It’s time to discuss a dividend growth company I have never covered before. Not noticing Roper Technologies (NYSE:ROP) in the past was a huge mistake as it’s the perfect stock for my portfolio. While I’m going to annoy some dividend investors given that we’re discussing a 0.60% dividend yield, I will explain why that isn’t a dealbreaker. Roper is a fast-growing technology/software-focused industrial giant with high dividend growth and outperforming capital gains. Moreover, the stock has limited volatility, which makes it a fantastic tool for conservative but growth-focused investors. Adding to that, this tech company is currently close to 20% below its all-time high, making it one of its largest sell-off in recent history, and providing investors with the chance to buy quality at a decent price.

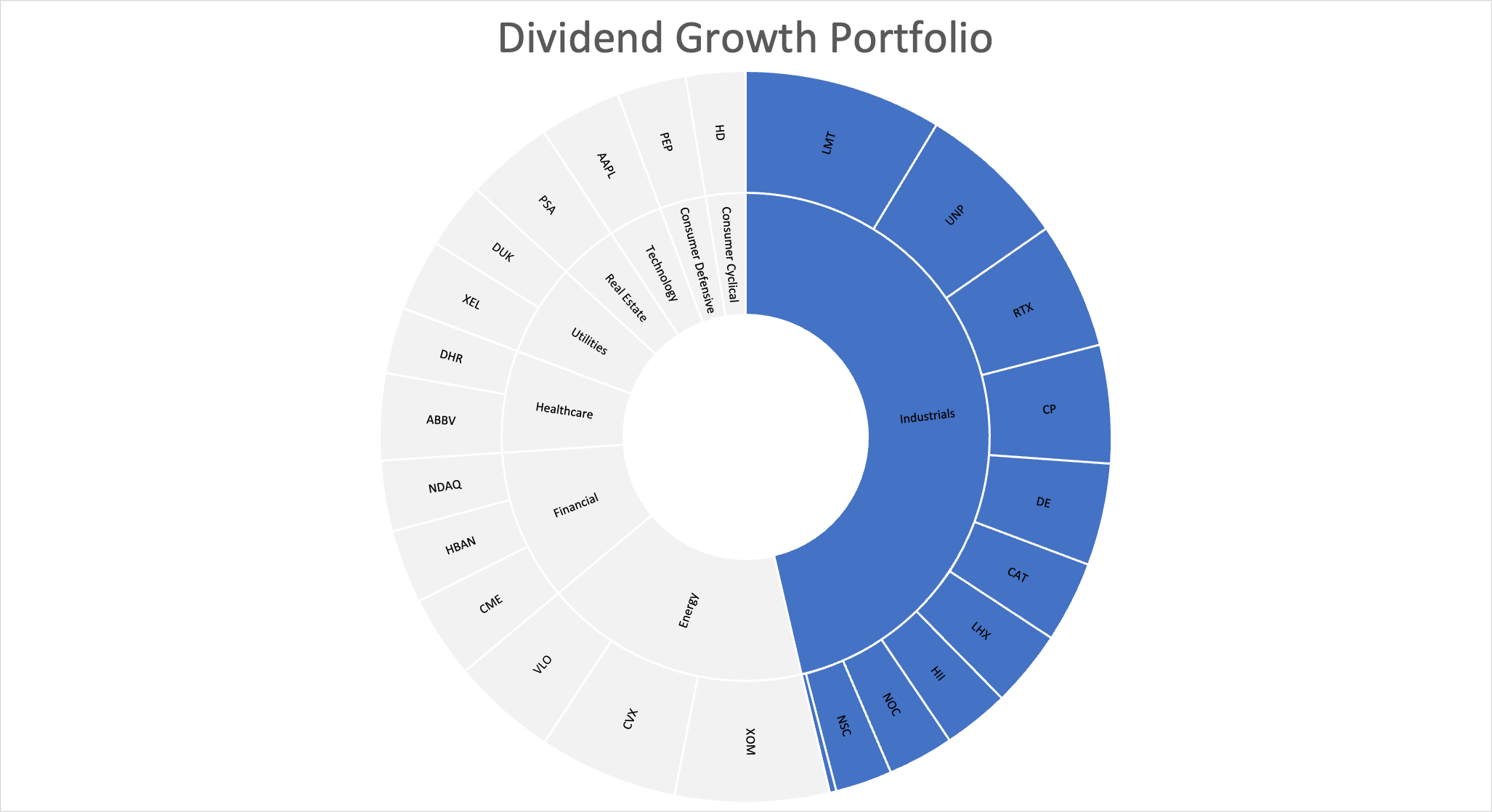

The chart below shows my industrial exposure, which makes looking into this fast-growing industrial stock even more interesting.

Author (Almost 50% industrial exposure)

I will start this article by digging up some research papers I used in the past few weeks/months to build a case for low-yield dividend growth stocks.

So, without further ado, let’s look at the details.

