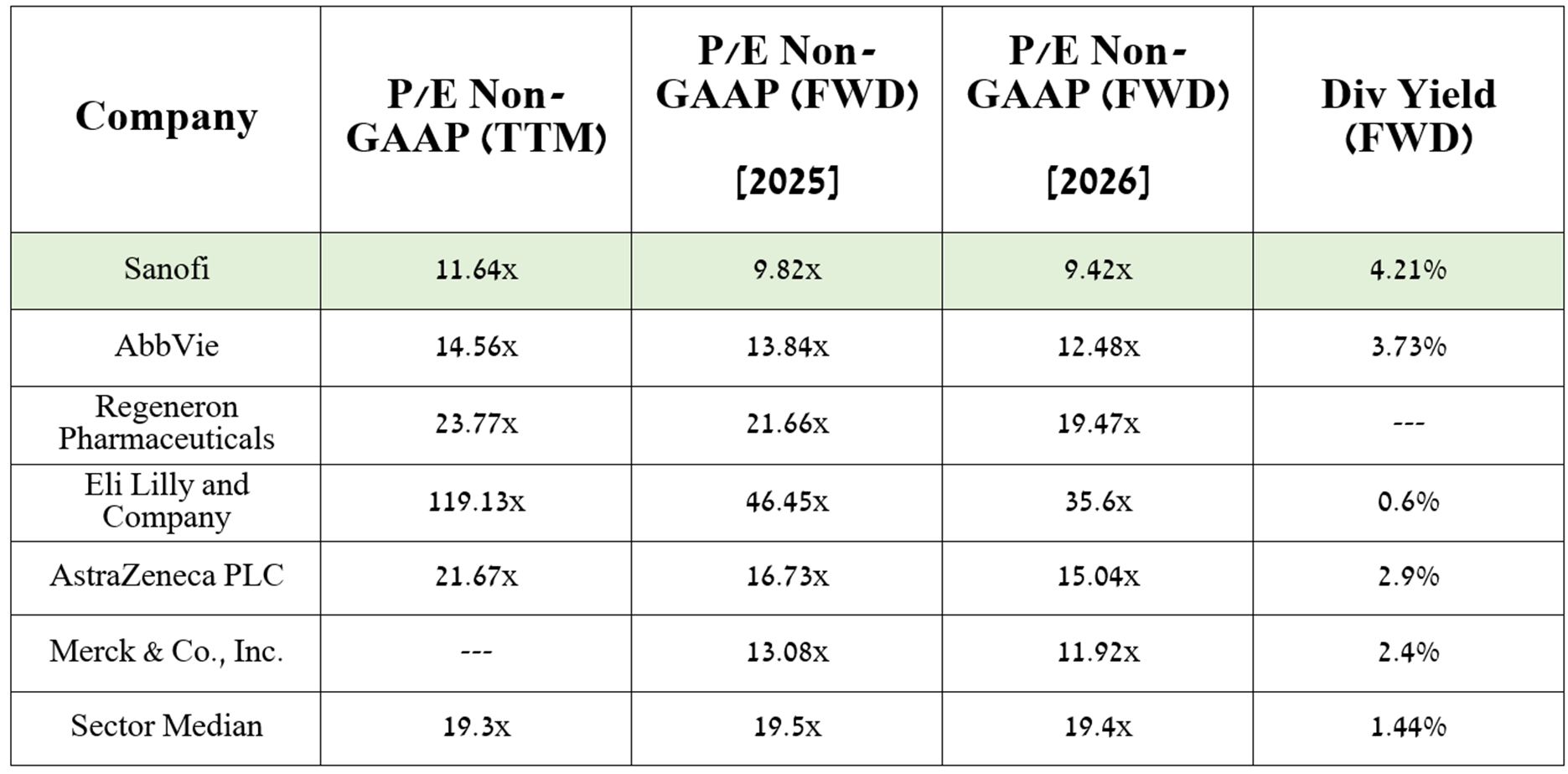

In my estimation and analysts’ expectations, thanks to the FDA-approved medications, as well as amlitelimab, frexalimab, and the label expansions for Dupixent and Sarclisa, the company’s EPS in 2026 will reach 9.42x.

Source: Seeking Alpha

As a result, this indicates that it is trading at a discount to many of its healthcare peers, as noted in the table above, and given its dividend yield of over 4%, I believe Sanofi represents a potential investment opportunity for long-term investors, contrary to current market sentiment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment