Kwarkot/iStock via Getty Images

Investment Thesis

Sachem Capital (NYSE:SACH) is a loan provider focusing on developmental real estate loans. Namely, Sachem provides shorter-term real estate funding (12-36-month terms) on secured first-lien investment properties. Geographically, Sachem has the most customers in Connecticut and Southern Florida but will lend anywhere in the United States.

The customer base is developers who wish to acquire and renovate existing property or acquire vacant land for a quick turnover on building a residential property.

As Sachem is a REIT, 90% of income must be distributed to shareholders. In 1Q22, Sachem announced a 16% quarter-over-quarter increase in the dividend for 2Q22 – bringing the forward yield to 12.9%. With real estate being historically underdeveloped in the last decade and vacancies at an all-time low, Sachem has a significant advantage with its short-term loans as developers are committed to fast turnaround projects rather than higher-risk large multiyear ventures. For this reason, we believe that Sachem is a good choice for high income from real estate.

|

Sachem Capital |

FY2021 |

E2022 |

E2023 |

|

Price-to-Sales |

5.5 |

3.2 |

2.4 |

|

Price-to-Earnings |

9.9 |

7.6 |

6.5 |

|

Net Income Margin |

37.7% |

33.0% |

36.9% |

General Overview

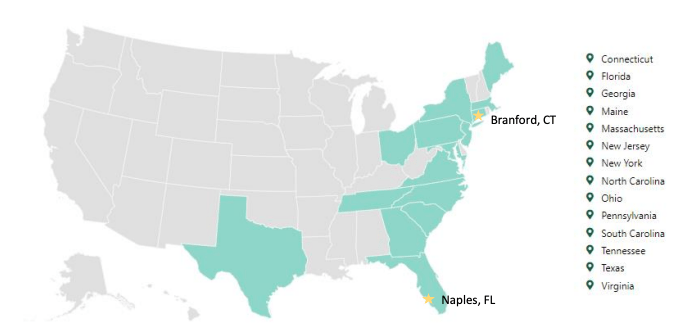

Sachem operates in 14 key markets, with a total asset under management (AUM) of just over $500 million, made up of 500 current loans.

Sachem leverages relationships with existing borrowers or referrals from real estate brokers or banks. As Sachem is not a traditional lender, they are primarily looking at collateral value when deciding on a loan, which may include personal guarantees, other property, or equity in the project. Extensive due diligence including on-site visits is conducted to evaluate the property itself and the area around it to confirm viability. Of course, standard loan due diligence applies through researching financial and operational data provided by the borrower’s history also apply. Sachem’s concentration risk is managed to limit exposure, but still has 55.1% of properties in CT and 18.2% in Florida. If a good investment in an area would further an already heavily concentrated area, the loan may be declined. As a result of this and other underwriting criteria, Sachem has an industry-low default rate of 3.1% as of FY21.

SACH investor presentation

While most other lenders focus on cash flows or credit of the developer, Sachem primarily looks at the value in the collateral provided, which is often less susceptible to swings in the housing market. Sachem’s latest initiative is a repositioning toward larger principal loans with more experienced developers. The average loan size has grown to $562,000 in FY21, with an average term maturity decreasing to 8 months.

Real Estate Market Dynamics

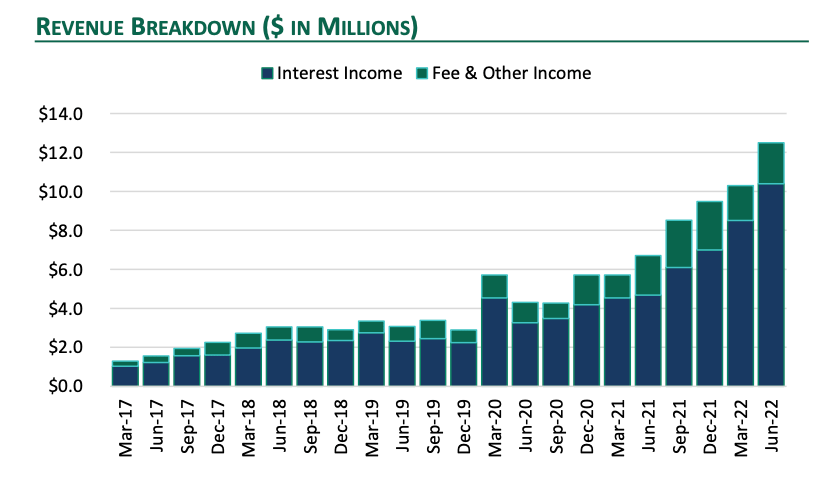

In FY21, Sachem broke a revenue record and is on track to do it again in FY22. As of 2Q22, it has 503 current loans, a 5.3% increase year over year. This small increase in volume is mostly made up of loans with much higher principal values to experienced developers. Over the same time period, total outstanding loan amount increased 83.9%, leading to a 122.8% increase in interest income within the portfolio. Overall, in 2Q22, revenue has increased 86.9% year over year.