Reasons To Buy Dividend Growth

While I’m highly focused on dividend growth, I do own high-yield stocks. Most of them are in the energy and utility sectors. It’s “fun” to see high dividends hitting our accounts and allows us to reinvest or use it for other purposes.

However, what worries me is not missing out on dividends, but buying stocks that make it impossible for me to beat the market on a long-term basis. While this does not apply to people close to, or in retirement, it does apply to everyone else. After all, I believe that it’s “always” possible to buy a quality high yield. If I wanted to, I could sell all of my dividend growth stocks this week and move my cash into 4-5% yielding stocks. It would give me a good yield, but it sure would limit my upside.

Hence, I believe that “younger” need to own dividend growth as it gives them the possibility to achieve outperforming capital gains that can be turned into higher-yielding investments when the time is right.

In a recent article covering Nasdaq Inc. I brought up a number of research papers and articles that make the case for investments in dividend growth stocks.

Reason one for dividend growth is the fact that historically speaking, dividend growth is the place to be. As I wrote in my Nasdaq article:

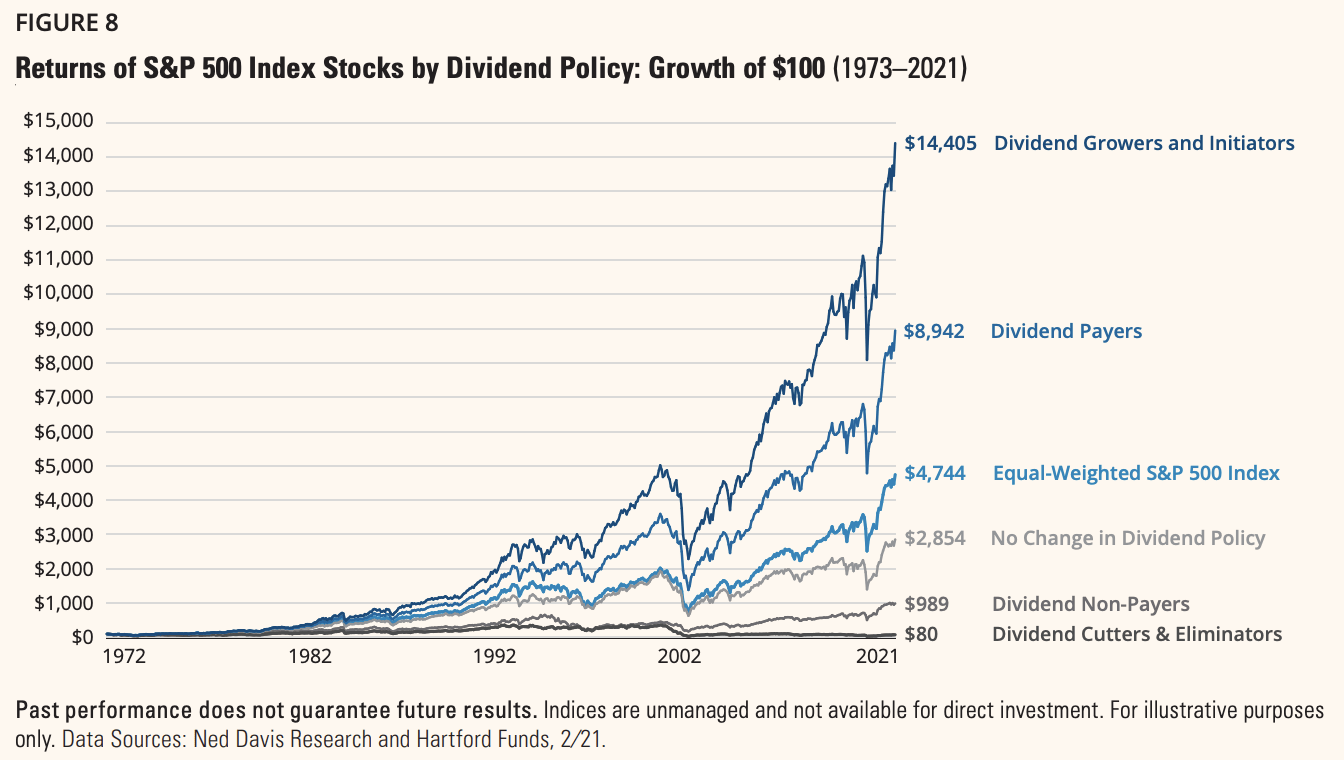

The chart below, for example, has been featured in multiple articles of mine this year. It shows the long-term performance of various dividend categories between 1973 and 2021. What we see is that an equal-weighted S&P 500 investment would have resulted in a $4,655 profit on a $100 investment in 1973. That’s 8.2% per year.

Dividend growers and initiators rose by 10.7% per year. That’s a 250 basis points difference per year, resulting in $10,000 more in profits. On a side note, dividend payers, in general, outperformed the market.

