ChristianNasca/E+ via Getty Images

Intro

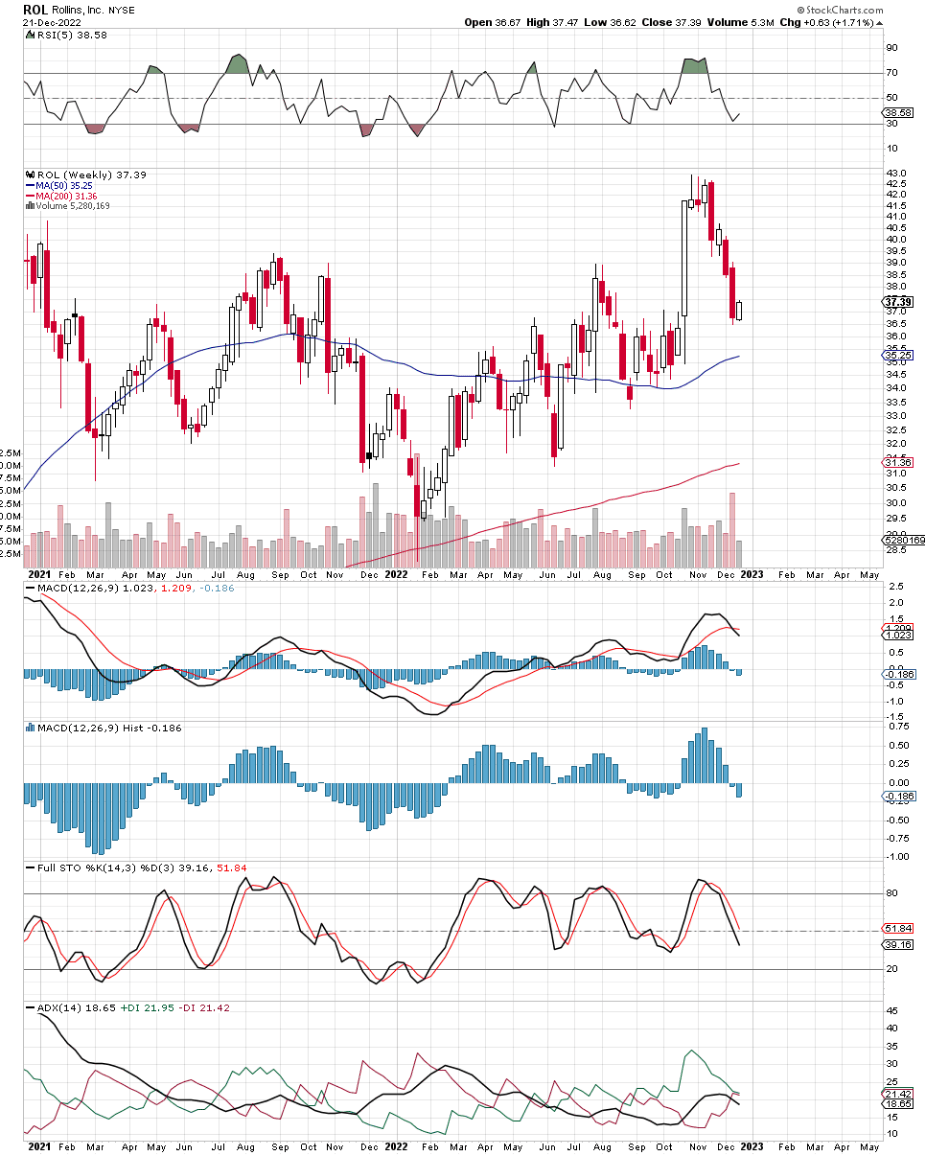

If we pull up an intermediate 2-year chart of Rollins, Inc. (NYSE:ROL), we can see that shares have been undergoing a steep decline in recent weeks. The down move may be noteworthy as the strongest trending moves in either direction take place from either market highs or lows. Therefore, it is imperative that shares regain stability here over the near term to keep a potential aggressive down move at bay. As we can see from the popular ADX trend following technical indicator, shares are very close to giving an intermediate sell signal which is worrying in itself. Suffice it to say, bulls will be hoping the stock’s recent December lows can hold here so sentiment can be reset somewhat going forward.

In saying the above, Rollins reported a convincing earnings beat in its recent third quarter on organic sales growth of almost 9%. EBITDA, earnings per share as well as operating cash flow all grew compared to the same period of 12 months prior. The encouraging aspect of the report was the organic sales growth rate which was driven particularly by the Termite & Commercial segments in the quarter.

Suffice it to say, given the strong growth we witnessed across all three of Rollins’ segments in Q3 where retention rates remained buoyant, it is bewildering to see that shares remain well down since that Q3 earnings print. Therefore, let’s see where things stand with Rollins at present. As always, it is the relationship between the stock’s profitability & valuation trends that can give us insights into whether Rollins remains overvalued at this juncture.

Rollins’ Technical Chart (Stockcharts.com)

Profitability

First off, Rollins’ net income comes in at $345.7 million over the past four quarters. This figure is actually down from the fiscal 2021 bottom-line figure which came in at $350.7 million. The culprit from the drop-off in bottom-line growth thus far this year is the first quarter, which reported a net profit tally of $72.4 million ($20+ million decline over Q1 of 2021).

