CaraMaria

Introduction

Safe Bulkers (NYSE:SB) is a dry bulk owner and operator with a fleet of 44 on-the-water vessels plus an additional nine newbuilds set to be delivered from 2023 through 2025. SB has historically traded at a premium valuation relative to peers despite the related-party structure, but it recently lost its luster as its peers prioritized substantial dividend payouts while the company focused on deleveraging and renewing the fleet.

The company is now trading at an enticing discount to net asset value, whereas what was previously viewed as a meager dividend distribution has become increasingly significant, while the company resorted to share repurchases throughout H2-22 to accrete shareholder value. I like the asymmetry the company provides: if bulker rates fare strongly going forward, the company’s leverage and prevailing discount to NAV should allow it to outperform most of its peers, whereas if rates remain at lackluster levels, the company should fare decently nonetheless given the aforementioned discount to NAV and a dividend that should be better defended than variable dividend policies.

The Current State of Affairs on the Bulker Market

After a decade of lackluster rates (2010-2020), the overall dry bulk market improved significantly going into 2021, providing much needed respite to shipowners in the sector, some of which carried heavily indebted balance sheets (that is the case of SB). However, part of the strength in rates was attributable to inefficiencies caused by COVID (mostly port congestion), which have eased over the past few months, pressuring rates to the downside.

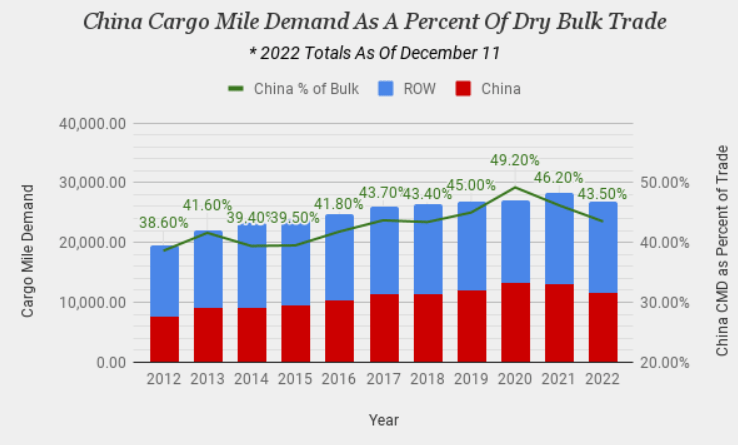

Furthermore, the draconian measures to fight COVID in China weighed on economic activity in the region (which is, by far, the biggest importer of dry commodities, and thus needs to be carefully examined). Chinese seaborne iron ore, coking coal, and thermal coal imports are forecasted to finish the year down by an estimated 1%, 5%, and 17% respectively.

2022 Full Year Shipping Charts & Commentary, by James Catlin for Value Investor’s Edge.

Coal imports have been under pressure given China’s focus on increasing domestic supply, which makes sense considering the strength we have seen in coal pricing and on the USD (which exacerbates its expensiveness). Iron ore imports have been under limited pressure mostly given the weakening property/real estate market in the region. Since the Evergrande debacle, the property market has been under pressure, and new starts (on a square footage basis) are down an estimated 38% on the January to October period.

Considering the real estate market represents around a third of total Chinese steel demand, as long as we don’t see some kind of strengthening, iron ore demand should remain subdued (analysts initially expect another mild decrease in demand y/y in 2023). Overall, despite all the doom and gloom, Chinese imports have held up decently throughout 2022 despite the zero-COVID policy.

As the region reopens, I would not be surprised to initially see an increase in inefficiencies as previously non-infected individuals get the virus for the first time, potentially wreaking havoc in the near-term. Though, as herd immunity is achieved, China’s economy should tend to improve, leading the way to higher demand for dry commodities (as well as for oil and gas).

Minor bulks have been one of the sub-segments where the weaker Chinese industrial trends (as well as overall macroeconomic headwinds) have been felt. If China effectively reopens, we should expect an improvement in demand, which should positively affect smaller vessel classes. Grain volumes have been under pressure due to the war in Ukraine but changing trading patterns have offset part of the ton-mile demand declines. Overall, rates were mediocre throughout H2-2022 for several reasons, but easing inefficiencies and the slump in the Chinese property sector stand out.

The demand side for dry commodities remains uncertain going into 2023; coal volumes have been a tailwind throughout 2022 (Europe has increased substantially its imports), but it remains to be seen whether that will remain the case in 2023. However, China’s reopening should be a positive, albeit it will certainly have its up and downs.