Hartford Funds

That’s nice, but what’s the reason behind this outperformance?

Reason 1 is quality.

A dividend is like a stamp of approval. According to a recent S&P Global report:

Dividend growth stocks tend to be of higher quality than those of the broader market in terms of earnings quality and leverage. Quite simply, when a company is reliably able to boost its dividend for years or even decades, this may suggest it has a certain amount of financial strength and discipline.

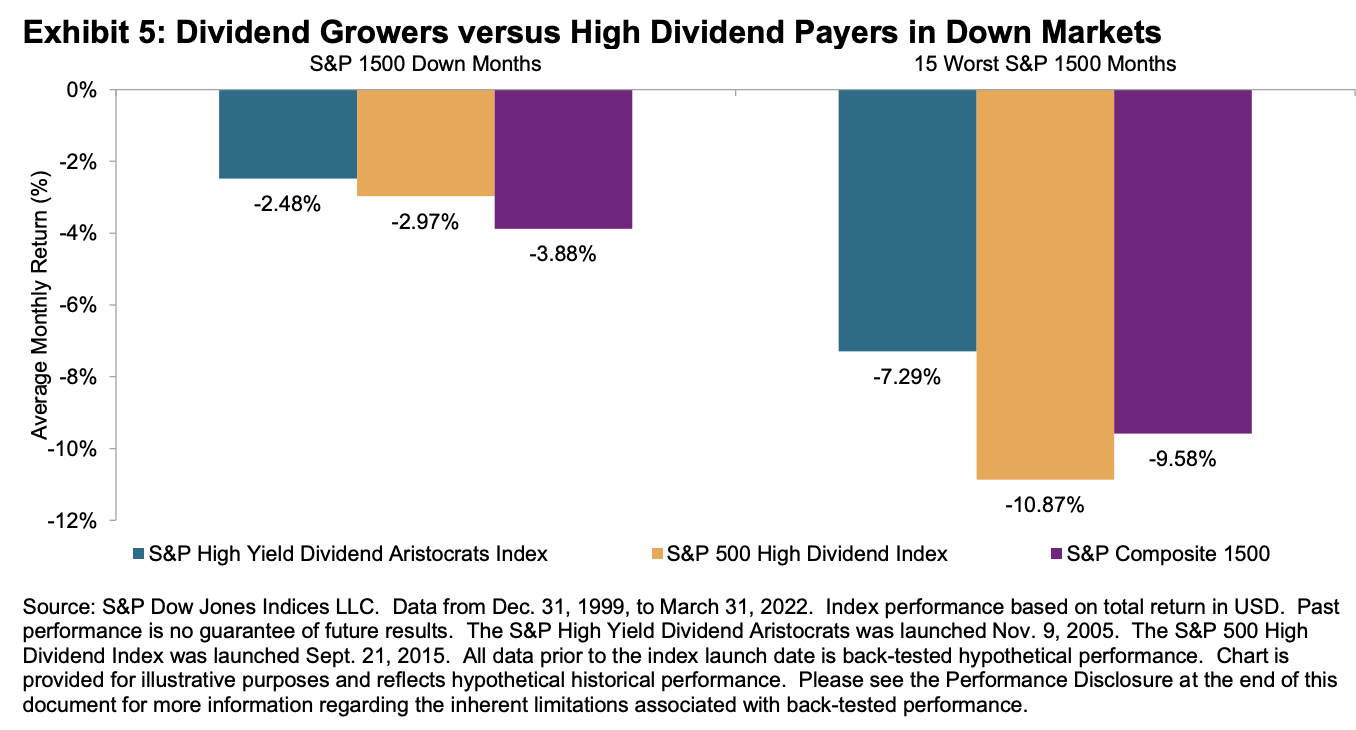

Reason 2 is low volatility (tied to reason number 1). According to the same report:

Dividend growth stocks could be attractive to market participants looking for disciplined companies that can endure difficult market and economic environments relatively well.

[…]

When we focus on the 15 worst-performing months for the S&P 1500 during the same period, the protection provided by the S&P High Yield Dividend Aristocrats was prominent. Its monthly outperformance was 229 bps and 358 bps against the S&P 1500 and S&P 500 High Dividend Index, respectively (see Exhibit 5).