However, earnings growth is not the only way to gauge profitability. Operating cash flow, for example, over a trailing twelve-month average comes in at a very healthy $445.4 million (10.8%+ increase over the same metric in fiscal 2021). Furthermore, Rollins’ high free cash flow is not being generated to the detriment of the balance sheet, which is particularly impressive given the number of acquisitions Rollins goes through per year (27 in total year to date). Shareholder equity continues to increase on the balance sheet and the company remains in a favorable position regarding its debt position.

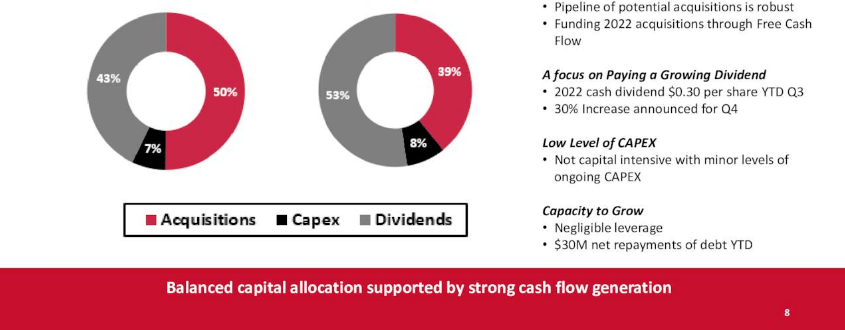

As we see below, Rollins is using its cash to compensate shareholders through dividends, acquire more companies, and for capital investment purposes. The low CAPEX investment is another strong calling card in this stock in that capital investment does not need to be elevated in order for free cash flow to keep growing meaningfully. This is a big advantage that enables companies to continue to scale.

Rollins’ Capital Allocation Breakdown (Seeking Alpha)

Valuation

Despite Rollins’ prowess in consistently generating more cash flow off the earnings the company generates, the stock’s forward cash-flow multiple still comes in at a lofty 39.3. Furthermore, Rollins’ forward sales multiple comes in at 6.84 whereas the trailing book multiple comes in at 15.39. Suffice it to say, although Rollins’ 5-year average sales multiple of 6.79 demonstrates that the company’s sales are no more expensive than what we have been used to, the company’s assets and earnings are both 12%+ more expensive over their 5-year respective multiples.

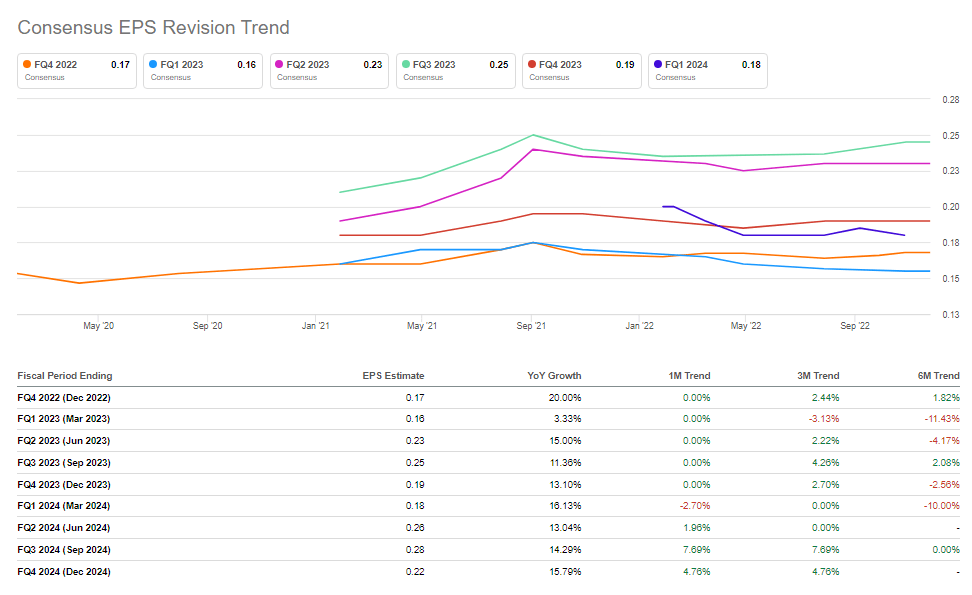

In saying this, it is not Rollins’ fault that the market continues to love this stock. Although bottom-line growth is expected to come in a tad softer this year (8% – which is an excellent result considering the negative growth in the first quarter), Rollins is expected to deliver up to 13% bottom-line growth in fiscal 2023, which is right in line with the growth we expect from this stock. Near-term earnings revisions have been encouraging also, which is not surprising really considering how the company always seems able to produce growth even in periods of economic contractions.

ROL Consensus Earnings Revisions (Seeking Alpha)

Conclusion

Therefore, to sum up, given Rollins’ expected return to strong double-digit earnings growth next year, this stock is not a potential short even if the present down move continues to gain traction. Hopefully, shares will drop far enough to reset the stock’s valuation to a level we would be interested in on the long side. We look forward to continued coverage.

Be the first to comment