apricitas.io

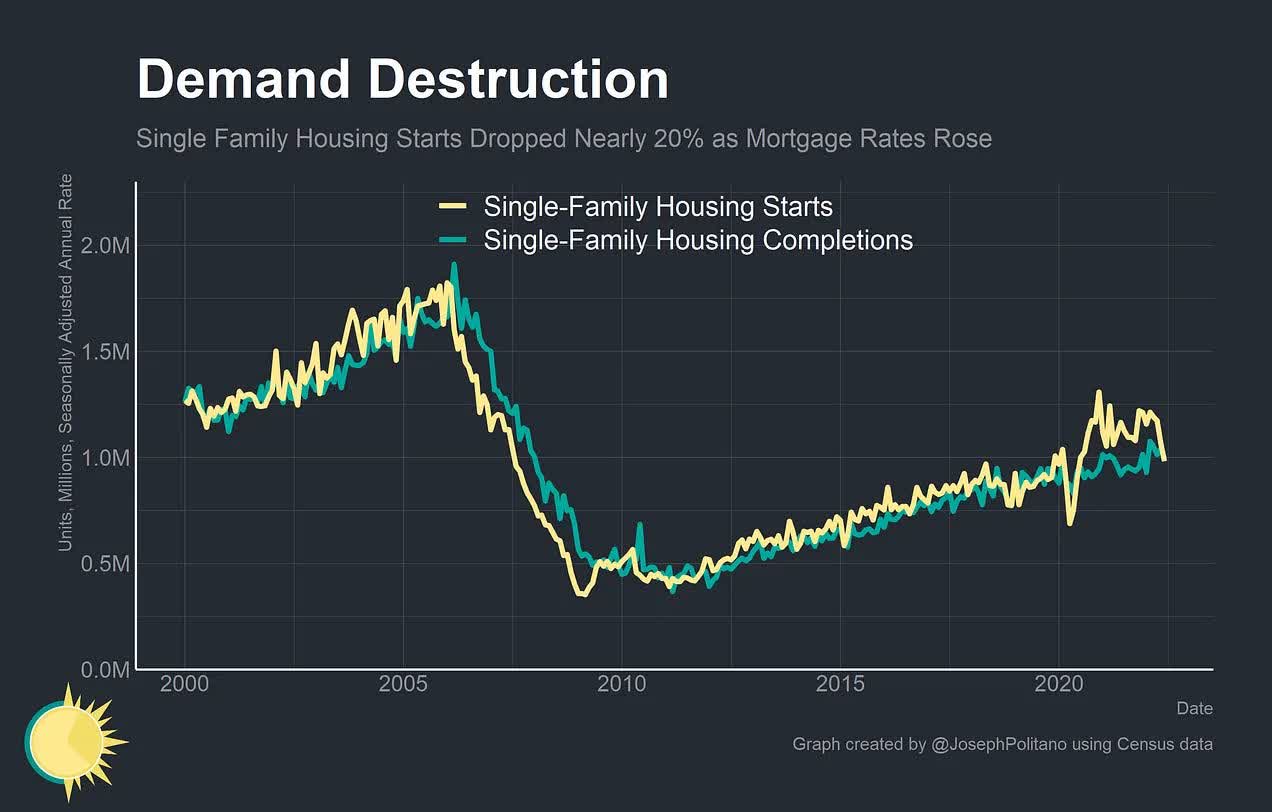

There is a veritable perfect storm in real estate markets presently. 80% of housing stock was built before 2000, and historically low vacancies in rentals and homes. Despite the last decade being rich in equity financing, there has been a definitive underdevelopment in housing.

The Small Business Administration (SBA) takes approximately 2-3 months at best to approve loans of this size for this purpose, with particularly large loans taking upwards of 6 months. Even traditional bank financing can take a similar timeframe. Sachem boasts that it can close a loan in as little time as 5 days, giving it the flexibility to adapt very quickly to market changes.

Risk Profile of Portfolio

All loans issued by Sachem are first mortgage lien, meaning they have a primary claim to real estate properties should the borrower default. It maintains a targeted loan-to-value ratio of 70%, which is conservative. Because of this high LTV, the portfolio yield is 11.3% with interest rates being 6.9% at the lowest.

1H22 presentation from SACH

To fund a large expanse of new loans (170% volume increase in 5 years, 58% CAGR over the same period) Sachem uses debt financing and a large line of credit from Wells Fargo (WFC). Sachem’s lines of credit tend to be below the prime rate, with the Wells Fargo line of credit being only 1.5% at the end of FY21 (the prime rate over the same period was 3.25%).

With dynamics in the market changing quickly, it is advantageous that Sachem maintains a loan portfolio with 92.3% of loans expiring in 2022. Though this does lead to the price-to-book value of Sachem being lower than the sector average, it creates a stronger balance sheet over the long term, allowing Sachem to regularly outpace the sector for dividend yields.

|

(End of Year) |

2018 |

2019 |

2020 |

2021 |

|

Total Assets (in millions of $) |

86.0 |

141.2 |

266.7 |

416.9 |

|

Number of Loans Outstanding |

403 |

438 |

495 |

520 |

|

Remaining Principal Of all Loans |

78.9 |

94.5 |

155.6 |

292.3 |

|

Weighted Average Interest (excluding fee) |

12.9% |

12.4% |

11.8% |

11.6% |

|

Average Term Length |

11 |

10 |

8 |

8 |

|

Foreclosure Rate |

3.2% |

2.1% |

3.2% |

3.1% |

Risk

Sachem is a REIT, which provides certain advantages while investing in real estate. However, this also means that at least 75% of total assets must be in real estate, cash, or treasuries. During a real estate market downturn, this qualification could severely limit Sachem’s ability to earn revenue. However, due to Sachem’s ability to adapt to market dynamics, we do not believe that it would pose a long-term threat to the company.

Conclusion

Despite rates having been at rock bottom for the last 14 years, there was a definitive downtick in the amount of new housing being constructed. There has been a significant push across the economy and political sphere to alleviate the cost of living crisis tied to housing. Sachem can not only capitalize on this but will also thrive in this environment as it can offer bridging loans to experienced developers and house flippers alike. It has a very fast approval time, as little as 5 days, compared to traditional banking which may require extensive verification of cash flows and credit. Despite the speedier process of Sachem’s approvals, it maintains a ~3% foreclosure rate and realizes minimal losses given collateral requirements imposed on clients.

Be the first to comment