S&P Global

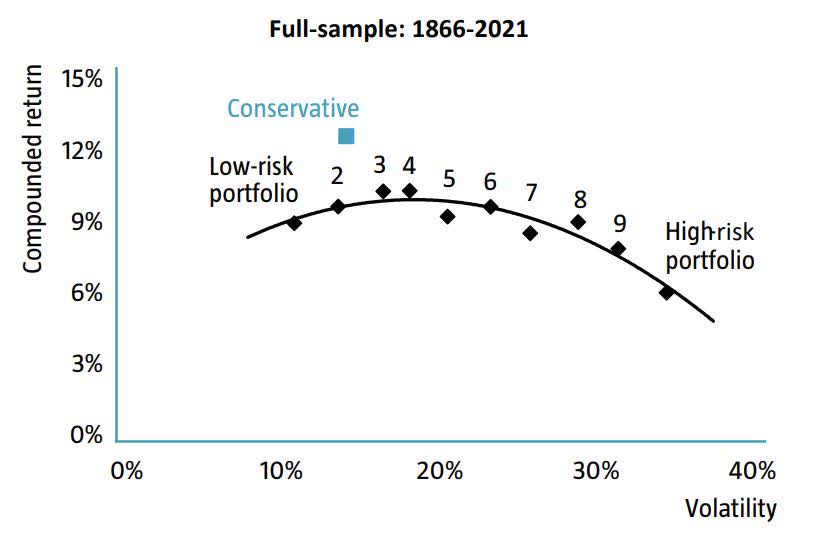

Usually, higher risks need a higher reward. Hence, lower volatility should mean underperformance. Yet, that’s not the case – at all – as shown by a recent ROBECO report. The higher the volatility, the lower the compounded return.

ROBECO

The key here is downside protection. Even if stocks don’t outperform in all bull markets, outperformance during bear markets (limited downside) has a huge impact on long-term results.

To put all things together, I found the chart below (and modified it a bit). Vanguard found that between 1997 and 2016, both high yield and dividend growth stocks outperformed global equities. Moreover, dividend growth outperformed high yield. And, on top of that, dividend growth stocks did it with lower volatility.

Vanguard

In other words, there’s a very strong case for dividend growth stocks, even if the yield is low and somewhat “unattractive” to some.

That’s enough theoretical background for now. Time to look at Roper Technologies.

Why Roper Technologies Is A Fantastic Dividend Growth

With a market cap of $42.4 billion, Roper is the 8th-largest company in the specialty industrial machinery industry.

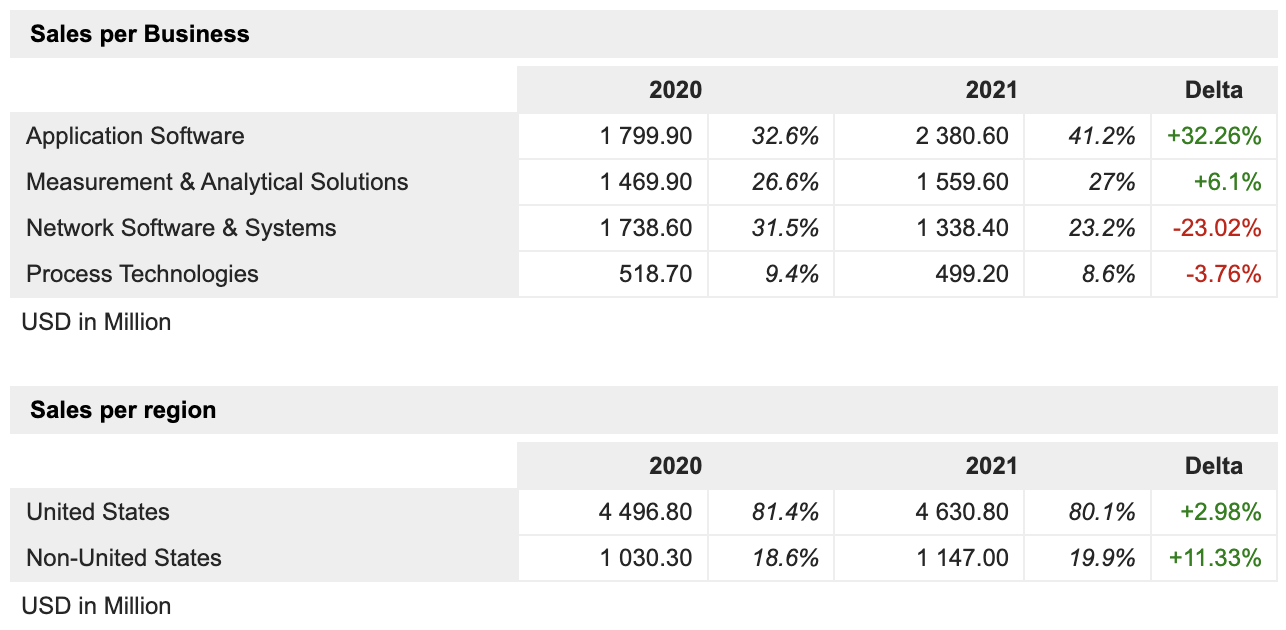

The company has a highly-diversified business model focused on application and network software as well as measurement & analytical solutions and process technologies. Roughly 80% of its sales are generated domestically.

MarketScreener

What’s interesting is that the company’s business description is basically just a big list of its software applications and related services per business segment.

For example, in its application software segment, the company has two solutions called Aderant and CBORD. According to the company:

Aderant – provides comprehensive management software solutions for law and other professional services firms, including business development, calendar/docket matter management, time and billing and case management.