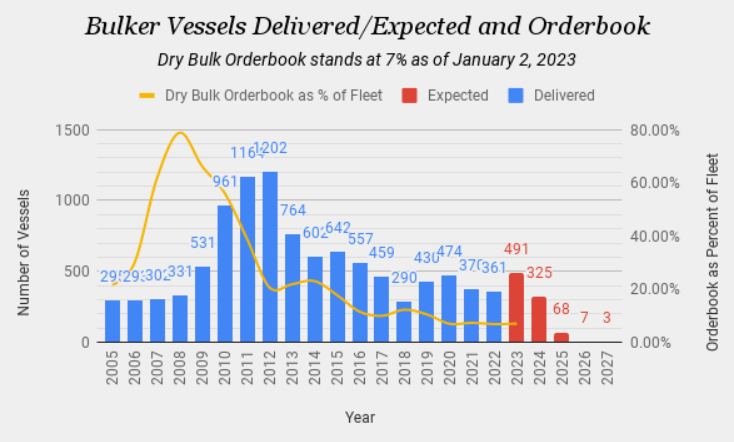

Despite the mixed demand outlook, the sector’s attractiveness is primarily supply-based with a tiny orderbook by historical standards, currently estimated at just 7% of the fleet. Furthermore, and despite its currently low standing, I would not be surprised to see further declines going forward given the murky macroeconomic outlook and uncertainty regarding future environmental regulations. Moreover, the EEXI regulation will be enforced starting in 2023, potentially reducing vessel supply (the impact should be limited, but is a positive, nonetheless). The CII regulation will also be enacted starting in 2023, but its impact will be spread out as guidelines become increasingly strict.

2022 Full Year Shipping Charts & Commentary, by James Catlin for Value Investor’s Edge.

Overall, despite the attractive supply side, there are still several clouds on the horizon for dry bulk owners. If a global recession materializes, we could be looking at weaker market balances given the downward pressure that would exert on global commodities demand. After all, the shipping industry is well known for its volatility, and that’s a double-edged sword.

Safe Bulkers’ Fleet & Charterbook

SB owns a fleet of 44 on-the-water vessels with an additional nine vessels on order (to be delivered between Q1-23 and Q1-25). The company operates its fleet with a mixture of time charters (fixed and floating) and spot voyages, which helps smooth out earnings volatility a tad.

The fixed time charter cover is mostly on Capesizes, where five out of the eight assets are chartered out for at least one year (one of the contracts runs until September 2031!). The company also has some shorter-term cover on the Kamsarmaxes and the Panamaxes. The company’s full fleet positioning can be reviewed on the Q3-22 earnings release. Lower headline rates will certainly take their toll on overall results, but the company’s charter cover on their Capesizes coupled with a decent amount of modern eco tonnage should allow them to operationally outperform most of their peers.

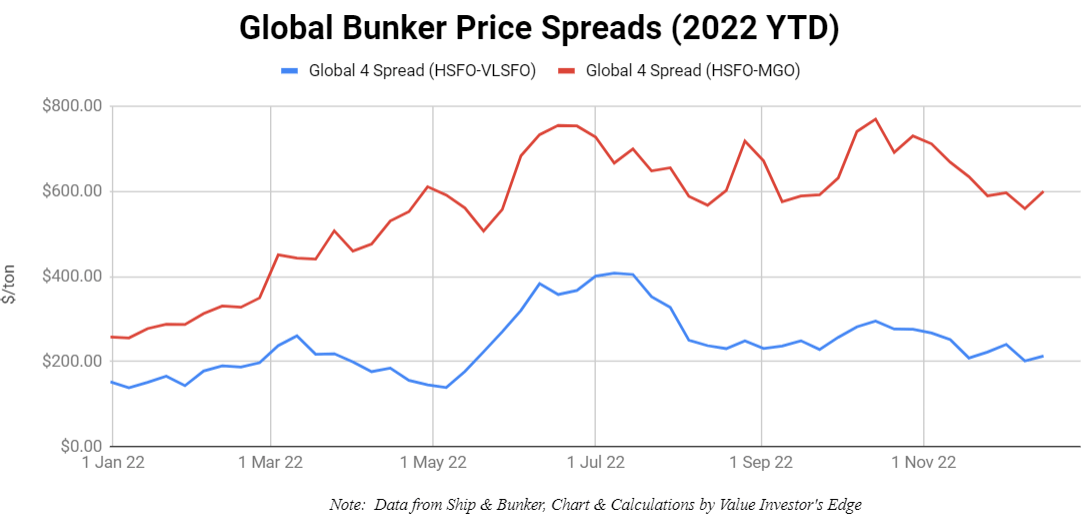

Additionally, it is relevant to keep in mind SB has 18 scrubber-fitted vessels, and the company is planning to install another five devices this year. The spread between HSFO and VLSFO has been remarkably strong throughout the year, providing a substantial tailwind to scrubber-equipped vessels. Overall, considering the paybacks scrubber investments generate in the current environment, I believe it makes sense to pursue some additional installations (especially if rates are low, which reduces offhire opportunity costs).

Value Investor’s Edge Live Analytics Platform

Capital Allocation

Throughout 2021 and 2022, as most bulker peers ramped up their dividend distributions with Star Bulk Carriers (SBLK) and Golden Ocean (GOGL) at the forefront (followed by Eagle Bulk (EGLE), Genco Shipping (GNK), etc.), SB followed a different strategy. The company started the upturn with a rickety balance sheet, whereas management also decided to pursue an aggressive fleet renewal program. The company ordered eleven vessels (two of which have already been delivered), and they also completed a second-hand Capesize vessel acquisition (while disposing of some of their older tonnage). Furthermore, the company also used its ATM authorization to issue 19.4M shares throughout late-2020 and 2021 (the company was trading above NAV at the time).