CBORD – provides campus solutions software including access and cashless systems and food and nutrition service management serving primarily higher education and healthcare markets.

The full list can be found in the company’s 10-K starting on page 4.

While this Sarasota, Florida, based company is an industrial firm, it benefits from growth in the service-oriented parts of industrial and related companies. So far, it was in a good spot to deal with supply issues.

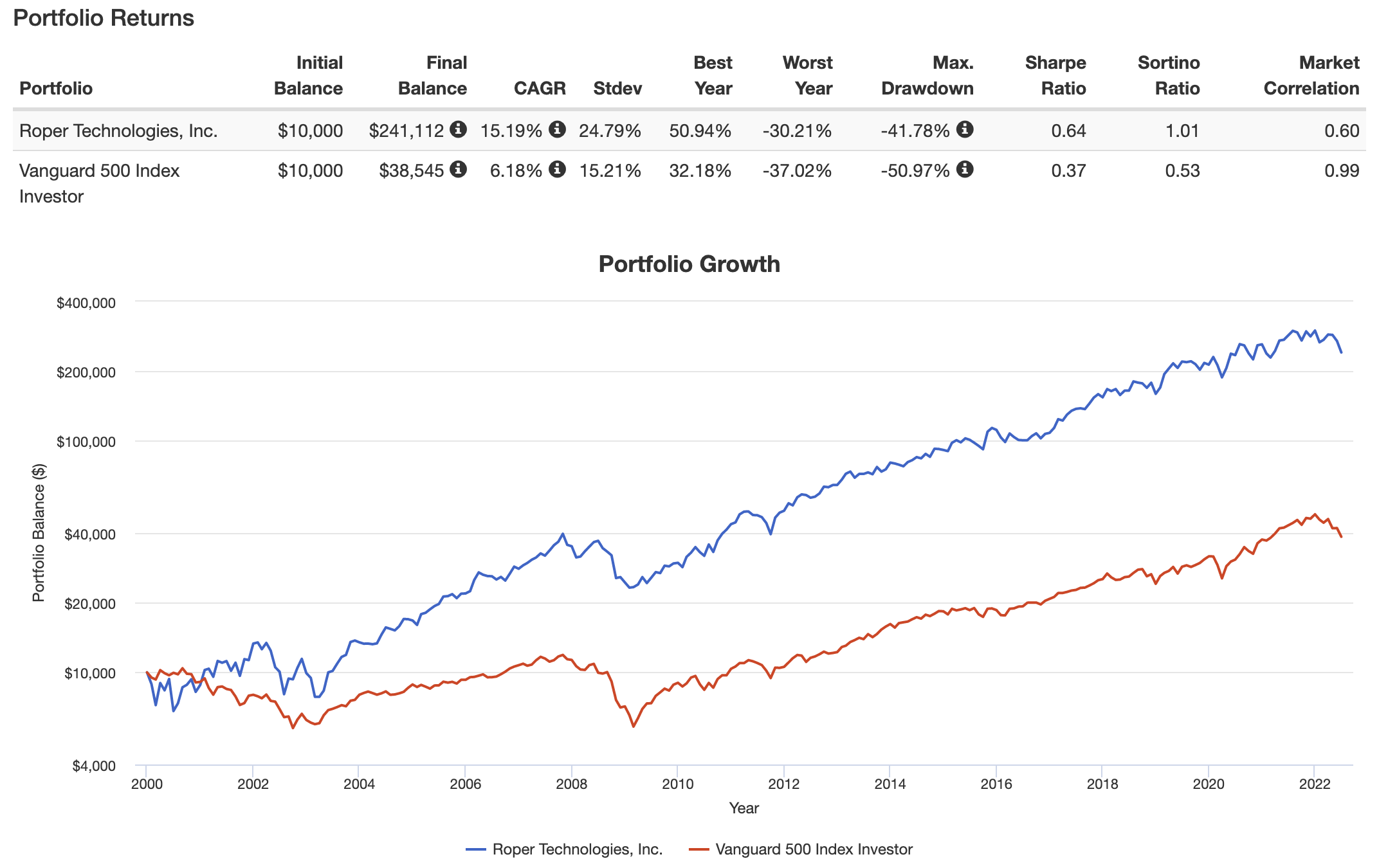

Moreover, the company has a history of low volatility and outperformance. Between 2000 and now, the stock has returned 15.2% per year. The S&P 500 has returned 6.2% during this period. Roper had a standard deviation of 24.8% during this period versus 15.2% for the market. This results in a Sharpe ratio (volatility-adjusted performance) of 0.64 versus 0.37.

Portfolio Visualizer

In other words, while we haven’t talked about growth rates or dividends, we can say that volatility-adjusted outperformance is indeed what happened. Note that the chart above starts in 2000. If we go back to 1993, the annual return rises to 19.9%.