From a valuation standpoint, these decisions most likely weighed on the company’s relative valuation. SB has historically traded at a solid premium to NAV, but over the past couple of years it has lost its luster as investors have preferred to invest in companies with solid dividend distribution policies. To take advantage of the sizable discount to NAV, the company instituted a share repurchase program last summer for up to 5M shares. As of November 4th, SB had already repurchased 2.8M shares. If the share repurchase program is fully executed, the company will have bought back approximately 4% of its outstanding capital. Since shares continue to trade at a massive discount to NAV, we might also see this authorization expanded further during 2023.

Safe Bulkers also initiated a $0.05/sh quarterly distribution in early2022. Although this represented a negligible portion of net income and FCF in booming times, it now offers a decent yield of about 7%. Over the past few months, management has reiterated they wanted to have a dividend that is sustainable in the longer run, so I don’t expect to see a cut in the near-term even if rates are weaker in 2023 (although of course there is no guarantee!).

Overall, SB’s management has taken a very conservative approach over the past couple years, preserving capital to renew the fleet and lower leverage levels. Although this has weighed on the company’s relative valuation given investor’s understandable preference for big shareholder returns, the company has not destroyed equity value. Going forward, I expect the company to focus on maintaining balance sheet strength.

Financial Position

The 2021 and early-2022 upturn in rates had a very positive effect on SB’s balance sheet. As of the end of Q3-22, the company had $121.7M in cash, which compares to $455.6M in debt and lease liabilities. Additionally, we also must include the net proceeds (estimated at around $10M) from the sale of the “MV Pedhoulas Trader”, a 2006-built Kamsarmax, which was delivered in December.

On the liability side, we also must include around $100M in preferred outstanding (series C and D). Therefore, as of quarter end, the company had a total net debt position of approximately $434M. However, given the company’s extensive newbuilds program, I believe the remaining capital expenditure requirements should be included as well; as of Q3-end, the company still had to pay $250M in relation to the nine newbuilds on order.

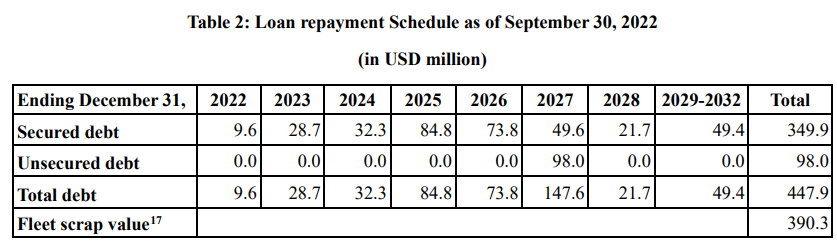

Given the company’s prevailing market capitalization, it may seem they may encounter a difficult time in 2023 or 2024 if markets are weak since their debt load is significant relative to their market cap; however, the market cap is misleadingly low due to the huge discount to NAV and SB has an attractive debt repayment schedule, as can be seen in the image below. Additionally, they have $144.3M in undrawn borrowing capacity under existing revolving credit facilities.

Safe Bulker’s Q3 earnings release, page 5.

Despite the company’s substantial fleet renewal plan, leverage remains manageable at around 50% D/A (the denominator is the current market value of assets, not the asset book values on the balance sheet) when including the remaining obligations under the newbuild program. The risk would be that asset valuations could fall further in a mediocre or weak market rate environment. There is some risk here, especially if a global recession ultimately materializes and demand comes under pressure. However, should that happen, SB’s discount to NAV arguably acts as a sort of ‘margin of safety’, potentially softening the blow relative to most other peers.

Conclusion

China reopening its economy should be a positive for dry bulk markets, but it is a far more nuanced situation considering the weakening real estate sector as well as the potential for weaker economic performance in the near future (which could exacerbate the usual seasonality) as COVID ravages throughout the region.

I am not making a directional call on the bulker market; the orderbook is sitting at attractive levels, whereas the EEXI should provide a tailwind regarding effective vessel supply in 2023, but concerns over the global economy as well as on China specifically are reason enough to be nimble. As long as the Chinese real estate sector continues to languish, Capesize rates will most likely remain under pressure.

Safe Bulkers is at an interesting juncture. The company is sitting at an abnormally high discount to NAV (especially relative to its historical overvaluation on the same metric), while the firm also owns a decently modern fleet with several scrubbers installed along with some charter cover at higher fixed rates.

Overall, I believe SB offers an asymmetrical risk-reward proposition at current pricing; given its higher leverage and significant discount to NAV. If the market strengthens going forward, the company should fetch very decent performance. On the other hand, should rates fare weakly going forward, the common equity is in an adequate position to withstand the storm given the limited charter cover and the significant discount to NAV.

Be the first to comment