With that said, the company’s focus on industrial services has resulted in high growth. Over the past 5 years, revenue has grown by 8.3% per year. This includes the pandemic. Thanks to higher margins, the company has grown EBITDA by roughly 11%.

TIKR.com/Seeking Alpha

Moreover, free cash flow growth is impressive. Between 2015 and 2024E, free cash flow has grown by 11.1% CAGR.

Free cash flow is net income adjusted for non-cash operating items and capital expenditures. It’s cash a company can distribute to shareholders or use to strengthen its balance sheet.

When it comes to Roper’s balance sheet health, the company ended last year with $7.6 billion in net debt. That was roughly 3.4x EBITDA. This year, the company is expected to lower this number to $4.2 billion, or 1.7x EBITDA. In 2024, net debt could be at $1.0 billion, or barely 0.3x EBITDA.

However, these numbers are based on current debt and free cash flow used to reduce debt. It excludes future M&A as analysts cannot predict when Roper will acquire a new company.

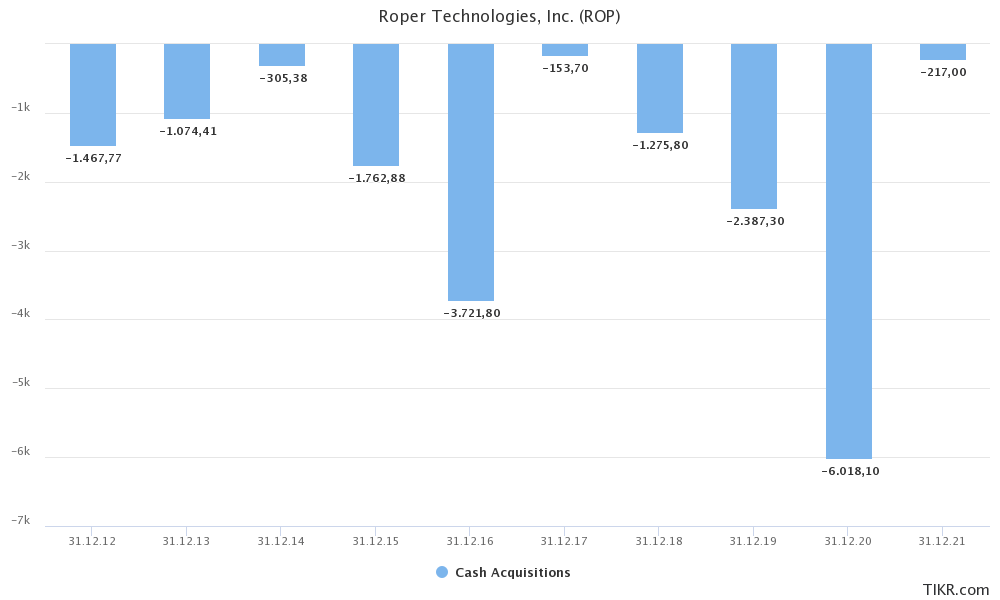

Roper has a rich history of adding acquired growth. This is common for companies with big diversified portfolios. It’s highly unusual that these services and products are all coming from organic growth.

TIKR.com

The big negative bar in 2020 is cash outflow as a result of the Vertafore acquisition. This cost the company $5.35 billion and added insurance software to its portfolio.

As a matter of fact, the company is now so technology-oriented that it changed its name from Roper Industries to Roper Technologies in 2015, which I believe is a smart move as it fits the company much better.

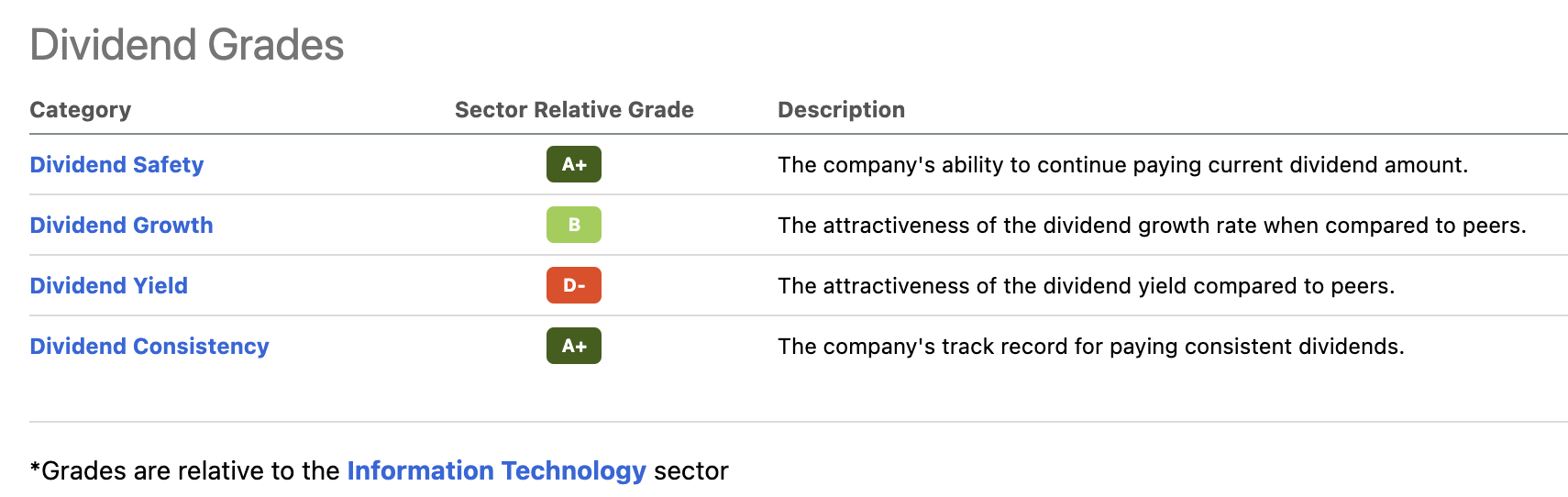

Anyway, there’s some downside for income-oriented investors when it comes to Rope’s business. There is no focus on dividends or buybacks – yet.

Roper Technologies is paying a $0.62 quarterly dividend per share. That’s $2.48 per year and 0.60% per share. This explains the big far D minus in the dividend scorecard below.

Seeking Alpha

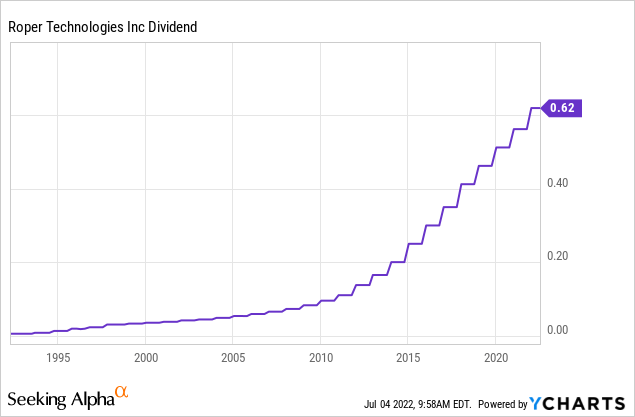

The good news is that the low dividend yield is not the company’s fault. On a 10-year basis, the average annual dividend growth rate is 16.9%. On a three-year basis, that number is still 10.6%. It’s investors who are to blame as capital gains have been almost equal to dividend growth. This resulted in extremely high total returns as I explained in this article. The bad news is that income-oriented investors won’t like this company.

Data by YCharts

With that said, the valuation has also “never” really been cheap as investors always priced in high growth. It helps that the stock market is now in bear market territory.

ROP Stock Valuation

Roper is 18% below its all-time high. This makes it one of the worst sell-offs in recent history based on monthly closing prices (hence, the 2020 sell-off doesn’t look so bad).

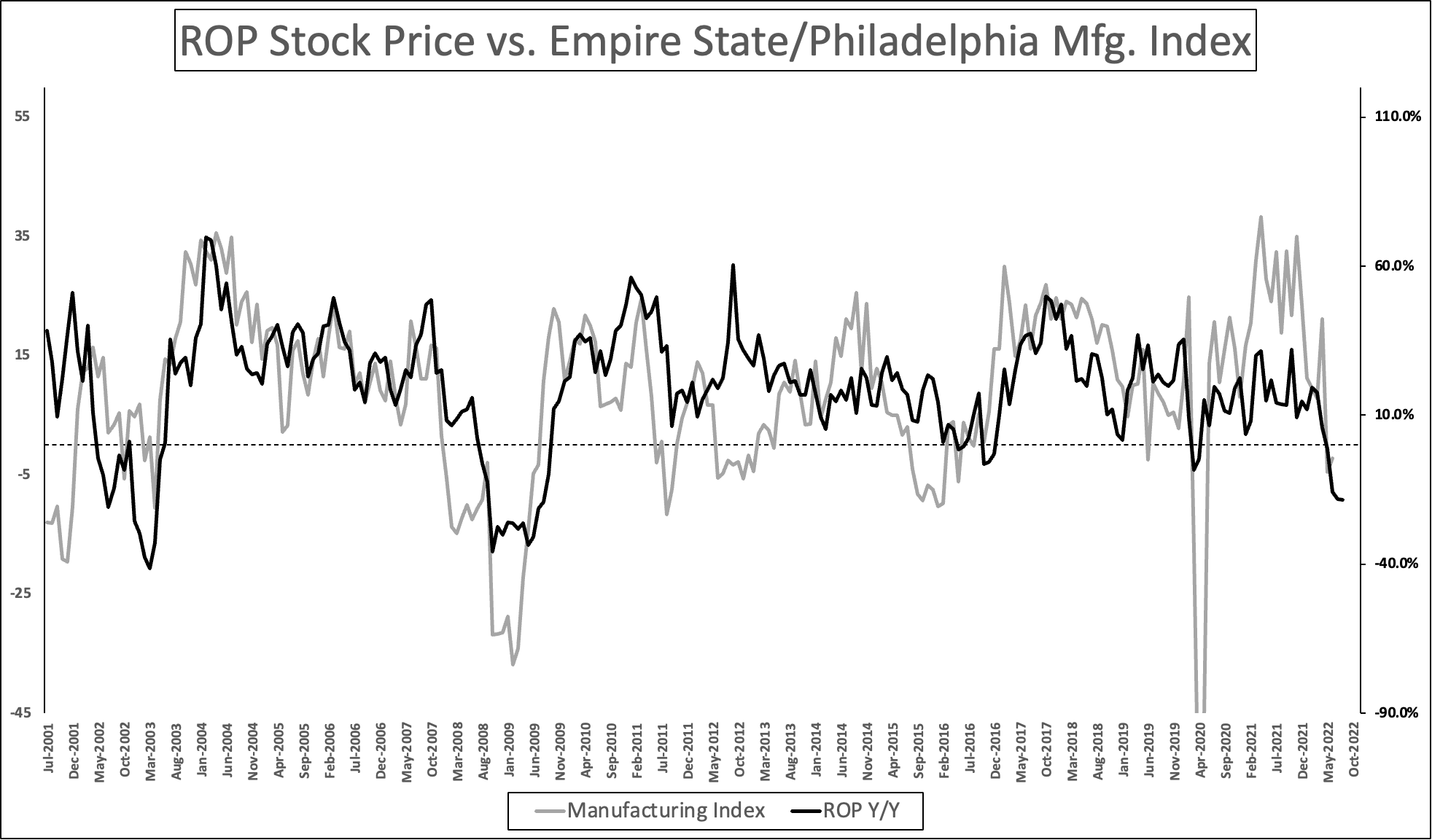

The chart below displays two things:

ROP is highly cyclical. The company is service-oriented, but still dependent on companies’ willingness to boost CapEx and related investments.

Because it’s service-oriented, drawdowns during manufacturing recessions are extremely limited. I.e., the 2014/2015 manufacturing recession was extremely mild on ROP investors.

Author

Right now, we’re once again in a situation where a recession is being priced in. It’s not a lot of fun for existing positions, but it allows investors to buy quality stocks at good prices.

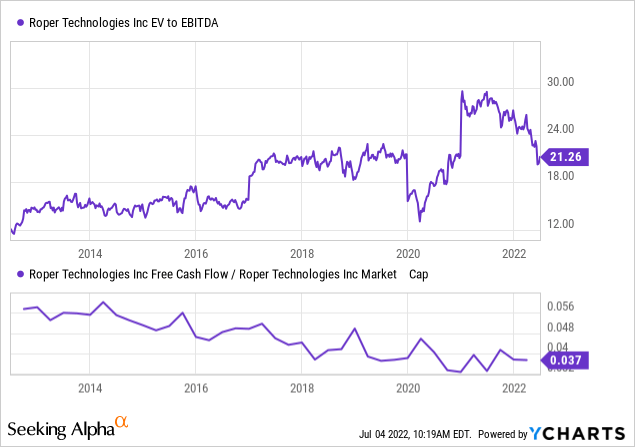

In the case of ROP, we’re dealing with a 17.5x 2023 EBITDA multiple (EV/EBITDA). This is based on the company’s $42.4 billion market cap, $2.7 billion in expected net debt, and $2.6 billion in expected EBITDA.

The implied 2023 free cash flow yield is 5.0%, which is one of the highest in recent history and an indication that there’s cash to support and grow the dividend, reduce debt, and engage in new acquisitions.

17.5x 2023 EBITDA isn’t cheap either, but it’s now in line with pre-pandemic valuations incorporating high net income growth backed by acquisitions. That’s a fair valuation – but not deep value.

Data by YCharts

Takeaway

Roper Technologies is a stock that fits my overall strategy. The company has an interesting business model, offering diversified services and solutions for industrial and industrial clients.

While its dividend yield is extremely low, investors are in a good place. Free cash flow generation is high and growth rates are strong. The company is able to use acquired growth to rapidly fuel sales and net income growth, leading to further free cash flow.

This is keeping the balance sheet from being damaged by high debt. It’s truly a fantastic business model and management is doing a terrific job turning ROP into a technology-focused company.

Going forward, I expect dividend growth to remain very strong leading to outperforming capital gains with limited downside during (manufacturing) recessions.

The current stock price is looking good thanks to the 18% sell-off.

Investors interested in buying ROP should buy in intervals to incorporate high market uncertainty and economic risks. For example, buying 25% now and adding over time allows investors to average down if the market keeps falling. If the stock suddenly takes off, investors have a foot in the door.

Other than that, I think ROP is a great long-term stock and I’m looking for ways to incorporate the company into my portfolio.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment